Resources

About Us

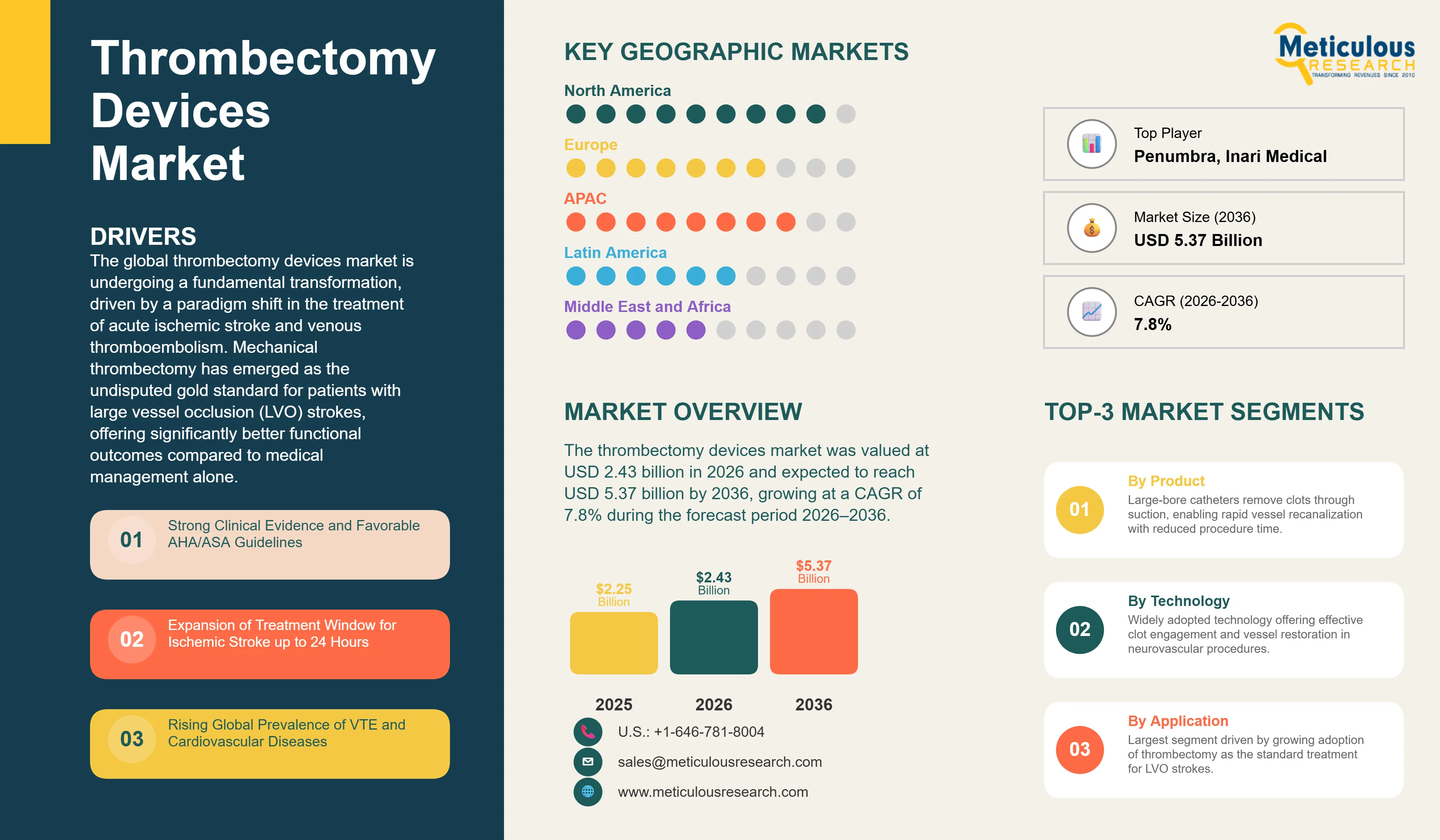

The global thrombectomy devices market was valued at USD 2.43 billion in 2026. This market is expected to reach USD 5.37 billion by 2036, growing at a CAGR of 7.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global thrombectomy devices market is undergoing a fundamental transformation, driven by a paradigm shift in the treatment of acute ischemic stroke and venous thromboembolism. Mechanical thrombectomy has emerged as the undisputed gold standard for patients with large vessel occlusion (LVO) strokes, offering significantly better functional outcomes compared to medical management alone. The market's expansion is fueled by landmark clinical trials such as DAWN and DEFUSE 3, which have extended the treatment window for mechanical thrombectomy from 6 hours to 24 hours in selected patients. This extension has dramatically increased the eligible patient population, catalyzing a surge in procedure volumes and the establishment of thrombectomy-capable stroke centers worldwide.

The clinical efficacy of thrombectomy is backed by robust data, with modern stent retrievers and aspiration catheters achieving successful revascularization in approximately 82% of cases (meta-analysis of 31 studies). Approximately 15 million people worldwide suffer a stroke each year, with ischemic strokes accounting for ~85–87% of all cases. In the U.S., the lifetime cost of a stroke is estimated at $103,576 per patient (1990 data, adjusted to ~$250,000 today), making the $15,000–$25,000 cost of a thrombectomy procedure highly cost-effective (worth $14,137 per QALY gained) by reducing long-term disability and institutional care requirements. This economic value proposition is a major driver for healthcare systems and payers to expand reimbursement and infrastructure for thrombectomy services.

The market is also witnessing significant expansion in the peripheral vascular segment, particularly for the treatment of deep vein thrombosis (DVT) and pulmonary embolism (PE). New device approvals and favorable clinical data are driving the adoption of mechanical thrombectomy as a first-line therapy for venous thromboembolism, reducing the reliance on thrombolytic drugs and their associated bleeding risks. The competitive landscape is characterized by intense innovation, with leading players like Medtronic, Stryker, and Penumbra constantly refining their portfolios to improve procedural speed, safety, and technical success rates. Strategic consolidation and the development of hybrid technologies that combine aspiration and mechanical retrieval are key trends shaping the future of the market.

Geographically, North America leads the global market, accounting for approximately 40% of total revenue in 2026. This dominance is supported by a mature network of comprehensive stroke centers and favorable reimbursement policies. However, the Asia-Pacific region is projected to witness the fastest growth, driven by a high stroke burden in countries like China and India, increasing healthcare investments, and the expansion of domestic manufacturing capabilities. As global stroke systems of care continue to evolve, the thrombectomy devices market is poised for sustained growth over the next decade, with China at 10.3% CAGR and India at 9.5% CAGR, though the overall market grows at approximately 7% CAGR.

The primary driver for the thrombectomy devices market is the strong clinical evidence and favorable guidelines from organizations like the AHA/ASA. Mechanical thrombectomy is now the standard of care for large vessel strokes, leading to its rapid adoption worldwide. The expansion of the treatment window based on advanced imaging has also significantly increased the pool of eligible patients. Furthermore, the rising global prevalence of atrial fibrillation, obesity, and hypertension all major risk factors for stroke and thrombosis is providing a continuous stream of patients requiring these life-saving procedures.

A significant restraint is the shortage of trained neurointerventionalists and specialized stroke teams, particularly in rural and underserved areas. These procedures require high levels of technical expertise and 24/7 availability of advanced cath labs. The high cost of the devices and the associated hospital stay also pose challenges in emerging markets with limited healthcare budgets. Additionally, the logistical hurdles in transporting stroke patients to specialized centers within the critical time window remain a major barrier to wider market adoption.

There are massive opportunities in the development of robotic-assisted thrombectomy systems, which could improve precision and eventually allow for remote procedures in areas lacking local specialists. The expansion of mechanical thrombectomy into distal vessel occlusions (M2/M3 branches) also offers a significant new growth path. Furthermore, the increasing adoption of mechanical thrombectomy for venous thromboembolism (PE and DVT) is a major opportunity, as clinicians move away from systemic thrombolytics. The development of 'smart' thrombectomy devices with integrated sensors for real-time feedback also holds high potential.

A key challenge is the continuous optimization of stroke systems of care to minimize 'door-to-puncture' times. Reducing procedural delays is critical for improving patient outcomes. Vendors also face the challenge of minimizing procedure-related complications, such as vessel perforation or embolization of clot fragments to previously unaffected territories. As the market becomes more crowded, manufacturers must also navigate complex regulatory pathways and demonstrate clear clinical superiority to maintain market share and justify premium pricing.

A major trend in the thrombectomy devices market is the increasing adoption of aspiration thrombectomy as either a first-line approach or in combination with stent retrievers. Clinical evidence from the COMPASS trial demonstrated that aspiration thrombectomy is non-inferior to stent retrievers in selected large-vessel occlusion cases, supporting the growing use of the "Save a Bullet" strategy. In addition, guidelines from the Society of NeuroInterventional Surgery (SNIS) recognize both aspiration and stent retriever approaches for mechanical thrombectomy, driving wider adoption of large-bore aspiration catheters due to their potential to reduce procedure time, vessel trauma, and overall treatment costs.

A growing trend in the thrombectomy devices market is the expansion of thrombectomy-capable stroke centers worldwide. According to the American Heart Association/American Stroke Association (AHA/ASA), timely access to endovascular therapy significantly improves outcomes in patients with large-vessel occlusion stroke, prompting healthcare systems to invest in specialized infrastructure and 24/7 neurointerventional capabilities. In the U.S., The Joint Commission has certified more than 350 Thrombectomy-Capable Stroke Centers and Comprehensive Stroke Centers, while the World Stroke Organization continues to promote the development of organized stroke systems globally. These initiatives are expanding patient access to mechanical thrombectomy and supporting sustained demand for thrombectomy devices.

Based on application, the market is segmented into Neurovascular, Peripheral Vascular, and Cardiovascular. In 2026, the Neurovascular segment is expected to hold the largest share of the market. This dominance is driven by the clear clinical superiority of mechanical thrombectomy for ischemic stroke and its inclusion in international treatment guidelines. This segment is also projected to grow at the fastest CAGR as more stroke centers become operational globally.

The Peripheral Vascular segment is also witnessing significant growth, driven by the increasing use of mechanical thrombectomy for pulmonary embolism and deep vein thrombosis, where it offers a safer alternative to thrombolytic therapy.

Based on technology, the market is segmented into Stent Retriever, Aspiration, and Hybrid. In 2026, the Stent Retriever segment is expected to hold the largest share of the market. Stent retrievers were the first devices to demonstrate clear clinical benefit in randomized trials and remain the primary tool for most neurointerventionalists.

The Aspiration Technology segment is projected to witness the fastest growth during the forecast period. The speed of the procedure and the effectiveness of new, highly flexible, large-bore catheters are driving its rapid adoption across both neuro and peripheral applications.

North America is expected to hold the largest share of the global thrombectomy devices market in 2026, accounting for approximately 40% of the total revenue. This is due to a highly developed network of Comprehensive Stroke Centers, favorable reimbursement for thrombectomy procedures, and a high awareness of stroke symptoms among the general public. Key companies operating in the North American market include Medtronic, Stryker, and Penumbra.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region faces a massive stroke burden, particularly in China, where stroke is the leading cause of death. Increasing healthcare infrastructure investment, the expansion of stroke centers in Tier 2 and Tier 3 cities, and the rising adoption of advanced medical technologies are the primary growth drivers. Key companies operating in the Asia-Pacific market include Terumo, MicroPort, and major global vendors.

The global thrombectomy devices market is highly competitive and is dominated by a few major medical technology companies. Medtronic, Stryker, and Penumbra collectively hold a significant portion of the market share, supported by their extensive R&D capabilities and global distribution networks. However, the market is seeing increased competition from specialized neurovascular players and emerging companies in the peripheral space, such as Inari Medical.

Innovation in device design—focusing on trackability, clot integration, and revascularization speed—is the primary competitive strategy. Companies are also investing in large-scale clinical trials to expand the indications for their devices. Strategic acquisitions are common, as larger players look to strengthen their portfolios with novel technologies. Key players in the global thrombectomy devices market include Medtronic, Stryker, Penumbra, Terumo (MicroVention), Boston Scientific, Johnson & Johnson (Cerenovus), Abbott, Inari Medical, MicroPort, and Rapid Medical.

The market is projected to reach USD 5.37 billion by 2036, growing at a CAGR of 7.8% from 2026 to 2036.

Stent Retriever technology is currently considered the gold standard for neurovascular LVO strokes.

The primary driver is the expansion of the treatment window up to 24 hours post-stroke based on clinical evidence.

The Asia-Pacific region is projected to witness the fastest growth due to high stroke burden and healthcare investment.

Modern devices achieve successful revascularization (TICI 2b/3) in over 85% of cases.

The market is expected to grow at a CAGR of 7.8% during the forecast period 2026–2036.

The Mechanical Thrombectomy Devices segment (including stent retrievers) holds the largest share in 2026.

The shortage of trained neurointerventionalists and the high cost of procedures are the main restraints.

Mechanical thrombectomy improves functional outcomes in up to 60% of patients with LVO stroke, compared with approximately 20–30% receiving medical management alone.

The Leading manufacturers in the thrombectomy devices market include Medtronic plc, Stryker Corporation, Penumbra, Inc., and Terumo Corporation (MicroVention), along with Boston Scientific Corporation, Johnson & Johnson (Cerenovus), Inari Medical, and Becton, Dickinson and Company.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product

3.2.2. Market Analysis, by Technology

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Strong Clinical Evidence and Favorable AHA/ASA Guidelines

4.2.1.2. Expansion of Treatment Window for Ischemic Stroke up to 24 Hours

4.2.1.3. Rising Global Prevalence of VTE and Cardiovascular Diseases

4.2.2. Restraints

4.2.2.1. Shortage of Trained Neurointerventionalists and Specialized Teams

4.2.2.2. High Cost of Devices and Specialized Hospital Infrastructure

4.2.3. Opportunities

4.2.3.1. Development of Robotic-Assisted and Remote Thrombectomy Systems

4.2.3.2. Expansion into Distal Vessel Occlusions and Smaller Branch Strokes

4.2.4. Challenges

4.2.4.1. Logistical Delays in Transporting Patients to Specialized Stroke Centers

4.2.4.2. Risk of Procedure-Related Complications and Vessel Trauma

4.2.5. Trends

4.2.5.1. Rapid Adoption of Aspiration and Hybrid Retrieval Techniques

4.2.5.2. Establishment and Certification of Thrombectomy-Capable Stroke Centers

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Thrombectomy Devices Market, by Product

5.1. Overview

5.2. Aspiration Thrombectomy Devices

5.3. Mechanical Thrombectomy Devices (Stent Retrievers)

5.4. Ultrasound-Assisted Thrombectomy Devices

5.5. Hydrodynamic Thrombectomy Devices

6. Global Thrombectomy Devices Market, by Technology

6.1. Overview

6.2. Stent Retriever Technology

6.3. Aspiration Technology

6.4. Hybrid Technology

7. Global Thrombectomy Devices Market, by Application

7.1. Overview

7.2. Neurovascular (Ischemic Stroke)

7.3. Peripheral Vascular (DVT, PE)

7.4. Cardiovascular (Coronary Thrombectomy)

8. Global Thrombectomy Devices Market, by End User

8.1. Overview

8.2. Hospitals & Specialty Centers (Stroke Centers)

8.3. Ambulatory Surgical Centers (ASCs)

8.4. Academic & Research Institutes

9. Global Thrombectomy Devices Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Medtronic plc

11.2. Stryker Corporation

11.3. Penumbra, Inc.

11.4. Terumo Corporation (MicroVention, Inc.)

11.5. Boston Scientific Corporation

11.6. Johnson & Johnson (Cerenovus)

11.7. Becton, Dickinson and Company

11.8. Abbott Laboratories

11.9. Inari Medical, Inc.

11.10. Teleflex Incorporated

11.11. AngioDynamics, Inc.

11.12. MicroPort Scientific Corporation

11.13. Merit Medical Systems, Inc.

11.14. phenox GmbH (Wallaby Medical)

11.15. Acandis GmbH

11.16. Rapid Medical Ltd.

12. Appendix

Published Date: Aug-2026

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Dec-2017

Subscribe to get the latest industry updates