Resources

About Us

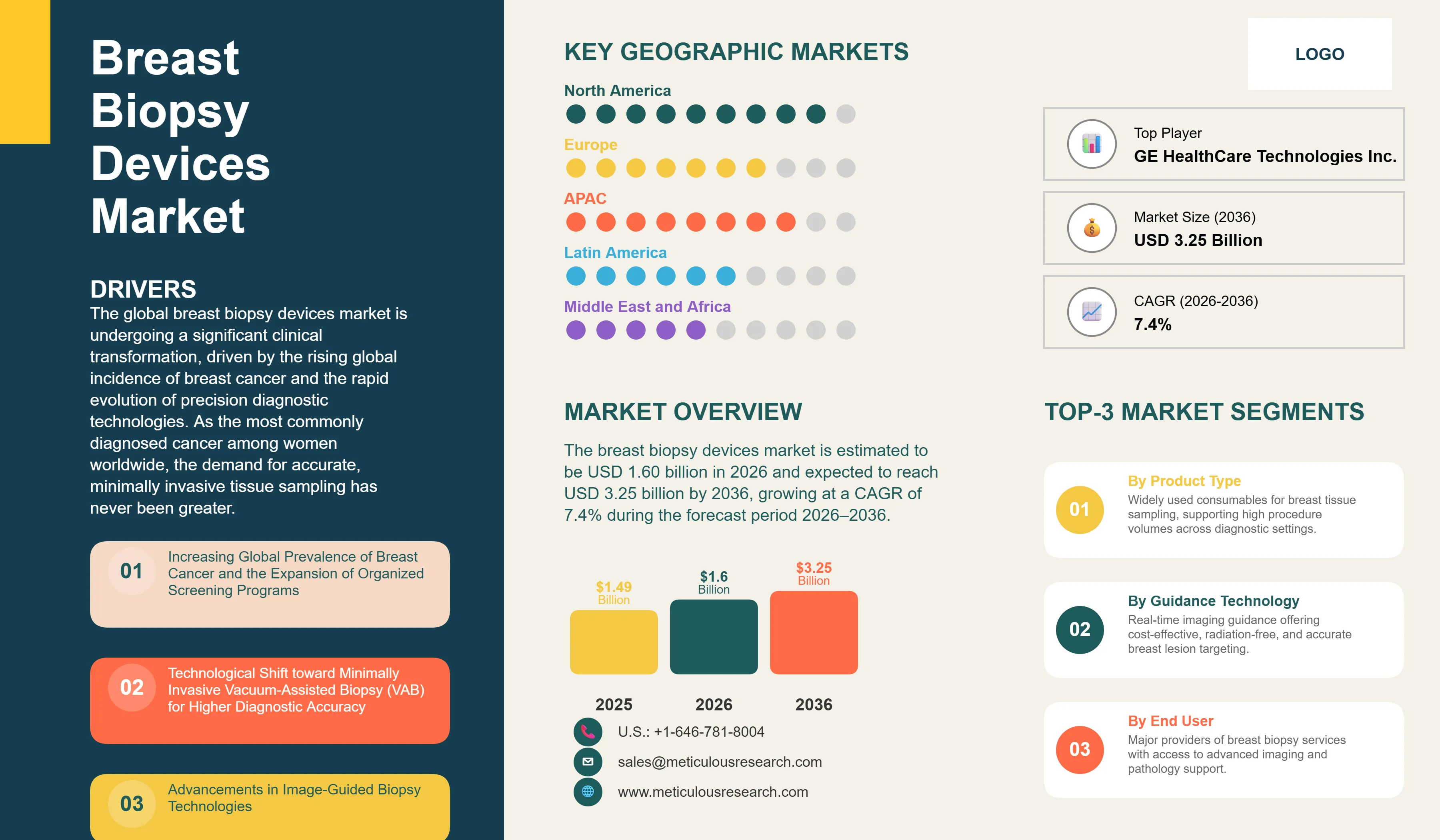

The global breast biopsy devices market is estimated to be USD 1.60 billion in 2026. This market is expected to reach USD 3.25 billion by 2036, growing at a CAGR of 7.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global breast biopsy devices market is undergoing a significant clinical transformation, driven by the rising global incidence of breast cancer and the rapid evolution of precision diagnostic technologies. As the most commonly diagnosed cancer among women worldwide, the demand for accurate, minimally invasive tissue sampling has never been greater. The market is primarily fueled by the increasing adoption of organized screening programs, the shift toward vacuum-assisted biopsy (VAB) systems, and the integration of advanced guidance technologies such as 3D mammography, high-resolution ultrasound, and breast MRI. These innovations are enabling clinicians to detect and biopsy smaller, more complex lesions with higher diagnostic confidence, thereby improving patient outcomes and reducing the need for repeat procedures. Clinical guidelines from the American College of Radiology (ACR), the Society of Breast Imaging (SBI), and the World Health Organization (WHO) increasingly emphasize the importance of early detection and the use of image-guided biopsy as the gold standard for definitive diagnosis. Furthermore, the development of specialized biopsy markers and the migration of diagnostic workflows to outpatient specialized breast centers are enhancing the efficiency and patient-centricity of breast cancer care. As the industry moves toward personalized medicine, the integration of genomic profiling with tissue sampling is expected to further drive the demand for high-quality biopsy devices, ensuring sustained market growth through 2036.

Drivers: Rising Global Incidence of Breast Cancer and the Growing Clinical Preference for Minimally Invasive Vacuum-Assisted Biopsy

The growth of the global breast biopsy devices market is primarily driven by the escalating burden of breast cancer and the rapid adoption of next-generation, high-yield tissue sampling systems.

Increasing Global Prevalence of Breast Cancer and the Expansion of Organized Screening Programs

A major driver for the market is the rising global incidence of breast cancer, which remains the most commonly diagnosed cancer among women worldwide. According to the International Agency for Research on Cancer and the World Health Organization, approximately 2.3 million new breast cancer cases and nearly 670,000 breast cancer-related deaths were reported globally in 2022. This trend is coupled with the widespread implementation of organized breast cancer screening programs, which are increasing the detection of non-palpable and early-stage suspicious lesions requiring tissue diagnosis. Furthermore, the global cancer burden is projected to increase substantially, with more than 35 million new cancer cases expected annually by 2050, representing a 77% increase compared with 2022 levels. Government initiatives promoting early detection and screening participation, along with growing public awareness regarding the benefits of regular mammography, are significantly expanding the patient pool for diagnostic biopsy procedures. This consistent volume of screening-detected abnormalities remains a fundamental driver of sustained demand for breast biopsy needles, localization devices, and image-guided biopsy systems.

Technological Shift toward Minimally Invasive Vacuum-Assisted Biopsy (VAB) for Higher Diagnostic Accuracy

The market is significantly driven by the clinical shift toward minimally invasive vacuum-assisted biopsy (VAB) systems. Compared to traditional core needle biopsies, VAB allows for the retrieval of larger, contiguous tissue samples with a single needle insertion, which reduces the risk of sampling error and improves the detection of architectural distortion and microcalcifications. The ability to obtain high-quality tissue specimens with minimal patient trauma is making VAB the preferred choice for complex or small lesions. The continuous innovation in VAB hardware, including the development of smaller, more ergonomic handpieces and faster tissue acquisition cycles, is further accelerating its adoption across clinical settings.

Restraints: High Costs of Advanced Guidance Systems and the Global Shortage of Specialized Biopsy Consumables

Despite its growth potential, the breast biopsy devices market faces challenges related to high capital investment requirements and intermittent supply chain disruptions affecting essential consumables.

Significant Capital Investment for Advanced Image-Guided Biopsy Platforms

A major restraint for the market is the high cost associated with advanced image-guided biopsy systems, particularly stereotactic/3D mammography and MRI-guided platforms. These systems require substantial capital investment, specialized installation, and ongoing maintenance, creating financial challenges for smaller hospitals and diagnostic centers, particularly in low- and middle-income countries. According to the World Health Organization, approximately 90% of high-income countries report comprehensive availability of cancer diagnostic services, compared with less than 15% of low-income countries, highlighting significant disparities in access to advanced diagnostic infrastructure. Furthermore, the need for dedicated imaging suites, specialized personnel, and ongoing service contracts increases the total cost of ownership, limiting the adoption of advanced biopsy technologies in resource-constrained healthcare settings. As a result, access to sophisticated image-guided breast biopsy procedures remains concentrated within larger, well-funded healthcare institutions.

Supply Chain Disruptions and Shortages of Specialized Biopsy Needles and Markers

The market is also impacted by intermittent supply chain disruptions and shortages of specialized biopsy consumables, such as vacuum-assisted needles and biopsy site markers. As highlighted by the American College of Radiology (ACR) and the FDA, shortages of these essential tools can lead to delays in cancer diagnosis and impact patient care. The reliance on a limited number of high-quality manufacturers for these precision instruments makes the market vulnerable to manufacturing delays or logistics challenges. These supply-side constraints can restrain the growth of procedural volumes and pose a significant challenge for healthcare providers in maintaining consistent diagnostic workflows.

Opportunities: Increasing Adoption of MRI-Guided Biopsy for High-Risk Screening and the Expansion of Healthcare Infrastructure in Emerging Economies

Future growth opportunities in the breast biopsy devices market are centered on the expanding role of MRI in high-risk surveillance and the significant untapped potential in emerging geographic regions.

Expanding Role of MRI-Guided Biopsy in High-Risk Surveillance and Dense Breast Tissue Analysis

There is a significant opportunity for market growth driven by the increasing use of breast MRI for screening high-risk patients and those with dense breast tissue. As clinical guidelines increasingly recommend MRI as a supplemental screening tool, the need to biopsy lesions that are only visible on MRI is surging. Manufacturers that can develop more efficient, MRI-compatible biopsy tools and simplified guidance workflows are well-positioned to capitalize on this high-growth niche. The integration of AI-assisted lesion detection with MRI-guided biopsy is further expected to enhance procedural precision and drive demand for specialized guidance systems.

Rising Healthcare Expenditure and Infrastructure Investment in High-Growth Emerging Markets

The expansion of healthcare infrastructure and rising healthcare expenditures in emerging economies, particularly in Asia-Pacific and Latin America, represent a major opportunity. Government-led initiatives to improve cancer care and the increasing establishment of specialized oncology centers in these regions are driving the demand for advanced diagnostic tools. Manufacturers that can offer cost-effective biopsy solutions and provide comprehensive clinical training to local radiologists are likely to lead the next phase of market expansion in these high-potential regions.

Key Trends: Shift toward Outpatient Specialized Breast Centers and the Integration of AI for Precision Needle Guidance

Migration of Diagnostic Biopsy Procedures to Specialized Outpatient Breast Health Centers

A prominent trend in 2026 is the migration of diagnostic breast biopsy procedures from traditional hospital settings to specialized outpatient breast health centers and ambulatory surgical centers (ASCs). These facilities offer a more streamlined, patient-centric environment and are often equipped with the latest integrated biopsy workflows. This trend is driven by the desire to improve patient experience, reduce procedural wait times, and optimize healthcare costs. Manufacturers are increasingly focusing on providing comprehensive, modular biopsy solutions that are tailored to the needs of high-volume outpatient facilities, reflecting a broader market shift toward specialized diagnostic care.

Integration of Artificial Intelligence and Robotic Assistance for Enhanced Needle Placement Precision

The market is witnessing an increasing trend toward the integration of artificial intelligence (AI) and robotic assistance for enhanced needle placement precision. AI algorithms are being used to analyze real-time imaging data and provide clinicians with optimal needle trajectories, particularly for small or difficult-to-access lesions. Robotic-assisted biopsy systems are also emerging to provide more consistent and precise tissue acquisition. This trend is enhancing the diagnostic confidence of radiologists and reducing the risk of procedural complications, marking a significant step toward the digitalization and automation of breast cancer diagnosis.

Analysis by Product Type

Based on product type, the biopsy needles segment is expected to hold the largest share of the global breast biopsy devices market in 2026. This leadership is substantiated by the high procedural volume of core needle and vacuum-assisted biopsies and the status of needles as essential consumables required for every diagnostic procedure. However, the vacuum-assisted biopsy (VAB) systems segment is projected to register the highest CAGR during the forecast period. The increasing clinical preference for minimally invasive procedures that offer higher tissue yields and more definitive results for small or complex lesions is driving the rapid adoption of VAB systems.

Analysis by Guidance Technology

By guidance technology, the ultrasound-guided biopsy segment is expected to hold the largest share in 2026. This dominance is driven by its cost-effectiveness, real-time imaging capabilities, and lack of ionizing radiation, making it the preferred first-line guidance method for most lesions. However, the MRI-guided biopsy segment is projected to register the highest CAGR during the forecast period. The increasing use of breast MRI for screening high-risk patients and the need to biopsy lesions that are only visible on MRI are fueling the surge in demand for specialized MRI-compatible guidance systems.

Analysis by End User

By end user, the hospitals & diagnostic centers segment is expected to hold the largest share in 2026, as these facilities provide a full continuum of care and house multiple guidance technologies. However, the specialized breast centers & ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward outpatient-based, specialized care and the development of integrated, efficient biopsy workflows in these centers are significantly accelerating adoption.

Geographic Analysis: North America's Market Dominance and Asia-Pacific's Rapid Diagnostic Expansion

Largest Share: North America

North America is expected to dominate the global breast biopsy devices market in 2026. This leading position is attributed to its advanced healthcare infrastructure, high awareness of breast cancer screening, and favorable reimbursement policies. The region has a high prevalence of breast cancer and a well-established network of specialized breast centers. Data from the National Institutes of Health (NIH) and the American Cancer Society (ACS) indicate a consistent and high demand for diagnostic biopsy procedures, with over 300,000 new breast cancer cases expected annually in the U.S. alone.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global breast biopsy devices market, with a CAGR of 10-12% during the forecast period. This rapid expansion is driven by increasing healthcare expenditures, rising awareness of early cancer detection, and government-led screening programs in countries like China, India, and Japan. The expansion of healthcare infrastructure and the entry of global manufacturers into these high-growth markets are significantly accelerating adoption. Clinical reports from the World Health Organization (WHO) highlight a significant increase in breast cancer incidence in the APAC region, fueling the surge in investment in diagnostic biopsy capabilities.

The global breast biopsy devices market is characterized by intense competition between established medical technology giants and specialized diagnostic imaging firms. Competition is primarily focused on enhancing the diagnostic yield and safety of biopsy procedures and improving the patient experience through miniaturization and integrated guidance workflows. Key players are investing heavily in R&D to develop next-generation vacuum-assisted biopsy systems and advanced MRI-compatible tools to capture the growing specialized and outpatient markets. Strategic developments often involve acquisitions of innovative biopsy marker firms and partnerships with leading breast health centers to validate new diagnostic protocols. Furthermore, there is a growing focus on providing integrated digital solutions that combine AI-assisted lesion detection with precise needle guidance. Manufacturers are also increasingly focusing on comprehensive clinical training programs and robust supply chain management to ensure the successful implementation and consistent availability of their technologies in diverse healthcare settings, which is critical for maintaining market leadership in this rapidly evolving diagnostic field.

Hologic, Inc. (US), Danaher Corporation (Mammotome/Devicor Medical Products) (US), Becton, Dickinson and Company (BD) (US), Merit Medical Systems, Inc. (US), Argon Medical Devices, Inc. (US), Cook Medical LLC (US), Stryker Corporation (US), Olympus Corporation (Japan), FUJIFILM Holdings Corporation (Japan), GE HealthCare Technologies Inc. (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Scion Medical Technologies, LLC (US), Planmed Oy (Finland), Izi Medical Products (US), Tsunami Medical S.r.l. (Italy), Teleflex Incorporated (Z-Medica) (US), Ranfac Corp. (US), Medtronic plc (Ireland/US), AngioDynamics, Inc. (US).

The global market is estimated at USD 1.60 billion in 2026, with a projected growth to USD 3.25 billion by 2036, at a CAGR of 7.4%.

Primary drivers include the rising global incidence of breast cancer and the growing clinical preference for minimally invasive vacuum-assisted biopsy (VAB) systems.

Major restraints include the high capital investment for advanced guidance platforms and the intermittent global shortages of specialized biopsy consumables.

Opportunities lie in the expanding role of MRI-guided biopsy for high-risk screening and the rising healthcare infrastructure investment in emerging markets.

Biopsy needles are expected to hold the largest share due to high procedural volumes and their status as essential diagnostic consumables.

Vacuum-assisted biopsy (VAB) systems are projected to grow at the fastest CAGR, driven by the shift toward high-yield tissue sampling.

Ultrasound-guided biopsy is expected to hold the largest share, supported by its cost-effectiveness and real-time imaging capabilities.

North America is expected to dominate the market due to its advanced screening infrastructure and high breast cancer prevalence.

Asia-Pacific is projected to witness the fastest growth, fueled by rising awareness and government-led cancer screening programs.

Key trends include the migration of procedures to specialized outpatient breast centers and the integration of AI for precision needle guidance.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Global Prevalence of Breast Cancer and the Expansion of Organized Screening Programs

4.2.1.2. Technological Shift toward Minimally Invasive Vacuum-Assisted Biopsy (VAB) for Higher Diagnostic Accuracy

4.2.2. Restraints

4.2.2.1. Significant Capital Investment for Advanced Image-Guided Biopsy Platforms

4.2.2.2. Supply Chain Disruptions and Shortages of Specialized Biopsy Needles and Markers

4.2.3. Opportunities

4.2.3.1. Expanding Role of MRI-Guided Biopsy in High-Risk Surveillance and Dense Breast Tissue Analysis

4.2.3.2. Rising Healthcare Expenditure and Infrastructure Investment in High-Growth Emerging Markets

4.2.4. Trends

4.2.4.1. Migration of Diagnostic Biopsy Procedures to Specialized Outpatient Breast Health Centers

4.2.4.2. Integration of Artificial Intelligence and Robotic Assistance for Enhanced Needle Placement Precision

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Breast Biopsy Devices Market, by Product Type

5.1. Biopsy Needles

5.1.1. Core Needle Biopsy (CNB) Needles

5.1.2. Fine Needle Aspiration (FNA) Needles

5.1.3. Localization Needles/Wires

5.2. Vacuum-Assisted Biopsy (VAB) Systems

5.2.1. Console-Based VAB Systems

5.2.2. Handheld VAB Systems

5.2.3. Disposable VAB Probes

5.3. Biopsy Markers

5.3.1. Metallic Markers

5.3.2. Bioabsorbable Markers

5.3.3. Hydrogel Markers

5.4. Others

5.4.1. Biopsy Guidance Grids & Accessories

5.4.2. Specimen Collection Devices

5.4.3. Ancillary Biopsy Instruments

6. Global Breast Biopsy Devices Market, by Guidance Technology

6.1. Ultrasound-Guided Biopsy

6.2. Mammography/Stereotactic-Guided Biopsy

6.3. MRI-Guided Biopsy

6.4. Others

7. Global Breast Biopsy Devices Market, by End User

7.1. Hospitals & Diagnostic Centers

7.2. Specialized Breast Centers & Ambulatory Surgical Centers (ASCs)

8. Global Breast Biopsy Devices Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share/Ranking Analysis, By Key Player (2025)

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Hologic, Inc.

10.2. Danaher Corporation (Mammotome)

10.3. Becton, Dickinson and Company (BD)

10.4. Merit Medical Systems, Inc.

10.5. Argon Medical Devices, Inc.

10.6. Cook Medical LLC

10.7. Stryker Corporation

10.8. Olympus Corporation

10.9. FUJIFILM Holdings Corporation

10.10. GE HealthCare Technologies Inc.

10.11. Siemens Healthineers AG

10.12. Koninklijke Philips N.V.

10.13. Scion Medical Technologies, LLC

10.14. Planmed Oy

10.15. Izi Medical Products

10.16. Tsunami Medical S.r.l.

10.17. Teleflex Incorporated (Z-Medica)

10.18. Ranfac Corp.

10.19. Medtronic plc

10.20. AngioDynamics, Inc.

11. Appendix

11.1. Disclaimer

12. Key Questions Answered

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: May-2026

Published Date: Jan-2025

Published Date: Jan-2025

Subscribe to get the latest industry updates