Resources

About Us

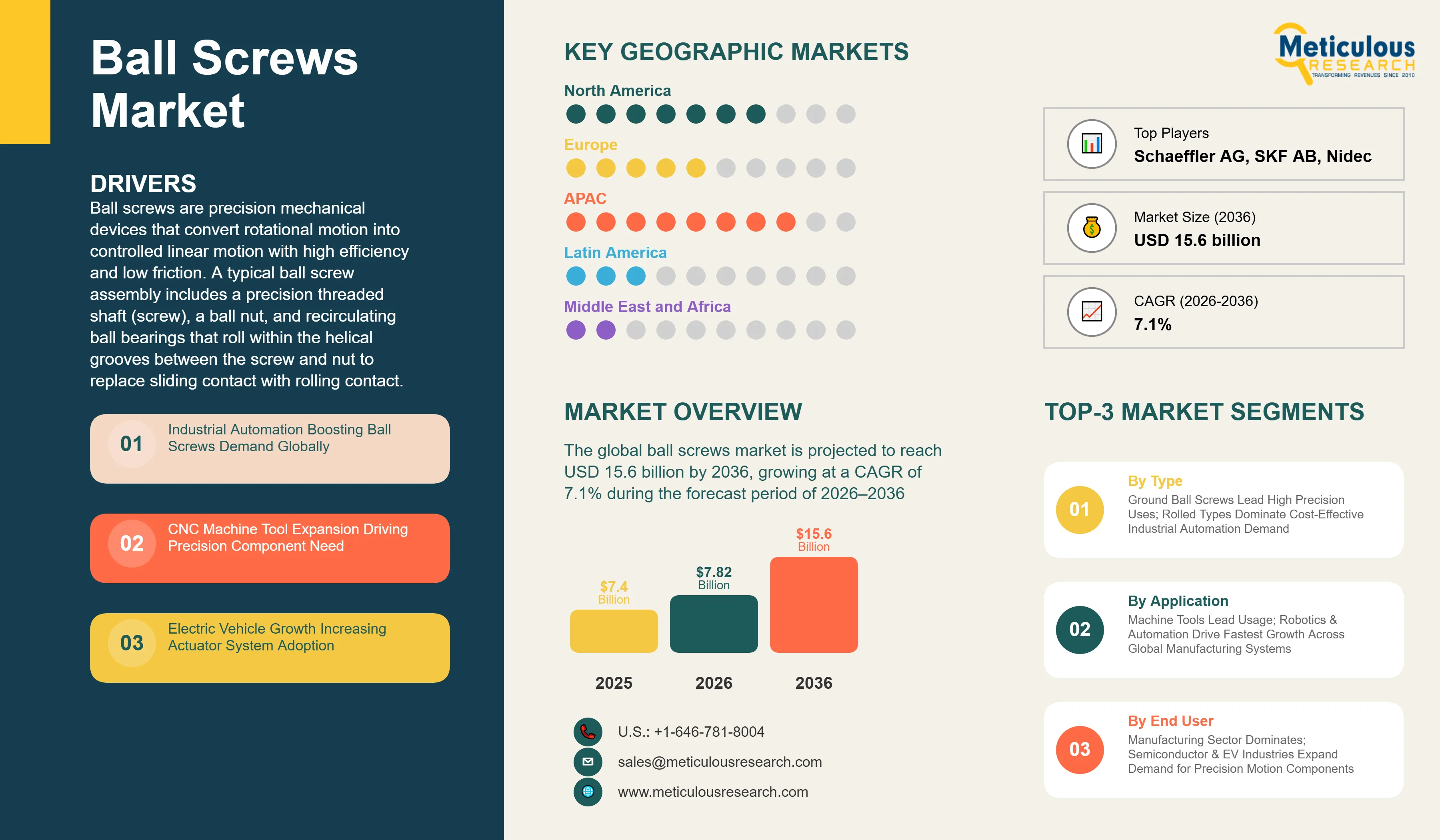

The global ball screws market was valued at USD 7.40 billion in 2025. This market is estimated to reach USD 7.82 billion in 2026 and is projected to reach USD 15.6 billion by 2036, growing at a CAGR of 7.1% during the forecast period of 2026–2036

Ball screws are precision mechanical devices that convert rotational motion into controlled linear motion with high efficiency and low friction. A typical ball screw assembly includes a precision threaded shaft (screw), a ball nut, and recirculating ball bearings that roll within the helical grooves between the screw and nut to replace sliding contact with rolling contact. This recirculating mechanism allows ball screws to achieve mechanical efficiencies above 90%, which is much higher than traditional sliding lead screws. They also deliver consistent positioning accuracy, a high load carrying capacity, and smooth motion in both directions under load. These features make ball screws essential in any mechanical system that requires precise and reliable linear movement

Ball screws are made by two main production methods that impact their accuracy and commercial use. Ground ball screws are created by precision grinding the screw shaft after hardening. This process achieves tight dimensional tolerances and an excellent surface finish. Products in this category meet accuracy grades from C0 to C5 as defined by the JIS B 1192 standard and similar ISO classifications. They are used in applications that require high positional accuracy and repeatability, such as CNC machine tool feed axes, semiconductor wafer handling systems, precision medical equipment, and aerospace actuation systems. On the other hand, rolled ball screws are made by cold rolling the thread form onto the screw blank. This method is quicker and more affordable than grinding. Rolled ball screws meet accuracy grades from C7 to C10 and are widely used in general industrial machinery, conventional automation systems, and applications where extreme positioning precision is not as important

Ball screw assemblies has applications in various industries. Machine tools are the primary segment, with ball screws acting as the main linear positioning mechanism in CNC machining centers, turning centers, grinding machines, electric discharge machines, and milling machines. In these cases, the ball screw directly affects the positioning accuracy and surface quality of machined parts. In industrial automation and robotics, ball screws are used in linear actuators, gantry systems, delta robots, multi-axis handling systems, and collaborative robot end-of-arm tooling. For semiconductor equipment, ground ball screws with the highest accuracy grades are used in wafer transport systems, die bonding machines, lithography steppers, and inspection equipment, where sub-micron positional accuracy is crucial. In electric vehicles, ball screws are increasingly used in electric power steering systems and electronic parking brake actuators, replacing hydraulic systems as vehicle electrification progresses

The global ball screws market is witnessing steady growth, mainly driven by rising investment in industrial automation, the expanding electric vehicle manufacturing sector, ongoing capital investment in semiconductor production capacity, and the growing use of precision motion control technologies in robotics and medical equipment. Additionally, advancements in high speed ball screw design, hollow shaft configurations with internal cooling, and the integration of embedded condition monitoring systems are enhancing the performance of ball screw products and opening new opportunities in precision manufacturing and industrial automation

Click here to: Get Free Sample Pages of this Report

The global biological seed treatment market was valued at USD 7.40 billion in 2025. This market is estimated to reach USD 15.6 billion by 2036 from USD 7.82 billion in 2026, at a CAGR of 7.1% during the forecast period of 2026–2036

|

Market Size by 2036 |

USD 15.6 Billion |

|

Market Size in 2025 (Base Year) |

USD 7.40 Billion |

|

Market Size in 2026 |

USD 7.82 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of ~7.1% |

|

Dominating Region (2026) |

Asia-Pacific |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Type: Ground Ball Screws (Precision Grade C0–C3, Precision Grade C5); Rolled Ball Screws (Standard Grade C7, Utility Grade C10). By Nut Configuration: Single Nut (Spring Preload, Lead Shift Preload, Oversized Ball Preload); Double Nut (Fixed Position Preload, Variable Position Preload). By Shaft Diameter: Below 16 mm; 16 mm–40 mm; 41 mm–80 mm; Above 80 mm. By End-Use Industry: Machine Tools & Machining Centers; Industrial Automation & Robotics; Semiconductor & Electronics Manufacturing Equipment; Aerospace & Defense; Medical Equipment & Devices; Automotive & Electric Vehicles; Other End-Use Industries. By Geography: North America; Europe; Asia-Pacific; Latin America; Middle East & Africa |

|

Countries Covered |

North America (U.S.; Canada; Mexico); Europe (Germany; Italy; Switzerland; France; U.K.; Rest of Europe); Asia-Pacific (China; Japan; South Korea; Taiwan; India; Rest of Asia-Pacific); Latin America (Brazil; Mexico; Rest of Latin America); Middle East & Africa |

|

Key Companies |

THK Co., Ltd., NSK Ltd., HIWIN Technologies Corp., Bosch Rexroth AG, Schaeffler AG, SKF AB, PMI Group (Precision Motion Industries), TBI Motion Technology Co., Ltd., Kuroda Precision Industries Ltd., Nachi-Fujikoshi Corp., JTEKT Corporation, Tsubaki Nakashima Co., Ltd., Nidec Corporation, KSS Co., Ltd., NB Corporation, Steinmeyer Mechatronik GmbH (part of AMETEK Inc.), Thomson Industries, Inc. (part of Danaher Corporation), Barnes Industries, Inc., Umbra Cuscinetti S.p.A., and SBC Linear Co., Ltd. |

Accelerating Global Industrial Automation Investment and Expansion of Robotics Installations

The constant growth of industrial automation in manufacturing industries drives the demand for ball screws globally. Ball screws are essential components of linear actuation systems in industrial robots, gantry based handling systems, and multi-axis automation equipment. According to the International Federation of Robotics (IFR), global industrial robot installations reached 542,000 units in 2024. This figure is more than double the annual installation volume recorded ten years ago. The total operational stock of industrial robots worldwide reached 4.66 million units, marking a 9% increase compared to the previous year. The IFR predicts that annual robot installations will surpass 700,000 units by 2028. China is the leading market with 54% of all global industrial robot installations in 2024. Meanwhile, India recorded a new annual installation high of 9,100 units in 2024, represent the growth of automation in emerging manufacturing economies. Each new articulated robot installation, linear transfer system, or automated machining cell creates direct demand for ball screw assemblies. This reinforces the connection between global automation investment and ball screw market growth

Continued Capital Investment in CNC Machine Tool Manufacturing Capacity

CNC machine tools are the largest single application for ball screws globally, as they serve as the standard linear positioning mechanism for machine tool feed axes. Global machine tool production and consumption are closely linked to manufacturing capital spending cycles, and investment in machining capacity continues to rise. Manufacturers in the automotive, aerospace, and general engineering sectors upgrade to multi-axis CNC machining centers. Countries such as China, Germany, Japan, South Korea, and the United States are the largest consumers of CNC machine tools. China, the world's biggest machine tool market, is expanding its domestic CNC machine tool manufacturing capability as part of its broader industrial upgrading strategy. The ongoing shift from conventional manual and hydraulically actuated machine tools to fully CNC-controlled machining centers drives demand for precision ground ball screws in feed axis applications

Structural Growth of Electric Vehicle Manufacturing Driving Demand for Electromechanical Actuators

The global shift from internal combustion engine vehicles to battery electric vehicles (BEV) is creating new and increasing demand for ball screw-based electromechanical actuation systems. Ball screws are vital components in electric power steering (EPS) systems, which replace conventional hydraulic power steering. They are standard equipment in all battery electric vehicles because there is no continuously running engine to drive a hydraulic pump. Additionally, ball screws are increasingly used in electric parking brake systems, active chassis control actuators, and brake-by-wire systems as vehicle electrification progresses. According to the International Energy Agency (IEA), global electric vehicle sales exceeded 17 million units in 2024, representing more than 20% of total new car sales worldwide. The IEA anticipates continued strong growth throughout the decade. Global EV sales could exceed 40% of all new passenger car sales by 2030 under current policy paths. This shift in automotive drivetrain technology is creating a sustainable and growing demand for ball screws in the automotive actuation supply chain

Semiconductor Fabrication Capacity Expansion Requiring High-Precision Linear Motion Components

Global investment in semiconductor fabrication capacity has risen sharply due to supply chain diversification policies, government sponsored chip manufacturing programs, and increasing demand from artificial intelligence computing infrastructure. Semiconductor manufacturing equipment, including wafer stepper lithography machines, wafer handling robots, die bonding systems, and precision inspection machines, relies solely on high-accuracy ground ball screws for linear positioning. These applications require the highest accuracy grades (C0–C3 under JIS B 1192), strict contamination control specs, and high reliability standards. The U.S. CHIPS and Science Act, enacted in August 2022, allocated over USD 52 billion in federal funding to support domestic semiconductor manufacturing and research. Similar programs have been announced in the European Union (the EU Chips Act), Japan, South Korea, and India, collectively representing hundreds of billions of dollars in semiconductor fabrication investment over the next decade. This wave of investment is driving significant demand for precision ball screws in semiconductor equipment manufacturing across all major production areas

Development of High-Speed Ball Screws for CNC and Semiconductor Applications

The need for increased machine tool productivity and quicker semiconductor equipment cycles is driving the advancement of ball screw designs capable of operating at higher DN values the product of shaft diameter and rotational speed (rpm). Traditional ball screw designs are limited by ball recirculation dynamics, which restrict maximum operating speeds, especially with larger diameter configurations. Leading manufacturers like THK, NSK, and HIWIN have created proprietary high speed ball screw series. They use better ball recirculation end cap designs, smaller precision balls, and improved lubrication delivery systems. These changes allow for higher operational speeds without sacrificing positioning accuracy or service life. These high speed designs are essential for next-generation five-axis machining centers and advanced semiconductor lithography equipment. In these cases, axis velocity and acceleration performance directly affect equipment throughput

Integration of Hollow-Shaft Designs and Internal Cooling to Address Thermal Errors in Precision Machining

Friction heating during sustained high speed operation causes thermal expansion in ball screw shafts, which is a well-known source of positioning errors in CNC machine tools especially in high duty cycle production environments. Hollow shaft ball screws address this problem by allowing coolant to circulate through the interior of the shaft, dissipating heat before it can lead to dimensional changes. This cooling method keeps the shaft temperature consistent and minimizes thermal elongation, improving positional accuracy and dimensional consistency of machined parts during long production runs. Major manufacturers now offer hollow-shaft ball screw series as standard items for high-productivity machining centers, and their use is growing as machine tool builders include thermal error compensation as a standard feature

Adoption of Embedded Condition Monitoring and Predictive Maintenance Capabilities

The use of ball screws in connected manufacturing environments under Industry 4.0 is increasing the demand for ball screw assemblies with built in sensor systems that can monitor operational conditions in real time. Vibration, acoustic emission, and temperature sensors incorporated into ball screw nut housings can identify early signs of ball screw wear, lubrication loss, and preload issues before this lead to machine downtime or accuracy problems. THK has rolled out its IoT-enabled Mechatro Cloud platform, which connects linear motion components, including ball screws, to cloud-based monitoring systems. This allows for predictive maintenance scheduling based on the actual condition of components rather than fixed time intervals. NSK has also developed condition monitoring sensor systems for ball screws. This move towards digitally connected linear motion components is becoming more popular in automotive, semiconductor, and precision aerospace manufacturing, where unexpected downtime can significantly impact production costs

Asia-Pacific: Largest Market for Ball Screws

Asia-Pacific is the largest market for ball screws. This position comes from the region’s strong role in global CNC machine tool manufacturing and consumption, industrial robot use, semiconductor production, and electronics manufacturing. Japan is home to leading ball screw manufacturers like THK, NSK, Kuroda Precision Industries, Nachi-Fujikoshi, JTEKT, and NB Corporation. Japan's precision engineering industry is a key player in ground ball screw manufacturing. China is the largest consumer of ball screws by volume, thanks to its status as the biggest CNC machine tool market and its fast growth in industrial automation across electronics, automotive, and general manufacturing. According to IFR, China represented about 54% of all global industrial robot installations in 2024. Taiwan plays a crucial role in producing rolled and mid-range ground ball screws through companies like HIWIN Technologies and PMI Group. The island's strong semiconductor and electronics manufacturing also creates significant demand for precision-grade ball screw assemblies. South Korea's electronics, semiconductor, and automotive sectors also contribute to high ball screw consumption

Europe: Precision Engineering and Machine Tool Manufacturing Base

Europe has a mature and skilled market for ball screws, supported by its world class precision engineering, machine tool manufacturing, and automation systems. Germany stands out as the largest national market in the region, bolstered by its competitive machine tool industry, which typically ranks among the top three globally. Its strong automotive and supplier manufacturing base further supports growth. Italy is the second largest machine tool producer in Europe and a major user of ball screws for metalworking machinery, packaging equipment, and precision automation. Switzerland's precision engineering and medical device industries also consume a lot of high-accuracy ground ball screws. Bosch Rexroth AG and Schaeffler AG (INA brand) are leading ball screw manufacturers based in Europe. They have manufacturing facilities in Germany and extensive distribution networks. The European machine tool industry is increasingly integrating direct-drive and electromechanical actuation technologies instead of hydraulic systems, which boosts the demand for ball screw-based linear drive systems.

North America: Fastest-Growing Regional Market

North America is expected to witness the fastest growth during the forecast period. This growth is driven by investments in semiconductor manufacturing, industrial capital spending due to nearshoring, and increasing electric vehicle production. The U.S. CHIPS and Science Act is encouraging the building of new semiconductor wafer fabrication plants in Arizona, Texas, Ohio, and New York. Each facility demands a significant amount of capital for manufacturing equipment that includes precision ball screws. The nearshoring trend, where manufacturers bring production closer to North American markets, is creating demand for factory automation and CNC machining in the United States and Mexico. This trend supports the growth of the ball screw market. In the automotive sector, the rapid growth of battery electric vehicle manufacturing at plants operated by General Motors, Ford, Stellantis, and international companies like Toyota, Honda, BMW, and Volkswagen in the United States and Mexico is increasing the need for ball screws in EPS system manufacturing and assembly automation. Thomson Industries and Barnes Industries are the main domestic ball screw manufacturers in North America, but most high-precision ground ball screws in the region come from imports from Japan and Taiwan

Latin America and Middle East & Africa: Emerging Growth Market

Latin America and the Middle East and Africa are smaller markets for ball screws but are expected to see moderate growth. This growth will likely come from industrial development and investments in manufacturing capabilities. Brazil, Mexico, and Argentina are the main markets in Latin America, driven by automotive production, general industrial machinery, and agricultural equipment. Mexico is especially benefiting from nearshoring investments in automotive and electronics manufacturing. In the Middle East and Africa, the UAE, Saudi Arabia, and South Africa lead the market, supported by the growth of the manufacturing sector and government initiatives for industrial diversification

The report provides a competitive landscape based on an extensive assessment of product portfolios, manufacturing capabilities, geographic presence, and key strategic developments adopted by leading ball screw manufacturers worldwide. The key companies profiled in this market include THK Co., Ltd., NSK Ltd., HIWIN Technologies Corp., Bosch Rexroth AG, Schaeffler AG, SKF AB, PMI Group (Precision Motion Industries), TBI Motion Technology Co., Ltd., Kuroda Precision Industries Ltd., Nachi-Fujikoshi Corp., JTEKT Corporation, Tsubaki Nakashima Co., Ltd., Nidec Corporation, KSS Co., Ltd., NB Corporation, Steinmeyer Mechatronik GmbH (part of AMETEK Inc.), Thomson Industries, Inc. (part of Danaher Corporation), Barnes Industries, Inc., Umbra Cuscinetti S.p.A., and SBC Linear Co., Ltd., among others

These companies compete across a broad range of ball screw configurations, accuracy grades, and end-use applications. Market leaders such as THK, NSK, and HIWIN maintain deep proprietary libraries of ball screw designs, precision grinding and metrology capabilities, and global distribution infrastructure. THK, the originator of the commercial ball screw, holds a particularly strong position in high-accuracy machine tool and semiconductor equipment applications, supported by its extensive patent portfolio and direct sales model in major industrial markets. NSK maintains broad product coverage across ground and rolled ball screw categories and operates dedicated ball screw manufacturing facilities in Japan, the United States, Germany, China, and the United Kingdom. HIWIN Technologies, headquartered in Taiwan, has established a strong position across the machine tool, semiconductor, and industrial automation segments, with manufacturing and sales operations across Asia, Europe, and North America. Bosch Rexroth offers ball screws within its broader electromechanical linear motion systems, often bundled with servo motors and drive electronics, targeting system-level solutions for machine tool and factory automation customers

Ball Screws Market, by Type

Ball Screws Market, by Nut Configuration

Ball Screws Market, by Shaft Diameter

Ball Screws Market, by End-Use Industry

Ball Screws Market, by Geography

The global ball screws market was valued at USD 7.40 billion in 2025 and is estimated to reach USD 7.82 billion in 2026. The market is projected to reach USD 15.6 billion by 2036, growing at a CAGR of 7.1% during the forecast period (2026–2036).

Ground ball screws are expected to account for the largest revenue share in 2026. Their adoption is concentrated in high-value precision applications, including CNC machining center feed axes, semiconductor wafer handling systems, aerospace actuation, and precision medical equipment, where high positional accuracy and repeatability are non-negotiable performance requirements.

The double nut ball screw segment is projected to register the highest growth rate during the forecast period. Increasing demand from high-precision CNC machine tools and advanced industrial automation systems requiring zero-backlash, high-rigidity linear actuation is driving adoption of double nut configurations, which achieve these performance characteristics through controlled mechanical preloading between two adjacent nut assemblies.

The 16 mm–40 mm shaft diameter segment accounts for the largest revenue share of the market, as this range covers the most widely adopted ball screw configurations in standard CNC machine tool feed axes, industrial linear actuators, and general factory automation equipment.

Machine tools and machining centers represent the largest end-use industry segment, as ball screws are the standard linear positioning mechanism across CNC machining centers, turning centers, and grinding machines. This segment's market share is directly linked to global capital expenditure trends in manufacturing and the ongoing upgrade cycle toward multi-axis CNC machining technology.

Industrial automation and robotics is the fastest-growing end-use industry segment during the forecast period. The IFR reports that global industrial robot installations reached 542,000 units in 2024 — more than double the volume recorded ten years earlier — and projects that annual installations will surpass 700,000 units by 2028, creating a structurally growing demand for ball screw-based linear motion components.

Asia-Pacific is expected to account for the largest share of the global ball screws market in 2026, driven by the concentration of CNC machine tool manufacturing, semiconductor fabrication, electronics production, and industrial robot deployment in China, Japan, South Korea, and Taiwan.

North America is projected to register the highest CAGR during the forecast period, driven by accelerating domestic semiconductor fabrication investment under the U.S. CHIPS Act, nearshoring-driven industrial capital expenditure, and expanding electric vehicle manufacturing capacity across the United States and Mexico.

Key companies operating in this market include THK Co., Ltd., NSK Ltd., HIWIN Technologies Corp., Bosch Rexroth AG, Schaeffler AG, SKF AB, PMI Group, TBI Motion Technology Co., Ltd., Kuroda Precision Industries Ltd., Nachi-Fujikoshi Corp., JTEKT Corporation, Tsubaki Nakashima Co., Ltd., Nidec Corporation, KSS Co., Ltd., NB Corporation, Steinmeyer Mechatronik GmbH, Thomson Industries, Inc., Barnes Industries, Inc., Umbra Cuscinetti S.p.A., and SBC Linear Co., Ltd.

Market growth is driven by accelerating global industrial automation and robotics investment, continued capital expenditure in CNC machine tool manufacturing capacity, the structural shift to electric vehicles driving demand for electromechanical actuation systems, and large-scale semiconductor fabrication capacity expansion programs supported by government industrial policy in the United States, European Union, Japan, South Korea, and India.

Key opportunities include the development of high-speed and high-DN ball screw designs for next-generation CNC and semiconductor equipment, the integration of embedded sensor-based condition monitoring systems for predictive maintenance applications, adoption of hollow-shaft internally cooled designs for high-precision machining, and expanding demand for miniature ball screws in growing medical device and semiconductor equipment segments.

Key challenges include competitive pricing pressure from lower-cost rolled ball screw producers, particularly those based in China, the technical complexity of meeting increasingly stringent accuracy grade and contamination control specifications for semiconductor and medical applications, and the potential for substitution by alternative linear motion technologies including linear motors in ultra-high-speed and contact-free positioning applications.

1. Introduction

1.1. Market Definition and Scope

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Industry Experts

2.2.2.2. Country-/Region-Level Analysis Approaches

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Market Analysis, by Type

3.3. Market Analysis, by Nut Configuration

3.4. Market Analysis, by Shaft Diameter

3.5. Market Analysis, by End-Use Industry

3.6. Market Analysis, by Geography

3.7. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Market Drivers

4.2.1. Accelerating Global Industrial Automation Investment and Expansion of Robotics Installations

4.2.2. Continued Capital Investment in CNC Machine Tool Manufacturing Capacity

4.2.3. Structural Growth of Electric Vehicle Manufacturing Driving Demand for Electromechanical Actuators

4.2.4. Semiconductor Fabrication Capacity Expansion Requiring High-Precision Linear Motion Components

4.2.5. Increasing Adoption of Multi-Axis Motion Control in Medical and Aerospace Applications

4.3. Market Restraints

4.3.1. Competitive Pricing Pressure from Lower-Cost Rolled Ball Screw Producers

4.3.2. Substitution Risk from Linear Motor Technology in Ultra-High-Speed Positioning Applications

4.3.3. Cyclical Demand Exposure Tied to Manufacturing Capital Expenditure Cycles

4.3.4. Technical Barriers to Meeting Increasingly Stringent Accuracy and Contamination Specifications

4.4. Market Opportunities

4.4.1. High-Speed and High-DN Ball Screw Development for Advanced Machine Tool and Semiconductor Equipment

4.4.2. Hollow-Shaft Internally Cooled Designs Addressing Thermal Error in High-Productivity Machining

4.4.3. Integration of Embedded Condition Monitoring for Predictive Maintenance Applications

4.4.4. Miniature Ball Screw Expansion into Medical Devices and Next-Generation Semiconductor Equipment

4.4.5. Electromechanical Actuation Adoption in Automotive Replacing Hydraulic Systems

4.5. Market Challenges

4.5.1. Demonstrating Long-Term Total Cost of Ownership Advantages Over Alternative Technologies

4.5.2. Managing Supply Chain Concentration and Raw Material Quality for Precision Shaft Production

4.5.3. Meeting Cleanroom Contamination and Outgassing Requirements for Semiconductor Applications

4.6. Market Trends

4.6.1. Development of High-Speed Ball Screws for Advanced CNC and Semiconductor Applications

4.6.2. Integration of Hollow-Shaft Designs and Internal Cooling to Suppress Thermal Errors

4.6.3. Adoption of Embedded Condition Monitoring and Predictive Maintenance Capabilities

4.6.4. Shift from Hydraulic to Electromechanical Actuation Accelerating Ball Screw Adoption in Automotive

4.6.5. Chinese Domestic Manufacturers Gaining Capability in Mid-Range Ball Screw Segments

4.6.6. Miniaturization Trend Driving Innovation in Small-Diameter Ball Screw Design

4.7. Porter's Five Forces Analysis

4.7.1. Threat of New Entrants

4.7.2. Bargaining Power of Suppliers

4.7.3. Bargaining Power of Buyers

4.7.4. Threat of Substitutes

4.7.5. Competitive Rivalry

4.8. Value Chain Analysis

4.8.1. Raw Material Sourcing (Bearing Steel, Precision Steel Bar Stock)

4.8.2. Screw Shaft Manufacturing (CNC Grinding, Thread Rolling)

4.8.3. Ball Nut and Ball Complement Manufacture

4.8.4. Assembly, Preloading, and Quality Inspection

4.8.5. Distribution and Technical Support to OEM Customers

4.9. Regulatory and Standards Framework

4.9.1. JIS B 1192 Ball Screw Accuracy Grade Standards (Japan)

4.9.2. ISO 3408 Ball Screw Standard

4.9.3. Equipment Safety and CE Marking Requirements for European Industrial Machinery

4.9.4. RoHS and REACH Compliance Requirements for Lubrication and Surface Treatment

4.10. Impact of 2025 U.S. Tariff Policy on Precision Motion Component Supply Chains

5. Ball Screws Market Assessment — by Type

5.1. Overview

5.2. Ground Ball Screws

5.2.1. Precision Grade C0–C3

5.2.2. Precision Grade C5

5.3. Rolled Ball Screws

5.3.1. Standard Grade C7

5.3.2. Utility Grade C10

6. Ball Screws Market Assessment — by Nut Configuration

6.1. Overview

6.2. Single Nut

6.2.1. Spring Preload

6.2.2. Lead Shift Preload

6.2.3. Oversized Ball Preload

6.3. Double Nut

6.3.1. Fixed Position Preload

6.3.2. Variable Position Preload

7. Ball Screws Market Assessment — by Shaft Diameter

7.1. Overview

7.2. Below 16 mm

7.3. 16 mm–40 mm

7.4. 41 mm–80 mm

7.5. Above 80 mm

8. Ball Screws Market Assessment — by End-Use Industry

8.1. Overview

8.2. Machine Tools & Machining Centers

8.2.1. CNC Machining Centers (Vertical & Horizontal)

8.2.2. CNC Turning Centers & Lathes

8.2.3. Grinding Machines

8.2.4. Electrical Discharge Machines (EDM)

8.2.5. Other Machine Tools

8.3. Industrial Automation & Robotics

8.3.1. Industrial Robots & Collaborative Robots

8.3.2. Linear Transfer & Gantry Systems

8.3.3. General Factory Automation Equipment

8.4. Semiconductor & Electronics Manufacturing Equipment

8.4.1. Wafer Handling & Transport Equipment

8.4.2. Lithography & Inspection Equipment

8.4.3. Die Bonding & Packaging Equipment

8.4.4. PCB Assembly Equipment

8.5. Aerospace & Defense

8.5.1. Flight Control & Actuation Systems

8.5.2. Ground-Based Defense Equipment

8.5.3. Aerospace MRO & Testing Equipment

8.6. Medical Equipment & Devices

8.6.1. Surgical Robots & Robotic-Assisted Systems

8.6.2. Diagnostic Imaging Equipment

8.6.3. Dental Milling & Prosthetics Equipment

8.6.4. Laboratory Automation & Analytical Instruments

8.7. Automotive & Electric Vehicles

8.7.1. Electric Power Steering (EPS) Systems

8.7.2. Electronic Parking Brake & Brake-by-Wire Systems

8.7.3. Automotive Assembly & Manufacturing Automation

8.8. Other End-Use Industries

8.8.1. Packaging Machinery

8.8.2. Printing & Converting Equipment

8.8.3. Renewable Energy Equipment

8.8.4. Other Industrial Applications

9. Ball Screws Market Assessment — by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. Italy

9.3.3. Switzerland

9.3.4. France

9.3.5. U.K.

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. South Korea

9.4.4. Taiwan

9.4.5. India

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Argentina

9.5.4. Rest of Latin America

9.6. Middle East & Africa

10. Competition Analysis

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share Analysis (2025)

11. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, SWOT Analysis, Strategic Developments)

11.1. THK Co., Ltd.

11.2. NSK Ltd.

11.3. HIWIN Technologies Corp.

11.4. Bosch Rexroth AG

11.5. Schaeffler AG

11.6. SKF AB

11.7. PMI Group (Precision Motion Industries)

11.8. TBI Motion Technology Co., Ltd.

11.9. Kuroda Precision Industries Ltd.

11.10. Nachi-Fujikoshi Corp.

11.11. JTEKT Corporation

11.12. Tsubaki Nakashima Co., Ltd.

11.13. Nidec Corporation

11.14. KSS Co., Ltd.

11.15. NB Corporation

11.16. Steinmeyer Mechatronik GmbH (part of AMETEK Inc.)

11.17. Thomson Industries, Inc. (part of Danaher Corporation)

11.18. Barnes Industries, Inc.

11.19. Umbra Cuscinetti S.p.A.

11.20. SBC Linear Co., Ltd.

11.21. Others

12. Appendix

12.1. Available Customization

12.2. Related Reports

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates