Resources

About Us

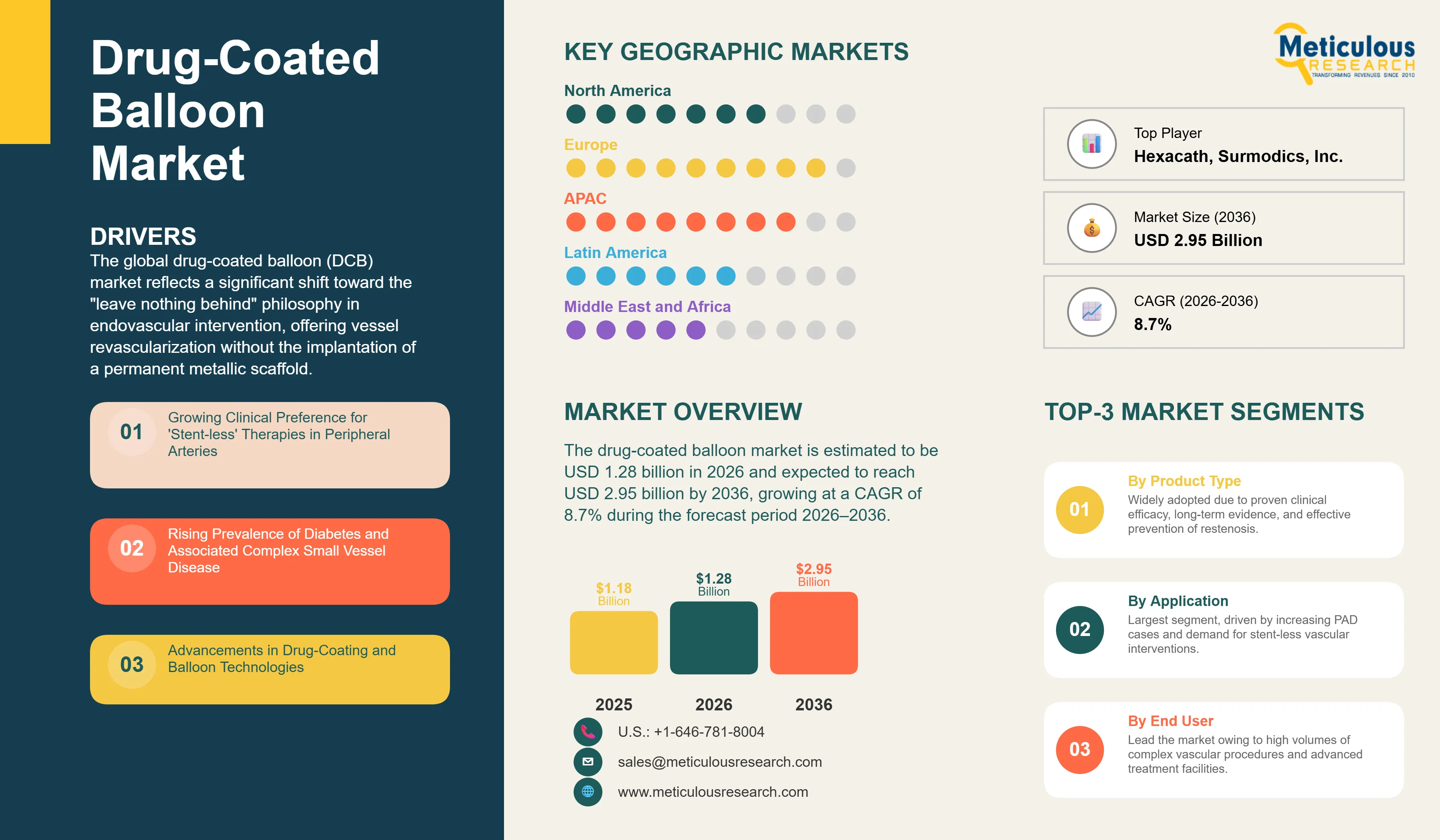

The global drug-coated balloon market is estimated to be USD 1.28 billion in 2026. This market is expected to reach USD 2.95 billion by 2036, growing at a CAGR of 8.7% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global drug-coated balloon (DCB) market reflects a significant shift toward the "leave nothing behind" philosophy in endovascular intervention, offering vessel revascularization without the implantation of a permanent metallic scaffold. DCBs are specialized angioplasty balloons coated with anti-proliferative agents that are rapidly transferred to the vessel wall during inflation, reducing neointimal hyperplasia and minimizing restenosis. This approach has become an established treatment modality in peripheral vascular interventions, particularly in femoropopliteal lesions and selected below-the-knee (BTK) applications, where conventional stents are susceptible to fracture and mechanical stress.

Market growth is being driven by the increasing burden of peripheral artery disease (PAD) and diabetes worldwide. According to the American Heart Association (AHA), more than 230 million people globally are living with PAD, representing a substantial increase over the past two decades. Furthermore, the International Diabetes Federation (IDF) estimates that approximately 643 million adults aged 20–79 years will be living with diabetes by 2030, up from 589 million in 2024, significantly increasing the population at risk for vascular complications and restenosis. Diabetes affects nearly one in four patients with symptomatic PAD and is associated with a higher incidence of below-the-knee disease and repeat interventions.

The continued evolution of drug-delivery technologies and coating formulations has improved drug transfer efficiency and vessel-wall retention, supporting favorable long-term outcomes. Clinical guidelines from the European Society of Cardiology (ESC) and the European Society for Vascular Surgery (ESVS) recognize drug-coated balloons as a recommended treatment option for femoropopliteal in-stent restenosis, while professional societies including the American College of Cardiology (ACC) and the Society for Cardiovascular Angiography and Interventions (SCAI) acknowledge DCBs as an established therapy for coronary in-stent restenosis. In parallel, growing clinical evidence supporting sirolimus-coated balloon platforms is expanding the use of DCBs beyond traditional indications and reinforcing their role in the treatment of small-vessel disease and selected de novo coronary lesions. As physicians increasingly seek to preserve future treatment options and reduce complications associated with permanent implants, adoption of next-generation DCB technologies is expected to accelerate over the coming decade.

Drivers: Addressing Stent-Challenged Anatomies and Preserving Future Treatment Options

The growth of the global drug-coated balloon market is primarily driven by the clinical need for effective alternatives to stenting in complex vascular anatomies and the rising prevalence of diabetes-related vascular disease.

Growing Clinical Preference for 'Stent-less' Therapies in Peripheral Arteries

In many peripheral vascular segments, particularly the superficial femoral artery (SFA) and the popliteal artery, permanent stents are subject to significant mechanical stress, leading to high rates of fracture and restenosis. Drug-coated balloons offer a critical solution by providing local drug delivery to prevent vessel re-narrowing while leaving the vessel in its natural state. This 'stent-less' approach is highly favored by vascular surgeons and interventionalists as it preserves the vessel's integrity and maintains all future surgical and endovascular treatment options, which is particularly important for patients with chronic and progressive vascular disease.

Rising Prevalence of Diabetes and Associated Complex Small Vessel Disease

The global epidemic of diabetes is a major driver for the DCB market, as diabetic patients are highly prone to complex, diffuse, and small vessel disease. In these patients, traditional stenting is often less effective and carries a higher risk of complications. DCBs have shown significant clinical benefit in treating below-the-knee (BTK) disease and small coronary vessels, where they can effectively inhibit restenosis in anatomies that are not suitable for large metal implants. The increasing volume of diabetic patients requiring vascular intervention is creating a sustained demand for advanced drug-delivery balloons that can provide targeted therapy in challenging clinical scenarios.

Restraints: Navigating Regulatory Scrutiny and the High Cost of Specialized Drug-Delivery Systems

Despite their clinical advantages, the adoption of DCBs is restrained by lingering regulatory concerns regarding drug safety and the high economic burden associated with these advanced interventional tools.

Lingering Safety Concerns and Regulatory Scrutiny Regarding Paclitaxel-Coated Devices

The DCB market has faced significant regulatory scrutiny following historical meta-analyses that suggested a potential increase in long-term mortality associated with paclitaxel-coated devices. While subsequent large-scale clinical trials and regulatory reviews by the FDA and EMA have largely reaffirmed the safety and efficacy of these devices, the lingering impact of these concerns can still influence clinical decision-making in certain regions. The need for rigorous, long-term safety data remains a requirement for new device approvals, which can slow the entry of innovative technologies into the market.

High Cost of DCBs and Budgetary Constraints in Healthcare Systems

Drug-coated balloons are significantly more expensive than standard angioplasty balloons. In many healthcare systems, particularly in developing nations, the additional cost of a DCB can be a major barrier to routine use. Budgetary constraints in hospitals often lead to a risk-based approach where DCBs are only used in cases of in-stent restenosis or for specific high-risk patients. The lack of adequate incremental reimbursement for DCBs in some markets further limits their widespread adoption, as facilities may prioritize lower-cost traditional therapies despite their lower clinical efficacy.

Opportunities: Expanding into Coronary Interventions and Advancing Sirolimus-Based Nanotechnology

The future of the DCB market lies in the expansion into primary coronary applications and the development of next-generation sirolimus-coated balloons that offer an improved safety and efficacy profile.

Expansion into Primary Coronary Interventions and Small Vessel Disease

The recent FDA approval of coronary DCBs for in-stent restenosis represents just the beginning of a major opportunity in the coronary space. There is significant potential for the use of DCBs in primary coronary interventions, particularly for small vessel disease and bifurcation lesions where stenting is technically challenging and associated with higher restenosis rates. As more clinical data emerges supporting the 'DCB-only' strategy in specific coronary subsets, the market for these devices is expected to expand significantly, offering a high-growth pathway for manufacturers.

Development of Next-Generation Sirolimus-Coated Balloons with Advanced Nanotechnology

The development of sirolimus-coated balloons (SCBs) offers a major growth opportunity. Sirolimus has a wider therapeutic window and potent anti-inflammatory properties compared to paclitaxel, but its lower lipophilicity has historically made it difficult to deliver via a balloon. Innovations in nanotechnology and advanced excipients are now allowing for effective sirolimus transfer and retention in the vessel wall. These next-generation SCBs are expected to gain significant market share as they provide a safer and potentially more effective alternative for both peripheral and coronary applications, particularly in patients where paclitaxel may be less desirable.

Rapid Clinical Adoption of Sirolimus-Coated Balloons in Complex Interventions

A key trend in 2026 is the accelerating adoption of sirolimus-coated balloons (SCBs) as physicians seek alternatives to paclitaxel-based technologies. Growing clinical evidence and new product launches are supporting their use in complex lesions, particularly below-the-knee (BTK) disease and coronary in-stent restenosis. According to the International Diabetes Federation (IDF), 589 million adults were living with diabetes in 2024, a population highly susceptible to diffuse and BTK peripheral artery disease. Results from multiple European studies and the PRESTIGE and SELUTION clinical programs have demonstrated favorable patency and low target lesion revascularization rates, encouraging broader physician acceptance. In addition, the 2024 ESC Guidelines for Peripheral Arterial and Aortic Diseases recognize drug-coated technologies as important components of endovascular therapy, reinforcing the industry's shift toward next-generation sirolimus-based drug-delivery platforms.

Shift Toward Outpatient Peripheral Vascular Procedures in ASCs

The migration of peripheral vascular interventions from hospitals to ambulatory surgical centers (ASCs) is becoming an important trend shaping DCB demand. This transition is being driven by cost-containment initiatives and favorable reimbursement policies. According to the U.S. Centers for Medicare & Medicaid Services (CMS), the number of procedures eligible for reimbursement in ASCs has expanded steadily, supporting the movement of minimally invasive vascular procedures to outpatient settings. The Ambulatory Surgery Center Association (ASCA) estimates that more than 6,300 Medicare-certified ASCs operate across the United States, providing substantial capacity for outpatient interventions. DCBs are particularly well suited to this environment because they enable effective vessel revascularization without leaving a permanent implant, facilitating shorter procedure times and same-day discharge. As healthcare systems emphasize lower-cost care delivery, manufacturers are increasingly tailoring products and commercialization strategies toward outpatient vascular facilities.

Analysis by Product Type

Based on product type, the paclitaxel-coated balloons segment is expected to hold the largest share of the global drug-coated balloon market in 2026. This dominant position is supported by decades of clinical experience and extensive long-term data that have established paclitaxel as a highly effective anti-proliferative agent for vascular applications. Its lipophilic properties allow for rapid and effective drug transfer during short balloon inflations, making it the current standard of care in peripheral interventions. However, the sirolimus-coated balloons segment is projected to register the highest CAGR during the forecast period. The increasing clinical preference for sirolimus due to its wider therapeutic window and the development of innovative nanotechnology-based delivery systems are driving its rapid adoption, particularly in coronary and complex peripheral cases.

Analysis by Application

By application, the peripheral artery disease (PAD) segment is expected to hold the largest share in 2026. PAD is the primary driver for DCB adoption, as these devices provide a critical solution for anatomies where stenting is technically challenging or associated with high failure rates. The 'leave nothing behind' approach is particularly valuable in the long and tortuous vessels of the legs. However, the coronary in-stent restenosis (ISR) segment is projected to grow at the fastest CAGR during the forecast period. The recent regulatory approvals of coronary DCBs in major markets like the U.S. and the rising volume of complex coronary interventions have created a high-growth opportunity for DCBs as a preferred treatment for ISR, where they can effectively inhibit restenosis without adding additional metal layers.

Analysis by End User

By end user, the hospitals & cardiac centers segment is expected to hold the largest share in 2026. The vast majority of complex vascular procedures requiring DCBs are performed in hospital-based catheterization labs that have the necessary interventional expertise and advanced imaging infrastructure. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing global trend toward moving minimally invasive vascular care to outpatient settings to improve efficiency and reduce costs is driving the rapid growth of this segment, as DCBs are highly suitable for the streamlined workflows of outpatient vascular facilities.

Geographic Analysis: European Leadership and Asia-Pacific's Rapid Adoption of Advanced Vascular Care

Largest Share: Europe

Europe is expected to dominate the global drug-coated balloon market in 2026, accounting for approximately 42% of total revenue. This leadership is supported by the region's early adoption of DCB technology through CE Mark approvals and a long-standing preference among European interventionalists for "leave-nothing-behind" treatment strategies. Europe performs a high volume of peripheral artery disease interventions, while clinical practice guidelines from the European Society of Cardiology (ESC) and the European Society for Vascular Surgery (ESVS) recognize drug-coated balloons as established treatment options for coronary in-stent restenosis and selected femoropopliteal lesions. Germany, Italy, France, and the UK represent major centers of DCB utilization, supported by strong physician awareness and extensive clinical evidence. Key companies operating in the European market include B. Braun Melsungen AG, Biotronik SE & Co. KG, Medtronic plc, Koninklijke Philips N.V., Cordis, Concept Medical, and iVascular S.L.U.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global drug-coated balloon market, with a CAGR of 10.8% during the forecast period. This rapid expansion is fueled by the rising prevalence of diabetes and associated vascular complications in China and India, increasing healthcare infrastructure investment, and the entry of innovative regional manufacturers. The high volume of complex coronary cases in Japan also contributes significantly to regional growth. Key companies operating in the Asia Pacific market are Terumo Corporation, Concept Medical, Acotec Scientific, and various regional partners for global medical device leaders.

The global drug-coated balloon market is highly competitive, characterized by a mix of global medical device giants and innovative specialized players focusing on advanced drug-delivery technologies. Competition is centered on improving drug transfer efficiency, enhancing balloon deliverability in complex anatomies, and expanding clinical indications into the coronary and neurovascular spaces. Key players are investing heavily in large-scale, long-term clinical trials to differentiate their products and gain regulatory approvals in new markets. The market is also seeing a significant shift toward sirolimus-based systems, with several companies launching next-generation SCBs. Strategic acquisitions of smaller companies with innovative coating technologies or specialized niche applications are a major trend as larger players seek to provide a comprehensive portfolio of 'stent-less' vascular solutions. Furthermore, there is an increasing focus on providing complete procedural sets that combine DCBs with advanced guidewires and lesion preparation tools for optimized clinical outcomes.

Medtronic plc, Boston Scientific Corporation, Becton, Dickinson and Company (BD), Abbott Laboratories, B. Braun Melsungen AG, Cook Medical, Terumo Corporation, Koninklijke Philips N.V. (Royal Philips), Biotronik SE & Co. KG, Cordis (Hellman & Friedman), Concept Medical Inc., Acotec Scientific Holdings Limited, Lepu Medical Technology (Beijing) Co., Ltd., iVascular S.L.U., Cardionovum GmbH, Eurocor Tech GmbH, Hexacath, Surmodics, Inc., Teleflex Incorporated, Endocor GmbH.

The global market is estimated at USD 1.28 billion in 2026, with a projected growth to USD 2.95 billion by 2036, at a CAGR of 8.7%.

Primary drivers include the clinical need for stent-less therapies in complex anatomies and the rising prevalence of diabetes-related vascular disease.

Major restraints include lingering regulatory scrutiny regarding drug safety and the high cost of specialized drug-delivery systems.

Opportunities lie in expanding into primary coronary interventions and developing next-generation sirolimus-based balloons.

Paclitaxel-coated balloons are expected to hold the largest share due to their established safety profile and extensive long-term clinical data.

Coronary in-stent restenosis (ISR) is projected to grow at the fastest CAGR, driven by recent regulatory approvals and the rising volume of complex coronary cases.

Hospitals & cardiac centers are expected to hold the largest share as the primary setting for complex vascular interventions.

Europe is expected to dominate the market due to its early adoption of the technology and strong clinical preference for stent-less therapies.

Asia Pacific is projected to witness the fastest growth, fueled by the rising burden of vascular disease in China and India.

Key trends include the rapid adoption of sirolimus-based systems and the expansion of outpatient endovascular care in ASCs.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Growing Clinical Preference for 'Stent-less' Therapies in Peripheral Arteries

4.2.1.2. Rising Prevalence of Diabetes and Associated Complex Small Vessel Disease

4.2.2. Restraints

4.2.2.1. Lingering Safety Concerns and Regulatory Scrutiny Regarding Paclitaxel-Coated Devices

4.2.2.2. High Cost of DCBs and Budgetary Constraints in Healthcare Systems

4.2.3. Opportunities

4.2.3.1. Expansion into Primary Coronary Interventions and Small Vessel Disease

4.2.3.2. Development of Next-Generation Sirolimus-Coated Balloons with Advanced Nanotechnology

4.2.4. Trends

4.2.4.1. Rapid Clinical Adoption of Sirolimus-Coated Balloons in Complex Interventions

4.2.4.2. Shift Toward Outpatient Peripheral Vascular Procedures in ASCs

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Drug-Coated Balloon Market, by Product Type

5.1. Paclitaxel-Coated Balloons

5.2. Sirolimus-Coated Balloons

6. Global Drug-Coated Balloon Market, by Application

6.1. Peripheral Artery Disease (PAD)

6.2. Coronary In-Stent Restenosis (ISR)

6.3. Coronary Small Vessel Disease

6.4. Neurovascular Interventions

6.5. Others

7. Global Drug-Coated Balloon Market, by End User

7.1. Hospitals & Cardiac Centers

7.2. Ambulatory Surgical Centers (ASCs)

7.3. Specialty Clinics

8. Global Drug-Coated Balloon Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Key Players Strategies

9.2. Market Share Analysis

9.3. Strategic Developments

9.4. Competitive Benchmarking

10. Company Profiles

10.1. Medtronic plc

10.2. Boston Scientific Corporation

10.3. Becton, Dickinson and Company (BD)

10.4. Abbott Laboratories

10.5. B. Braun Melsungen AG

10.6. Cook Medical

10.7. Terumo Corporation

10.8. Koninklijke Philips N.V. (Royal Philips)

10.9. Biotronik SE & Co. KG

10.10. Cordis (Hellman & Friedman)

10.11. Concept Medical Inc.

10.12. Acotec Scientific Holdings Limited

10.13. Lepu Medical Technology (Beijing) Co., Ltd.

10.14. iVascular S.L.U.

10.15. Cardionovum GmbH

10.16. Eurocor Tech GmbH

10.17. Hexacath

10.18. Surmodics, Inc.

10.19. Teleflex Incorporated

10.20. Endocor GmbH

11. Appendix

11.1. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Sep-2024

Subscribe to get the latest industry updates