Resources

About Us

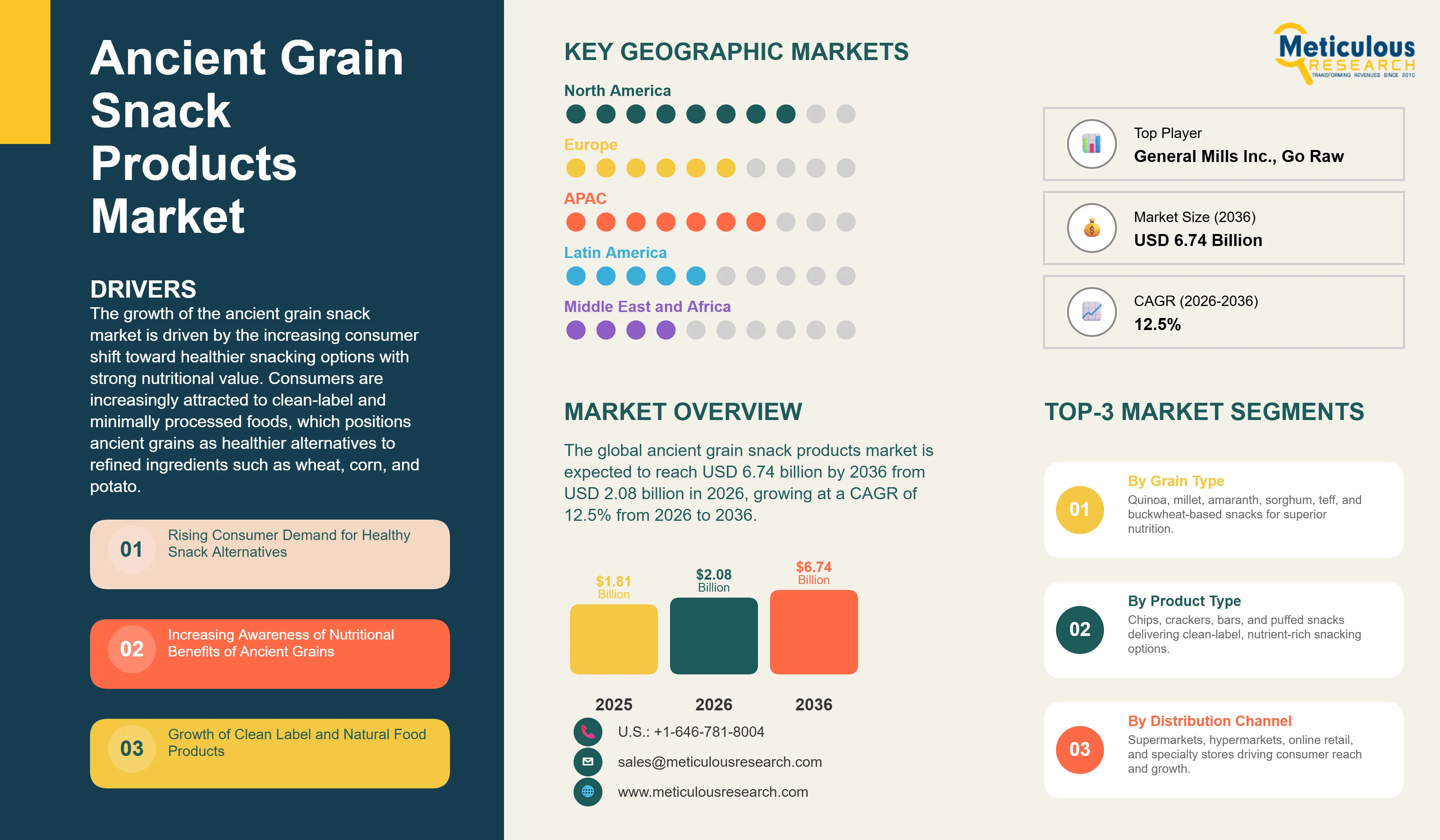

Ancient Grain Snack Products Market by Grain Type (Quinoa, Millet, Amaranth, Sorghum), Product Type (Chips, Crackers, Snack Bars), Distribution Channel, End User, and Geography — Global Forecast to 2036

Report ID: MRFB - 1041851 Pages: 267 Mar-2026 Formats*: PDF Category: Food and Beverages Delivery: 24 to 72 Hours Download Free Sample ReportThe global ancient grain snack products market was valued at USD 1.81 billion in 2025. This market is expected to reach USD 6.74 billion by 2036 from USD 2.08 billion in 2026, growing at a CAGR of 12.5% from 2026 to 2036.

The growth of the ancient grain snack market is driven by the increasing consumer shift toward healthier snacking options with strong nutritional value. Consumers are increasingly attracted to clean-label and minimally processed foods, which positions ancient grains as healthier alternatives to refined ingredients such as wheat, corn, and potato. At the same time, product innovation is expanding the use of ancient grains, including quinoa, millet, amaranth, sorghum, teff, and buckwheat, in familiar snack formats such as chips, crackers, granola bars, and puffed snacks, helping introduce these ingredients to a broader consumer base.

Ancient grain snacks include a wide range of packaged foods in which these grains serve as the primary base ingredient or a key differentiating component. These grains are valued for their strong nutritional profiles. For example, quinoa provides a complete protein source, amaranth offers high-quality protein and calcium, and teff is rich in iron and fiber. Similarly, millet and sorghum are naturally gluten-free and nutrient-rich, while buckwheat contains beneficial antioxidants and a balanced amino acid profile. These nutritional benefits allow manufacturers to position ancient grain snacks as premium, health-focused products, supporting higher price points and appealing to health-conscious consumers.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The ancient grain snack products market is a rapidly growing segment within the global better-for-you snacks industry, driven by increasing consumer demand for healthier, nutrient-rich snack options. Ancient grains such as quinoa, millet, amaranth, and teff are gaining popularity due to their high fiber, protein, and micronutrient content. As consumers increasingly seek snacks that provide both taste and nutritional benefits, ancient grain snacks are becoming positioned at the intersection of the snack and functional food markets.

The competitive landscape includes three key groups of players. Specialty and natural food brands such as Purely Elizabeth, Quinn Snacks, Go Raw, Rhythm Superfoods, Ancient Harvest, and Nature’s Path Foods helped establish the category by introducing organic, clean-label products through natural food retail channels. Large consumer packaged goods companies including PepsiCo, General Mills, Nestlé, and Kellanova have expanded the category by incorporating ancient grains into mainstream snack products and leveraging their strong global distribution networks. In addition, emerging direct-to-consumer brands are using e-commerce and social media platforms to reach health-conscious consumers and build brand awareness.

Ingredient sourcing also plays an important role in this market. Many companies emphasize the origin of grains such as Andean quinoa, Ethiopian teff, and Indian millet to highlight authenticity and sustainability. These sourcing narratives help brands differentiate their products and strengthen their positioning in the premium snack segment.

Expansion of Organic and Non-GMO Ancient Grain Snacks

One of the most important positioning strategies in the ancient grain snack market is combining ancient grain ingredients with organic certification and Non-GMO verification. This creates a strong clean-label value proposition that appeals to health-conscious consumers who prefer natural, minimally processed foods with transparent ingredient lists. Brands such as Nature’s Path Foods, Purely Elizabeth, and Go Raw have successfully built their brand identities around this positioning, allowing them to command premium pricing in the USD 6–10 per package range.

In addition, growing consumer awareness of regenerative agriculture is creating new opportunities for product differentiation. Many ancient grains such as millet, sorghum, amaranth, and teff are naturally aligned with regenerative farming practices due to their drought tolerance, low input requirements, and soil-health benefits. Companies that highlight these sourcing practices can strengthen their sustainability positioning and appeal to consumers seeking environmentally responsible food products.

Premiumization and Functional Positioning of Ancient Grain Snacks

The premiumization trend in the ancient grain snack market reflects a shift from basic healthy snacks to premium functional food products. Ancient grain snacks are increasingly positioned as higher-value products that combine nutritional benefits, authentic ingredients, innovative formulations, and sustainability messaging. As a result, many products in this category command higher price points, with some innovative offerings priced at USD 3–6 per serving, particularly when they incorporate additional functional ingredients such as plant-based proteins, adaptogenic botanicals, prebiotic fibers, and nutrient-dense seeds.

Product innovation is also driving growth in this segment. Manufacturers are enriching ancient grain snacks with protein, probiotics, omega-3 fatty acids, and key micronutrients, allowing these products to compete with functional nutrition bars while still offering familiar snack formats such as chips, crackers, and granola. For example, Purely Elizabeth’s ancient grain granola, which combines organic ancient grains with ingredients like coconut sugar, chia seeds, and hemp hearts, has achieved strong market success at premium price points, demonstrating growing consumer demand for nutrient-rich and functional snack options.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 6.74 Billion |

|

Market Size in 2026 |

USD 2.08 Billion |

|

Market Size in 2025 |

USD 1.81 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 12.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Grain Type, Product Type, Distribution Channel, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Rising Consumer Demand for Healthy Snack Alternatives

A major driver of the ancient grain snack products market is the growing consumer shift toward healthier snacking options that offer real nutritional benefits. Rising cases of lifestyle-related diseases such as obesity, diabetes, and cardiovascular conditions are encouraging consumers to adopt better dietary habits. At the same time, increasing awareness about the health benefits of whole grains and natural ingredients is influencing purchasing decisions, particularly among younger consumers who actively check nutrition labels and prefer transparent ingredient lists.

Ancient grain snacks are well positioned to benefit from this trend because they combine whole grain nutrition, clean-label ingredients, and authentic heritage grains. Products made with grains such as quinoa, millet, and amaranth offer a healthier alternative to conventional snacks made with refined wheat, corn, or potatoes. As a result, consumers are willing to pay premium prices—often 50–150% higher than conventional snacks—for products that provide stronger nutritional value and ingredient transparency. This shift toward better-for-you snack categories is driving sustained growth in ancient grain snack products while traditional high-calorie snack products face increasing market pressure.

Opportunity: Development of Gluten-Free Ancient Grain Snacks

The growing gluten-free food market presents a significant opportunity for the ancient grain snack products market. Demand for gluten-free products is driven not only by consumers with celiac disease, gluten sensitivity, or wheat allergies, but also by a larger group of consumers who adopt gluten-free diets for general health and wellness reasons. Ancient grains such as quinoa, amaranth, millet, sorghum, teff, and buckwheat are naturally gluten-free and offer stronger nutritional benefits compared to many conventional gluten-free snacks that rely on refined ingredients like rice flour, tapioca starch, or potato starch.

With an estimated 1–3% of the population diagnosed with celiac disease and a much larger group, often 6–13% of consumers, following gluten-free diets, the potential consumer base for gluten-free ancient grain snacks is substantial. Companies such as Enjoy Life Foods and Go Raw have demonstrated the commercial potential of this segment by offering gluten-free ancient grain snacks that combine dietary safety with improved nutritional value, helping attract health-conscious consumers seeking better alternatives to traditional gluten-free snack products.

How Does Quinoa Lead the Grain Type Segment?

In 2026, the quinoa segment is expected to hold the largest share of the ancient grain snack products market by grain type. Quinoa’s leading position in the ancient grain snack market is largely due to its strong recognition among health-conscious consumers, particularly in Western markets. Over the past two decades, extensive promotion by quinoa producers, natural food brands, and health-focused media has helped establish quinoa as one of the most popular and trusted ancient grains. Its key advantage is its complete protein profile, as quinoa contains all nine essential amino acids which is an uncommon trait among plant-based foods. This nutritional benefit strongly appeals to consumers who prioritize protein-rich and nutrient-dense snacks. In addition, quinoa is highly versatile and can be used in a wide range of snack formats, including puffed snacks, chips, crackers, granola, and snack bars. This versatility has encouraged both natural food brands and large consumer packaged goods companies to invest in quinoa-based product development, further strengthening its position in the ancient grain snack market.

However, the millet segment is expected to witness the fastest growth during the forecast period, driven by several favorable market developments. Increased promotion by the Indian government, including the recognition of 2023 as the International Year of Millets by the United Nations, has significantly raised global awareness about millet’s nutritional value and sustainability benefits. In addition, growing investments from Indian food startups such as Slurrp Farm, The Whole Truth, and True Elements in millet-based snack products are helping expand the category in both domestic and international health food markets.

Millet also offers strong sustainability advantages. The grain requires less water, grows well in poor soil conditions, and performs well in dry climates, making it an environmentally resilient crop. These characteristics align well with the increasing consumer demand for sustainable and climate-friendly food products, further supporting millet’s rapid growth in the ancient grain snack market.

How Do Ancient Grain Chips Lead the Product Type Segment?

In 2026, the ancient grain chips segment is expected to hold the largest share of the ancient grain snack products market by product type. Ancient grain chips occupy the most commercially accessible product format position in the market, directly substituting for conventional potato and corn chips in the dominant Western snacking occasion while delivering the superior nutritional profile and clean-label positioning that health-conscious consumers seek. Brands including Quinn Snacks, which has built a commercially successful business with its ancient grain popcorn and chip products featuring heirloom corn and ancient grain bases, and Rhythm Superfoods with its vegetable and ancient grain chip products, have demonstrated that ancient grain chip formats can achieve mainstream retail distribution while maintaining premium positioning and meaningful price premiums over conventional chip products.

However, the ancient grain snack bars segment is expected to witness the fastest growth during the forecast period. The nutrition and snack bar market is among the largest and most premium-priced segments of the global snack food industry, with consumers demonstrating established willingness to pay USD 2 to 4 per bar for products that deliver compelling nutritional benefit combinations in convenient portable formats. Ancient grain snack bar products that combine the whole grain and complete protein credentials of quinoa or amaranth bases with complementary nut butters, seeds, dried fruits, and natural sweeteners can command the premium pricing architecture of the established nutrition bar segment while differentiating on ingredient authenticity that conventional bar formulations built on oat, soy, and whey protein bases cannot match. The category is attracting investment from both specialist ancient grain bar brands and the innovation pipelines of large bar market participants including General Mills' Nature Valley and Nestlé's natural snack divisions.

How Do Supermarkets and Hypermarkets Lead the Market?

In 2026, the supermarkets and hypermarkets segment is expected to hold the largest share of the ancient grain snack products market by distribution channel. Mainstream grocery retail provides the highest consumer reach and sales volume for ancient grain snack brands that have achieved sufficient scale and retail brand building to compete effectively for natural food or better-for-you snack aisle placement in major grocery chain networks. The expansion of dedicated natural and organic food sections within mainstream supermarket formats — driven by retailer recognition of the high-margin and consumer traffic-attracting properties of premium health food categories — has created a growing in-store platform for ancient grain snack brands to reach mainstream consumers beyond the core natural food channel customer base. Retailers including Whole Foods Market, Trader Joe's, Sprouts Farmers Market, Target's Good & Gather natural line, and Kroger's Simple Truth organic range have each developed meaningful ancient grain snack assortments that are progressively normalizing the category across broader consumer audiences.

However, online retail is expected to witness the fastest growth during the forecast period. The structural advantages of digital commerce for the ancient grain snack category are compelling: health-conscious consumers who seek out ancient grain products are disproportionately active online shoppers who conduct ingredient and nutritional research before purchasing, making the rich product information environment of e-commerce product pages more commercially effective for ancient grain brands than constrained shelf label communication of physical retail. Thrive Market, which specializes in organic and natural food products at membership-based discount pricing, has become an important distribution channel for ancient grain snack brands, providing access to a curated audience of committed natural food consumers who purchase in multi-unit quantities. The growth of healthy snack subscription box services and curated wellness delivery programs is additionally expanding online discovery and trial opportunities for emerging ancient grain snack brands that lack conventional retail distribution scale.

How Do Health-Conscious Consumers Lead the End User Segment?

In 2026, the health-conscious consumers segment is expected to hold the largest share of the ancient grain snack products market by end user. Health-conscious consumers represent the broadest and most commercially accessible end user segment, encompassing all consumers who actively seek food products that support their health and wellness objectives through nutritional quality and clean-label ingredient integrity, regardless of specific dietary restriction or performance goal. This segment spans demographic groups including urban millennials and Gen Z consumers for whom health-positive food choices are a defining lifestyle attribute, aging baby boomer and Gen X consumers managing chronic disease risk through dietary modification, and parents seeking nutritionally substantive snack options for children that deliver better quality than conventional processed snack products. The breadth of the health-conscious consumer definition creates an addressable market encompassing the large majority of premium snack consumers in developed markets globally.

However, the gluten-free diet consumers segment is expected to witness the fastest growth during the forecast period. The structural growth drivers for gluten-free diet adoption — rising celiac disease diagnosis rates as awareness and testing quality improve, the growing recognition of non-celiac gluten sensitivity as a distinct clinical entity, the mainstream adoption of gluten-free eating as a general wellness strategy, and the elimination of gluten-containing grains in paleo, grain-free, and certain autoimmune protocol dietary frameworks — are creating a rapidly expanding consumer population for whom naturally gluten-free ancient grain snack products represent a nutritionally superior and genuinely satisfying snacking option. Unlike conventional gluten-free snacks built on refined starch bases that deliver adequate palatability but minimal nutritional value, ancient grain gluten-free snacks based on quinoa, amaranth, millet, sorghum, teff, and buckwheat deliver exceptional nutritional quality that addresses the micronutrient deficiency concerns commonly associated with long-term gluten-free dietary patterns.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global ancient grain snack products market. The United States is the primary market driver, supported by the world's most developed natural and specialty food retail infrastructure through which the ancient grain snack category has been built over the past two decades, the large and growing population of health-conscious, nutritionally aware consumers who are the core ancient grain snack target audience, and the concentration of pioneering and commercially successful ancient grain snack brands including Purely Elizabeth, Quinn Snacks, Go Raw, Rhythm Superfoods, Ancient Harvest, and Lundberg Family Farms that have invested in category building and consumer education across natural food retail channels. The U.S. ancient grain snack market benefits from a virtuous cycle of category development: specialist natural food brands pioneer ancient grain snack formats and build consumer awareness in natural retail channels; mainstream CPG companies observe commercial validation and develop ancient grain product lines for broader distribution; and mainstream grocery retailers expand ancient grain snack shelf space responding to consumer demand, further accelerating consumer awareness and category adoption.

General Mills' strategic investment in the ancient grain category through its Nature Valley brand ancient grain granola lines, Nestlé's natural food brand portfolio's inclusion of ancient grain products, and PepsiCo's better-for-you snack innovation programs all reflect the category's established commercial credibility in the North American market and the significant scale resources being committed to its continued development. Canada's well-developed natural food retail sector and its culturally diverse urban population with strong Asian and South Asian communities that have historical familiarity with ancient grain crops as food ingredients contribute meaningfully to regional market leadership alongside the United States' category-defining commercial activity.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the ancient grain snack products market during the forecast period. India represents the most strategically important growth market within Asia-Pacific, driven by the extraordinary alignment between India's cultural heritage of millet and sorghum cultivation and the global health food movement's current fascination with these same grains as nutritional superfoods. The Indian government's Nutri-Cereal and Millets promotion initiatives, including the declaration of 2023 as International Year of Millets under India's UN presidency, catalyzed unprecedented investment in millet-based food product innovation by Indian startups and established FMCG companies including ITC Limited, Marico, and Tata Consumer Products. Brands including Slurrp Farm, The Whole Truth, Yoga Bar, and True Elements are developing sophisticated millet-based and ancient grain snack products for both domestic and international markets, establishing India as an important innovation hub for the global ancient grain snack category.

China's rapidly expanding health food market, driven by the urban middle class's growing nutritional sophistication and the strong cultural resonance of traditional grain foods including various millet and sorghum varieties carrying traditional Chinese medicine health associations, is creating growing domestic demand for premium ancient grain snack products. Japan's highly sophisticated health food market and premium snack culture, South Korea's wellness-oriented food consumer base, and Australia's mature natural food retail sector and growing ancient grain cultivation industry, particularly quinoa and millet grown in Australian agricultural regions suited to these drought-tolerant crops, collectively contribute to Asia-Pacific's broad-based ancient grain snack market growth trajectory. Latin America, home to the traditional growing regions of quinoa and amaranth in Bolivia, Peru, Ecuador, and Mexico, represents both an important supply base and a growing consumption market as urban middle-class consumers in these countries develop awareness of the premium food market value of their traditionally cultivated ancient grain heritage crops.

Some of the key companies operating in the global ancient grain snack products market are PepsiCo Inc., General Mills Inc., Nestlé S.A., Kellogg Company (Kellanova), Nature's Path Foods, Alter Eco Foods, Ancient Harvest, Purely Elizabeth, Quinn Snacks, Go Raw, Rhythm Superfoods, Lundberg Family Farms, Enjoy Life Foods, The Hain Celestial Group, and Bob's Red Mill Natural Foods.

The global ancient grain snack products market is expected to grow from USD 2.08 billion in 2026 to USD 6.74 billion by 2036.

The global ancient grain snack products market is projected to grow at a CAGR of 12.5% from 2026 to 2036.

The quinoa segment is expected to dominate the overall market in 2026, reflecting quinoa's unrivaled consumer recognition among Western health food consumers, its complete protein positioning, and the broad range of commercially established quinoa-based snack product formats. The millet segment is expected to witness the fastest CAGR, driven by the global awareness generated by the International Year of Millets, the strong investment by Indian companies and startups in millet-based snack innovation, and millet's exceptional agricultural sustainability credentials resonating with environmentally motivated premium food consumers.

The ancient grain chips segment is expected to dominate the overall market in 2026, reflecting chips' position as the most familiar and broadly consumed Western snacking format and the most commercially accessible ancient grain product category for mainstream grocery retail distribution. The ancient grain snack bars segment is expected to witness the fastest CAGR, driven by the large and premium-priced global nutrition and snack bar market's receptivity to ancient grain ingredient differentiation and the strong functional benefit positioning achievable with quinoa and amaranth protein combined with complementary seed and nut ingredients.

The supermarkets and hypermarkets segment is expected to dominate the overall market in 2026, providing the highest-volume retail platform for ancient grain snack brands with established mainstream grocery distribution. The online retail segment is expected to witness the fastest CAGR, driven by health-conscious consumers disproportionately active on e-commerce platforms, the rich product information environment of digital retail that supports premium ancient grain product positioning, and the growing healthy snack subscription commerce model that drives strong retention and recurring revenue for specialty ancient grain brands.

The health-conscious consumers segment is expected to dominate the overall market in 2026, representing the broadest addressable consumer base within the premium snacking market. The gluten-free diet consumers segment is expected to witness the fastest CAGR, driven by the expanding gluten-free diet adopter population for whom naturally gluten-free ancient grain snacks represent a nutritionally superior alternative to the refined starch-based gluten-free snack products that currently dominate the gluten-free snack aisle in most retail markets.

North America is expected to lead the global market in 2026, supported by the United States' highly developed natural food retail infrastructure, the established ecosystem of specialist ancient grain snack brands, and the large health-conscious consumer base with strong purchasing power and active nutrition awareness. Asia-Pacific is expected to witness the fastest CAGR, driven by India's extraordinary millet heritage and innovation momentum supported by government promotion programs, China's growing premium health food market, and the broad-based adoption of health-conscious snacking behaviors across urban middle-class consumer segments across the region.

The major players are PepsiCo Inc., General Mills Inc., Nestlé S.A., Kellogg Company (Kellanova), Nature's Path Foods, Alter Eco Foods, Ancient Harvest, Purely Elizabeth, Quinn Snacks, Go Raw, Rhythm Superfoods, Lundberg Family Farms, Enjoy Life Foods, The Hain Celestial Group, and Bob's Red Mill Natural Foods.

Published Date: Mar-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2024

Published Date: Jun-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates