Resources

About Us

Heating Cables Market by Type (Self-regulating, Constant Wattage, Mineral Insulated), Application (Freeze Protection, Floor Heating, Roof & Gutter De-icing, Process Temperature Maintenance), End-User (Residential, Commercial, Industrial), Voltage Rating (Low Voltage, Medium Voltage) -- Global Forecast to 2036

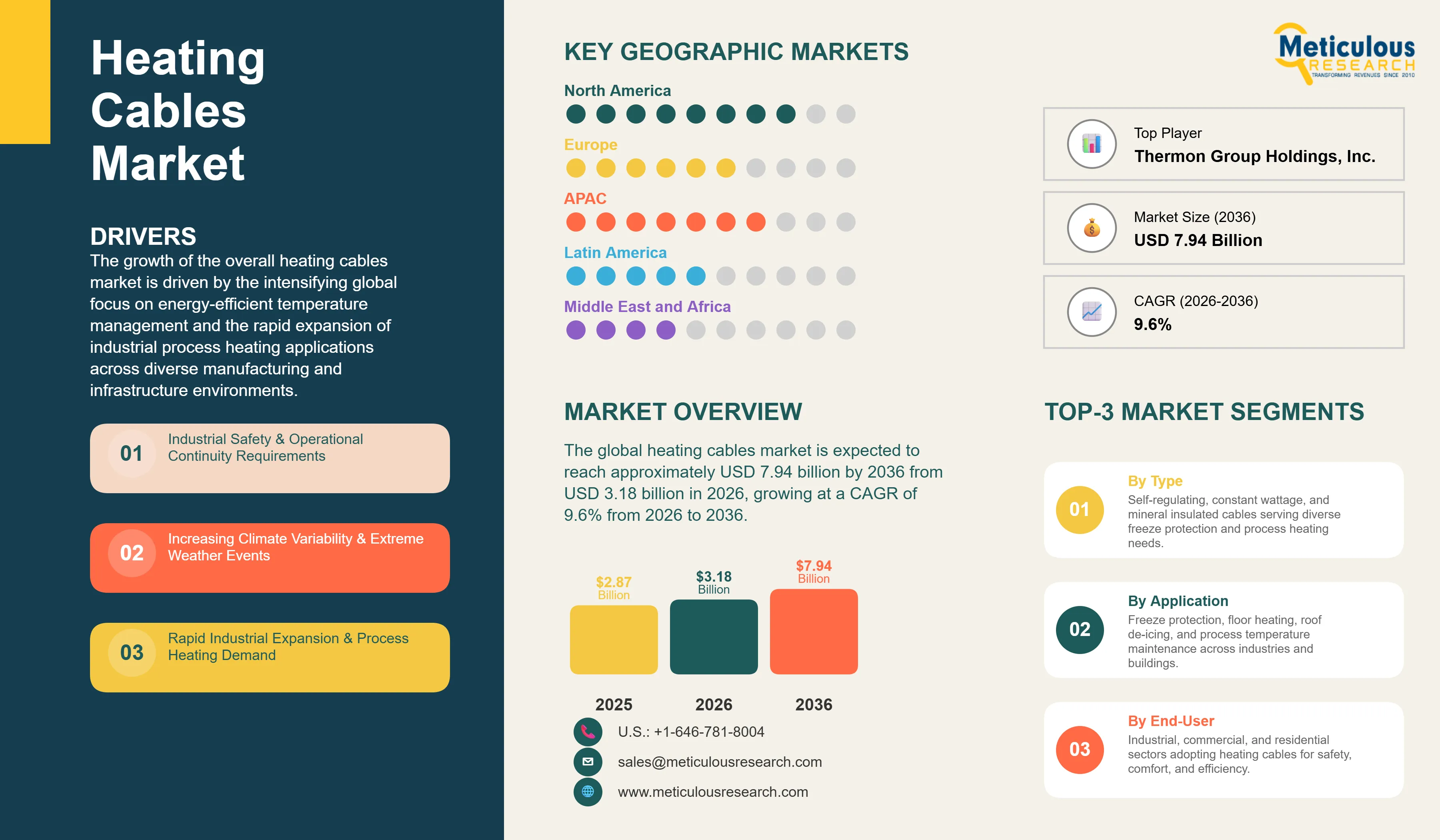

Report ID: MRSE - 1041817 Pages: 262 Mar-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global heating cables market was valued at USD 2.87 billion in 2025. The market is expected to reach approximately USD 7.94 billion by 2036 from USD 3.18 billion in 2026, growing at a CAGR of 9.6% from 2026 to 2036. The growth of the overall heating cables market is driven by the intensifying global focus on energy-efficient temperature management and the rapid expansion of industrial process heating applications across diverse manufacturing and infrastructure environments. As enterprises seek to integrate more reliability into their freeze protection systems and address the increasing demand for precise temperature control in harsh climate conditions, advanced heating cable solutions have become essential for maintaining operational continuity and safety standards. The rapid expansion of smart building technologies and the increasing need for automated thermal management in residential floor heating and commercial pipe protection continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Heating cables represent critical electric heating systems designed to provide controlled thermal energy for temperature maintenance, freeze protection, and comfort heating applications across industrial, commercial, and residential environments. These systems include self-regulating cables that automatically adjust heat output based on ambient temperature, constant wattage cables providing uniform heating for process applications, and mineral-insulated cables offering high-temperature capabilities exceeding 600°C for specialized industrial requirements. The market is defined by advanced technologies such as fluoropolymer insulation materials, digital temperature control systems, and IoT-enabled monitoring platforms, which significantly enhance energy efficiency and operational reliability in demanding thermal management applications. These systems are indispensable for facility managers and process engineers seeking to prevent costly freeze damage, maintain optimal viscosity in process fluids, and ensure safety-critical temperature control in hazardous area installations.

The market encompasses diverse heating cable configurations ranging from simple roof de-icing cables for residential snow melting to complex heat-traced pipeline systems extending hundreds of kilometers across industrial complexes. Modern installations increasingly integrate smart control systems featuring RTD temperature sensors, programmable logic controllers, and wireless monitoring capabilities enabling predictive maintenance and energy optimization. The evolution from basic resistance heating toward intelligent self-regulating technology has transformed heating cable applications, with polymer-based temperature-responsive conductors automatically modulating power output across their entire length—delivering maximum heat where coldest while reducing energy consumption up to 60% compared to constant wattage alternatives in variable ambient conditions.

The global infrastructure sector faces mounting pressure to maintain operational reliability while improving energy efficiency, particularly as climate variability increases freeze-thaw cycle frequency in traditionally temperate regions. This dynamic drives heating cable adoption beyond conventional cold-climate markets, with temperate zone industries implementing freeze protection systems to mitigate risk from increasingly unpredictable weather patterns. Simultaneously, building electrification trends and heat pump proliferation create synergies with electric floor heating systems, as low-temperature hydronic distribution naturally complements radiant heating delivery, positioning heating cables as complementary technology in decarbonization strategies replacing combustion-based space heating with efficient electric alternatives integrated with renewable energy systems.

Proliferation of Smart Heating Systems and IoT Integration

Manufacturers across the heating cables industry are rapidly integrating digital technologies, moving beyond traditional thermostatic controls toward networked monitoring and predictive maintenance platforms. nVent's latest Raychem TraceTek systems deliver significantly enhanced fault detection capabilities through continuous impedance monitoring, while Thermon's QuEST wireless monitoring enables real-time energy consumption tracking across distributed heat trace installations. The transformation comes with cloud-connected control systems providing building-wide or facility-wide thermal management optimization, automatically adjusting heating output based on weather forecasts, occupancy patterns, and time-of-use electricity rates. These advancements make sophisticated energy management practical for applications ranging from residential floor heating responding to home automation commands to industrial installations optimizing power consumption across hundreds of heat-traced circuits, reducing operating costs 20-40% through intelligent control algorithms impossible with conventional thermostatic systems.

Innovation in High-Performance Materials and Hazardous Area Solutions

Material science advances are driving heating cable performance improvements addressing increasingly stringent industry requirements. Fluoropolymer insulation systems enable operation in corrosive chemical environments that would degrade conventional materials, while advanced polymer conductor technology extends self-regulating cable maximum exposure temperatures from 65°C to 85°C and beyond, expanding addressable applications. These developments prove critical for oil & gas sector applications where heating cables must maintain certification for explosive atmosphere installations (ATEX, IECEx) while withstanding mechanical stress from pipeline thermal expansion, UV degradation in outdoor installations, and chemical exposure from process fluids—requirements driving specification of premium cable constructions and specialized installation accessories.

Concurrently, sustainability considerations are reshaping product development priorities, with manufacturers emphasizing recyclable materials, reduced installation waste through precise cable length optimization, and extended service life minimizing replacement frequency. Energy efficiency certifications become standard requirements, particularly in European markets where ErP directives and building energy codes mandate minimum system efficiencies for electric heating applications. The convergence of performance enhancement and environmental responsibility creates differentiation opportunities for manufacturers demonstrating verifiable sustainability credentials—recycled content in cable jackets, take-back programs for end-of-life materials, and transparent lifecycle assessment data—increasingly influencing procurement decisions as corporate ESG commitments cascade through supply chains into component-level specifications.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 7.94 Billion |

|

Market Size in 2026 |

USD 3.18 Billion |

|

Market Size in 2025 |

USD 2.87 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 9.6% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Application, End-User, Voltage Rating, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Industrial Safety Requirements and Climate Variability

A key driver of the heating cables market is the stringent industrial safety and operational continuity requirements across process industries where temperature control directly impacts production uptime and personnel safety. Oil and gas facilities face catastrophic consequences from freeze-related shutdowns—solidified hydrocarbons blocking pipelines, water condensate freezing in instrumentation lines, fire suppression systems rendered inoperative—making heat tracing systems mandatory safety equipment rather than optional accessories. Chemical processing plants similarly depend on maintaining precise viscosity in transfer lines, preventing crystallization in reactors, and ensuring emergency systems remain operational regardless of ambient conditions. These requirements exist independent of geographic location, as even facilities in moderate climates specify freeze protection for worst-case weather scenarios, while process temperature maintenance applies universally wherever heated materials are transported or stored, creating baseline demand driven by industrial activity levels rather than purely climate-dependent factors.

Opportunity: Building Electrification and Radiant Heating Adoption

The global building electrification movement creates substantial opportunities for heating cable market expansion as jurisdictions implement combustion heating bans and building codes increasingly favor electric systems compatible with renewable energy integration. Radiant floor heating provides superior thermal comfort compared to forced-air systems—delivering warmth at floor level where occupants experience it most directly, eliminating uncomfortable drafts, and enabling lower ambient temperatures while maintaining comfort, thereby reducing overall heating energy consumption 10-20% according to building science research. This efficiency advantage combines with compatibility with low-temperature heat sources including air-source heat pumps operating most efficiently at moderate supply temperatures ideal for radiant distribution, creating technical and economic synergies driving floor heating specification in new construction and major renovations across residential and commercial building segments increasingly subject to electrification mandates and net-zero energy targets.

Why Do Self-regulating Heating Cables Lead the Market?

The self-regulating heating cables segment accounts for the largest portion of the overall heating cables market in 2026, representing approximately 55-60% of total revenue. This dominance stems from fundamental technical advantages inherent to self-regulating technology—conductive polymer core automatically increasing electrical resistance as temperature rises, thereby reducing heat output in warm sections while maintaining higher output where colder, creating self-balancing system requiring no external temperature control for basic applications. This automatic adjustment delivers substantial energy efficiency benefits compared to constant wattage alternatives, particularly in applications experiencing variable ambient conditions or where cable experiences differential exposure—portions in conduit versus exposed to weather, sections near heat sources versus remote locations. The technology virtually eliminates overheating risks even under insulation or overlapping conditions that would cause constant wattage cables to fail, simplifying installation by removing requirements for precise spacing and enabling field-cutting to exact lengths without factory termination, significantly reducing installation costs and complexity compared to constant wattage systems requiring pre-determined circuit designs. However, constant wattage cables demonstrate steady growth in specialized applications requiring precise process temperatures or extreme ambient conditions exceeding self-regulating cable exposure ratings, maintaining 30-35% market share concentrated in industrial process heating, high-temperature maintenance, and critical applications where predictable heat output justifies additional installation complexity.

How Does Freeze Protection Dominate?

Based on application, the freeze protection segment holds the largest share of the overall market in 2026, accounting for approximately 40-45% of heating cable deployment. This dominance reflects universal industrial requirement to prevent freeze damage in water lines, process piping, fire suppression systems, and instrumentation across facilities in cold climates and temperate regions experiencing occasional freezing conditions. The consequences of freeze-related failures extend beyond immediate damage—burst pipes causing facility flooding, production shutdowns lasting days or weeks while repairs complete, potential safety system failures during emergencies, and liability exposure from property damage or injuries resulting from inadequate freeze protection. These risks drive conservative engineering approaches where freeze protection systems are installed on all potentially vulnerable piping regardless of historical weather patterns, as single severe weather event can justify decades of heat trace operating costs through prevented damage. The floor heating segment demonstrates highest growth rate at 11-13% CAGR, driven by residential and commercial construction markets increasingly adopting radiant heating for comfort, energy efficiency, and design flexibility enabling tile, stone, or concrete finish flooring without compromise in thermal comfort, particularly in luxury residential projects, hotels, and commercial spaces where underfloor heating provides premium amenities differentiating property offerings in competitive real estate markets.

Why Does Industrial Segment Command Market Leadership?

The industrial segment commands the largest share of the global heating cables market in 2026, representing approximately 50-55% of total revenue driven by extensive heat trace requirements across process industries. Oil and gas sector alone represents substantial demand—upstream production facilities maintaining wellhead and gathering line temperatures, midstream pipeline networks requiring hundreds of kilometers of heat trace, downstream refineries and petrochemical complexes with thousands of individual heat-traced circuits maintaining process temperatures. Chemical manufacturing facilities similarly deploy comprehensive heat tracing systems maintaining viscosity in transfer lines, preventing solidification in storage tanks, and ensuring emergency systems remain operational. Water and wastewater treatment plants require freeze protection on outdoor piping, building heating systems, and process equipment exposed to weather. Power generation facilities protect fuel oil systems, condensate lines, and critical instrumentation from freezing. These industrial applications typically involve larger system scale, higher power density requirements, more demanding environmental conditions, and longer system lifespans compared to commercial or residential deployments, generating higher revenue per installation and requiring specialized engineering, premium materials, and ongoing maintenance services creating recurring revenue opportunities for heating cable suppliers and installation contractors serving industrial markets.

How Do Low Voltage Systems Dominate Residential Applications?

Low voltage heating cables (typically 120-277V) dominate residential and light commercial applications, representing approximately 60% of unit volume installations though lower per-project value compared to industrial medium voltage systems. This prevalence stems from compatibility with standard building electrical systems, simplified installation not requiring specialized high-voltage electrician certifications, and inherent safety advantages at lower voltage levels particularly relevant in occupied building environments. Residential floor heating systems universally employ low voltage cables integrated with standard 120V or 240V residential circuits, while small-scale commercial applications including gutter de-icing, pipe freeze protection, and comfort heating similarly utilize low voltage systems interfacing with conventional building electrical infrastructure. Medium voltage systems (typically 480V industrial power or higher) concentrate in large industrial installations where power distribution efficiency and cable cost economics favor higher voltage operation—longer circuit lengths achievable with given conductor size, reduced current requirements minimizing voltage drop, and lower installed cost per linear foot of coverage in large-scale applications. However, medium voltage systems require certified electricians, more complex control panels, and additional safety precautions, limiting deployment to industrial and large commercial projects where scale justifies additional installation complexity and cost, creating market bifurcation between high-volume low-voltage residential/commercial applications and high-value medium-voltage industrial installations.

How is North America Maintaining Market Dominance?

North America holds the largest share of the global heating cables market in 2026, accounting for approximately 35-40% of total revenue. This dominance reflects multiple factors: extensive industrial infrastructure including oil and gas pipeline networks, chemical processing complexes, and water treatment facilities requiring comprehensive freeze protection and process temperature maintenance systems; harsh winter climates across northern United States and Canada creating substantial residential and commercial demand for pipe freeze protection, floor heating, and roof de-icing applications; mature market awareness and established installation practices driving heating cable specification as standard engineering practice rather than specialty application; and presence of major heating cable manufacturers including nVent (Raychem), Emerson (Chromalox), and Thermon maintaining extensive distribution networks and technical support infrastructure serving North American markets. The region benefits from replacement and retrofit opportunities in aging industrial facilities upgrading obsolete heat trace systems, building renovation projects installing radiant floor heating during major remodels, and infrastructure modernization including municipal water system upgrades incorporating freeze protection in previously unprotected distribution networks as climate variability increases freeze event frequency in traditionally temperate regions.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates highest growth rate at 11-13% CAGR, propelled by multiple concurrent trends: rapid industrial expansion in China and India creating demand for heat trace systems in new chemical plants, refineries, and manufacturing facilities; explosive growth in residential and commercial construction incorporating floor heating systems as standard amenity in premium developments across China, Japan, South Korea, and Taiwan where radiant heating aligns with cultural preferences for floor-level comfort; increasing adoption of Western building practices including freeze protection systems as cold-region construction activity expands; and growing awareness of energy efficiency benefits driving specification of advanced heating cable technologies. China represents largest single-country opportunity, with government initiatives promoting building electrification, industrial safety improvements, and energy efficiency in both new construction and facility retrofits creating favorable policy environment for heating cable adoption. Japan and South Korea demonstrate particularly strong floor heating markets, with mature markets for electric radiant systems in residential construction and expanding commercial applications in hotels, offices, and retail spaces. Southeast Asian markets remain primarily focused on industrial applications with limited residential adoption given tropical climates, though industrial sector expansion in petrochemical and manufacturing facilities drives steady growth in process heating and safety system applications.

The companies such as nVent Electric plc (Raychem, Tracer), Thermon Group Holdings, Inc., Emerson Electric Co. (Chromalox), and Danfoss A/S lead the global heating cables market with comprehensive product portfolios spanning self-regulating, constant wattage, and mineral insulated cables serving industrial, commercial, and residential applications. Meanwhile, specialized players including Bartec Group, eltherm GmbH, Heat Trace Products LLC, and SST Group focus on specific market segments such as hazardous area heating systems, high-temperature process applications, and custom-engineered heating solutions for specialized industrial requirements. Regional manufacturers such as Warmup plc (UK), Nexans S.A. (France), Heat Trace Ltd. (UK), and Anhui Huanrui Heating Manufacturing Co., Ltd. (China) strengthen the market through innovations in floor heating systems, energy-efficient control technologies, and cost-optimized product offerings targeting regional construction and industrial markets, while emerging players including King Manufacturing Company, BriskHeat Corporation, and Wuhu Jiahong New Material Co., Ltd. are expanding market presence through specialized heating cable products for niche applications and geographic markets underserved by established multinational suppliers.

The global heating cables market is expected to grow from USD 3.18 billion in 2026 to USD 7.94 billion by 2036.

The global heating cables market is projected to grow at a CAGR of 9.6% from 2026 to 2036.

Self-regulating heating cables dominate the market in 2026 due to inherent energy efficiency and installation flexibility advantages. However, mineral insulated cables demonstrate strong growth in high-temperature industrial applications requiring extreme durability and temperature capabilities exceeding 600°C.

Smart controls and IoT integration enable predictive maintenance through continuous system monitoring, optimize energy consumption through weather-responsive controls and time-of-use rate management, provide remote diagnostics reducing maintenance costs, and enable integration with building automation systems for comprehensive facility thermal management, particularly valuable in industrial facilities managing hundreds of heat trace circuits and commercial buildings optimizing comfort heating across multiple zones.

North America holds the largest share with 35-40% of global revenue, driven by extensive industrial infrastructure and harsh winter climates. Asia-Pacific demonstrates fastest growth at 11-13% CAGR, propelled by industrial expansion and residential floor heating adoption in China, Japan, and South Korea.

The leading companies include nVent Electric plc (Raychem), Thermon Group Holdings, Inc., Emerson Electric Co. (Chromalox), Danfoss A/S, and Warmup plc.

Published Date: Mar-2024

Published Date: Aug-2026

Published Date: Jan-2025

Published Date: Mar-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates