Resources

About Us

Geopolymer Concrete Market by Raw Material (Fly Ash, Slag, Metakaolin, Others), Product Type (Ready-mix Concrete, Precast Concrete), Application (Infrastructure, Industrial, Residential, Commercial) – Global Forecast to 2036

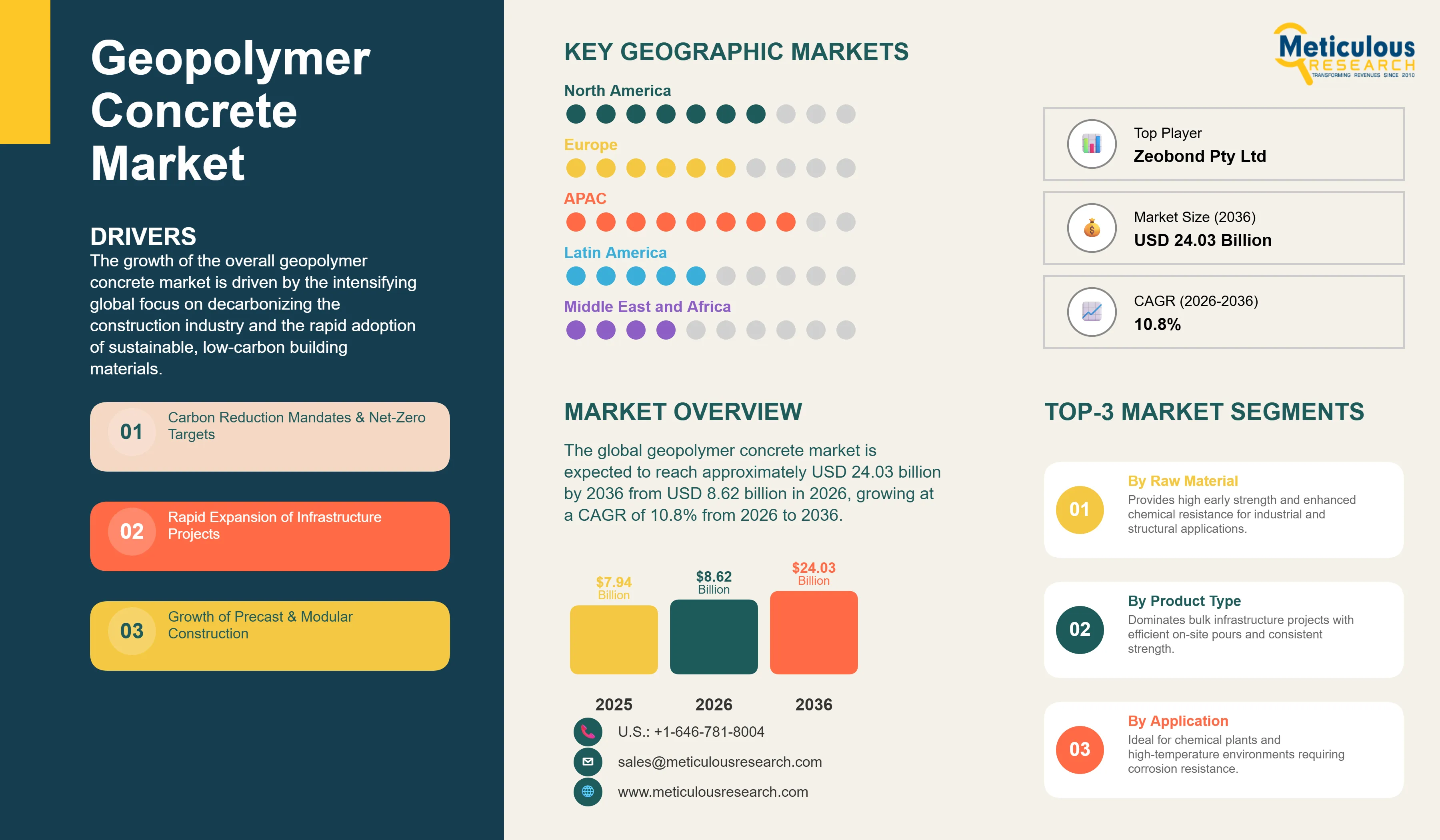

Report ID: MRCHM - 1041839 Pages: 286 Mar-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global geopolymer concrete market was valued at USD 7.94 billion in 2025. The market is expected to reach approximately USD 24.03 billion by 2036 from USD 8.62 billion in 2026, growing at a CAGR of 10.8% from 2026 to 2036. The growth of the overall geopolymer concrete market is driven by the intensifying global focus on decarbonizing the construction industry and the rapid adoption of sustainable, low-carbon building materials. As governments and developers seek to reduce the massive carbon footprint associated with traditional Portland cement, geopolymer technologies have become essential for green building initiatives and circular economy strategies. The rapid expansion of infrastructure projects, coupled with the increasing need for high-performance, fire-resistant, and chemically resilient concrete solutions, continues to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Geopolymer concrete is a sustainable alternative to traditional cement-based concrete, utilizing industrial by-products such as fly ash and slag as binders instead of ordinary Portland cement (OPC). These materials react with alkaline activators to form a robust, ceramic-like matrix that offers superior durability, lower permeability, and exceptional resistance to fire and chemical attack. The market is defined by high-performance technologies that significantly reduce CO2 emissions—often by up to 80-90%—making them indispensable for industries seeking to optimize their environmental impact and meet corporate sustainability targets.

The market includes a diverse range of configurations, ranging from ready-mix solutions for in-situ pours to high-precision precast elements for bridges, tunnels, and residential panels. These systems are increasingly integrated with advanced chemical admixtures and digital quality control platforms to provide services such as real-time strength monitoring and optimized mix designs. The ability to provide stable, high-strength structural recovery while utilizing waste streams has made advanced geopolymer concrete the technology of choice for industries where resource efficiency and environmental compliance are paramount.

The global construction sector is pushing hard to modernize aging infrastructure, aiming to meet net-zero emission and carbon-neutral targets. This drive has increased the adoption of geopolymer systems, with advanced binders helping to stabilize the industry’s carbon consumption. At the same time, the rapid growth in the precast and modular building markets is increasing the need for high-precision geopolymer formulations.

Manufacturers across the construction industry are rapidly shifting to precast geopolymer technology, moving well beyond traditional on-site pours toward smarter, factory-controlled modular setups. Wagners’ latest Earth Friendly Concrete (EFC) precast elements deliver up to 80% carbon savings over conventional designs, while Zeobond’s recent European infrastructure installations have demonstrated superior durability in harsh environments. The real game-changer comes with “smart” precast systems featuring integrated sensors that maintain structural health monitoring even when environmental conditions fluctuate wildly. These advancements make high-efficiency geopolymer concrete practical and cost-effective for everyone from bridge builders to residential developers chasing LEED certifications and lower carbon footprints.

Innovation in aluminosilicate sourcing and alkaline activation is rapidly driving the geopolymer concrete market, as the circular economy and sustainable building sectors scale up. Equipment suppliers are now designing binder systems specifically for high-purity metakaolin and industrial slag, with tight control over setting times, workability, and moisture content to meet stringent structural specifications. This often involves advanced mixing and curing technologies capable of handling highly reactive precursors without excessive shrinkage or cracking.

At the same time, growing focus on resource recovery is pushing manufacturers to develop geopolymer solutions tailored to specific industrial waste streams. These systems help recover value from fly ash, red mud, and mine tailings, concentrating and activating them into high-value construction materials instead of landfill waste. By combining high-efficiency binder chemistry with precisely controlled curing stages, these new designs support both primary infrastructure development and closed-loop recycling, strengthening the sustainability and resource security of the broader construction value chain.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 24.03 Billion |

|

Market Size in 2026 |

USD 8.62 Billion |

|

Market Size in 2025 |

USD 7.94 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.8% |

|

Dominating Region |

Asia Pacific |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Raw Material, Product Type, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A key driver of the geopolymer concrete market is the rapid movement of the global construction industry toward carbon neutrality and environmental stewardship. Global regulations requiring the reduction of embodied carbon in buildings have created significant incentives for the adoption of geopolymer technologies. The European Green Deal, the U.S. Buy Clean Initiative, and China’s “Green Building Action Plan” drive developers toward scalable solutions that geopolymer systems can uniquely provide. It is estimated that as carbon taxes rise and building permits become more restrictive through 2036, the need for low-carbon materials increases significantly; therefore, geopolymer concrete, with its ability to reduce CO2 emissions by up to 90%, is considered a crucial enabler of modern construction strategies.

The rapid growth of resilient infrastructure and resource recovery provides great opportunities for the geopolymer concrete market. Indeed, the global surge in circular economy initiatives has created a compelling demand for systems that can recover valuable materials from industrial waste streams. These applications require high reliability, long operational life, and the ability to handle corrosive or high-temperature environments, all attributes that are met with advanced geopolymer formulations. The resource recovery market is set to expand significantly through 2036, with geopolymer binders poised for an expanding share as operators seek to monetize waste streams. Furthermore, the increasing demand for fire-resistant and acid-resistant materials in the industrial and utility sectors is stimulating demand for modular geopolymer systems that provide structural independence and resilience.

The ready-mix concrete segment accounts for around 60-65% of the overall geopolymer concrete market in 2026. This is mainly attributed to the primary use of this technology in large-scale infrastructure pours, pavements, and foundations across a wide range of industries. These systems offer the most efficient way to manage bulk material shifts and provide consistent structural performance. The infrastructure and industrial sectors alone consume the vast majority of ready-mix geopolymer production, with major projects in Asia Pacific and North America demonstrating the technology’s capability to handle high-volume processing.

However, the precast concrete segment is expected to grow at the fastest CAGR during the forecast period, driven by the growing utility-scale projects in modular housing, bridge components, and tunnel linings. The ability to produce high-value solid products in controlled factory environments makes precast geopolymers highly attractive for modern industrial users.

Based on raw material, the fly ash segment holds the largest share of the overall market in 2026, accounting for around 50-55% of the overall market. From large-scale road construction to high-efficiency building panels, the use of fly ash is central to modernizing construction infrastructure. Current large-scale projects are increasingly specifying fly ash-based geopolymers for their superior workability and lower cost compared to metakaolin or slag-based alternatives.

The slag and metakaolin segments continue to find critical applications in industries where high early strength or specific aesthetic requirements favor specialized formulations. However, the shift toward waste-to-resource and decarbonization is pushing the requirement for standardized fly ash systems that allow businesses to scale their construction capacity while minimizing their carbon footprint.

Asia Pacific holds the largest share of the global geopolymer concrete market in 2026. The largest share of this region is primarily attributed to the massive urbanization and the presence of the world’s largest construction and industrial manufacturing hubs, particularly in China, India, and Australia. China alone accounts for more than 40% of global geopolymer consumption, with its position as a leading hub for infrastructure and automotive manufacturing driving sustained growth. The presence of leading manufacturers like Wagners and a well-developed industrial supply chain provides a robust market for both standard and high-efficiency geopolymer solutions.

North America and Europe together account for around 35 to 40% of the global geopolymer concrete market. The growth of these markets is mainly driven by the need for low-carbon modernization and the implementation of stringent environmental mandates. The demand for green building systems in North America is mainly due to its large-scale sustainable automation projects and the presence of innovators like Milliken & Company and Geopolymer Solutions.

In Europe, the leadership in sustainable industrial policies and the push for carbon neutrality are driving the adoption of high-efficiency geopolymer concrete. Countries like Germany, France, and the UK are at the forefront, with significant focus on integrating smart geopolymer elements into digital construction environments.

The companies such as Wagners, Zeobond Pty Ltd, Milliken & Company (GeoSpray), and Geopolymer Solutions lead the global geopolymer concrete market with a comprehensive range of binder and structural solutions, particularly for large-scale infrastructure and industrial applications. Meanwhile, players including CEMEX S.A.B. de C.V., BASF SE, Imerys Group, and JSW Cement focus on specialized chemical activators, metakaolin precursors, and slag-based systems targeting the residential and commercial sectors. Emerging manufacturers and integrated players such as Banah UK Ltd, Kiran Global Chems, and Woellner GmbH are strengthening the market through innovations in activator technology and smart monitoring systems.

The geopolymer concrete market is expected to grow from USD 8.62 billion in 2026 to USD 24.03 billion by 2036.

The geopolymer concrete market is expected to grow at a CAGR of 10.8% from 2026 to 2036.

The major players include Wagners, Zeobond Pty Ltd, Milliken & Company, Geopolymer Solutions, and CEMEX S.A.B. de C.V., among others.

The main factors include carbon reduction mandates, sustainable construction initiatives, and the rapid expansion of the circular economy.

Asia Pacific will lead the global geopolymer concrete market in terms of market share, while North America is expected to witness the fastest growth during the forecast period 2026 to 2036.

Published Date: Jul-2024

Published Date: Jan-2025

Published Date: May-2024

Published Date: Oct-2024

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates