Resources

About Us

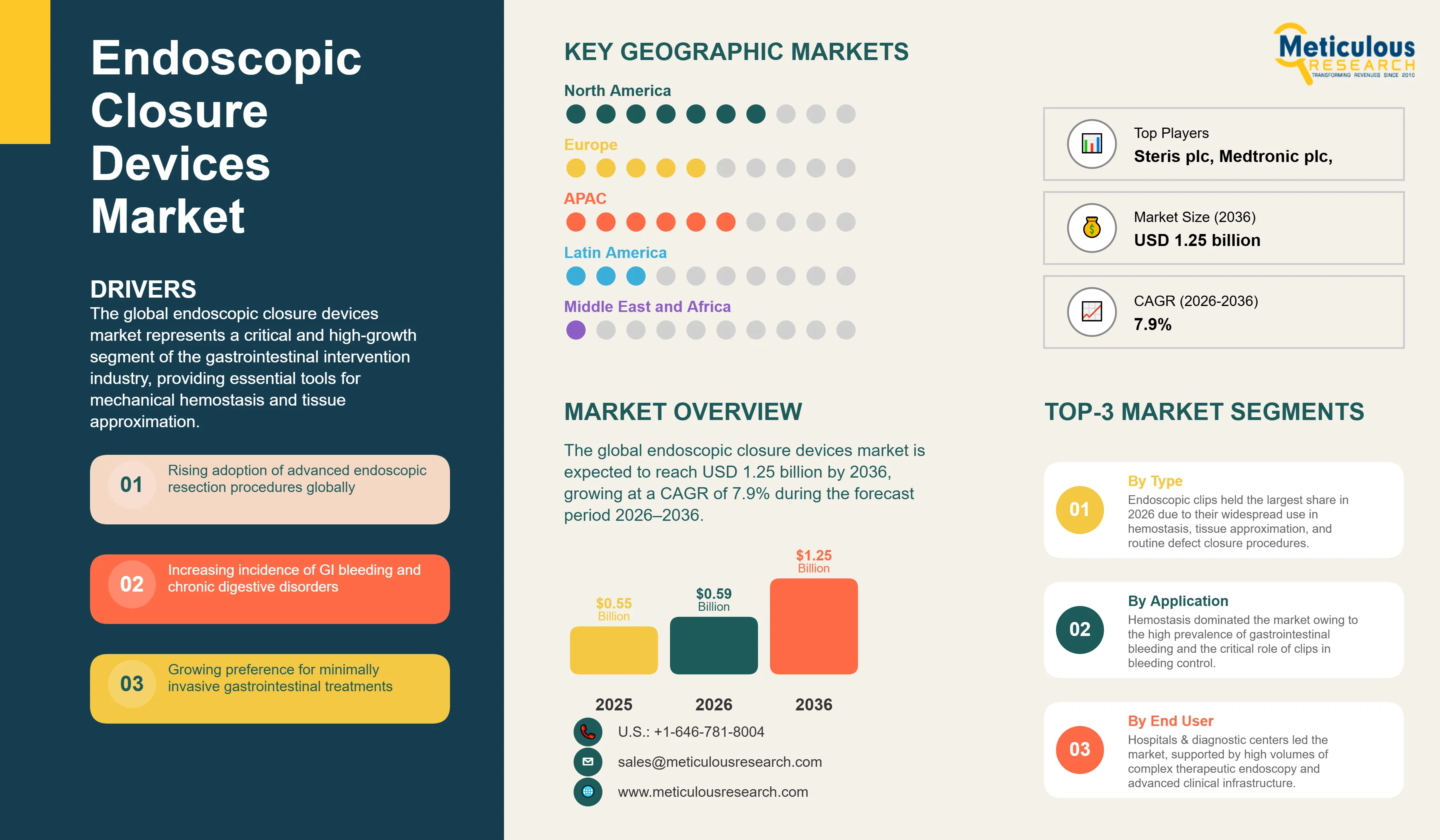

The global endoscopic closure devices market is estimated to be USD 0.59 billion in 2026. This market is expected to reach USD 1.25 billion by 2036, growing at a CAGR of 7.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global endoscopic closure devices market represents a critical and high-growth segment of the gastrointestinal intervention industry, providing essential tools for mechanical hemostasis and tissue approximation. Endoscopic closure devices, ranging from traditional through-the-scope clips to advanced over-the-scope systems and suturing devices, have revolutionized the management of gastrointestinal bleeding, perforations, and mucosal defects. This market is primarily driven by the rising global incidence of gastrointestinal diseases, the increasing adoption of minimally invasive resection techniques (such as EMR and ESD), and the continuous evolution of device designs that offer superior closure strength and precision. According to clinical guidelines from the American Society for Gastrointestinal Endoscopy (ASGE) and the European Society of Gastrointestinal Endoscopy (ESGE), mechanical closure is a cornerstone of safe and effective therapeutic endoscopy. As endoscopists move toward performing more complex endoluminal surgeries, the demand for robust closure systems that can manage full-thickness defects and large mucosal voids is expected to accelerate, supported by technological innovations that enhance device deliverability and procedural efficiency.

The growth of the global endoscopic closure devices market is primarily driven by the clinical shift toward complex endoluminal surgeries and the rising prevalence of gastrointestinal disorders requiring therapeutic intervention.

Rapid Expansion of Complex Endoscopic Resection and Endoluminal Surgery

The increasing adoption of advanced endoscopic resection techniques, such as Endoscopic Mucosal Resection (EMR) and Endoscopic Submucosal Dissection (ESD), is a major driver for the closure devices market. These procedures allow for the minimally invasive removal of early-stage cancers and large polyps but often leave behind significant mucosal defects that require prophylactic closure to prevent delayed complications. Furthermore, the rise of endoluminal surgeries like Peroral Endoscopic Myotomy (POEM) has created a critical need for high-tension closure systems that can safely seal intentional full-thickness incisions, driving the demand for specialized clips and suturing devices in advanced endoscopy units.

Rising Global Incidence of Gastrointestinal Bleeding and Chronic GI Disorders

The high global burden of gastrointestinal bleeding, driven by the widespread use of antiplatelet and anticoagulant medications and the rising prevalence of gastrointestinal disorders, remains a fundamental driver for the market. According to the International Agency for Research on Cancer, approximately 1.9 million new colorectal cancer cases were diagnosed globally in 2022, accelerating colorectal cancer screening and therapeutic endoscopy volumes. Furthermore, approximately 300 million surgical procedures are performed worldwide each year, according to estimates published by the The Lancet Commission on Global Surgery, reflecting the growing demand for minimally invasive interventions. Endoscopic clips remain the standard mechanical tool for achieving rapid hemostasis during acute gastrointestinal bleeding and for tissue closure following polypectomy and other therapeutic endoscopic procedures, creating sustained demand for advanced tissue approximation devices that improve procedural safety and patient outcomes.

Despite their clinical advantages, the adoption of advanced endoscopic closure devices is restrained by high acquisition costs and the steep learning curve associated with complex closure systems.

High Cost of Advanced Over-the-Scope and Suturing Systems

While standard through-the-scope clips are relatively cost-effective, advanced closure systems such as over-the-scope clips (OTSC) and endoscopic suturing devices carry significantly higher price points. In many healthcare systems, especially in developing regions or facilities with limited budgets, the high cost of these single-use devices can be a major barrier to routine adoption. The lack of incremental reimbursement for specialized closure tools in some markets further limits their use to high-risk or emergency scenarios, potentially slowing the growth of prophylactic closure practices.

Technical Complexity and Steep Learning Curve for Advanced Closure Techniques

The effective use of advanced endoscopic closure devices, particularly suturing systems and over-the-scope clips, requires a high level of technical skill and specialized training. The steep learning curve associated with these devices can be a restraint for widespread adoption among general endoscopists. Procedural complexity, such as navigating tortuous anatomy or managing large defects in difficult locations, can lead to longer procedure times and a higher risk of technical failure. The need for continuous education and hands-on training for endoscopists and their support teams remains a significant operational challenge for the market.

Future growth opportunities in the endoscopic closure devices market are centered on the development of innovative disposable technologies and the expansion of advanced endoscopy services in emerging economies.

Development of Next-Generation Multi-Clip and Automated Closure Systems

Innovations in device design present a major opportunity for manufacturers. The development of multi-clip appliers that allow for the deployment of multiple clips without withdrawing the endoscope can significantly improve procedural efficiency and reduce operative times. Furthermore, the creation of more intuitive, automated, or semi-automated closure systems that simplify the closure of large defects can lower the technical barrier for endoscopists, potentially expanding the market for advanced closure devices beyond specialized academic centers to broader community hospital settings.

Expansion of Advanced Endoscopy Services in Emerging Economies

There is a significant opportunity for market expansion in emerging economies, particularly in the Asia-Pacific and Latin American regions. As healthcare infrastructure modernizes and insurance coverage expands, there is a growing demand for advanced gastrointestinal care. Manufacturers that can provide cost-effective yet reliable closure solutions tailored to the needs of these markets are likely to gain a significant competitive advantage. The rising awareness of early-stage cancer screening and the subsequent need for therapeutic endoscopy in these regions represent a vast, untapped potential for the long-term growth of the closure devices market.

Shift Toward Routine Prophylactic Closure of Post-Resection Defects

A prominent trend in 2026 is the increasing clinical consensus toward routine prophylactic closure of large mucosal defects following EMR or ESD. Driven by the goal of reducing delayed bleeding and perforation rates—complications that can lead to costly hospitalizations—endoscopists are more frequently using clips and suturing devices to seal resection sites. This trend is leading to a higher volume of closure device consumption per procedure and is shifting the market focus toward devices that offer superior precision and ease of deployment in difficult-to-reach areas.

Migration of Therapeutic Endoscopy to Specialized Ambulatory Surgical Centers

The migration of routine therapeutic endoscopic procedures from hospitals to specialized ambulatory surgical centers (ASCs) is a significant trend impacting the market. This shift is driven by the need for cost-effective care and the increasing standardization of endoscopic techniques. ASCs are increasingly equipped to handle complex polypectomies and mucosal resections, driving the demand for reliable and easy-to-use closure clips in these settings. This trend is fostering the development of streamlined, procedural-focused closure solutions that align with the high-efficiency workflows of outpatient endoscopy facilities.

Analysis by Product Type

Based on product type, the endoscopic clips segment is expected to hold the largest share of the global endoscopic closure devices market in 2026. This dominant position is driven by the widespread clinical use of through-the-scope clips for routine hemostasis and small defect closure. Their ease of use, established safety profile, and relative cost-effectiveness make them the primary tool in every endoscopy unit. However, the over-the-scope closure systems segment is projected to register the highest CAGR during the forecast period. The increasing volume of complex endoluminal surgeries and the clinical need for robust, full-thickness closure of large defects and perforations are driving the rapid adoption of these advanced systems.

Analysis by Application

By application, the hemostasis segment is expected to hold the largest share in 2026. This segment's leadership is substantiated by the high frequency of gastrointestinal bleeding emergencies, where mechanical closure via clips is a critical and life-saving intervention. However, the endoscopic mucosal defect closure segment is projected to grow at the fastest CAGR during the forecast period. This growth is fueled by the rising adoption of advanced resection techniques like EMR and ESD, where prophylactic closure of the resulting mucosal voids is increasingly performed to optimize clinical outcomes and prevent delayed complications.

Analysis by End User

By end user, the hospitals & diagnostic centers segment is expected to hold the largest share in 2026. The vast majority of complex therapeutic and emergency endoscopic procedures are performed in hospital-based units that have the necessary specialized interventional expertise and advanced facilities. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing global trend toward moving routine therapeutic gastrointestinal care to outpatient settings to improve healthcare efficiency and reduce costs is driving the rapid growth of this specialized segment.

Largest Share: North America

North America is expected to dominate the global endoscopic closure devices market in 2026. This leading position is attributed to the high prevalence of gastrointestinal diseases, well-established reimbursement models for therapeutic endoscopy, and the early adoption of advanced endoscopic techniques. The region benefits from a highly developed healthcare infrastructure and a strong presence of leading medical device manufacturers. Key companies operating in the North America market are Boston Scientific Corporation, Steris plc, Cook Medical, and Medtronic plc.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global endoscopic closure devices market, with a CAGR of 8-10% during the forecast period. This rapid expansion is driven by the high incidence of gastric and esophageal cancers in countries like Japan, South Korea, and China, where advanced resection techniques (ESD) are widely practiced. Increasing healthcare expenditure and the modernization of endoscopy units are further accelerating the adoption of high-end closure systems. Key companies operating in the Asia Pacific market are Olympus Corporation, Fujifilm Holdings, Fujifilm, and various regional partners for global medical device leaders.

The global endoscopic closure devices market is characterized by a mix of major global medical technology corporations and specialized innovative players focusing on advanced tissue management. Competition is primarily focused on improving the closure strength, deliverability, and precision of clips and suturing systems. Key players are investing in next-generation multi-clip appliers and automated closure devices that can simplify complex procedures. There is also a significant emphasis on developing specialized systems for full-thickness closure and management of large mucosal voids. Strategic developments often involve acquisitions of smaller companies with innovative closure technologies or specialized niche applications. Furthermore, manufacturers are increasingly focusing on providing comprehensive procedural support and training programs for endoscopists, which is critical for gaining clinician trust and maintaining market leadership in an increasingly technically demanding field.

Olympus Corporation (Japan), Boston Scientific Corporation (US), Cook Medical (US), Ovesco Endoscopy AG (Germany), Steris plc (Ireland/US), Medtronic plc (Ireland), ConMed Corporation (US), Fujifilm Holdings Corporation (Japan), Hoya Corporation (PENTAX Medical) (Japan), Teleflex Incorporated (US), Apollo Endosurgery, Inc. (US/Boston Scientific), Micro-Tech (Nanjing) Co., Ltd. (China), Wilson Instruments (SHA) Co., Ltd. (China), G-Flex S.A. (Belgium), Medi-Globe GmbH (Germany), Endo-Technik W. Griesat GmbH (Germany), US Endoscopy (Steris) (US), Cantel Medical Corp. (Steris) (US), B. Braun Melsungen AG (Germany), and Laborie Medical Technologies (Canada).

The global market is estimated at USD 0.85 billion in 2026, with a projected growth to USD 1.25 billion by 2036, at a CAGR of 7.9%.

Primary drivers include the increasing adoption of advanced resection techniques like EMR/ESD and the rising global burden of GI bleeding.

Major restraints include the high cost of specialized closure systems and the technical complexity associated with advanced closure procedures.

Opportunities lie in the development of next-generation multi-clip systems and the expansion of advanced endoscopy in emerging economies.

Endoscopic clips are expected to hold the largest share due to their widespread use as a standard tool for routine hemostasis and tissue approximation.

Endoscopic mucosal defect closure is projected to grow at the fastest CAGR, driven by the increasing use of prophylactic closure after complex resections.

Hospitals & diagnostic centers are expected to hold the largest share as the primary setting for complex therapeutic endoscopic procedures.

North America is expected to dominate the market due to high disease prevalence and established reimbursement for therapeutic endoscopy.

Asia Pacific is projected to witness the fastest growth, fueled by high gastric cancer incidence and the practice of advanced resection techniques.

Key trends include the shift toward routine prophylactic closure and the migration of therapeutic endoscopy to specialized ASCs.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rapid Expansion of Complex Endoscopic Resection and Endoluminal Surgery

4.2.1.2. Rising Global Incidence of Gastrointestinal Bleeding and Chronic GI Disorders

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Over-the-Scope and Suturing Systems

4.2.2.2. Technical Complexity and Steep Learning Curve for Advanced Closure Techniques

4.2.3. Opportunities

4.2.3.1. Development of Next-Generation Multi-Clip and Automated Closure Systems

4.2.3.2. Expansion of Advanced Endoscopy Services in Emerging Economies

4.2.4. Trends

4.2.4.1. Shift Toward Routine Prophylactic Closure of Post-Resection Defects

4.2.4.2. Migration of Therapeutic Endoscopy to Specialized Ambulatory Surgical Centers

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Endoscopic Closure Devices Market, by Product Type

5.1. Endoscopic Clips

5.1.1. Through-the-Scope Clips (TTSC)

5.1.2. Over-the-Scope Clips (OTSC)

5.2. Endoscopic Suturing Systems

5.2.1. Endoscopic Suturing Devices

5.2.2. Suturing Accessories & Consumables

5.3. Others

5.3.1. Endoscopic Tissue Sealants

5.3.2. Endoscopic Tissue Adhesives

5.3.3. Endoscopic Closure Loops (Endoloops)

5.3.4. Endoscopic Band Ligation Devices

6. Global Endoscopic Closure Devices Market, by Application

6.1. Hemostasis

6.2. Endoscopic Mucosal Defect Closure

6.3. Perforation & Fistula Closure

6.4. Others

7. Global Endoscopic Closure Devices Market, by End User

7.1. Hospitals & Diagnostic Centers

7.2. Ambulatory Surgical Centers (ASCs)

7.3. Specialty Clinics

8. Global Endoscopic Closure Devices Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share/Ranking Analysis, By Key Player (2025)

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Olympus Corporation

10.2. Boston Scientific Corporation

10.3. Cook Medical

10.4. Ovesco Endoscopy AG

10.5. Steris plc

10.6. Medtronic plc

10.7. ConMed Corporation

10.8. Fujifilm Holdings Corporation

10.9. Hoya Corporation (PENTAX Medical)

10.10. Teleflex Incorporated

10.11. Apollo Endosurgery, Inc.

10.12. Micro-Tech (Nanjing) Co., Ltd.

10.13. Wilson Instruments (SHA) Co., Ltd.

10.14. G-Flex S.A.

10.15. Medi-Globe GmbH

10.16. Endo-Technik W. Griesat GmbH

10.17. US Endoscopy (Steris)

10.18. Cantel Medical Corp. (Steris)

10.19. B. Braun Melsungen AG

10.20. Laborie Medical Technologies

11. Appendix

11.1. Abbreviations

11.2. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Jan-2025

Subscribe to get the latest industry updates