Resources

About Us

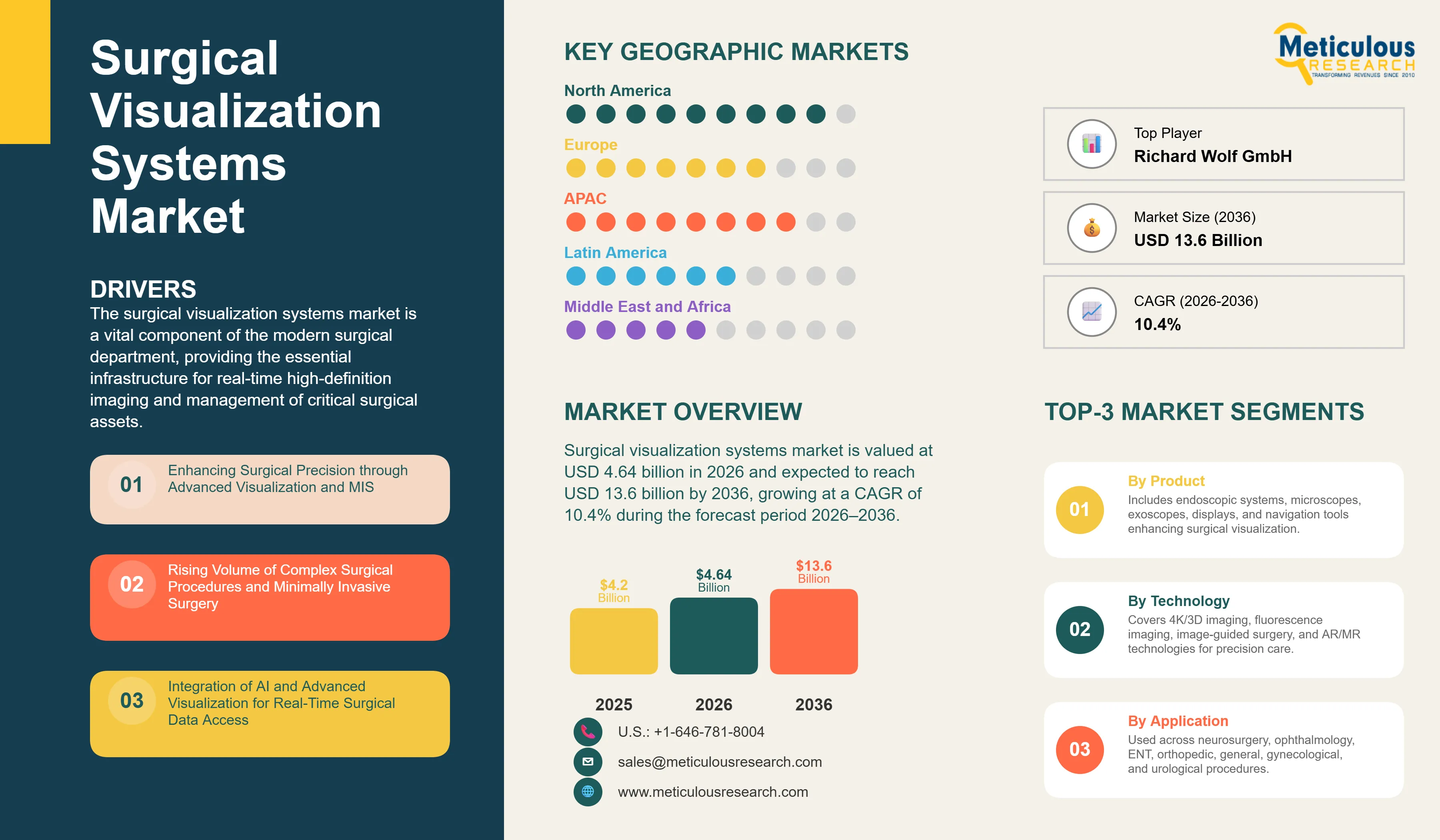

Surgical Visualization Systems Market Size, Share & Trends Analysis by Product, Technology, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

Report ID: MRHC - 1042034 Pages: 284 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global surgical visualization systems market is valued at USD 4.64 billion in 2026. This market is expected to reach USD 13.6 billion by 2036, growing at a CAGR of 10.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Market Overview: Enhancing Surgical Precision through Advanced Visualization and Minimally Invasive Interventions

The global surgical visualization systems market is a vital component of the modern surgical department, providing the essential infrastructure for real-time high-definition imaging and management of critical surgical assets. Surgical visualization solutions, including endoscopic systems, surgical microscopes, and exoscopes, enable surgical teams to maintain institutional integrity and clinical productivity. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to address the rising complexity of surgical procedures and the increasing demand for minimally invasive interventions. According to industry reports, advanced visualization is essential for reducing surgical errors and improving patient outcomes.

The transition toward integrated and AI-powered surgical imaging platforms is essential for improving clinical efficiency and surgical throughput in the healthcare industry. Modern surgical visualization solutions leverage advanced sensors and AI-driven analytics to provide a unified view of the surgical environment, ensuring that stakeholders have immediate access to actionable insights. As healthcare systems transition toward value-based care models, the demand for visualization solutions that can demonstrably reduce procedure times and improve resource utilization is expected to surge.

Drivers: Enhancing Surgical Precision through Advanced Visualization and Minimally Invasive Interventions

The primary driver for the surgical visualization systems market is the escalating global cost of healthcare and the increasing volume of complex surgical procedures, which necessitates a more efficient and data-driven approach to surgical management. According to the AHA, surgical throughput and resource underutilization account for significant annual losses in hospital capital budgets. This massive financial burden is driving the adoption of advanced visualization suites to manage the high volume of procedures and clinical documentation. Furthermore, the shift toward minimally invasive surgery (MIS) and the increasing demand for real-time surgical data access are significant drivers. Government initiatives promoting the adoption of connected health solutions and the exchange of health information are compelling healthcare organizations to invest in visualization solutions that can seamlessly integrate with broader healthcare IT ecosystems.

Restraints: High Implementation Costs and Technical Integration Challenges

Market growth is restrained by the high cost of implementing comprehensive surgical visualization solutions and the technical challenges of achieving seamless data interoperability across disparate surgical imaging platforms and legacy IT systems. For many mid-sized hospitals, the initial capital investment and ongoing maintenance costs of a facility-wide integrated visualization suite can be a significant barrier. Additionally, the lack of standardized data protocols between different surgical device providers often leads to data silos, making it difficult to achieve a truly unified surgical record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful implementation can lead to slower adoption rates.

Opportunities: Advancing AI-Driven Surgical Analytics and Augmented Reality

The integration of artificial intelligence (AI) and augmented reality (AR) into surgical visualization platforms offers substantial growth opportunities. AI-powered tools can analyze complex surgical data and clinical evidence to identify potential workflow bottlenecks, facilitating more precise surgical intervention. By 2026, AI-driven predictive analytics are being used to forecast surgical demand and optimize procedure scheduling, enabling proactive resource distribution and improving patient safety. Furthermore, the shift toward mixed reality (MR) provides healthcare organizations with superior surgical capabilities, combining advanced imaging with traditional surgical environments. This integration facilitates real-time data sharing among diverse surgical specialists, supporting multi-disciplinary collaboration, which is particularly beneficial for complex interventions.

Evolution toward Holistic and AI-Powered Surgical Care Orchestration

A key trend in 2026 is the transformation of surgical visualization platforms into integrated surgical intelligence hubs that connect imaging systems, navigation platforms, robotic technologies, and electronic health records. The growing focus on data-driven surgery is supported by initiatives such as the American College of Surgeons' (ACS) clinical data modernization strategy, which aims to automate surgical data capture and enable AI-driven decision support across healthcare systems. AI-enabled visualization platforms are increasingly being used to improve workflow efficiency, reduce documentation burden, and support intraoperative decision-making, reflecting the industry's shift toward enterprise-wide surgical care orchestration and quality improvement.

Integration of 4K/3D Visualization and Fluorescence Imaging Systems

The adoption of 4K/3D visualization and fluorescence-guided imaging continues to accelerate as healthcare providers seek greater surgical precision and improved patient outcomes. Fluorescence imaging using indocyanine green (ICG) has gained broad acceptance across gastrointestinal, oncologic, reconstructive, and minimally invasive procedures, with professional societies such as SAGES publishing dedicated clinical guidelines for fluorescence image-guided surgery. Recent FDA approvals and expanded indications for fluorescence imaging technologies further highlight the growing clinical importance of real-time tissue perfusion assessment, anatomical visualization, and intraoperative decision support. These advancements are being enabled by improvements in high-resolution sensors, image processing capabilities, and visualization software integrated directly into surgical workflows.

Analysis by Product

Endoscopic Visualization Systems

Based on product, the endoscopic visualization systems segment is expected to hold the largest share in 2026. This dominance is driven by the increasing demand for high-definition imaging in laparoscopic and arthroscopic procedures. Integrated endoscopic platforms provide a centralized 'source of truth' for surgical imaging and device status, enabling more efficient regional surgical coordination. Key sub-segments include surgical microscopes and exoscopes, which provide superior magnification and ergonomics for complex neurosurgery and ENT procedures. Digital surgery platforms are also essential for providing surgical teams with immediate access to critical procedural data.

Surgical Displays and Navigation Systems

The surgical display systems segment remains vital, providing the physical infrastructure for data visualization. This includes high-resolution 4K and 3D monitors, surgical cameras, and integration gateways that facilitate connectivity between disparate surgical devices. Simultaneously, the surgical navigation systems segment—including strategic consulting, custom implementation, and post-deployment support—is growing in importance as healthcare organizations seek expert guidance for organizational change management and technical integration. As surgical visualization solutions become more complex, the need for comprehensive maintenance and support services is becoming a critical success factor for hospitals.

Analysis by Technology

Based on technology, the 4K/3D visualization segment is expected to account for the largest share in 2026, reflecting the critical need for seamless communication and high-definition visualization in complex surgical procedures. Fluorescence imaging systems and image-guided surgery systems are also significant segments, providing the infrastructure for real-time surgical data access and interoperability. The integration of augmented reality (AR) and mixed reality (MR) tools is projected to witness the fastest growth, as hospitals prioritize minimally invasive interventions and automated surgical workflows.

Geographic Analysis: Regional Growth and Digital Health Adoption

North America is expected to dominate the global surgical visualization systems market in 2026, accounting for around 46.5% of total revenue. The region's leadership is supported by high adoption of minimally invasive and image-guided surgical procedures, substantial investments in advanced operating room infrastructure, and strong demand for 4K/3D visualization, surgical navigation, and fluorescence-guided imaging technologies. The presence of leading market participants, well-established healthcare facilities, and favorable reimbursement frameworks continues to support the adoption of advanced surgical visualization systems across the U.S. and Canada.

Asia Pacific is projected to register the fastest growth during the forecast period. Growth is driven by expanding healthcare infrastructure, increasing surgical procedure volumes, rising healthcare expenditure, and growing adoption of minimally invasive surgery across China, India, Japan, and Southeast Asian countries. Government investments in hospital modernization and the increasing availability of advanced surgical technologies are accelerating demand for endoscopic visualization systems, surgical microscopes, navigation platforms, and image-guided surgery solutions throughout the region.

The competitive landscape of the global surgical visualization systems market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end clinical care orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with robotic systems and other clinical management platforms. Strategic acquisitions of niche sensor and analytics companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between visualization vendors and healthcare providers to ensure seamless surgical monitoring across the care continuum.

Key players operating in the global market include Stryker Corporation (U.S.), Karl Storz SE & Co. KG (Germany), Olympus Corporation (Japan), Carl Zeiss Meditec AG (Germany), Smith & Nephew plc (U.K.), Richard Wolf GmbH (Germany), Leica Microsystems (Danaher) (Germany), ConMed Corporation (U.S.), B. Braun Melsungen AG (Germany), Medtronic plc (Ireland), Fujifilm Holdings Corporation (Japan), Barco NV (Belgium), Eizo Corporation (Japan), and various emerging technology providers specializing in AI-driven surgical analytics and advanced visualization tools.

The market is projected to reach USD 13.6 billion by 2036, growing at a CAGR of 10.4% from 2026 to 2036.

Hospitals report a significant reduction in procedure times and an improvement in surgical workflow efficiency and patient safety.

The Artificial Intelligence & Machine Learning (AI/ML) and Augmented Reality (AR) segments are expected to grow the fastest.

Software-enabled capabilities are becoming a key differentiator in new surgical visualization deployments in 2026. While hardware continues to account for the majority of market revenue, AI-powered image processing, surgical navigation software, workflow integration, and intraoperative analytics are representing an increasing share of new system value and purchasing decisions.

North America holds the largest share, estimated at 46.5% in 2026, driven by high adoption of MIS and robotic systems.

AI enables the prediction of surgical demand and optimizes procedure scheduling, improving resource distribution and patient safety.

The pressure to reduce surgical errors and procedure times is driving the demand for integrated platforms to manage high volumes.

Hospitals and clinics are the primary adopters, managing the highest volumes of diverse integrated surgical suites.

These systems provide the continuous, data-driven surgical management necessary to improve clinical outcomes and reduce the total cost of care.

The top 5 players are Stryker, Karl Storz, Olympus, Carl Zeiss Meditec, and Smith & Nephew.

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates