Resources

About Us

Hot Water Boilers Market by Fuel Type (Gas-fired, Oil-fired, Electric, Biomass-fired), Technology (Condensing, Non-condensing), Design (Fire-tube, Water-tube), Capacity (Low Capacity, Medium Capacity, High Capacity), and End-use Vertical - Global Forecast to 2036

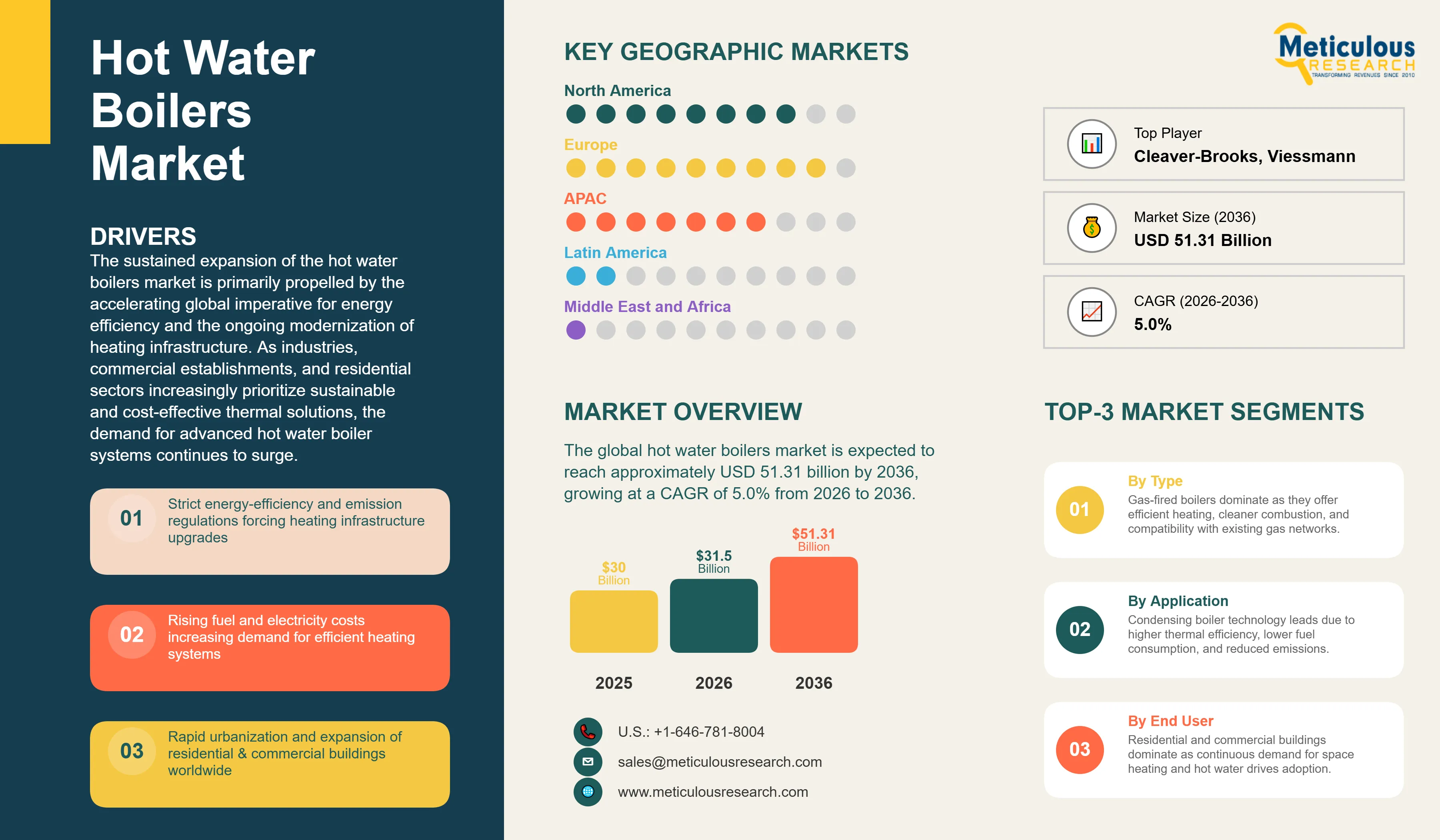

Report ID: MRSE - 1041820 Pages: 277 Mar-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global hot water boilers market was valued at USD 30.0 billion in 2025. The market is expected to reach approximately USD 51.31 billion by 2036 from USD 31.5 billion in 2026, growing at a CAGR of 5.0% from 2026 to 2036. The sustained expansion of the hot water boilers market is primarily propelled by the accelerating global imperative for energy efficiency and the ongoing modernization of heating infrastructure. As industries, commercial establishments, and residential sectors increasingly prioritize sustainable and cost-effective thermal solutions, the demand for advanced hot water boiler systems continues to surge. Key drivers include stringent environmental regulations, escalating energy costs, and the rapid growth of urban and industrial infrastructures worldwide. Furthermore, the integration of smart technologies and the expansion of district heating networks are creating new avenues for market growth, positioning modern hot water boilers as indispensable components for optimized thermal management.

Click here to: Get Free Sample Pages of this Report

Hot water boilers stand as a cornerstone of modern thermal management, seamlessly integrating efficient heat generation with reliable water circulation within a unified system. These sophisticated platforms are engineered with high-performance heat exchangers, advanced combustion mechanisms, and intelligent control systems that dynamically regulate heat delivery. Their operation is precisely calibrated to meet real-time demand, adapt to ambient conditions, and achieve optimal operational efficiency. The market is currently undergoing a profound transformation, moving away from outdated, hardware-centric systems towards integrated, high-efficiency platforms. These contemporary solutions are often cloud-enabled, ensuring consistent and optimized thermal energy distribution across diverse environments, from individual residences to expansive commercial complexes and demanding industrial facilities.

Modern hot water boiler architectures encompass a broad spectrum of designs, ranging from compact, wall-mounted units ideal for residential use to large-scale industrial boiler plants that can effectively replace entire legacy heating infrastructures. A notable trend is the increasing integration of artificial intelligence (AI) and machine learning (ML) capabilities. These advanced features enable autonomous combustion optimization, dynamic adjustment of thermal output based on occupancy or process requirements, and proactive maintenance management across distributed systems. The ability to deliver precise temperature control, granular energy consumption tracking, and continuous performance monitoring through a single digital interface has cemented the position of modern hot water boiler technology as the preferred choice for organizations seeking both operational agility and thermal resilience.

The global thermal energy landscape is in the midst of a significant paradigm shift, driven by a confluence of factors including sustainability mandates, persistent energy efficiency regulations, and volatile fuel prices. This shift has accelerated the decommissioning of traditional non-condensing infrastructure and older, less efficient units. Consequently, organizations are increasingly prioritizing unified boiler platforms that can ensure compliance with emission standards, automate incident response, and maintain regulatory adherence across geographically dispersed operations. The burgeoning growth in sustainable building initiatives, the expansion of district energy systems, and the development of hydrogen-ready boiler designs are further solidifying the role of hot water boilers as a fundamental thermal architecture for the evolving industrial and commercial ecosystem.

Rise of AI-Integrated Boiler Platforms and Autonomous Thermal Optimization

The hot water boiler landscape is experiencing a significant evolution, as leading manufacturers are now embedding AI and machine learning capabilities directly into their core platform architectures, moving beyond mere optional add-ons. For instance, Bosch’s latest industrial boiler series incorporates AI-driven performance management that continuously monitors system health and thermal efficiency across all circulation paths. This intelligence allows for automatic identification and resolution of issues before they can impact facility comfort or process productivity. Similarly, Viessmann’s digital ecosystem leverages real-time analysis of usage patterns and ambient weather data to generate precise thermal profiles, triggering automated setpoint adjustments without human intervention. This intelligence-led approach is transforming the boiler from a passive heating component into an active, self-optimizing thermal fabric capable of predicting and neutralizing inefficiencies. As AI capabilities become a primary differentiator, vendors that integrate autonomous detection, optimization, and response workflows into their boiler stacks are gaining a measurable competitive edge.

Convergence Toward High-Efficiency Condensing Units and the Decline of Non-Condensing Patchwork Architectures

Enterprise buyers are increasingly moving away from mixed-technology and non-condensing boiler solutions, opting instead for fully converged, high-efficiency condensing platforms. These systems offer superior thermal recovery and reduced emissions, all managed through a single, unified console. The complexities, maintenance overheads, and integration challenges associated with combining disparate legacy heating products from various vendors have become unsustainable, especially as enterprise environments become more distributed and energy-conscious. Cleaver-Brooks has been at the forefront of this trend, offering fully integrated boiler systems supported by a global network, providing commercial facilities and industrial plants with a consistent thermal experience managed from a single interface. A.O. Smith has further reinforced this by consolidating its high-efficiency offerings under a unified digital platform, delivering optimized water heating and AI-powered system protection. Industry projections indicate that by 2028, a substantial majority of commercial boiler purchases will be for high-efficiency condensing platforms, a trajectory that is fundamentally reshaping competitive dynamics and procurement strategies across the market.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 51.31 Billion |

|

Market Size in 2026 |

USD 31.5 Billion |

|

Market Size in 2025 |

USD 30.0 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 5.0% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Fuel Type, Technology, Design, Capacity, End-use Vertical, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Accelerating Shift to Energy-Efficient and Sustainable Building Architectures

The global hot water boilers market is primarily driven by the intensifying mandate for energy efficiency and sustainable building operations. As governments worldwide implement rigorous carbon reduction targets and building codes, organizations are compelled to modernize their heating infrastructure. The transition from legacy, high-emission boilers to advanced condensing and electric systems is no longer a discretionary upgrade but a strategic necessity for regulatory compliance and operational cost management. This driver is particularly potent in developed markets where the “Renovation Wave” is transforming the existing building stock into low-carbon environments.

Opportunity: Expansion of Smart District Heating and Industrial Electrification

A significant growth opportunity lies in the rapid expansion of smart district heating networks and the increasing electrification of industrial thermal processes. District heating offers a highly efficient model for urban heat distribution, and the integration of large-scale hot water boiler plants into these networks is a major growth avenue. Simultaneously, the push for industrial decarbonization is creating a surge in demand for high-capacity electric boilers that can leverage renewable energy sources. Manufacturers that can provide modular, hydrogen-ready, and fully electric boiler solutions are exceptionally well-positioned to lead the next phase of the global thermal energy transition.

How is Europe Maintaining Dominance in the Global Hot Water Boilers Market?

Europe holds the largest share of the global hot water boilers market in 2026. This dominance is primarily attributable to the region’s high concentration of leading boiler manufacturers, mature energy efficiency awareness, and strong regulatory impetus driving the adoption of condensing technology across both public and private sectors. The European Union alone accounts for the majority of regional revenue, with mandates like the EcoDesign Directive and the Energy Performance of Buildings Directive (EPBD) accelerating procurement timelines across residential and commercial sectors. The presence of established vendors including Bosch, Viessmann, and Vaillant, alongside a well-developed channel of specialized installers and system integrators, provides European enterprises with robust access to mature, fully supported boiler deployments.

Which Factors Support Asia-Pacific and North America Market Growth?

Asia-Pacific is the fastest-growing regional market for hot water boilers during the forecast period, driven by rapid urbanization across China, India, Southeast Asia, and Japan. The region’s massive and rapidly digitizing industrial base, combined with growing awareness of sustainable heating and evolving environmental regulations, is creating strong demand for high-efficiency boiler platforms that can scale with the pace of economic development. Governments across the region are also actively promoting cleaner heating frameworks aligned with global climate goals, further accelerating enterprise adoption.

North America represents a substantial and steadily growing share of the global market, shaped by the continent’s stringent emission standards and the increasing focus on smart building technologies. The regulatory requirement for high-efficiency systems in new constructions and the ability to enforce strict energy codes at the state and federal levels are driving North American enterprises to prioritize advanced boiler vendors with locally distributed support networks. The United States and Canada are among the most active adoption markets, supported by a mature commercial HVAC landscape and a well-developed ecosystem of regional thermal energy service providers.

Companies such as Bosch Thermotechnik GmbH, Viessmann Group, Cleaver-Brooks, Inc., A.O. Smith Corporation, Vaillant Group, Ariston Group, BDR Thermea Group, Ferroli S.p.A., Weil-McLain, Lochinvar, LLC, Rheem Manufacturing Company, Navien, Inc., Hurst Boiler & Welding Co., Inc., and Fulton Thermal Corporation lead the global hot water boilers market with comprehensive, fully converged platforms that integrate advanced combustion, condensing technology, and smart digital controls under unified management consoles. These players offer a diverse range of solution architectures, from compact residential units to high-capacity industrial boiler plants, catering to various infrastructure preferences and existing vendor relationships. Their innovations in AI-driven efficiency monitoring, managed thermal delivery, and purpose-built offerings for diverse commercial and industrial environments are strengthening their market positions.

The global hot water boilers market is expected to grow from USD 31.5 billion in 2026 to USD 51.31 billion by 2036.

The global hot water boilers market is projected to grow at a CAGR of 5.0% from 2026 to 2036.

The gas-fired segment is expected to dominate the market in 2026 due to its superior ability to address immediate efficiency requirements through integrated condensing technology. The electric segment is projected to accelerate its growth as enterprises consolidate their sustainability and electrification strategies under unified boiler platforms.

AI is transforming the market by enabling platforms to move beyond passive heating toward autonomous efficiency optimization, dynamic load adjustment, and predictive performance management. Leading vendors are embedding machine learning-driven combustion analytics and automated incident response directly into their core architectures, enabling enterprises to significantly reduce operational costs while minimizing reliance on manual maintenance workflows.

Europe holds the largest share of the global market in 2026. The region’s dominance is primarily driven by the high concentration of leading solution providers, strong regional energy efficiency mandates, and mature enterprise adoption of advanced condensing boiler architectures.

The leading companies include Bosch Thermotechnik, Viessmann Group, Cleaver-Brooks, A.O. Smith, Vaillant Group, Ariston Group, BDR Thermea Group, Ferroli S.p.A., Weil-McLain, Lochinvar, LLC, Rheem Manufacturing Company, Navien, Inc., Hurst Boiler & Welding Co., Inc., and Fulton Thermal Corporation.

Published Date: Aug-2025

Published Date: Jan-2025

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates