Resources

About Us

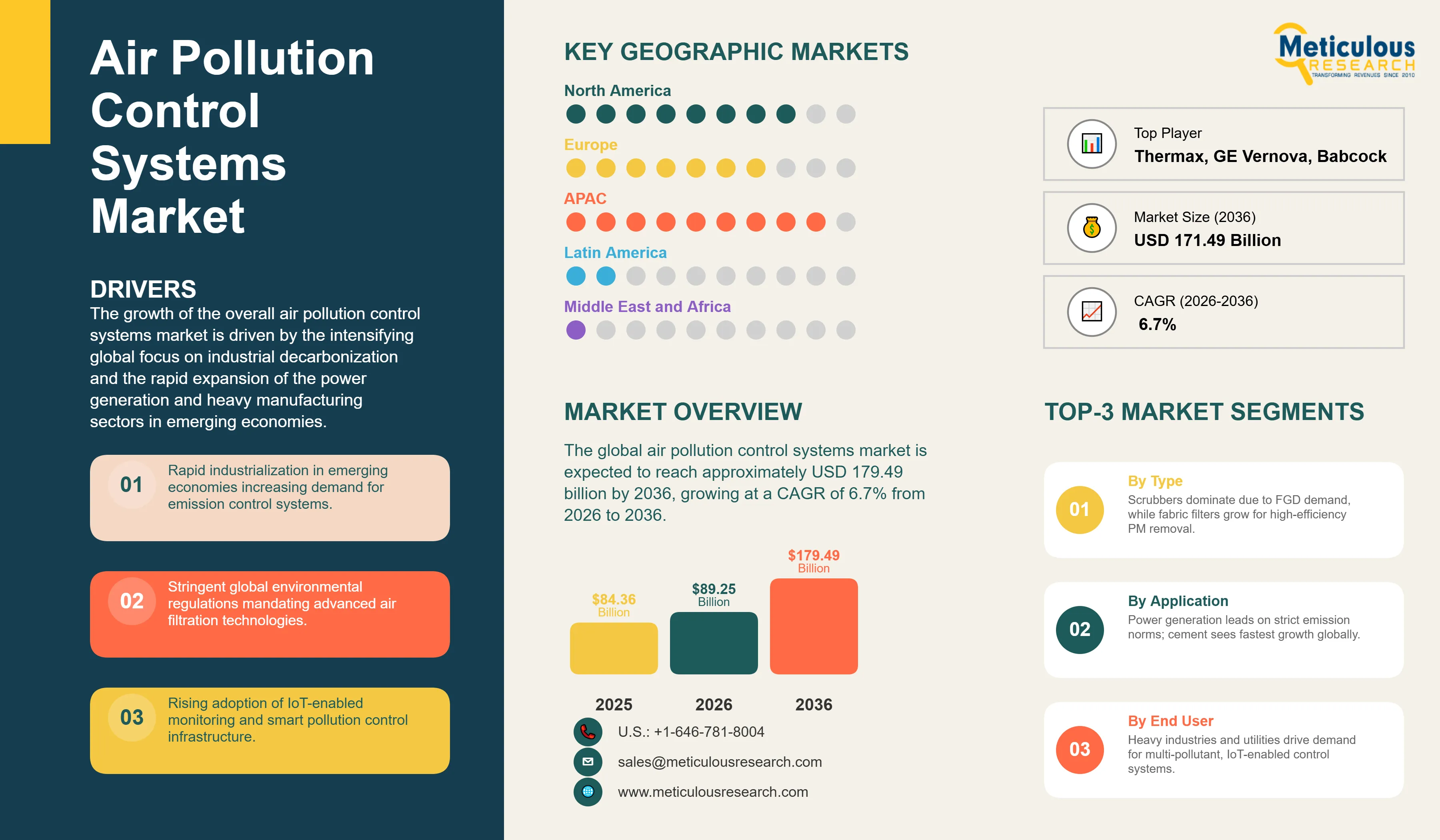

The global air pollution control systems market was valued at USD 84.36 billion in 2025. The market is expected to reach approximately USD 179.49 billion by 2036 from USD 89.25 billion in 2026, growing at a CAGR of 6.7% from 2026 to 2036. The growth of the overall air pollution control systems market is driven by the intensifying global focus on industrial decarbonization and the rapid expansion of the power generation and heavy manufacturing sectors in emerging economies. As manufacturers seek to integrate more functionality into their environmental management substrates and reduce the emission of hazardous pollutants, advanced filtration and scrubbing systems have become essential for maintaining high-speed operational compliance and mechanical durability. The rapid expansion of the industrial infrastructure in Asia-Pacific and the increasing need for high-density multi-pollutant control solutions in coal-fired power plants and advanced cement kilns continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Air Pollution Control Systems are critical environmental protection systems used to provide pollutant removal while allowing for mechanical efficiency and space-saving designs throughout the industrial exhaust process. These systems include scrubbers, electrostatic precipitators (ESPs), fabric filters, and catalytic reactors, which are designed to withstand high-temperature environments and fit into non-linear industrial layouts. The market is defined by high-efficiency technologies such as selective catalytic reduction (SCR) and wet electrostatic precipitation (WESP), which significantly enhance chemical stability and signal performance in high-frequency applications. These systems are indispensable for manufacturers seeking to optimize their internal environmental architecture and meet aggressive emission reduction targets.

The market includes a diverse range of configurations, ranging from simple mechanical collectors for basic dust removal to complex multilayer multi-pollutant systems for high-performance metallurgy and waste-to-energy plants. These systems are increasingly integrated with advanced components such as smart sensors and ultra-fine ceramic filters to provide services such as real-time emission monitoring and improved heat recovery. The ability to provide stable, high-precision filtration while minimizing physical footprint has made advanced air pollution control systems the technology of choice for industries where environmental efficiency and reliability are paramount.

The global industrial sector is pushing hard to modernize production capabilities, aiming to meet AI-driven monitoring and IoT connectivity targets. This drive has increased the adoption of high-density pollution control pipelines, with advanced “smart” scrubbing techniques helping to stabilize production yields for ultra-fine chemical features. At the same time, the rapid growth in the hydrogen and green steel markets is increasing the need for high-reliability, corrosion-resistant environmental solutions.

Proliferation of AI-Driven Monitoring and High-Speed Connectivity

Manufacturers across the environmental industry are rapidly shifting to AI-optimized hardware, moving well beyond traditional filter designs toward high-speed, low-loss digital setups. Mitsubishi Heavy Industries’ latest high-efficiency scrubbers deliver significantly higher data throughput for emission tracking, while Babcock & Wilcox’s recent installations have slashed reagent interference in 5G-enabled industrial plants. The real game-changer comes with “smart” pollution control circuits featuring integrated sensors and shielding capabilities that maintain peak performance even in electromagnetically noisy environments. These advancements make high-precision environmental management practical and cost-effective for everyone from industrial startups to global energy giants chasing operational excellence and lower system weight.

Innovation in Multi-Pollutant and Ultra-Thin Hybrid Systems

Innovation in multi-pollutant and ultra-thin hybrid systems is rapidly driving the air pollution control market, as industrial facilities become more compact and multi-functional. Equipment suppliers are now designing units that combine the structural integrity of traditional ESPs with the versatility of fabric filters in a single assembly, saving valuable internal space and simplifying assembly logistics. These systems often involve advanced laser monitoring and plasma etching capable of handling ultra-fine particles without compromising mechanical strength or electrical reliability.

At the same time, growing focus on sustainable manufacturing is pushing manufacturers to develop pollution control solutions tailored to circular economy principles. These systems help reduce material waste through reagent recovery processes and the use of recyclable substrates. By combining high-density interconnectivity with robust environmental performance, these new designs support both technological advancement and corporate sustainability, strengthening the resilience of the broader industrial value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 171.49 Billion |

|

Market Size in 2026 |

USD 89.25 Billion |

|

Market Size in 2025 |

USD 84.36 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 6.7% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Technology, Pollutant Type, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Industrialization and Rise of Stringent Emission Norms

A key driver of the air pollution control systems market is the rapid movement of the global industrial sector toward cleaner, more sustainable, and highly functional production processes. Global demand for high-purity air, carbon neutrality, and health-monitoring industrial zones has created significant incentives for the adoption of advanced filtration systems. The trend toward “zero-emission” technology and the integration of environmental controls into smart factory patches drive manufacturers toward scalable solutions that air pollution control systems can uniquely provide. It is estimated that as industrial adoption of IoT-enabled monitoring rises and environmental diagnostic tools become more decentralized through 2036, the need for robust, high-capacity filtration increases significantly; therefore, multi-pollutant and SCR systems, with their ability to ensure high-density packaging, are considered a crucial enabler of modern industrial design strategies.

Opportunity: Carbon Capture (CCS) Expansion and Green Manufacturing

The rapid growth of the carbon capture and storage market and green manufacturing technologies provides great opportunities for the air pollution control systems market. Indeed, the global surge in CCS production has created a compelling demand for systems that can replace heavy traditional stacks and integrate seamlessly into carbon management systems (CMS). These applications require high reliability, thermal resistance, and the ability to handle high-vibration environments, all attributes that are met with advanced environmental circuits. The green industrial market is set to expand significantly through 2036, with air pollution control systems poised for an expanding share as manufacturers seek to maximize operational range and minimize environmental weight. Furthermore, the increasing demand for hydrogen-ready sensors and waste-to-energy displays is stimulating demand for modular environmental solutions that provide high-speed data transmission and design flexibility.

Why Do Scrubbers Lead the Market?

The scrubbers segment accounts for a significant portion of the overall air pollution control systems market in 2026. This is mainly attributed to the versatile use of this technology in supporting flue gas desulfurization and complex chemical neutralization within extremely tight spaces, such as in premium power plants and high-performance refining modules. These systems offer the most comprehensive way to ensure chemical integrity across diverse high-frequency applications. The power generation and chemical sectors alone consume a large share of scrubber production, with major projects in Asia Pacific and North America demonstrating the technology’s capability to handle high-density environmental requirements. However, the fabric filters segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust particulate removal in cement plants, medical waste incinerators, and aerospace systems.

How Does the Power Generation Segment Dominate?

Based on application, the power generation segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of coal and gas power production and the rigorous design standards required for modern energy facilities. Current large-scale manufacturing plants are increasingly specifying high-density environmental circuits to ensure compliance with global performance standards and consumer expectations for cleaner, more reliable energy.

The cement manufacturing segment is expected to witness the fastest growth during the forecast period. The shift toward sustainable construction and the complexity of autonomous sensor suites are pushing the requirement for advanced environmental systems that can handle varied temperatures and mechanical stresses while ensuring absolute reliability for safety-critical industrial systems.

Why Does Particulate Matter (PM) Lead the Market?

The particulate matter (PM) segment commands the largest share of the global air pollution control systems market in 2026. This dominance stems from its superior visibility, health impact, and excellent mechanical properties, making it the primary target for high-performance environmental circuits. Large-scale operations in mining, construction, and high-end manufacturing drive demand, with advanced filters from suppliers like Mitsubishi and Babcock & Wilcox enabling reliable performance in extreme environments.

However, the nitrogen oxides (NOx) segment is poised for steady growth through 2036, fueled by expanding applications in low-cost transport goods and simple combustion switches. Manufacturers face mounting pressure to optimize costs for high-volume, less demanding applications, where SCR provides a cost-effective alternative for basic environmental connectivity.

How is Asia Pacific Maintaining Dominance in the Global Air Pollution Control Systems Market?

Asia Pacific holds the largest share of the global air pollution control systems market in 2026. The largest share of this region is primarily attributed to the massive industrialization and the presence of the world’s largest manufacturing hubs, particularly in China, India, and Japan. China alone accounts for a significant portion of global environmental system production, with its position as a leading exporter of high-end industrial equipment driving sustained growth. The presence of leading manufacturers like Fujian Longking and a well-developed industrial supply chain provides a robust market for both standard and high-density environmental solutions.

Which Factors Support North America and Europe Market Growth?

North America and Europe together account for a substantial share of the global air pollution control systems market. The growth of these markets is mainly driven by the need for technological modernization in the aerospace, defense, and medical sectors. The demand for advanced environmental systems in North America is mainly due to its large-scale defense projects and the presence of innovators like Babcock & Wilcox and GE Vernova.

In Europe, the leadership in environmental engineering and the push for green technology innovation are driving the adoption of high-reliability environmental circuits. Countries like Germany, France, and the UK are at the forefront, with significant focus on integrating smart environmental solutions into industrial automation and advanced healthcare devices to ensure the highest levels of performance and reliability.

The companies such as Mitsubishi Heavy Industries, Ltd., Babcock & Wilcox Enterprises, Inc., GE Vernova, and Thermax Limited lead the global air pollution control systems market with a comprehensive range of scrubber and filtration solutions, particularly for large-scale power generation and high-speed applications. Meanwhile, players including Andritz AG, Hamon Group, Ducon Technologies Inc., and FLSmidth & Co. A/S focus on specialized multilayer and high-density circuits targeting the cement, chemical, and metallurgical sectors. Emerging manufacturers and integrated players such as Fujian Longking Co., Ltd., KC Cottrell Co., Ltd., and John Wood Group PLC are strengthening the market through innovations in smart monitoring technology and modular environmental platforms.

The global air pollution control systems market is expected to grow from USD 103.66 billion in 2026 to USD 171.49 billion by 2036.

The global air pollution control systems market is projected to grow at a CAGR of 6.7% from 2026 to 2036.

Scrubbers are expected to dominate the market in 2026 due to their superior ability to support chemical neutralization and high-density gas cleaning. However, Fabric Filters are projected to be the fastest-growing segment owing to their increasing adoption in cement plants, medical waste, and aerospace applications where ultra-fine particulate removal is required

AI and IoT are transforming the air pollution control landscape by demanding higher data integrity, lower latency, and improved thermal management. These technologies drive the adoption of advanced materials like smart sensors and ultra-fine ceramic filters, enabling manufacturers to support the complex routing and high-frequency requirements of next-generation industrial plants and green infrastructure.

Asia Pacific holds the largest share of the global air pollution control systems market in 2026. The largest share of this region is primarily attributed to the massive industrialization and the presence of the world’s largest manufacturing hubs in China, India, and Japan. North America and Europe together account for a substantial share, driven by high-end applications in aerospace, defense, and medical electronics.

The leading companies include Mitsubishi Heavy Industries, Ltd., Babcock & Wilcox Enterprises, Inc., GE Vernova, Thermax Limited, and Andritz AG.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of AI and IoT on the Air Pollution Control Industry

3.4. Regulatory Landscape & Standards (Clean Air Act, IED, China Ultra-Low Emission)

3.5. Porter’s Five Forces Analysis

4. Global Air Pollution Control Systems Market, by Technology

4.1. Introduction

4.2. Scrubbers

4.2.1. Wet Scrubbers

4.2.2. Dry/Semi-dry Scrubbers

4.2.3. Flue Gas Desulfurization (FGD)

4.3. Electrostatic Precipitators (ESP)

4.3.1. Dry ESP

4.3.2. Wet ESP (WESP)

4.4. Fabric Filters

4.4.1. Baghouse Filters

4.4.2. Pulse-Jet Filters

4.5. NOx Control Systems

4.5.1. Selective Catalytic Reduction (SCR)

4.5.2. Selective Non-Catalytic Reduction (SNCR)

4.6. Thermal & Catalytic Oxidizers (VOC Control)

4.7. Others

5. Global Air Pollution Control Systems Market, by Pollutant Type

5.1. Introduction

5.2. Particulate Matter (PM)

5.3. Sulfur Dioxide (SO₂)

5.4. Nitrogen Oxides (NOx)

5.5. Volatile Organic Compounds (VOCs)

5.6. Carbon Monoxide (CO)

5.7. Others (Mercury, Acid Gases)

6. Global Air Pollution Control Systems Market, by Application

6.1. Introduction

6.2. Power Generation

6.2.1. Coal-fired Power Plants

6.2.2. Gas-fired Power Plants

6.3. Cement Manufacturing

6.4. Iron & Steel Industry

6.5. Chemical & Petrochemical

6.6. Mining & Metallurgy

6.7. Waste-to-Energy

6.8. Others

7. Global Air Pollution Control Systems Market, by Region

7.1. Introduction

7.2. North America

7.2.1. U.S.

7.2.2. Canada

7.3. Europe

7.3.1. Germany

7.3.2. France

7.3.3. U.K.

7.3.4. Italy

7.3.5. Spain

7.3.6. Netherlands

7.3.7. Rest of Europe

7.4. Asia-Pacific

7.4.1. China

7.4.2. Japan

7.4.3. South Korea

7.4.4. India

7.4.5. Australia

7.4.6. Rest of Asia-Pacific

7.5. Latin America

7.5.1. Brazil

7.5.2. Mexico

7.5.3. Rest of Latin America

7.6. Middle East & Africa

8. Competitive Landscape

8.1. Overview

8.2. Key Growth Strategies

8.3. Competitive Benchmarking

8.4. Competitive Dashboard

8.4.1. Industry Leaders

8.4.2. Market Differentiators

8.4.3. Vanguards

8.4.4. Emerging Companies

8.5. Market Ranking/Positioning Analysis of Key Players, 2024

9. Company Profiles (Manufacturers & Providers)

9.1. Mitsubishi Heavy Industries, Ltd.

9.2. Babcock & Wilcox Enterprises, Inc.

9.3. GE Vernova

9.4. Thermax Limited

9.5. Andritz AG

9.6. Hamon Group

9.7. Ducon Technologies Inc.

9.8. FLSmidth & Co. A/S

9.9. Fujian Longking Co., Ltd.

9.10. KC Cottrell Co., Ltd.

9.11. John Wood Group PLC

9.12. Siemens Energy AG

10. Appendix

10.1. Questionnaire

10.2. Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Subscribe to get the latest industry updates