Resources

About Us

Food Packaging Equipment Market by Type (Cartoning Equipment, Filling & Dosing Equipment, Wrapping & Bundling Equipment, Case Packing Equipment, Labeling & Coding Equipment), Application (Dairy, Bakery, Chocolate & Confectionery, Fruits & Vegetables, Meat, Poultry, Seafood), and Geography - Global Forecast to 2036

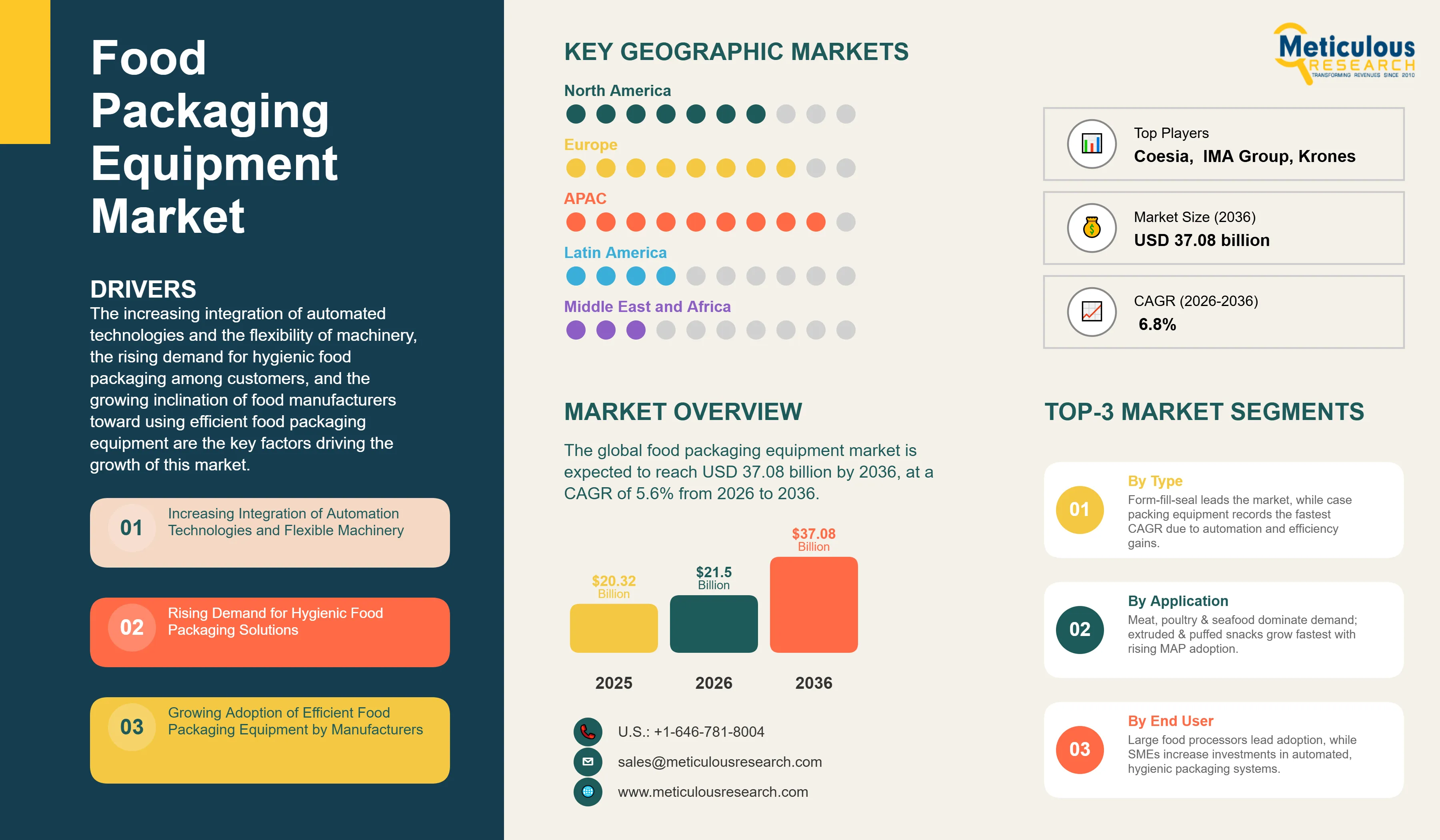

Report ID: MRFB - 104562 Pages: 270 Feb-2026 Formats*: PDF Category: Food and Beverages Delivery: 24 to 48 Hours Download Free Sample ReportThe global food packaging equipment market was valued at USD 20.32 billion in 2025. This market is expected to reach USD 37.08 billion by 2036 from USD 21.50 billion in 2026, at a CAGR of 5.6% from 2026 to 2036. In terms of volume, the global food packaging equipment market is expected to reach around 19,230 thousand units by 2036, at a CAGR of 6.8% during the forecast period.

The increasing integration of automated technologies and the flexibility of machinery, the rising demand for hygienic food packaging among customers, and the growing inclination of food manufacturers toward using efficient food packaging equipment are the key factors driving the growth of this market. The growth of the packaged food industry in emerging economies and the growing use of packaging as a product differentiation tool provide significant growth opportunities for market players. However, the high cost of advanced food packaging solutions and stringent environmental regulations are expected to restrain market growth to some extent during the forecast period.

Click here to: Get Free Sample Pages of this Report

The global food packaging equipment market encompasses machines and systems used to package food products into primary, secondary, and tertiary packaging formats across a diverse range of food industry segments. The equipment covered includes form-fill-seal machines, cartoning equipment, filling and dosing equipment, wrapping and bundling machines, case packing equipment, labeling and coding systems, and inspecting, detecting, and check weighing machines. These equipment types serve applications across dairy, bakery, chocolate and confectionery, fruits and vegetables, meat, poultry and seafood, snack food, and other food product categories.

The global food packaging equipment market is undergoing a significant transformation driven by the increasing automation of food manufacturing processes, the growing emphasis on food safety and hygiene across all production environments, and the rapid expansion of the packaged food industry in developing economies. Rapid technological advancements, heightened consumer expectations for product quality and safety, and increasingly stringent regulatory requirements are collectively driving food manufacturers to invest in advanced packaging equipment capable of delivering both operational efficiency and compliance with evolving food safety standards. The integration of IoT technology, smart sensors, and big data analytics into modern food packaging equipment platforms is enabling manufacturers to achieve real-time monitoring of packaging operations, automated quality control, and end-to-end supply chain traceability that was previously unattainable with conventional packaging machinery.

Increasing Integration of Automation Technologies and Flexible Packaging Machinery

Rapid technological advancements, rising consumer expectations for food quality and safety, and increasingly stringent regulatory requirements are encouraging food manufacturers to automate packaging processes at an accelerated pace. Food processing remains a labor-intensive industry, with labor costs accounting for around 20-40% of the total production costs, creating strong incentives for manufacturers to adopt automated packaging solutions to improve productivity and reduce operational expenditure.

The growing demand for packaging formats offering portability, resealability, and extended shelf life, such as lightweight, micro-perforated, and modified atmosphere packaging, has increased the need for specialized and adaptable packaging equipment across product categories such as snacks, meat and poultry, confectionery, sauces, processed fruits and vegetables, and dairy products. In addition, the integration of Industry 4.0 technologies, including IoT-enabled monitoring systems and data analytics platforms, is driving the adoption of smart packaging equipment capable of real-time product tracking and quality monitoring throughout the supply chain.

Rising Demand for Hygienic and Safe Food Packaging Solutions

The growing global burden of foodborne illnesses and increasing consumer awareness regarding food safety risks are compelling food manufacturers to prioritize hygienic design across packaging operations. According to the World Health Organization (WHO), an estimated 600 million people, nearly 1 in 10 globally, fall ill each year due to contaminated food, resulting in approximately 420,000 deaths annually, highlighting the critical importance of safe food handling and packaging practices.

Regulatory frameworks across major markets, including food safety regulations in the U.S., Europe, and Asia-Pacific, are establishing stricter requirements for packaging equipment cleanability, material compatibility, and contamination prevention. The COVID-19 pandemic further accelerated the transition toward automated packaging systems designed to reduce manual human contact with food products during packaging processes. Moreover, the increasing adoption of vacuum and modified atmosphere packaging (MAP) systems, particularly in meat, poultry, seafood, and fresh produce applications, is driving demand for equipment that enhances product shelf life, reduces food waste, and ensures tamper-evident and hygienic packaging in compliance with retailer and regulatory standards.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 37.08 Billion |

|

Revenue CAGR from 2026 to 2036 |

5.6% |

|

Largest Type Segment (2025) |

Form-fill-seal Equipment |

|

Fastest Growing Type Segment |

Case Packing Equipment |

|

Fastest Growing FFS Sub-type |

Vertical Form-fill-seal Equipment |

|

Largest Application Segment (2025) |

Meat, Poultry, and Seafood |

|

Fastest Growing Snack Sub-segment |

Extruder & Puffed Snacks |

|

Largest Geography (2025) |

Asia-Pacific |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Application, and Geography |

|

Geographies Covered |

Asia-Pacific, Europe, North America, Latin America, and Middle East & Africa |

Food Packaging Equipment Market Analysis, by Type

Form-fill-seal Equipment to Lead; Case Packing Equipment to Register Highest CAGR

Based on type, the food packaging equipment market is segmented into form-fill-seal equipment (horizontal and vertical), cartoning equipment, filling and dosing equipment, wrapping and bundling equipment, case packing equipment, labeling and coding equipment, inspecting, detecting, and check weighing machines, and other equipment. In 2026, the form-fill-seal equipment segment is expected to account for the largest share of the overall food packaging equipment market. Form-fill-seal equipment, mainly vertical form-fill-seal (VFFS) machines, is extensively deployed across snack food, bakery, frozen food, and fresh produce applications due to its ability to form, fill, and seal packages from a continuous roll of packaging film in a single automated operation, delivering high throughput efficiency and hygienic containment of a wide range of food products.

However, the case packing equipment segment is expected to register the highest CAGR during the forecast period. The high growth rate of this segment is driven by the increasing demand for higher production volumes within shorter time frames, improved food safety through reduced manual handling of primary packaged products, lowered company expenses through reduced labor costs in secondary packaging operations, and reduced risk of potential bottlenecks and downtime associated with manual case packing processes. Within the form-fill-seal equipment sub-segment, vertical form-fill-seal equipment is expected to grow at a faster CAGR than horizontal form-fill-seal equipment, attributed to its flexibility to support automated assembly-line packaging systems, suitability for restricted floor space environments, and simplified design that constitutes an easier and faster system to clean, making it well-suited for food applications with stringent hygienic design requirements.

Meat, Poultry, and Seafood Holds Largest Share; Extruder & Puffed Snacks Fastest-growing Sub-segment

Based on application, the food packaging equipment market is segmented into dairy, bakery, chocolate and confectionery, fruits and vegetables, meat, poultry and seafood, snack food, and others. In 2026, the meat, poultry, and seafood segment is expected to account for the largest share of the overall food packaging equipment market and is also expected to grow at a significant pace during the forecast period. The high market share and growth rate of this segment are attributed to the higher usage of vacuum and MAP-sealed trays in meat, poultry, and seafood product packaging for aesthetic appeal and shelf life extension.

Within the snack food application segment, the extruder and puffed snacks sub-segment is expected to register the highest CAGR during the forecast period. The high growth rate of this sub-segment is driven by the specific packaging requirements of high-fat content snack food products, which are prone to rancidity without proper modified atmosphere packaging. To ensure longer shelf life, oxygen inside the package is replaced by an inert gas such as nitrogen, requiring packaging materials and equipment capable of reliably executing gas-flush operations and delivering consistently strong seal integrity to maintain package atmosphere. The bakery segment represents a significant application for food packaging equipment, driven by the high diversity of bakery product formats and the extensive use of flow wrapping, cartoning, and tray-sealing equipment across industrial bakery production.

Asia-Pacific to Lead and Register Highest CAGR

Based on geography, the Asia-Pacific is expected to account for the largest share of the food packaging equipment market in 2026 and is also expected to grow at the fastest CAGR during the forecast period. This is mainly attributed to the growing application of packaged food products across the region, the high concentration of locally available packaging equipment manufacturers, mainly China and Japan, and the rapidly increasing demand for processed and packaged food products in major emerging and developing economies, including India, China, South Korea, and Australia. This region is witnessing tremendous growth in its food and beverage industry, driven by increasing urbanization, growing health awareness, and rising disposable income levels. The changing regulatory environment and shifting consumer preferences in the Asia-Pacific also provide continued growth opportunities for both domestic and international packaging equipment market players.

Europe is the second-largest regional market for food packaging equipment, driven by its highly developed food processing industry, strong regulatory environment for food safety and packaging sustainability, and significant concentration of global food packaging equipment manufacturers. Germany is both one of the largest markets for food packaging equipment and the home of several global market leaders including Syntegon Technology GmbH, GEA Group Aktiengesellschaft, Krones AG, and OPTIMA Packaging Group GmbH.

North America is also a major market driven by the large and sophisticated U.S. food processing industry, strong demand for automation in food manufacturing, and high penetration of advanced packaging technologies across all food product categories. Latin America and the Middle East and Africa represent emerging but growing markets, with growing food processing industries and increasing investment in modern packaging equipment driven by the growth of organized retail and the formalization of food supply chains.

Food Packaging Equipment Market: Competitive Landscape

The global food packaging equipment market is characterized by the presence of several established multinational original equipment manufacturers offering advanced packaging technologies across diverse food applications. Key companies operating in this market include Syntegon Technology GmbH (Germany), Coesia S.p.A. (Italy), GEA Group Aktiengesellschaft (Germany), MULTIVAC Group (Germany), Krones AG (Germany), Tetra Laval Group (Switzerland), OPTIMA Packaging Group GmbH (Germany), Ishida Co., Ltd. (Japan), Omori Machinery Co., Ltd. (Japan), and TNA Solutions Pty Ltd (Australia), among others. These players compete based on technological innovation, hygienic equipment design, automation capabilities, and the ability to provide integrated packaging solutions supported by global service and aftermarket networks.

Food Packaging Equipment Market Assessment, by Type

Food Packaging Equipment Market Assessment, by Application

Food Packaging Equipment Market Assessment, by Geography

The report provides a detailed assessment of the global food packaging equipment market based on type, application, and geography, including value and volume analysis at the regional and country levels, along with an evaluation of market dynamics and the competitive landscape.

The global food packaging equipment market is projected to reach approximately USD 37.08 billion by 2036 from USD 21.50 billion in 2026, at a CAGR of 5.6% from 2026 to 2036.

Based on type, the form-fill-seal equipment segment is expected to account for the largest share of the global food packaging equipment market in 2025.

Based on type, the case packing equipment segment is expected to register the highest CAGR during the forecast period, driven by increasing production volumes, improved food safety, reduced labor costs, and minimized operational bottlenecks.

The vertical form-fill-seal equipment segment is expected to grow at a faster rate during the forecast period due to its operational flexibility, compact footprint, and ease of cleaning.

Based on application, the meat, poultry, and seafood segment is expected to account for the largest share and register significant growth during the forecast period. Within snack foods, the extruder and puffed snacks sub-segment is expected to record the highest CAGR.

Key growth drivers include the increasing adoption of automation technologies, rising demand for hygienic and safe food packaging solutions, and the growing emphasis on operational efficiency among food manufacturers. Opportunities are expected to emerge from the expanding packaged food industry in emerging economies and the increasing use of packaging as a product differentiation tool.

Asia-Pacific is expected to account for the largest share and register the highest CAGR during the forecast period. Countries such as India and China are anticipated to offer significant growth opportunities for food packaging equipment manufacturers.

Key companies operating in the global food packaging equipment market include Syntegon Technology GmbH (Germany), Coesia S.p.A. (Italy), GEA Group Aktiengesellschaft (Germany), MULTIVAC Group (Germany), IMA Group (Italy), Krones AG (Germany), Tetra Laval Group (Switzerland), OPTIMA Packaging Group GmbH (Germany), ARPAC LLC (U.S.), Ishida Co., Ltd. (Japan), Omori Machinery Co., Ltd. (Japan), and TNA Solutions Pty Ltd (Australia), among others.

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Nov-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates