Resources

About Us

Food Processing Equipment Market Size, Share, Forecast, & Trends Analysis by Type (Meat, Poultry, and Seafood; Beverage; Bakery; Dairy; Chocolate & Confectionery; Fruit and Vegetable; Snacks Processing Equipment), Mode of Operation (Semi-Automatic, Automatic) – Global Forecast to 2036

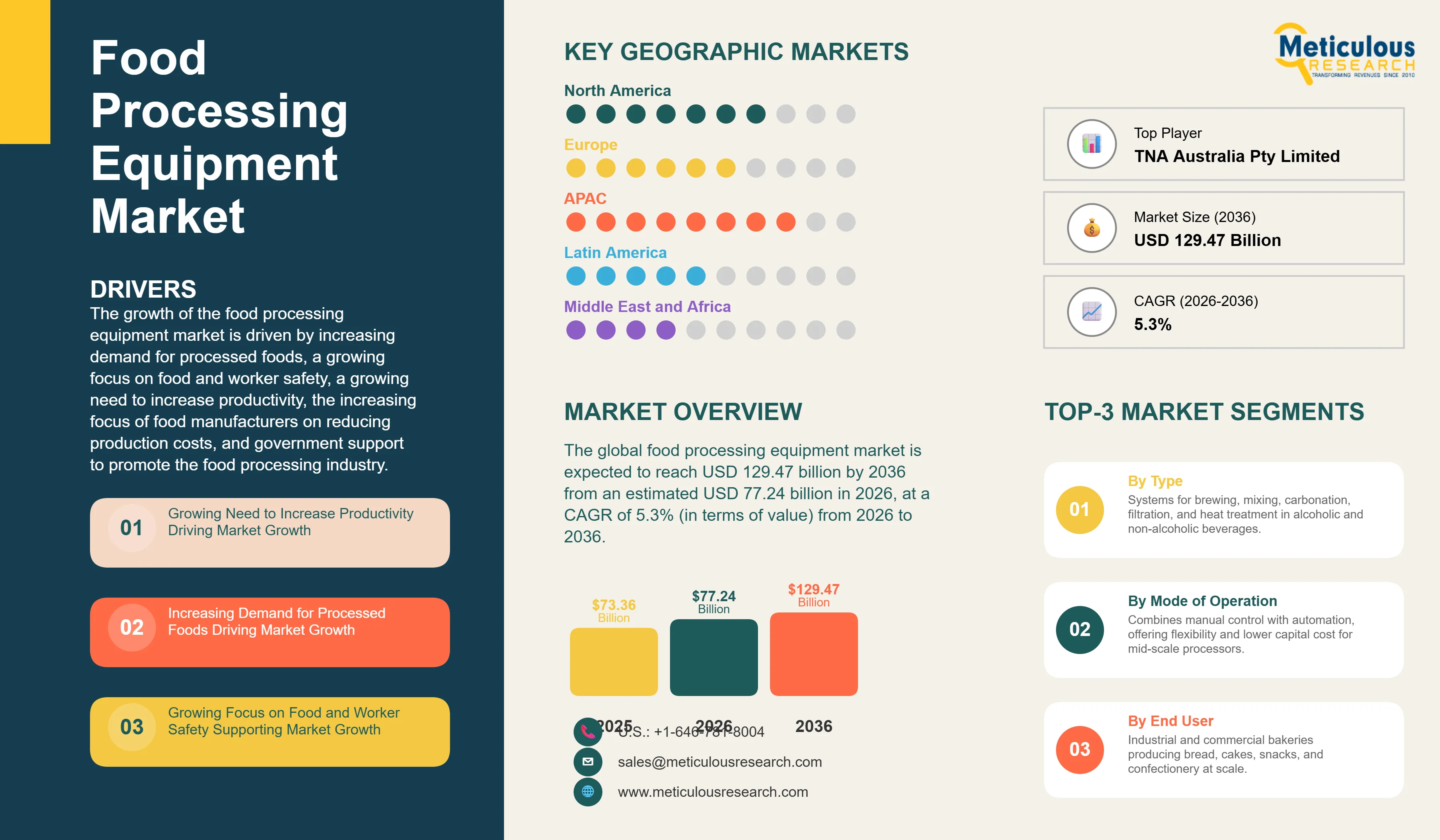

Report ID: MRFB - 104350 Pages: 250 Feb-2026 Formats*: PDF Category: Food and Beverages Delivery: 24 to 48 Hours Download Free Sample ReportThe global food processing equipment market was valued at USD 73.36 billion in 2025. This market is expected to reach USD 129.47 billion by 2036 from an estimated USD 77.24 billion in 2026, at a CAGR of 5.3% (in terms of value) from 2026 to 2036. In terms of volume, the market is expected to reach 3.45 million units by 2036, at a CAGR of 3.1% from 2026 to 2036.

The growth of the food processing equipment market is driven by increasing demand for processed foods, a growing focus on food and worker safety, a growing need to increase productivity, the increasing focus of food manufacturers on reducing production costs, and government support to promote the food processing industry. However, the high cost of equipment and increasing inclination of consumers towards minimally processed food products restrain market growth. In addition, emerging economies such as those in Latin America, Southeast Asia, and Africa, and a rapidly growing plant-based foods market, are expected to generate growth opportunities for the players operating in this market. However, the lack of trained labor remains a major challenge.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The food processing equipment market includes the machinery and systems used to transform raw agricultural products such as meat, poultry, seafood, grains, dairy, fruits, vegetables, and beverages into consumer-ready food products through processes including cleaning, cutting, mixing, cooking, pasteurizing, homogenizing, packaging, and preservation. The market spans a diverse range of equipment types across eight principal product categories: meat, poultry, and seafood processing equipment; beverage processing equipment; bakery processing equipment; dairy processing equipment; chocolate and confectionery processing equipment; fruit and vegetable processing equipment; snack processing equipment; and other food processing equipment.

The food processing equipment industry is undergoing a period of significant technological transformation and competitive consolidation. Technological advancements are driving the integration of automation, robotics, artificial intelligence, IoT connectivity, and digital twin technologies into food processing machinery, enhancing productivity, consistency, and traceability across production lines. Smart sensors and real-time monitoring systems are enabling advanced quality control and predictive maintenance capabilities, while hygienic design innovations and energy-efficient systems are improving regulatory compliance and sustainability performance. Modular and flexible equipment configurations are enabling food manufacturers to accommodate diverse and rapidly changing product portfolios on shared production lines. Digitalization is enabling predictive maintenance platforms that reduce unplanned downtime and total cost of ownership across installed equipment bases.lobal industry average.

Integration of Automation, Robotics, and AI in Food Processing Equipment

The integration of automation, robotics, and artificial intelligence into food processing equipment represents the most transformative technology trend reshaping the market during the 2026–2036 forecast period. Food manufacturers across all major product segments are increasingly deploying automated processing lines, including robotic deboning and portioning systems in meat and poultry processing, automated filling and aseptic packaging lines in beverage and dairy processing, and robotic depositing and packaging systems in bakery and confectionery, to address persistent challenges of labor cost inflation, labor shortages, and the need for consistent product quality and food safety compliance. AI algorithms are being integrated into quality inspection systems using machine vision to detect defects, foreign bodies, and quality deviations in real time at production line speeds that exceed human inspection capabilities. Smart sensors connected via IIoT platforms enable predictive maintenance strategies that anticipate equipment failures before they occur, minimizing unplanned downtime.

Sustainability and Energy Efficiency as Design Imperatives

Sustainability and energy efficiency have become defining design imperatives for food processing equipment manufacturers, driven by the evolving corporate sustainability commitments of food manufacturers, rising energy costs, tightening environmental regulations, and consumer and retailer expectations for measurable environmental performance improvements across food supply chains. Equipment innovations targeting sustainability include heat recovery systems in pasteurization and cooking processes, water recycling and closed-loop cleaning systems, energy-efficient motors and drives, low-emission refrigeration systems using natural refrigerants, and hygienic design improvements that reduce cleaning chemical and water consumption. Tetra Pak’s May 2024 announcement of homogenizer components using Circle Green stainless steel, with a carbon footprint 93% lower than the global industry average. This shows how leading equipment manufacturers are embedding sustainability credentials into their product value propositions. Additionally, Alfa Laval’s acquisition of cryogenics technology from Fives Group reflects strategic investment in sustainable processing technologies for gas liquefaction with applications across food and beverage processing.

The global food processing equipment market was valued at USD 73.36 billion in 2025. This market is expected to reach USD 129.47 billion by 2036 from an estimated USD 77.24 billion in 2026, at a CAGR of 5.3% (in terms of value) from 2026 to 2036. In terms of volume, the market is expected to reach 3.45 million units by 2036, at a CAGR of 3.1% from 2026 to 2036.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 129.47 Billion |

|

Market Size in 2026 |

USD 77.24 Billion |

|

Market Size in 2025 |

USD 73.36 Billion |

|

Market Volume by 2036 |

~3.45 Million Units |

|

Market Growth Rate – Value |

CAGR of 5.3% (2026–2036) |

|

Market Growth Rate – Volume |

CAGR of 3.1% (2026–2036) |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Dominating Type Segment |

Meat, Poultry, and Seafood Processing Equipment |

|

Highest CAGR Type Segment |

Beverage Processing Equipment |

|

Dominating Mode of Operation |

Semi-Automatic |

|

Highest CAGR Mode of Operation |

Automatic |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Type: Meat, Poultry & Seafood; Beverage; Bakery; Dairy; Chocolate & Confectionery; Fruit & Vegetable; Snacks; Other By Mode of Operation: Semi-Automatic, Automatic By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Growing Need to Increase Productivity in Food Manufacturing

The growing global need to increase food production productivity is a key driver of the growth of the food processing equipment market. Global food demand is projected to increase by 50% by 2050, according to the Food and Agriculture Organization of the United Nations (FAO), driven by a world population that is expected to reach 9.7 billion by 2050 from 7.8 billion in 2020. Simultaneously, more than one-third of all food produced globally is lost or wasted each year, with postharvest losses representing the greatest overall component of this waste. Modern food processing equipment addresses both the demand growth and the waste reduction imperatives simultaneously, enabling food processors to scale production throughput while extending product shelf life, improving yield recovery, and reducing processing losses. Automation of production lines enables food manufacturers to operate at consistently higher speeds and throughputs than manual or semi-manual alternatives, with greater consistency and lower defect rates. The adoption of modern food processing technologies and equipment among food processors represents the primary pathway to addressing the gap between projected food demand and current production capabilities.

Increasing Demand for Processed Foods

The growing global demand for processed foods across all major food categories is another major driver of the growth of the food processing equipment market. The global trend of urbanization, fast-paced modern lifestyles, growing prevalence of nuclear families, the increasing participation of women in the workforce, and the limited time available for food preparation are collectively driving demand for processed, packaged, and ready-to-eat food products across both developed and developing markets. Brand consciousness, exposure to Western food products in Asian markets, the introduction of new food categories, and the development of product variants catering to diverse consumer tastes all further drive consumption of processed food products. Rising per capita incomes in developing markets, mainly in Asia-Pacific, Latin America, and Africa, are expanding the addressable consumer population for processed foods, reinforcing demand for food processing equipment across these emerging markets. As food manufacturers respond to growing and diversifying consumer demand, they are continuously investing in new and upgraded processing equipment capable of handling expanded product portfolios and higher production volumes.

Why Does the Meat, Poultry, and Seafood Processing Equipment Segment Dominate?

Based on type, the meat, poultry, and seafood processing equipment segment is expected to account for the largest share of the overall food processing equipment market in 2026. The large share of this segment is attributed to growing global meat production driven by rising protein demand in developing markets, the high demand for processed meat products including pre-cooked, marinated, and convenience formats, the growing focus on food safety requirements of meat processors to prevent contamination and comply with stringent regulatory standards, and consumer preference for protein-rich food products across global markets. This equipment segment includes a comprehensive range of equipment such as cutters and grinders, smokers, massagers and tumblers, mixers and blenders, tenderizers, killing and defeathering equipment, slicers, evisceration equipment, cookers, roasters and grillers, de-heading and gutting equipment, and filleting equipment.

The beverage processing equipment segment is projected to witness the fastest CAGR during the forecast period. This growth is driven by the increasing demand for alcoholic beverages (craft beer, spirits, wine), growing consumption of ready-to-drink (RTD) beverages (functional beverages, energy drinks, RTD tea and coffee), increasing per capita spending in developing countries, and rising adoption of advanced processing technologies for quality and productivity enhancement. The segment includes brewery equipment, filtration equipment, carbonation equipment, blenders and mixers, and heat exchangers.

Why Does the Semi-Automatic Segment Lead the Food Processing Equipment Market?

Based on mode of operation, the semi-automatic segment is expected to account for the largest share of the overall food processing equipment market in 2026. Semi-automatic food processing equipment offers significantly improved labor productivity while retaining operator oversight for quality control and flexible product changeovers, along with the benefits of production flexibility and technical and economic feasibility for a broad range of food manufacturers from small artisanal producers to mid-scale industrial processors. The lower capital cost of semi-automatic equipment relative to fully automatic alternatives makes it accessible to the large segment of food manufacturers globally with moderate capital budgets and diverse, frequently changing product portfolios that require adaptable production capabilities.

However, the automatic segment is projected to grow at the fastest CAGR during the forecast period. The growth of this segment is driven by the increasing need for higher efficiency and improved food safety across large-scale food manufacturing operations, and the compelling operational benefits of automatic food processing equipment such as monitored and consistent production, substantially reduced labor costs, automatic tracking and traceability of production batches and individual loads, elimination of human errors and variability, effective automated cleaning systems, and complete elimination of cross-contamination risks associated with human handling.

Asia-Pacific: Largest and Fastest-Growing Regional Market

Based on geography, the Asia-Pacific is expected to account for the largest share of the global food processing equipment market in 2026. The largest share of this region is primarily attributed to the increasing demand for processed food products in rapidly growing emerging and developing economies including China, India, Indonesia, Vietnam, and Thailand; rising investments from major global and regional food and beverage manufacturers expanding their Asian production capacity; and government support programs across the region to promote domestic food processing industry development. The food processing sectors in China, India, Australia, and New Zealand are export-oriented, with players focusing on technology adoption and automation to enhance competitiveness in global food markets.

Moreover, the food processing equipment market in Asia-Pacific is projected to grow at the fastest CAGR during the forecast period, driven by significant growth in the food and beverage industry, fueled by growing urbanization, increasing health awareness, and rising disposable income levels. The region is expected to experience a sharp rise in demand for advanced food processing machinery that reduces processing time and enhances manufacturing efficiency. The growing number of food processing units across the region is further projected to boost the supply and consumption of food processing equipment.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by the leading players over the past 3 years. The key players profiled in the food processing equipment market report are Bühler AG (Switzerland), Marel hf (Iceland) – now part of JBT Marel Corporation, GEA Group Aktiengesellschaft (Germany), Bucher Industries AG (Switzerland), John Bean Technologies Corporation (U.S.) – now JBT Marel Corporation, The Middleby Corporation (U.S.), Heat and Control Inc. (U.S.), SPX Flow, Inc. (U.S.), Alfa Laval AB (Sweden), Krones AG (Germany), Paul Mueller Company (U.S.), Tetra Pak International S.A. (Sweden), Bigtem Makine A.S. (Turkey), TNA Australia Pty Limited (Australia), and Hosokawa Micron B.V. (Netherlands).

Food Processing Equipment Market, by Type

Food Processing Equipment Market, by Mode of Operation

Food Processing Equipment Market, by Geography

This study focuses on market assessment and opportunity analysis by analyzing the sales of food processing equipment across type, mode of operation, and geography in terms of both value (USD billion) and volume (million units). It provides market sizes and forecasts for each segment across five key geographies (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa) along with key countries. The study also offers a competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, and key growth strategies adopted over the past 3–4 years.

The global food processing equipment market was valued at USD 73.36 billion in 2025. This market is expected to reach USD 129.47 billion by 2036 from an estimated USD 77.24 billion in 2026, at a CAGR of 5.3% (in terms of value) from 2026 to 2036. In terms of volume, the market is expected to reach 3.45 million units by 2036, at a CAGR of 3.1% from 2026 to 2036.

The meat, poultry, and seafood processing equipment segment is expected to hold the largest share of the overall food processing equipment market, attributed to growing global meat production, strong processed meat demand, food safety investment requirements, and consumer preference for protein-rich food products.

The beverage processing equipment segment is projected to register the fastest CAGR during the forecast period, driven by increasing demand for alcoholic beverages, growing consumption of ready-to-drink beverages, rising per capita spending in developing markets, and the adoption of advanced processing technologies.

The automatic segment is expected to witness the fastest growth during the forecast period, driven by increasing demand for higher efficiency, improved food safety, reduced labor costs, and the elimination of human error and cross-contamination in food manufacturing operations.

The key players operating in the food processing equipment market are Bühler AG (Switzerland), Marel hf (Iceland) – now part of JBT Marel Corporation, GEA Group Aktiengesellschaft (Germany), Bucher Industries AG (Switzerland), John Bean Technologies Corporation (U.S.) – now JBT Marel Corporation, The Middleby Corporation (U.S.), Heat and Control Inc. (U.S.), SPX Flow, Inc. (U.S.), Alfa Laval AB (Sweden), Krones AG (Germany), Paul Mueller Company (U.S.), Tetra Pak International S.A. (Sweden), Bigtem Makine A.S. (Turkey), TNA Australia Pty Limited (Australia), and Hosokawa Micron B.V. (Netherlands).

Asia-Pacific is slated to register the highest CAGR of 6.1% during the forecast period of 2026–2036, driven by tremendous growth in its food and beverage industry, primarily fueled by increasing urbanization, growing health awareness, rising disposable income levels, and government support for food processing industry development. Emerging economies in Latin America, Southeast Asia, and Africa also present significant growth opportunity markets.

Published Date: Feb-2026

Published Date: Feb-2025

Published Date: Jan-2025

Published Date: Jan-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates