Resources

About Us

Air Receivers Market by Material (Carbon Steel, Stainless Steel), Orientation (Vertical, Horizontal), Pressure Rating (Low, Medium, High), End-User (Manufacturing, Automotive, Food & Beverage, Oil & Gas, Healthcare), and Geography – Global Forecast to 2036

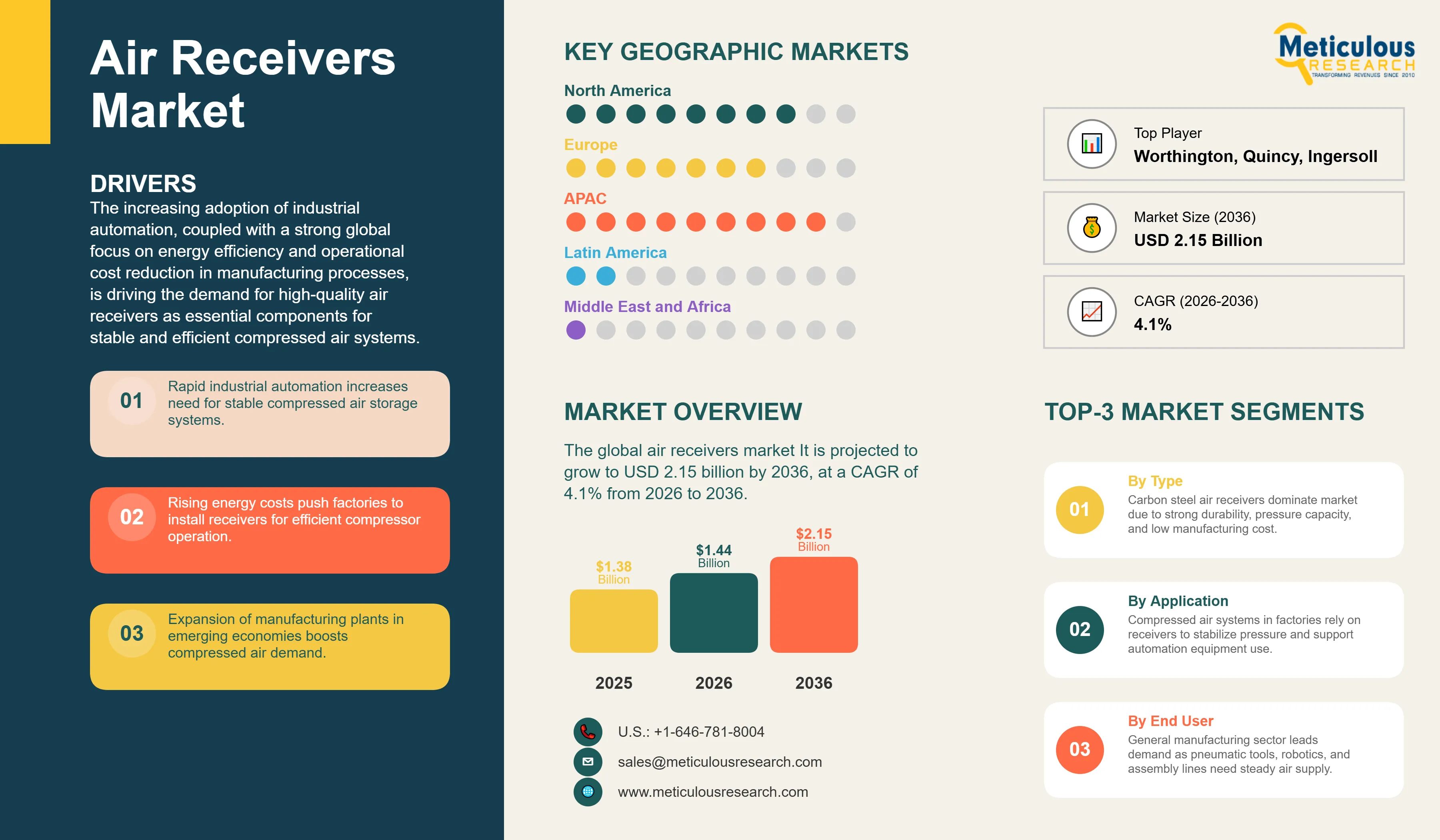

Report ID: MRSE - 1041771 Pages: 189 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global air receivers market was valued at USD 1.38 billion in 2025. It is projected to grow to USD 2.15 billion by 2036 from USD 1.44 billion in 2026, at a CAGR of 4.1% from 2026 to 2036. The increasing adoption of industrial automation, coupled with a strong global focus on energy efficiency and operational cost reduction in manufacturing processes, is driving the demand for high-quality air receivers as essential components for stable and efficient compressed air systems.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

An air receiver, also known as a compressed air tank or vessel, is a fundamental component of virtually every compressed air system. Its primary purpose is to serve as a storage buffer for compressed air, acting as an intermediary between the air compressor and the point of use. This storage capacity allows the system to manage fluctuations in demand, preventing the compressor from cycling too frequently and providing a stable supply of air pressure to downstream equipment. By storing a volume of compressed air, the receiver can supply air to meet short, high-volume demands that exceed the compressor’s capacity, thereby preventing pressure drops that could disrupt sensitive production processes. The key types of air receivers are categorized by their position in the system (wet or dry), their orientation (vertical or horizontal), and their material of construction (primarily carbon steel or stainless steel). Their role is critical not only for meeting peak demand but also for improving the overall energy efficiency and longevity of the entire compressed air system.

The growth of the overall air receivers market is driven by the widespread use of compressed air across a vast array of industries, from general manufacturing and automotive to food & beverage, pharmaceuticals, and oil & gas. As industrial automation continues to expand globally, the reliance on pneumatic tools, robotics, and control systems grows, making a stable and reliable compressed air supply more critical than ever. Furthermore, with rising energy costs and increasing environmental regulations, industrial facilities are under constant pressure to optimize their energy consumption. A properly sized air receiver is a key element in an energy-efficient compressed air system, as it reduces the number of times a compressor needs to start and stop, which is when it consumes the most energy. According to technical sources like Atlas Copco, a well-designed system with adequate storage can significantly reduce energy costs and extend the life of the compressor. This focus on energy efficiency, coupled with industrial growth in emerging economies and the need to upgrade aging infrastructure in developed nations, provides a solid foundation for sustained market growth.

How is Technology Innovation Transforming the Air Receivers Market?

What are the Key Trends in the Air Receivers Market?

Customization for Specific Applications: A significant trend in the market is the increasing demand for customized air receiver solutions tailored to the specific needs of different industries and applications. Standard, off-the-shelf tanks are often not sufficient for specialized processes that may have unique pressure, temperature, or air quality requirements. Manufacturers are increasingly offering custom-engineered solutions, including tanks with special internal coatings for food-grade applications, higher pressure ratings for industries like PET bottle blowing, or specific port configurations to simplify installation. For example, Atlas Copco provides custom high-pressure receivers like their MDA series endee for PET bottling (up to 40 bar), while Ingersoll Rand's CycloStore Visi-Trol models feature specialized coatings for food-grade pharma use. This trend reflects a move towards a more solutions-oriented approach, where manufacturers work closely with end-users to design and build air receivers that are optimized for their specific process.

Emphasis on System-Wide Energy Efficiency: There is a growing recognition that an air receiver is not just a standalone component but an integral part of a larger system. The trend is to look at the compressed air system holistically and optimize all components to maximize energy efficiency. This includes properly sizing the air receiver in conjunction with the compressor, air dryer, and piping system. Leading manufacturers are providing more sophisticated sizing tools and consulting services to help customers design and implement the most energy-efficient system possible. This system-level approach ensures that the air receiver is not just a storage vessel but an active contributor to reducing the overall energy consumption of the facility.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 2.15 Billion |

|

Market Size in 2026 |

USD 1.44 Billion |

|

Market Growth Rate from 2026 to 2036 |

CAGR of 4.1% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Material, Orientation, Pressure Rating, End-User, and Geography |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers

Increasing Industrial Automation and Manufacturing Expansion

The relentless drive towards industrial automation across the globe is a primary driver for the air receivers market. The global industrial automation market is expected to reach around USD 570.4 billion by 2035, at a CAGR of 10.3% from 2025. As industries from automotive to electronics and food processing adopt more robotics, pneumatic controls, and automated assembly lines, the need for a consistent and reliable supply of compressed air becomes paramount. Air receivers are essential to buffer these systems, providing the instantaneous air supply needed for high-speed, intermittent operations without causing pressure drops that could lead to production errors or downtime. The expansion of manufacturing facilities, particularly in emerging economies in Asia-Pacific and Latin America, further fuels this demand. Every new factory or production line that utilizes compressed air requires a corresponding investment in air receivers, making industrial growth a direct and powerful driver for the market.

Growing Emphasis on Energy Efficiency and Cost Reduction

In an environment of rising energy costs and increasing pressure to improve sustainability, industrial facilities are intensely focused on reducing their energy consumption. Compressed air systems are often one of the largest consumers of electricity in a manufacturing plant, and they are also a significant source of energy waste. A properly sized air receiver plays a crucial role in optimizing the efficiency of a compressed air system. By providing storage, it allows the compressor to operate in longer, more efficient cycles and reduces the frequency of energy-intensive startups. This leads to significant energy savings and a lower total cost of ownership. The clear and measurable return on investment from an optimized compressed air system, with the air receiver as a key component, makes it a compelling proposition for facility managers and a strong driver for the market.

High Initial Capital Investment and Space Constraints

Despite the long-term benefits, the initial capital investment required for a high-quality, properly sized air receiver can be a restraint for some companies, particularly small and medium-sized enterprises (SMEs). While the payback period in terms of energy savings can be relatively short, the upfront cost can be a barrier to adoption. Additionally, in existing facilities, space can be a significant constraint. Large air receivers, especially vertical models, require a considerable footprint and ceiling height. Finding a suitable location for the tank that is close to the compressor and integrated into the piping system can be a challenge in crowded industrial environments. These factors can lead some companies to opt for undersized receivers or to forgo a dedicated receiver altogether, which ultimately compromises the efficiency and reliability of their compressed air system.

Lack of Awareness and Perception as a Commodity

In some segments of the market, there is a lack of awareness regarding the critical role that an air receiver plays in the overall performance and efficiency of a compressed air system. It is sometimes viewed as a simple, passive component, a commodity tank, rather than an engineered solution that can deliver significant operational benefits. This perception can lead to decisions based solely on price, resulting in the purchase of undersized or low-quality tanks that do not meet the needs of the system. Overcoming this lack of awareness and educating end-users on the importance of proper sizing and selection is a key challenge for manufacturers. The tendency to focus on the compressor as the primary component of the system, while overlooking the importance of storage, can limit the market’s potential for higher-value, engineered solutions.

Integration of IoT and Smart Monitoring for Predictive Maintenance

The integration of the Internet of Things (IoT) and smart monitoring technologies offers a significant opportunity for the air receivers market. By equipping air receivers with sensors to monitor pressure, temperature, and condensate levels, manufacturers can offer solutions that provide real-time data and predictive maintenance alerts. This allows plant operators to proactively address issues before they lead to downtime, such as detecting leaks or identifying a malfunctioning condensate drain. This data can be integrated into a plant’s overall energy management system, providing a more complete picture of the compressed air system’s performance and identifying further opportunities for optimization. As industries embrace digital transformation and Industry 4.0, the demand for intelligent components that can contribute to a smart factory environment will continue to grow, creating a strong opportunity for advanced air receiver solutions.

Expansion in High-Growth End-User Industries

The rapid growth of specific end-user industries, such as food & beverage, pharmaceuticals, and electronics, creates a significant opportunity for the air receivers market. These industries have stringent requirements for air quality (e.g., oil-free, dry air) and often require specialized materials, such as stainless steel, to prevent contamination. This creates a demand for higher-value, specialized air receivers. For example, the expansion of food and beverage industry, driven by a growing global population and changing consumer preferences, requires significant investment in new processing and packaging facilities, all of which rely heavily on compressed air. Similarly, the growth of the pharmaceutical industry, driven by an aging population and the development of new biologic drugs, also fuels demand for high-purity compressed air systems. Targeting these high-growth sectors with specialized, compliant solutions is a key opportunity for manufacturers.

Why is Carbon Steel the Dominant Material for Air Receivers?

The carbon steel segment holds the largest share of the air receivers market primarily due to its excellent balance of strength, durability, and cost-effectiveness. For the vast majority of industrial applications, carbon steel provides the necessary pressure containment capabilities at a significantly lower cost than stainless steel or other alloys. It is a well-understood material with established manufacturing processes, making it a reliable and economical choice. While it is susceptible to corrosion, this can be managed with proper internal and external coatings and regular condensate draining. The combination of robust performance and economic value makes carbon steel the go-to material for most standard air receiver applications across a wide range of industries.

Why is the Vertical Orientation Segment Expected to Grow Faster?

While both horizontal and vertical air receivers are widely used, the vertical orientation segment is expected to witness slightly faster growth. The primary advantage of a vertical air receiver is its smaller footprint, which is a critical consideration in many industrial facilities where floor space is at a premium. By utilizing vertical space, these tanks can provide a large storage capacity without occupying a significant amount of valuable production area. Additionally, the vertical design facilitates more effective condensate drainage, as gravity helps to collect moisture at the bottom of the tank where it can be easily removed. This improved condensate management helps to protect downstream equipment from moisture and corrosion. As industrial facilities become more densely packed, the space-saving advantage of vertical air receivers will continue to drive their adoption.

How Does the General Manufacturing Sector Drive the Market?

The general manufacturing sector is the largest end-user of air receivers due to the sheer breadth and variety of applications for compressed air in this segment. From powering pneumatic tools and actuators on assembly lines to operating material handling equipment and providing control air for automated processes, compressed air is a ubiquitous utility in manufacturing. The diverse needs of this sector, which includes everything from metal fabrication to plastics and woodworking, create a constant demand for air receivers of all sizes and configurations. The ongoing drive for increased productivity and automation in manufacturing continues to reinforce the reliance on compressed air, and therefore, on the air receivers that are essential for the system’s stability and efficiency.

What is the Role of Air Receivers in the Automotive Industry?

The automotive industry is another major consumer of air receivers. Modern automotive manufacturing is a highly automated process that relies heavily on compressed air. Air receivers are critical for providing the large volumes of instantaneous air required for robotic welding and assembly lines, as well as for powering the pneumatic tools used by workers. The spray painting process, in particular, requires a very stable and clean supply of compressed air to ensure a high-quality finish, and air receivers are essential for dampening any pressure fluctuations that could affect the spray pattern. The high-speed, cyclical nature of automotive production makes a robust compressed air storage system, with air receivers at its core, an absolute necessity.

U.S. Air Receivers Market Size and Growth 2026 to 2036

The U.S. air receivers market is projected to be worth around USD 604 million by 2036, growing at a CAGR of 3.4% from 2026 to 2036.

How is Asia-Pacific Leading the Air Receivers Market?

Asia-Pacific is expected to be the largest and fastest-growing market for air receivers. This is primarily driven by its position as the world’s manufacturing hub. Rapid industrialization, significant foreign investment in new production facilities, and large-scale infrastructure projects in countries like China, India, and Southeast Asian nations are creating a massive demand for compressed air systems. The growth of key end-user industries, such as automotive, electronics, and textiles, in the region is a major factor. Furthermore, as labor costs rise, there is an increasing trend towards automation in Asia-Pacific, which further boosts the demand for compressed air. The combination of strong economic growth, expanding industrial capacity, and a growing focus on improving manufacturing efficiency makes Asia-Pacific the key engine of growth for the global air receivers market.

By Material

By Orientation

By Pressure Rating

By End-User

By Geography

The air receivers market is expected to increase from USD 1.44 billion in 2026 to USD 2.15 billion by 2036.

The air receivers market is expected to grow at a CAGR of 4.1% from 2026 to 2036.

The major players in the air receivers market include Atlas Copco, Ingersoll Rand, Kaeser Kompressoren, and other specialized tank manufacturers. These companies are leaders in compressed air technology and provide a wide range of air receivers and system solutions.

The key driving factors for the market are the increasing adoption of industrial automation, the growing focus on energy efficiency and cost reduction, and the expansion of manufacturing activities in emerging economies.

The Asia-Pacific region will lead the global air receivers market during the forecast period 2026 to 2036.

Published Date: Feb-2026

Published Date: Aug-2025

Published Date: Apr-2025

Published Date: Jan-2025

Published Date: Nov-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates