Resources

About Us

Surgical Video Analytics Market Size, Share, Forecast, & Trends Analysis by Offering (Software, Hardware, Services), Deployment Mode, Application (Intraoperative Guidance, Training & Skills Assessment), Surgical Approach, Surgical Specialty, End User, and Geography — Global Forecast to 2036

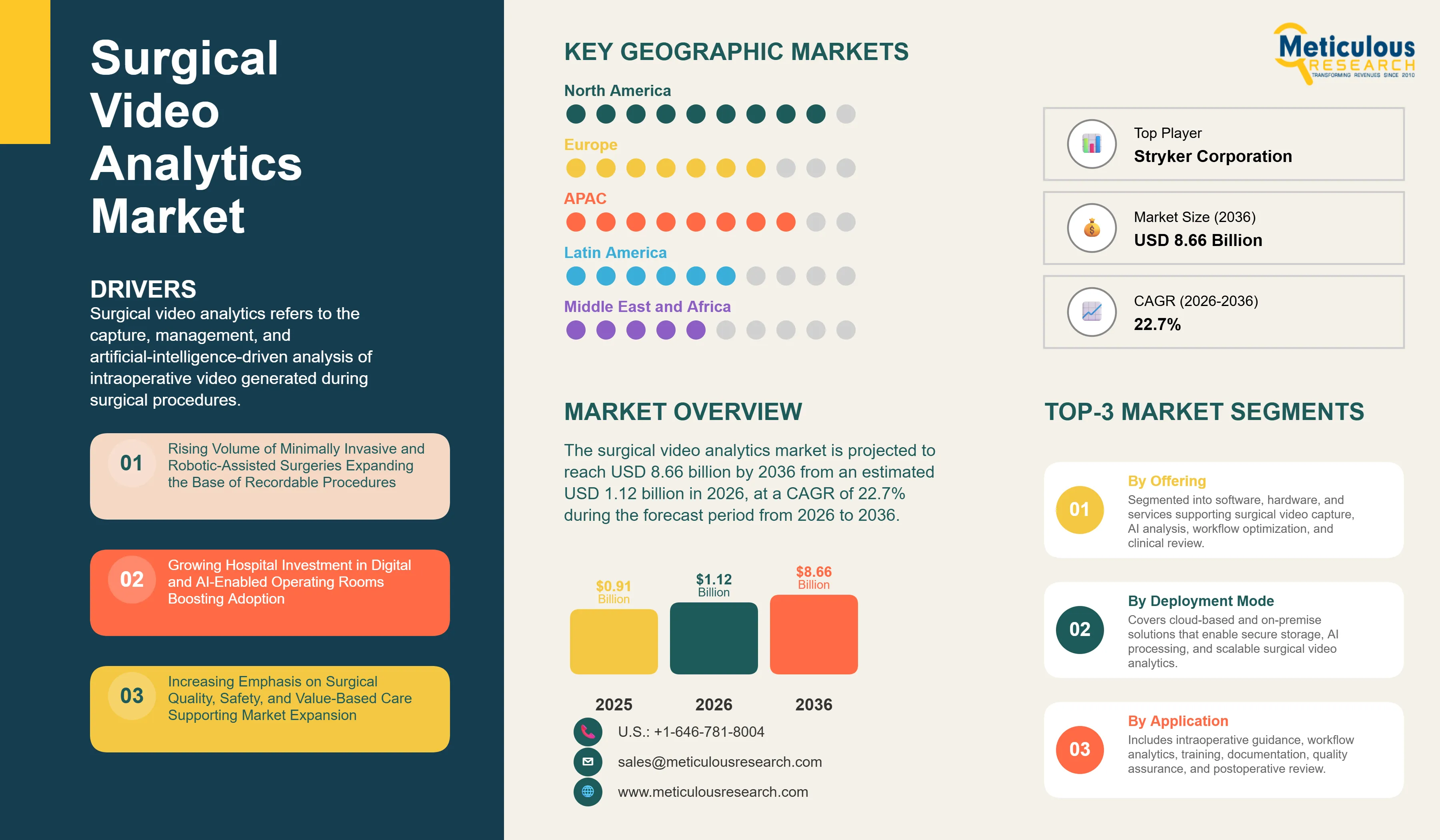

Report ID: MRHC - 1042098 Pages: 257 Jul-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global surgical video analytics market is projected to reach USD 8.66 billion by 2036 from an estimated USD 1.12 billion in 2026, at a CAGR of 22.7% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

Surgical video analytics refers to the capture, management, and artificial-intelligence-driven analysis of intraoperative video generated during surgical procedures. These systems combine recording hardware, cloud or on-premise software, and computer-vision algorithms to convert raw operative footage into structured, searchable data — recognizing procedural phases, instruments, anatomy, and events, and linking them to workflow, training, documentation, and quality metrics. The category spans dedicated platforms from large surgical-device manufacturers as well as specialist software firms, and increasingly overlaps with robotic surgery, endoscopy, and operating-room integration systems.

According to Johnson & Johnson MedTech, more than 330 million surgical procedures are performed worldwide each year, while the Lancet Commission on Global Surgery estimates approximately 313 million major operations annually — a vast and expanding pool of procedures, a growing share of which are visualized through a camera and therefore recordable.

The most important structural driver is the shift toward minimally invasive surgery (MIS), which by design produces a video feed. Peer-reviewed analysis of U.S. surgical training data shows minimally invasive approaches rising sharply between 2003 and 2018 — laparoscopic cholecystectomy from 88% to 94%, appendectomy from 38% to 93%, and colectomy from 8% to 43% of cases. Robotic-assisted surgery has compounded this effect: Intuitive Surgical reports an installed base exceeding 11,000 da Vinci systems and more than 3 million procedures performed in 2025 alone, each generating rich, standardized video and system data.

Demand is further reinforced by a persistent surgical safety and quality gap. Published surgical-safety literature indicates that preventable surgical errors account for nearly half of all in-hospital adverse events, and that variability in intraoperative technique remains a measurable contributor to complications. Video-based analytics offers hospitals an objective mechanism to review performance, standardize technique, support training, and document care — needs that have historically been served only through subjective, manual review.

Hospital digitization is turning that demand into procurement. Johnson & Johnson MedTech reports that over 90% of U.S. hospitals and health systems now operate an AI or automation strategy, up from 53% in 2019, and that roughly 95% of surveyed healthcare professionals advocate for greater use of AI in their practice. Combined with the expansion of cloud-based delivery, flexible subscription pricing models, and integration with electronic health records, these forces position surgical video analytics for sustained double-digit growth, driven by the need for surgical transparency, operational efficiency, and data-driven care.

Rising Volume of Minimally Invasive and Robotic-Assisted Surgeries

The key driver of the surgical video analytics market is the expanding volume of camera-based surgery. Minimally invasive and robotic-assisted procedures inherently generate an endoscopic or console video stream, creating the raw material on which analytics depends. As MIS displaces open surgery across specialties, the addressable base of recordable procedures grows in lockstep.

The scale of this transition is substantial. Peer-reviewed U.S. data show minimally invasive representation increasing across every studied procedure between 2003 and 2018, with appendectomy rising from 38% to 93% and colectomy from 8% to 43% of cases. Robotic surgery has accelerated the trend: By the end of 2025, Intuitive Surgical's installed base of da Vinci surgical systems had surpassed 11,000 worldwide. Approximately 3.15 million da Vinci procedures were performed during the year, representing around 18% year-over-year growth, while the cumulative number of patients treated using da Vinci surgical systems exceeded 20 million. Competing platforms — Medtronic's Hugo, which received U.S. FDA clearance for urologic procedures in December 2025, and Johnson & Johnson's Ottava, submitted for FDA review in early 2026 — are widening the installed base further.

Each of these procedures produces standardized, high-quality video and, in the robotic case, synchronized system data. This has made surgical video the fastest-growing untapped data asset in the operating room and the primary substrate for analytics adoption. As robotic and laparoscopic volumes continue to climb across urology, gynecology, general surgery, and thoracic care, the volume of recordable procedures directly expands the surgical video analytics market.

Growing Hospital Investment in Digital and AI-Enabled Operating Rooms

Hospitals are moving beyond isolated video capture toward integrated, intelligent operating rooms, and this capital shift is a direct catalyst for surgical video analytics adoption. Digital-OR integration platforms, such as KARL STORZ's OR1 and AIDA, Stryker's Connected OR Hub, and Caresyntax's ORI, consolidate video, device data, and imaging into a single environment, providing the infrastructure into which analytics software is sold.

The strategic intent behind this investment is now widespread. According to Johnson & Johnson MedTech, more than 90% of U.S. hospitals and health systems have an AI or automation strategy in place, compared with 53% in 2019, while approximately 95% of surveyed clinicians support expanded use of AI. Vendors have responded by embedding analytics directly into their flagship platforms. Medtronic's Touch Surgery ecosystem combines video capture with AI-enabled post-operative workflow analysis and performance insights, while Intuitive's da Vinci 5—featuring more than 10,000 times the computing power of the da Vinci Xi—supports advanced data analytics, integrated video review, and objective surgical performance insights.

Because analytics platforms are typically sold as software and services layered onto this hardware, rising digital-OR capital expenditure directly enlarges the recurring-revenue opportunity for surgical video analytics providers. The trend is particularly pronounced in academic medical centers and large integrated delivery networks, which are standardizing surgical video capture as part of enterprise quality and training programs.

Expansion of Cloud-Based Surgical Intelligence and Subscription Models

The migration of surgical video analytics to cloud-based, subscription delivery represents one of the most significant growth opportunities, lowering the barrier to adoption and creating durable recurring revenue for providers. Cloud deployment removes the capital burden of on-premise storage and compute, enables centralized algorithm updates, and allows analytics to scale across multiple sites from a single platform.

Adoption signals are strong. Cloud-based surgical intelligence platforms, including Medtronic's Touch Surgery ecosystem on AWS, Theator's surgical intelligence platform, and Caresyntax's edge-to-cloud ORION analytics, are being sold as software-as-a-service, aligning cost with usage and easing procurement for hospitals unable to justify large upfront systems. Caresyntax, which reports its platform in use across more than 3,000 operating rooms, has raised substantial growth capital to scale cloud adoption, while Proximie reports deployment in 500 hospitals across more than 50 countries.

This delivery model unlocks segments previously priced out of surgical analytics, particularly ambulatory surgical centers, community hospitals, and providers in emerging markets. It also enables continuous model improvement, as pooled, de-identified video strengthens the underlying algorithms over time. Recent ecosystem moves, such as the June 2026 collaboration between Oracle Health and Theator to distribute AI surgical intelligence to U.S. hospital customers, illustrate how cloud partnerships are broadening market access. The combination of lower entry cost, recurring revenue, and network effects makes cloud-based surgical intelligence a defining commercial opportunity for the market.

By Offering: The Software Segment to Dominate the Surgical Video Analytics Market in 2026

Based on offering, the surgical video analytics market is segmented into software, hardware, and services. In 2026, the software segment accounts for the largest share of 52.4% of the global surgical video analytics market. The large share of this segment is primarily attributed to the central role of video management platforms and AI analytics algorithms, which deliver the core value of the category — turning raw footage into structured, actionable insight.

Software also benefits from favorable economics, as platforms such as Medtronic's Touch Surgery ecosystem, Theator's surgical intelligence platform, and Caresyntax's ORION analytics are sold on recurring licenses that scale independently of hardware. Their ability to layer onto existing endoscopic and robotic infrastructure, and to improve continuously through algorithm updates, further reinforces the segment's leading position.

However, the services segment is projected to record the highest CAGR during the forecast period. Growth is driven by rising demand for managed clinical review, implementation, and analytics-as-a-service offerings, as hospitals seek outcomes without building in-house data-science capacity. Expert-led review services — pioneered by offerings such as C-SATS and adopted across surgical-intelligence vendors — are expanding as health systems outsource performance assessment and documentation workflows.

By Deployment Mode: The Cloud-Based Segment to Dominate the Surgical Video Analytics Market in 2026

Based on deployment mode, the market is segmented into cloud-based and on-premise. In 2026, the cloud-based segment accounts for the largest share of 63.8% of the global surgical video analytics market. This dominance reflects the lower upfront cost, elastic storage, centralized model updates, and multi-site scalability that cloud platforms provide, making them the default choice for enterprise surgical-video programs.

Leading vendors have standardized on cloud or hybrid edge-to-cloud architectures, with automatic de-identification, encryption, and compliance controls that address hospital data-governance requirements. The same attributes that make cloud attractive today — recurring cost alignment and continuous improvement — are expected to sustain its lead.

The cloud-based segment is also projected to grow fastest during the forecast period, as health systems consolidate surgical data onto centralized platforms and as regulatory clearances expand the range of cloud-delivered analytics. On-premise deployment retains relevance where data-residency or latency requirements are strict, but its share is expected to decline steadily relative to cloud.

By Application: The Surgical Training & Skills Assessment Segment to Dominate the Market in 2026

Based on application, the market is segmented into intraoperative guidance & decision support, surgical workflow & operating-room efficiency analytics, surgical training & skills assessment, quality assurance & surgical documentation, and postoperative performance review. In 2026, the surgical training & skills assessment segment accounts for the largest share of 28.6% of the global surgical video analytics market. This reflects the earliest and most established use case for surgical video — objective assessment of technique and structured trainee feedback — which underpins offerings such as Medtronic's Touch Surgery, Intuitive's Case Insights, and C-SATS.

However, the intraoperative guidance & decision support segment is projected to record the highest CAGR during the forecast period. Growth is driven by the maturation of real-time capabilities and their progression through regulatory clearance — exemplified by Intuitive's da Vinci 5 real-time insights, which received FDA 510(k) clearance in 2025. As live anatomy recognition, safety alerts, and decision support move from development into commercial use, this application is expected to become the fastest-expanding portion of the market.

By Surgical Approach: The Laparoscopic Surgery Segment to Dominate the Market in 2026

Based on surgical approach, the market is segmented into laparoscopic surgery, robotic-assisted surgery, endoscopic surgery, open surgery, and other approaches. In 2026, the laparoscopic surgery segment is expected to hold the largest share of 40.7% of the global surgical video analytics market. Laparoscopy represents the largest installed base of camera-based procedures worldwide and spans the broadest range of specialties, giving it the widest pool of recordable cases for analysis.

Because laparoscopic systems are ubiquitous across general surgery, gynecology, and urology, analytics vendors have prioritized compatibility with existing laparoscopic scopes, allowing hospitals to adopt video analytics without replacing capital equipment. This broad applicability sustains the segment's leading share.

However, the robotic-assisted surgery segment is projected to grow fastest during the forecast period. Robotic platforms generate richer, synchronized video and kinematic data and are expanding rapidly, with multiple new systems entering the market. As robotic procedure volumes accelerate and manufacturers embed analytics directly into their consoles, robotic-assisted surgery is expected to be the highest-growth approach for video analytics adoption.

By Surgical Specialty: The General Surgery Segment to Dominate the Market in 2026

Based on surgical specialty, the market is segmented into general surgery, gynecology, urology, orthopedic surgery, cardiothoracic surgery, neurosurgery, otolaryngology, bariatric surgery, colorectal surgery, and others. In 2026, the general surgery segment holds the largest share of 28.9% of the global surgical video analytics market. General surgery encompasses the highest volume of minimally invasive procedures, such as cholecystectomy, appendectomy, and hernia repair, providing the broadest and most standardized base of recordable cases.

The specialty's high procedure volume, established laparoscopic and robotic adoption, and clear training and quality use cases make it the natural entry point for surgical video analytics, sustaining its leading position.

However, the neurosurgery segment is projected to record the fastest growth during the forecast period, driven by the high complexity and stakes of neurosurgical procedures, where precision visualization and objective performance review deliver disproportionate value. Rising adoption of advanced visualization and microsurgery analytics in this specialty is expected to outpace broader market growth.

By End User: The Hospitals Segment to Dominate the Surgical Video Analytics Market through 2036

Based on end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, academic & research institutes, and medical device & life sciences companies. In 2026, the hospitals segment accounts for the largest share of 61.2% of the global surgical video analytics market. Hospitals perform the majority of complex and high-volume surgical procedures, hold the largest robotic and laparoscopic installed bases, and have the resources and quality mandates to invest in enterprise surgical-video programs.

Large hospitals and integrated delivery networks are also the primary adopters of digital-OR infrastructure and value-based quality initiatives, both of which anchor surgical video analytics purchasing, reinforcing the segment's dominant share.

However, the ambulatory surgical centers (ASC) segment is projected to grow fastest during the forecast period. The migration of surgical volume to lower-cost outpatient settings, combined with cloud-based, subscription delivery that fits ASC economics, is expanding access to analytics beyond large hospitals. As vendors and robotic manufacturers increasingly target ASCs, this segment is expected to record the highest growth.

North America Dominated the Surgical Video Analytics Market in 2025

Based on geography, the global surgical video analytics market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2026, North America accounts for the largest share of 42.5% of the global surgical video analytics market.

The large share of North America is attributed to the region's dense robotic and laparoscopic installed base, high per-capita surgical volume, early and widespread digital-OR investment, and the concentration of leading vendors, such as Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, Stryker, Surgical Safety Technologies, and Theator. The United States represents the dominant national market, supported by strong hospital AI adoption and value-based care programs that reward measurable surgical quality.

However, the Asia-Pacific is expected to register the fastest CAGR during the forecast period. Rapid expansion of surgical capacity, rising minimally invasive and robotic adoption across China, India, Japan, and South Korea, and growing investment in hospital digitization are driving demand for surgical video analytics. Europe remains a significant market, led by Germany, the United Kingdom, and France, where surgical-safety initiatives and academic adoption of video-based training support steady growth.

Major companies in the global surgical video analytics market have pursued strategies including product launches & enhancements, partnerships & collaborations, acquisitions, and geographic expansion to strengthen their positions. Product launches and enhancements, together with ecosystem partnerships, have accounted for the majority of strategic activity, as large medtech firms embed analytics into flagship platforms and specialist vendors extend cloud reach.

Some of the prominent players operating in the global surgical video analytics market include Medtronic plc (Ireland), Intuitive Surgical, Inc. (U.S.), Johnson & Johnson (through Johnson & Johnson MedTech) (U.S.), Olympus Corporation (Japan), Stryker Corporation (U.S.), KARL STORZ SE & Co. KG (Germany), Carl Zeiss Meditec AG (Germany), Brainlab AG (Germany), Caresyntax GmbH (Germany), Theator Inc. (U.S.), Proximie Ltd. (U.K.), Surgical Safety Technologies Inc. (Canada), Surgical Science Sweden AB (Sweden), Activ Surgical, Inc. (U.S.), and Apella, Inc. (U.S.).

|

Particulars |

Details |

|

Forecast Period |

2026–2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

22.7% |

|

Market Size (Value) in 2026 |

USD 1.12 Billion |

|

Market Size (Value) in 2036 |

USD 8.66 Billion |

|

Segments Covered |

By Offering - Software - Hardware - Services By Deployment Mode - Cloud-Based - On-Premise By Application - Intraoperative Guidance & Decision Support - Surgical Workflow & OR Efficiency Analytics - Surgical Training & Skills Assessment - Quality Assurance & Surgical Documentation - Postoperative Performance Review By Surgical Approach - Laparoscopic Surgery - Robotic-Assisted Surgery - Endoscopic Surgery - Open Surgery - Other Approaches By Surgical Specialty - General Surgery, Gynecology, Urology, Orthopedic, Cardiothoracic, Neurosurgery, ENT, Bariatric, Colorectal, Others By End User - Hospitals - Ambulatory Surgical Centers - Specialty Clinics - Academic & Research Institutes - Medical Device & Life Sciences Companies |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Netherlands, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, Israel, and Rest of Middle East & Africa) |

|

Key Companies |

Medtronic plc (Ireland), Intuitive Surgical, Inc. (U.S.), Johnson & Johnson (U.S.), Olympus Corporation (Japan), Stryker Corporation (U.S.), KARL STORZ SE & Co. KG (Germany), Carl Zeiss Meditec AG (Germany), Brainlab AG (Germany), Caresyntax GmbH (Germany), Theator Inc. (U.S.), Proximie Ltd. (U.K.), Surgical Safety Technologies Inc. (Canada), Surgical Science Sweden AB (Sweden), Activ Surgical, Inc. (U.S.), and Apella, Inc. (U.S.) |

The global surgical video analytics market size is estimated at USD 1.12 billion in 2026.

The market is projected to grow from USD 1.12 billion in 2026 to USD 8.66 billion by 2036, at a CAGR of 22.7%.

The surgical video analytics market is projected to reach USD 8.66 billion by 2036, at a compound annual growth rate (CAGR) of 22.7% from 2026 to 2036.

Key companies operating in this market include Medtronic plc (Ireland), Intuitive Surgical, Inc. (U.S.), Johnson & Johnson (U.S.), Olympus Corporation (Japan), Stryker Corporation (U.S.), KARL STORZ SE & Co. KG (Germany), Caresyntax GmbH (Germany), Theator Inc. (U.S.), Surgical Safety Technologies Inc. (Canada), and others.

The shift toward real-time intraoperative decision support, integration of video analytics with robotic platforms and hospital information systems, and the migration to cloud-based surgical intelligence are prominent trends in the market.

By offering, the software segment held the largest share; by deployment mode, the cloud-based segment dominated; by application, the surgical training & skills assessment segment held the largest share, while intraoperative guidance & decision support is expected to grow fastest; by surgical approach, laparoscopic surgery led; by surgical specialty, general surgery dominated; by end user, the hospitals segment held the largest share; and by geography, North America commanded the largest share in 2025.

North America holds the largest share of the surgical video analytics market in 2025, supported by dense robotic installed bases, high surgical volume, and early digital-OR investment. Asia-Pacific is expected to register the highest growth rate during the forecast period, driven by expanding surgical capacity and rising minimally invasive and robotic adoption.

Key drivers include the rising volume of minimally invasive and robotic-assisted surgeries, growing hospital investment in digital and AI-enabled operating rooms, and an increasing emphasis on surgical quality, safety, and value-based care. These factors are collectively accelerating adoption of surgical video analytics across care settings.

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Jul-2026

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates