Resources

About Us

Advanced Battery Materials Market Size, Share & Trends Analysis by Material Type (Cathode Materials, Anode Materials), Battery Chemistry (Lithium-Ion, Solid-State), Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

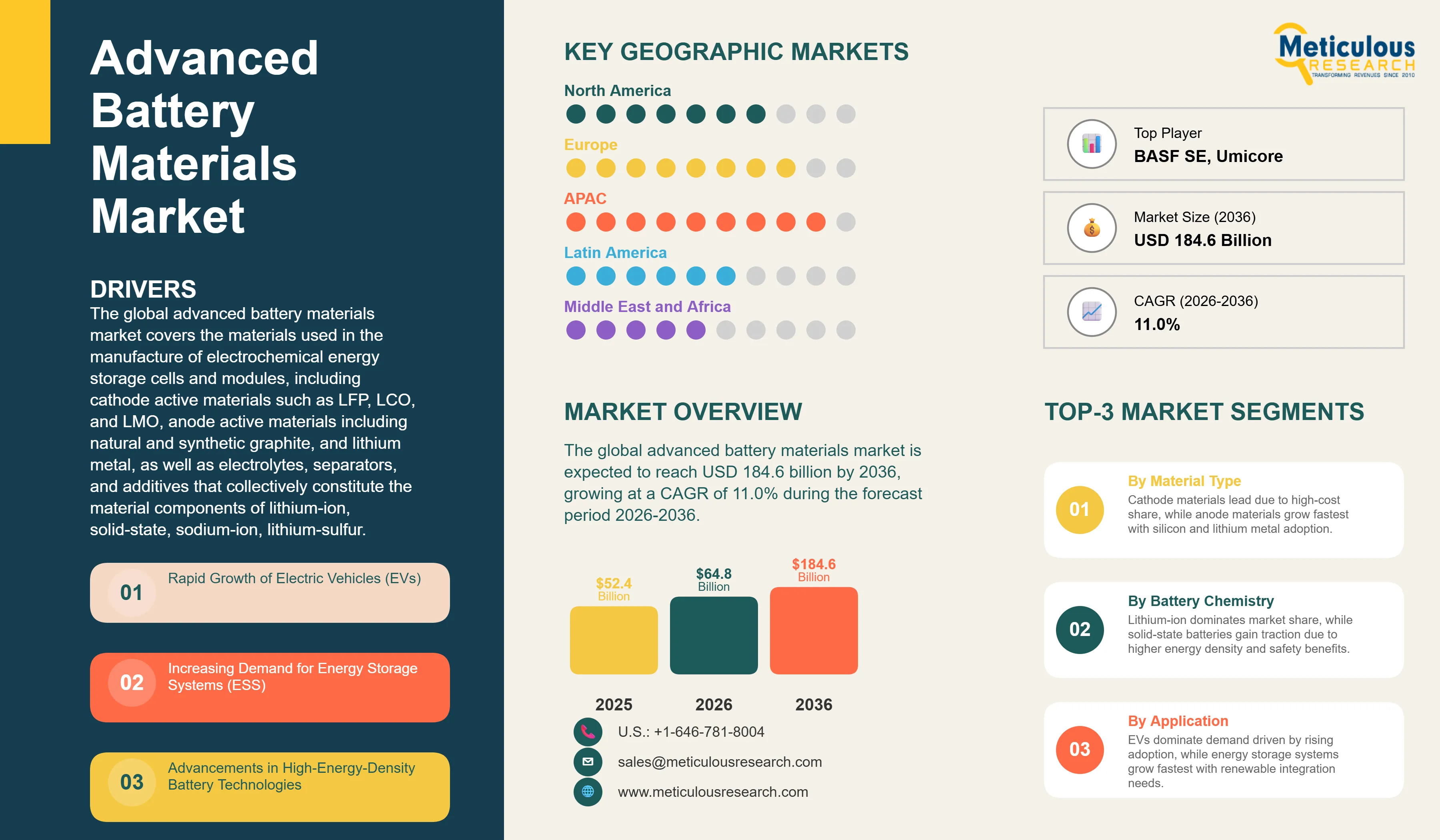

Report ID: MRCHM - 1041886 Pages: 292 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global advanced battery materials market was valued at USD 52.4 billion in 2025. This market is expected to reach USD 184.6 billion by 2036 from an estimated USD 64.8 billion in 2026, growing at a CAGR of 11.0% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global advanced battery materials market covers the materials used in the manufacture of electrochemical energy storage cells and modules, including cathode active materials such as LFP, NMC, NCA, LCO, and LMO, anode active materials including natural and synthetic graphite, silicon-based composites, and lithium metal, as well as electrolytes, separators, current collectors, binders, and additives that collectively constitute the material components of lithium-ion, solid-state, sodium-ion, lithium-sulfur, and other advanced electrochemical cell technologies serving EV, energy storage, consumer electronics, and industrial applications.

The growth of the global advanced battery materials market is primarily driven by the rapid global expansion of electric vehicle adoption, which is generating unprecedented demand for battery cell production and the cathode and anode materials that constitute the majority of cell material cost. Global EV sales exceeded 17 million units in 2024 and are projected to reach 40 to 50 million units annually by the mid-2030s, translating directly into battery material demand growth that is driving gigafactory capacity expansion across Asia, Europe, and North America and sustained investment in battery material supply chain development. In addition, the accelerating deployment of grid-scale and distributed energy storage to support renewable energy integration is creating a second major and rapidly growing demand pillar for advanced battery materials that is progressively diversifying the market beyond its EV application concentration.

Two significant opportunities are shaping the market's long-term trajectory. The commercial development of solid-state battery technology represents the most transformative near-term material opportunity, creating demand for solid-state electrolyte materials including sulfide, oxide, and polymer compositions and advancing the adoption of lithium metal anodes that could not be used safely in liquid electrolyte cell formats. The localization of battery material supply chains in Europe and North America, accelerated by the U.S. Inflation Reduction Act's domestic content requirements and the EU Battery Regulation's sustainability mandates, is creating large greenfield market opportunities for battery material producers establishing production capacity in these regions to serve the expanding local gigafactory base.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 184.6 Billion |

|

Market Size in 2026 |

USD 64.8 Billion |

|

Market Size in 2025 |

USD 52.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 11.0% |

|

Dominating Material Type |

Cathode Materials |

|

Fastest Growing Material Type |

Anode Materials |

|

Dominating Battery Chemistry |

Lithium-Ion Batteries |

|

Fastest Growing Battery Chemistry |

Solid-State Batteries |

|

Dominating Application |

Electric Vehicles (EVs) |

|

Fastest Growing Application |

Energy Storage Systems (ESS) |

|

Dominating End User |

Battery Manufacturers |

|

Fastest Growing End User |

Energy Companies |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Shift Toward LFP and High-Nickel Cathode Materials

The divergence of cathode material chemistry development into two distinct high-growth trajectories, centered on lithium iron phosphate for cost-optimized applications and high-nickel NMC and NCA formulations for energy-density-optimized applications, is the defining structural trend in the global cathode materials market. LFP cathode adoption has expanded well beyond its original Chinese EV market stronghold into global markets, driven by its compelling combination of low cost, excellent cycle life exceeding 3,000 to 4,000 full cycles, inherent thermal stability eliminating the thermal runaway risk of cobalt-containing cathodes, and the elimination of cobalt and nickel from the formulation that removes the supply chain and sustainability risks associated with these critical minerals.

Tesla's adoption of LFP for its standard-range global vehicle lineup, Ford's LFP adoption for its F-150 Lightning, and the broad deployment of LFP in energy storage systems globally have established the chemistry as a mainstream cathode platform beyond China. Simultaneously, high-nickel cathode formulations with nickel content of 80% or above, including NMC 811, NMC 9 series, and NCA variants, are advancing in premium EV applications where energy density, driving range, and vehicle weight considerations justify the premium over LFP. The progressive reduction of cobalt content toward zero in next-generation high-nickel cathode formulations is a primary R&D focus for cathode material developers including BASF, Umicore, and POSCO Future M.

Rise of Solid-State Battery Materials

The accelerating commercial development of solid-state battery technology is creating a new and rapidly growing material demand category for solid electrolyte materials, lithium metal anode preparations, and the specialized cathode and cell engineering materials required for solid-state cell architectures. Solid-state batteries replace the liquid electrolyte of conventional lithium-ion cells with a solid ionic conductor, eliminating the flammability and leakage risks associated with organic liquid electrolytes, enabling the use of lithium metal anodes with energy densities approximately ten times higher than graphite, and facilitating cell designs with higher operating voltage windows that further increase energy density. The combined energy density advantage of solid electrolytes plus lithium metal anodes could deliver battery cells with gravimetric energy densities of 400 to 500 Wh/kg, compared with 250 to 300 Wh/kg for current best lithium-ion cells.

Toyota has committed to solid-state battery vehicle production launch in the late 2020s and is the single largest patent holder in solid-state battery technology globally. Samsung SDI's solid-state battery development program targets automotive-grade cell production from 2027. QuantumScape, backed by Volkswagen Group, and Solid Power, in partnership with BMW and Ford, represent the leading U.S.-based solid-state battery commercial development programs. The solid-state electrolyte material market is projected to grow at a very high CAGR through the forecast period as these programs transition from pilot production to commercial volume, creating new demand for sulfide, oxide, and polymer solid electrolyte materials from specialty chemical suppliers including BASF, Mitsubishi Chemical Group, and a growing ecosystem of dedicated solid electrolyte manufacturers.

Growth in Battery Recycling and Secondary Raw Materials

The rapid growth of battery recycling capacity and the integration of secondary recovered materials into battery material supply chains is an increasingly important structural trend driven by both regulatory mandates and the economic imperative to reduce battery material cost and supply chain vulnerability. The EU Battery Regulation establishes binding minimum recycled content requirements for lithium (6% from 2031, rising to 12% from 2036), cobalt (16% from 2031, rising to 26% from 2036), and nickel (6% from 2031, rising to 15% from 2036) in new batteries placed on the European market, creating an obligatory demand for recovered battery materials that is driving investment in hydrometallurgical black mass processing capacity across Europe. The IRA's clean vehicle critical mineral requirements create equivalent incentives for domestic battery material recycling in the United States.

Battery recycling companies including Umicore, Li-Cycle, Redwood Materials, and Accurec are scaling commercial hydrometallurgical recovery processes that can recover 95% or more of lithium, cobalt, nickel, and manganese from spent battery black mass with materials quality suitable for re-entry into cathode active material production. The growing installed base of EV batteries approaching end of first life is beginning to generate commercially significant volumes of black mass feedstock, and by the early 2030s the recycled material streams from the current wave of EV battery retirements are projected to supply a meaningful fraction of battery material demand, reducing primary mining requirements and battery material cost.

Rapid Growth of Electric Vehicles (EVs)

The rapid global expansion of electric vehicle adoption is the primary structural demand driver of the advanced battery materials market, as EV battery packs require between 50 and 100 kilograms of battery materials per vehicle depending on battery capacity, directly translating EV sales growth into battery material volume demand at extraordinary scale. Global EV sales have grown from under 1 million units in 2017 to over 17 million units in 2024, and industry forecasts project continued strong growth toward 40 to 50 million annual EV sales by 2030 to 2035, driven by government combustion engine phase-out mandates in the EU and U.K., the Inflation Reduction Act EV tax credit structure in the United States, and the rapid improvement in EV price competitiveness relative to combustion vehicle equivalents driven by battery cost reduction. This EV demand trajectory directly translates into the multi-hundred-billion-dollar advanced battery material procurement programs that battery manufacturers and automotive OEMs are executing through gigafactory supply agreements spanning cathode active materials, anode materials, electrolytes, and separators.

Increasing Demand for Energy Storage Systems (ESS)

The accelerating global deployment of grid-scale and distributed battery energy storage to support renewable energy integration represents the second major and rapidly growing demand pillar for advanced battery materials. The International Energy Agency projects that installed global battery storage capacity needs to grow from approximately 85 GWh in 2024 to over 1,500 GWh by 2030 to support the renewable energy transition under a net-zero pathway, implying an extraordinary expansion of battery material demand from the energy storage sector over the forecast period. Grid-scale lithium-ion battery storage is being deployed at gigawatt-hour scale in the United States, China, Australia, and Europe as utilities, grid operators, and independent power producers invest in battery storage to provide grid frequency regulation, peak capacity, and renewable firming services. The residential storage market is growing rapidly in tandem with solar panel installation, with home battery systems from Tesla, Sonnen, BYD, and others creating an additional and broadly distributed demand channel for LFP and NMC battery materials.

Development of Solid-State Battery Materials

The commercial development of solid-state battery technology represents the highest-value material opportunity in the advanced battery materials market over the forecast period, creating entirely new material demand categories for solid electrolyte compositions and advancing the commercial viability of lithium metal anodes that would fundamentally transform the energy density frontier of battery technology. The solid electrolyte material market encompasses sulfide-based compositions including lithium argyrodite and LGPS that offer the highest ionic conductivity among solid electrolytes, oxide-based materials including garnet LLZO and NASICON-structured compositions that offer superior electrochemical stability, and polymer-based systems including PEO composites that offer processing flexibility for large-format cell manufacturing. Each of these material categories requires specialized synthesis and processing capabilities that are creating new business development opportunities for both established battery material suppliers including BASF and Mitsubishi Chemical and dedicated solid electrolyte developers.

Expansion of Battery Recycling and Circular Economy

The expansion of battery recycling into a commercially scaled secondary raw material supply channel represents a significant long-term opportunity for companies that establish strong positions in black mass processing and recovered material refining before the growing volume of spent EV batteries creates intense competition for this feedstock. The economics of battery recycling are improving as the lithium price recovery from the 2023 to 2024 downturn, the regulatory value created by EU recycled content mandates, and the improving recovery efficiency of hydrometallurgical processes collectively strengthen the business case for investment in recycling capacity. Companies including Redwood Materials, Li-Cycle, and Umicore's battery recycling division are positioning themselves as integrated recycled material suppliers that can provide cathode precursor materials meeting automotive-grade quality specifications from recovered battery feedstock, addressing a supply chain resilience priority that battery manufacturers and automotive OEMs are willing to pay a premium to secure.

By Material Type: In 2026, Cathode Materials to Dominate

Based on material type, the global advanced battery materials market is segmented into cathode materials, anode materials, electrolytes, separators, and binders and additives. In 2026, the cathode materials segment is expected to account for the largest share of the global advanced battery materials market. The large share of this segment is attributed to cathode active materials representing 30 to 40% of total lithium-ion cell material cost, the broadest commercial product development activity across LFP, NMC 811, NMC 9-series, NCA, and next-generation cobalt-free cathode formulations, and the very high dollar-per-kilogram value of advanced cathode materials including high-nickel NMC and NCA that generates substantial market value relative to other battery material categories. POSCO Future M, Umicore, BASF, and Sumitomo Metal Mining are among the leading commercial cathode active material suppliers serving global battery manufacturers.

However, the anode materials segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the accelerating commercial transition from pure graphite anodes toward silicon-blended graphite anodes that deliver higher energy density, the advancing development of high-silicon-content anodes targeting solid-state battery applications, and the long-term commercialization trajectory of lithium metal anodes that represent the anode material of choice for next-generation solid-state cells.

By Battery Chemistry: In 2026, Lithium-Ion Batteries to Hold the Largest Share

Based on battery chemistry, the global advanced battery materials market is segmented into lithium-ion batteries (LFP, NMC, NCA), solid-state batteries, sodium-ion batteries, lithium-sulfur batteries, and other emerging chemistries. In 2026, the lithium-ion batteries segment is expected to account for the largest share of the global advanced battery materials market. This dominance reflects lithium-ion technology's established position as the commercial standard across EV, energy storage, and consumer electronics applications, with the global installed base of lithium-ion manufacturing capacity representing several hundred GWh annually and providing a large and growing material demand base for cathode, anode, electrolyte, and separator material suppliers serving established cell production programs.

However, the solid-state batteries segment is projected to register the highest CAGR during the forecast period. This growth is driven by the advancing commercial development timelines of Toyota, Samsung SDI, QuantumScape, and Solid Power targeting automotive solid-state battery production launch in the late 2020s, the transformative energy density and safety advantages that solid-state electrolytes enable over liquid electrolyte lithium-ion cells, and the new and high-value material demand categories that solid-state cell architectures create for solid electrolyte, lithium metal anode, and advanced cathode material suppliers.

By Application: In 2026, Electric Vehicles to Hold the Largest Share

Based on application, the global advanced battery materials market is segmented into electric vehicles (passenger EVs, commercial EVs, two- and three-wheelers), energy storage systems (grid-scale and residential), consumer electronics, industrial applications, and aerospace and defense. In 2026, the electric vehicles segment is expected to account for the largest share of the global advanced battery materials market. This dominance reflects EV battery packs' position as the single largest and fastest-growing consumer of lithium-ion battery materials globally, with passenger EV and commercial EV battery procurement constituting the primary revenue driver for cathode active material, anode material, separator, and electrolyte producers. The global EV battery material demand is projected to grow from approximately 2 million metric tons of lithium carbonate equivalent in 2025 to over 8 million metric tons by 2035, establishing EV as the structurally dominant application category through the forecast period.

However, the energy storage systems segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating global deployment of grid-scale lithium-ion battery storage required to integrate growing renewable energy capacity, the IEA's projection of over 1,500 GWh of installed battery storage capacity required by 2030 under net-zero pathways, and the rapidly growing residential storage market that is expanding the ESS battery material demand base across a broad geographic and customer footprint well beyond the utility-scale project pipeline.

By End User: In 2026, Battery Manufacturers to Hold the Largest Share

Based on end user, the global advanced battery materials market is segmented into automotive OEMs, battery manufacturers, energy companies, electronics manufacturers, and others. In 2026, the battery manufacturers segment is expected to account for the largest share of the global advanced battery materials market. Battery cell and module manufacturers including CATL, BYD, Panasonic, LG Energy Solution, Samsung SDI, SK On, and Envision AESC represent the primary direct procurement channel for advanced battery materials, as they aggregate the material purchasing from individual cell chemistries and production programs into large-volume supply agreements that constitute the bulk of global battery material market revenue. CATL alone, as the world's largest battery manufacturer, accounts for a significant proportion of global cathode and anode material procurement, with annual material purchases representing tens of billions of dollars in market value.

However, the energy companies segment is projected to register the highest CAGR during the forecast period. This growth is driven by energy utilities, grid operators, and independent power producers directly procuring grid-scale battery storage systems in a procurement model that is increasingly bypassing battery manufacturer intermediaries for large project orders, creating direct battery material demand relationships with energy sector customers at rapidly growing scale. The expansion of vertically integrated energy storage procurement by companies including NextEra Energy, AES, Fluence, and national grid operators is establishing energy companies as a fast-growing direct end-user category in the advanced battery materials market.

Advanced Battery Materials Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global advanced battery materials market is segmented into Asia-Pacific, Europe, North America, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global advanced battery materials market. The largest share of this region is mainly due to China's dominant position across the full battery material supply chain, encompassing the processing of over 60% of global lithium, cobalt, and nickel into battery-grade materials, the manufacturing of approximately 70 to 75% of global cathode active materials and over 80% of synthetic graphite anode materials, and the production of the majority of global battery separator and electrolyte output. China's integrated battery material ecosystem, anchored by companies including Ganfeng Lithium, Tianqi Lithium, CATL's material subsidiaries, and BYD's upstream material operations, provides cost and scale advantages that are difficult to replicate in other geographies in the near term. South Korea's advanced battery material sector, anchored by LG Chem's advanced cathode material division, POSCO Future M's cathode and anode production, and Samsung SDI's material development programs, contributes significant high-performance material innovation and production capacity to the regional market. Japan's Sumitomo Metal Mining, Panasonic's material operations, and Mitsubishi Chemical's electrolyte and separator businesses add further depth to Asia-Pacific's battery material leadership.

However, the European advanced battery materials market is expected to grow at the fastest CAGR during the forecast period. Europe's rapid growth is driven by the EU Battery Regulation's establishment of binding requirements for recycled content, carbon footprint reporting, and battery passports that are creating a compliance-driven investment wave in European battery material production and recycling capacity. The large pipeline of gigafactory investments within the EU, including Northvolt in Sweden, ACC in France and Germany, AESC's Sunderland expansion, and the European manufacturing programs of CATL, Samsung SDI, and SK On, is creating substantial local battery material demand that European and global battery material producers are investing to serve. Umicore's cathode material expansion in Europe, BASF's European battery material production investments, and the growing ecosystem of European battery recycling companies including Li-Cycle's Rochester hub and Veolia's black mass processing operations collectively represent the supply-side investment that is positioning Europe as a growing battery material production region alongside its established role as a consumption market.

North America is establishing a rapidly developing advanced battery materials sector, accelerated by the IRA's stringent domestic content and foreign entity of concern restrictions that are driving significant greenfield investment in North American battery material production. The U.S. battery material investment pipeline includes Albemarle's lithium hydroxide processing expansions, Livent and Standard Lithium's domestic lithium production projects, and the cathode material investments of several Korean and Japanese battery material companies establishing U.S. production to serve the growing North American gigafactory base. Canada's position as a major holder of lithium, cobalt, and nickel mineral resources is attracting battery material processing investments that leverage domestic critical mineral supply into vertically integrated battery material production.

The global advanced battery materials market is moderately consolidated at the cathode material tier and more fragmented across anode, electrolyte, and separator material categories. Competition is focused on material performance differentiation, chemistry innovation, supply chain security, production scale, and the ability to develop and qualify materials meeting the increasingly stringent specifications of automotive-grade battery manufacturers and integrated EV platforms.

BASF leads in cathode material innovation for European and global battery manufacturers through its HiNa and Hedgehog cathode active material platforms targeting high-nickel and cobalt-free formulations. Umicore is a leading cathode material supplier and the most commercially advanced large-scale battery recycling operator. POSCO Future M and Sumitomo Metal Mining compete as major cathode and anode material suppliers to Asian and global battery cell manufacturers. Albemarle and Ganfeng Lithium are the leading lithium compound producers supplying battery-grade lithium hydroxide and lithium carbonate to cathode material manufacturers globally. CATL and BYD have established increasing vertical integration into cathode and anode material production in support of their cell manufacturing operations.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, production capacity, geographic presence, and key strategic developments. Some of the key players operating in the global advanced battery materials market include BASF SE (Germany), Umicore (Belgium), LG Chem Ltd. (South Korea), POSCO Future M (South Korea), Sumitomo Metal Mining Co. Ltd. (Japan), Mitsubishi Chemical Group (Japan), Albemarle Corporation (U.S.), Ganfeng Lithium (China), Tianqi Lithium (China), CATL (China), BYD Company Ltd. (China), Panasonic Holdings Corporation (Japan), SK On Co. Ltd. (South Korea), Samsung SDI Co. Ltd. (South Korea), and Envision AESC (Japan/U.K.), among others.

The global advanced battery materials market is expected to reach USD 184.6 billion by 2036 from an estimated USD 64.8 billion in 2026, at a CAGR of 11.0% during the forecast period 2026-2036.

In 2026, the cathode materials segment is expected to hold the largest share of the global advanced battery materials market, driven by cathode active materials representing the highest-cost and highest-revenue battery material category across both LFP and high-nickel chemistry platforms.

The anode materials segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the accelerating commercial transition toward silicon-blended and high-silicon anode formulations and the long-term commercialization of lithium metal anodes for solid-state battery applications.

In 2026, the lithium-ion batteries segment is expected to hold the largest share of the global advanced battery materials market, reflecting lithium-ion technology's established commercial dominance across EV, energy storage, and consumer electronics applications.

In 2026, the electric vehicles segment is expected to hold the largest share of the global advanced battery materials market, as EV battery packs represent the single largest and fastest-growing consumer of lithium-ion battery materials globally.

The growth of this market is primarily driven by the rapid global expansion of electric vehicle adoption generating unprecedented battery material demand at automotive scale, the accelerating deployment of grid-scale and distributed energy storage creating a second major battery material demand pillar, and government policies including the U.S. IRA and EU Battery Regulation that are mandating battery supply chain localization and recycled content requirements driving new investment in battery material production capacity.

Key players are BASF SE (Germany), Umicore (Belgium), LG Chem Ltd. (South Korea), POSCO Future M (South Korea), Sumitomo Metal Mining Co. Ltd. (Japan), Mitsubishi Chemical Group (Japan), Albemarle Corporation (U.S.), Ganfeng Lithium (China), Tianqi Lithium (China), CATL (China), BYD Company Ltd. (China), Panasonic Holdings Corporation (Japan), SK On Co. Ltd. (South Korea), Samsung SDI Co. Ltd. (South Korea), and Envision AESC (Japan/U.K.), among others.

Europe is expected to register the highest growth rate in the global advanced battery materials market during the forecast period 2026-2036, driven by the EU Battery Regulation's compliance-driven investment wave in European battery material production and recycling capacity and the large pipeline of gigafactory investments within the EU creating substantial local battery material demand.

Published Date: May-2026

Published Date: Feb-2025

Published Date: May-2024

Published Date: Apr-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates