Resources

About Us

Smart Water Management Market by Offering (Hardware, Software, Services), Application (Water Quality & Quantity Monitoring, Water Management, Asset Management, Leak Detection, Analytics & Data Management, Rain & Stormwater Management, Others), End User (Residential, Commercial, Industrial), and Geography – Global Forecast to 2036

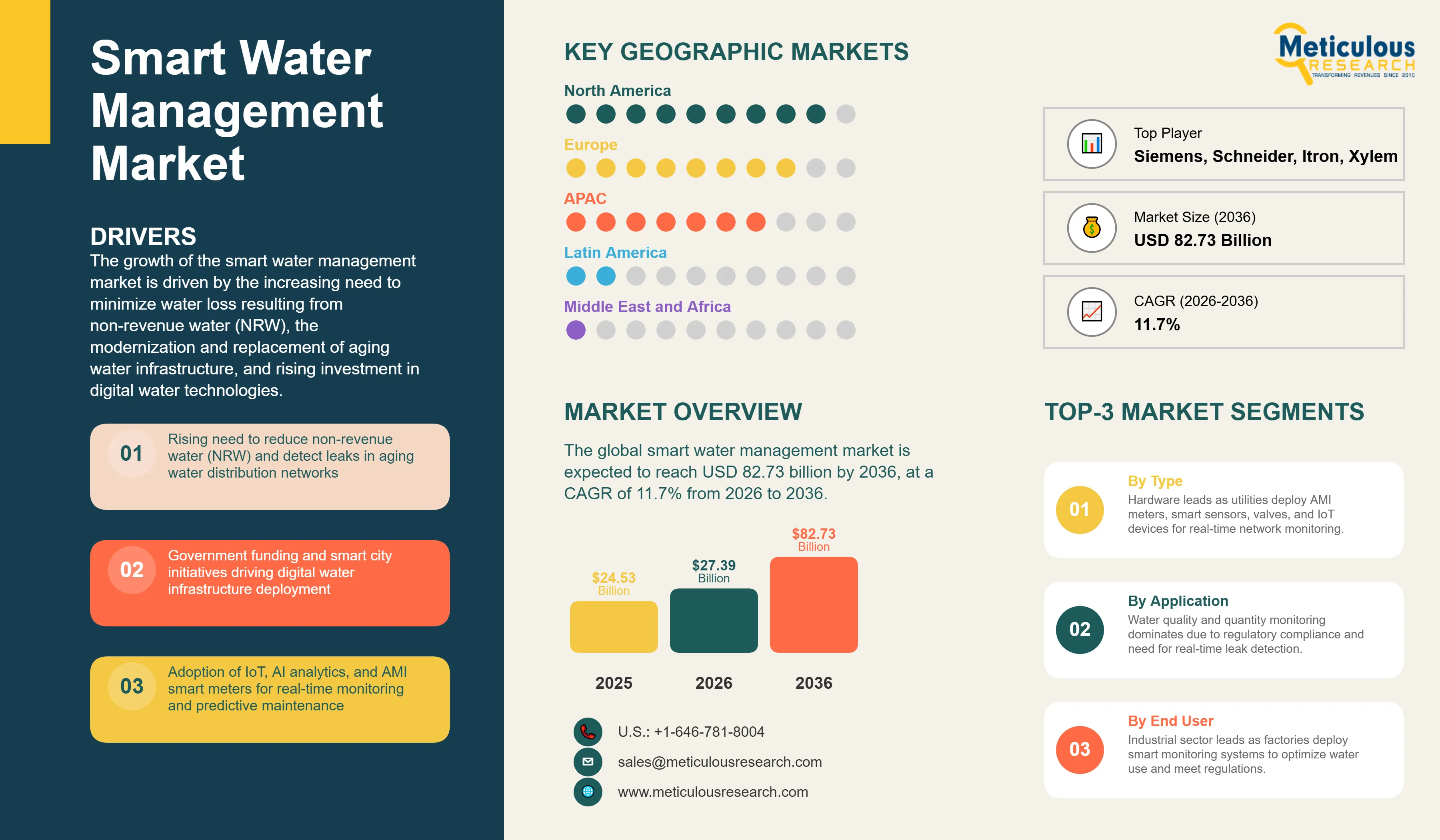

Report ID: MRICT - 104505 Pages: 255 Mar-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 48 Hours Download Free Sample ReportThe global smart water management market was valued at USD 24.53 billion in 2025. This market is expected to reach USD 82.73 billion by 2036 from USD 27.39 billion in 2026, at a CAGR of 11.7% from 2026 to 2036.

The growth of the smart water management market is driven by the increasing need to minimize water loss resulting from non-revenue water (NRW), the modernization and replacement of aging water infrastructure, and rising investment in digital water technologies. Capital flows into the broader water sector have strengthened in recent years. For instance, according to the White & Case LLP “Currents of Capital 2025” report, 30% of surveyed respondents deployed more than USD 500 million into the water sector in 2024, and a majority of organizations expected to increase investment levels in 2025 compared to the previous year. Government initiatives to integrate smart water management solutions into urban infrastructure programs, coupled with the proliferation of smart city projects globally, are also anticipated to create substantial growth opportunities for stakeholders in smart water management throughout the forecast period.

Smart water management solutions leverage advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), digital twin modeling, cloud analytics, advanced metering infrastructure (AMI), and LPWAN (Low-Power Wide-Area Network) connectivity to enable real-time monitoring, predictive maintenance, leak detection, and data-driven optimization of water distribution networks and treatment operations. The combination of these digital technologies with the urgent global need for sustainable water resource management, driven by accelerating water stress, stricter regulatory mandates, and the growing recognition of water as a strategic economic resource, is reshaping the water utility sector and creating significant demand for integrated smart water management platforms across residential, commercial, and industrial end users worldwide.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Smart water management (SWM) encompasses the integrated application of digital technologies, data analytics, and automation to optimize every stage of the water cycle, from source abstraction and treatment through distribution, consumption monitoring, leak detection, and wastewater management. SWM platforms integrate hardware components including smart meters (AMI and AMR), IoT-enabled sensors, smart pumps and drives, smart valves, and water controllers with software platforms for cloud-based and on-premise analytics, SCADA integration, digital twin modeling, asset management, geographic information systems (GIS), and customer engagement portals. These integrated systems enable water utilities, industrial operators, commercial facilities, and residential consumers to monitor water usage in real time, detect leaks and anomalies proactively, optimize pressure management, improve billing accuracy, and make data-driven decisions that enhance operational efficiency and resource sustainability.

The smart water management market is undergoing accelerated digital transformation driven by the combination of escalating water scarcity, aging water infrastructure, rising regulatory requirements, and the maturation of enabling technologies. In 2025, China invested a record USD 182.4 billion (1.28 trillion yuan) in the construction of water conservancy facilities, exceeding the trillion-yuan mark for the fourth consecutive year. In the U.S., the Bipartisan Infrastructure Law continues to direct more than USD 50 billion via the EPA toward improvements in drinking water, wastewater, and stormwater infrastructure, helping catalyze utility investment in modernization efforts such as smart metering, leak detection, and digital water management systems across North America. These substantial public investment programs are directly catalyzing procurement of smart metering, leak detection, and digital water management systems.

Accelerating Adoption of Advanced Metering Infrastructure (AMI) and IoT-Enabled Smart Meters

The ongoing transition from conventional mechanical meters and one-way automated meter reading (AMR) systems to advanced metering infrastructure (AMI) is a key trend in the global smart water management market. Unlike legacy systems, AMI enables two-way communication, interval-based consumption measurement, remote meter configuration, and real-time data transmission to utility control centers. This transition is allowing utilities to move from reactive billing models to proactive network management strategies.

AMI deployments now represent the dominant technology pathway for new smart water meter installations in developed markets. Utilities are increasingly prioritizing AMI to improve billing accuracy, reduce non-revenue water (NRW), detect customer-side leaks, enable time-of-use pricing structures, and enhance customer engagement through digital portals and mobile applications. The granular consumption data generated by AMI supports predictive maintenance and demand forecasting, improving operational efficiency across distribution networks.

As utilities seek to digitize water infrastructure while managing capital expenditure constraints, AMI and IoT-integrated smart metering systems are becoming foundational components of broader digital water strategies. This trend is expected to continue accelerating through 2036, driven by regulatory pressure to reduce water losses, improve transparency, and enhance resilience against climate-related water stress.

Growing Integration of AI, Machine Learning, and Digital Twin Technology in Water Networks

The growing integration of artificial intelligence, machine learning, and digital twin technology into smart water management platforms is transforming water utility operations from reactive, manual processes to proactive, data-driven management. Digital twins enable utilities to simulate outcomes, predict pipe failures, optimize pressure zones, and plan capital projects based on risk scores rather than asset age alone. Enterprise asset management modules integrated with hydraulic modeling engines predict pipe failures well ahead of visible leaks, reducing emergency repair expenditure significantly. AI algorithms applied to real-time sensor data from distribution networks can identify leak signatures, quantify non-revenue water losses, and prioritize intervention responses with a precision that is unachievable through conventional monitoring. Utilities implementing smart water systems with AI analytics achieve 15–30% reductions in water losses, yielding substantial operational savings. Shenzhen, China, has deployed IoT-enabled smart metering across over 80% of residential households, reducing NRW rates to approximately 6.2%.

Rising Governmental Initiatives and Smart City Programs Driving Large-Scale Deployments

Rising governmental initiatives to integrate smart water management into national infrastructure investment programs and the accelerating growth of smart city projects globally are creating significant large-scale deployment opportunities for smart water management technology and service providers. In the U.S., the Bipartisan Infrastructure Law’s water infrastructure provisions and the EPA’s WaterSense program are catalyzing municipal smart metering deployments and digital water system upgrades across hundreds of utilities. In Germany, the government’s Digital Strategy 2025 mandates a national rollout of smart meters to commercial and residential customers from 2025, creating a large addressable market for smart water metering providers. China continues to invest in water conservancy modernization, committing record capital to smart irrigation, urban water distribution digitization, and industrial water efficiency programs. Smart city projects across Asia-Pacific, the Middle East, and Europe are embedding smart water management as a core infrastructure component, thereby driving the growth of the overall smart water management market.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 82.73 Billion |

|

Market Size in 2025 |

USD 24.53 Billion |

|

Market Size in 2026 |

USD 27.39 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 11.7% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Offering: Hardware (Meters [AMR Meters, AMI Meters, Water Flow Meters], Smart Water Sensors, Water Controllers, Smart Pumps and Drives, Smart Valves, Other Hardware), Software (Cloud-based Deployments, On-premise Deployments), Services (Consulting Services, Integration and Deployment Services, Support and Maintenance Services) By Application: Water Quality & Quantity Monitoring, Water Management, Asset Management, Leak Detection, Analytics & Data Management, Rain & Stormwater Management, Other Applications By End User: Residential, Commercial, Industrial (Manufacturing, Agriculture, Utilities, Energy, Mining, Oil & Gas, Food & Beverage, Automotive, Pulp & Paper, Chemical, Textile, Construction) By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Why Does the Hardware Segment Dominate the Smart Water Management Market?

Based on offering, in 2026, the hardware segment is expected to account for the largest share of the global smart water management market. The significant market share of this segment is attributed to the increasing demand for automated meter reading for billing and analytical purposes, the widespread deployment of wireless communication-enabled smart meters capable of transmitting water usage data directly to central utility management systems, and the large installed base replacement cycle underway as utilities upgrade conventional mechanical meters to AMI and AMR devices.

However, the services segment is expected to witness the fastest CAGR during the forecast period. Professional services, managed services, and outcome-based service contracts are growing at an accelerated pace as utilities recognize that the full operational and financial value of smart water investments is realized only when supported by embedded data science expertise, system integration capabilities, and ongoing change management support. Vendors are increasingly offering multi-year platform agreements that bundle hardware, software licensing, connectivity, and guaranteed operational performance improvements, generating highly recurring and visible service revenue streams.

Why Does the Water Quality & Quantity Monitoring Segment Dominate the Smart Water Management Market?

Based on application, in 2026, the water quality & quantity monitoring segment is expected to account for the largest share of the global smart water management market. The large share of this segment is mainly attributed to the increasing deployment of IoT-enabled sensors for continuous real-time monitoring of water quality parameters, including physical, chemical, and microbial properties, across distribution networks, treatment plants, and industrial process water systems.

The leak detection application segment is expected to witness strong growth during the forecast period, driven by the growing financial imperative for utilities to reduce non-revenue water losses and the increasing sophistication of AI-powered acoustic leak detection, pressure transient analysis, and anomaly detection algorithms that can pinpoint leak locations in complex pipe networks with high accuracy.

Why Does the Industrial Segment Dominate the Smart Water Management Market?

Based on end user, in 2026, the industrial segment is expected to account for the largest share of the global smart water management market. The large market share of this segment is attributed to the widespread adoption of smart water management solutions across diverse industrial sectors such as manufacturing, agriculture, utilities, energy, mining, oil & gas, food & beverage, chemicals, and construction, which are deploying integrated IoT monitoring, real-time consumption analytics, and automated control systems to measure and manage water use at individual plant and process levels. Industrial operators use smart water management platforms to reduce operational costs by optimizing water consumption, minimize regulatory compliance risk through automated effluent monitoring and reporting, identify process inefficiencies driving excess water usage, and trigger automated alerts when consumption or quality parameters deviate from established thresholds.

The commercial segment is expected to witness the fastest CAGR during the forecast period, driven by stringent regulations and mandates governing water usage and conservation in commercial buildings, retail facilities, healthcare campuses, and data centers, and by the growing adoption of smart water solutions to meet corporate sustainability, ESG reporting, and net-zero water targets.

U.S. Smart Water Management Market Size and Growth 2026 to 2036

The U.S. smart water management market is projected to grow at a strong CAGR from 2026 to 2036, driven by the substantial federal funding provisions of the Bipartisan Infrastructure Law, the EPA’s expanded focus on water system cybersecurity and PFAS remediation, and the growing adoption of AMI metering, leak detection, and AI-powered distribution network analytics by municipal water utilities across the country. The U.S. is also a leader in smart water management innovation, with companies including IBM, Honeywell, Cisco, Mueller Water Products, Badger Meter, Trimble, HydroPoint, Sensus, Neptune Technology, and Itron headquartered or with major operations in the country.

Which Factors Support the Growth of the Asia-Pacific Smart Water Management Market?

Asia-Pacific is expected to register the fastest CAGR during the forecast period of 2026 to 2036. The growth of smart water management market in this region is primarily attributed to the combination of rapidly expanding urban populations and industrial activity that are straining existing water infrastructure, ambitious national smart city programs in China, India, South Korea, Singapore, and Japan, and significant government investment in digital water infrastructure and water security. China is a major driver of regional growth, with USD 182.4 billion invested in water conservancy facilities in 2025 and Shenzhen's deployment of IoT-enabled smart metering across over 80% of residential households achieving NRW rates of approximately 6.2%. Japan's coordinated smart water metering pilots in Tokushima, Kumamoto, and Kyoto highlight national-level commitment to household demand optimization and distribution network digitization. Singapore's PUB utility has achieved a 54.4% reduction in non-revenue water since 2010 and 750% increase in smart meter coverage since 2015, serving as a global benchmark for smart water management implementation. South Korea and India are also high-growth markets, driven by smart city infrastructure investment and growing industrial water management requirements.

The report provides a comprehensive competitive landscape based on an in-depth assessment of the key growth strategies adopted by leading market participants in the smart water management market during 2023–2026. The analysis evaluates strategic developments such as product innovations, partnerships, acquisitions, technology integrations, geographic expansions, and digital platform enhancements.

The key players profiled in this report include Xylem Inc. (U.S.) — including its Sensus smart metering and AMI portfolio — Itron, Inc. (U.S.), Schneider Electric SE (France), Siemens AG (Germany), ABB Ltd. (Switzerland), Badger Meter, Inc. (U.S.), Kamstrup A/S (Denmark), Landis+Gyr Group AG (Switzerland), Mueller Water Products, Inc. (U.S.), IBM Corporation (U.S.), Honeywell International Inc. (U.S.), Cisco Systems, Inc. (U.S.), Oracle Corporation (U.S.), Endress+Hauser AG (Switzerland), Neptune Technology Group Inc. (U.S.), SUEZ SA (France), Veolia Environnement S.A. (France), Arad Group (Israel), Trimble Inc. (U.S.), and HydroPoint Data Systems, Inc. (U.S.), among others.

Smart Water Management Market, by Offering

Smart Water Management Market, by Application

Smart Water Management Market, by End User

Smart Water Management Market, by Geography

The global smart water management market is projected to reach USD 82.73 billion by 2036, growing at a CAGR of 11.7% from 2026 to 2036.

In 2026, the hardware segment is expected to account for the largest share of the global smart water management market, driven by the continued deployment of advanced metering infrastructure (AMI), automated meter reading (AMR) systems, smart sensors, communication modules, and IoT-enabled field devices.

The municipal utilities segment is expected to account for the largest share of the global smart water management market in 2026, driven by large-scale investments in distribution network modernization, non-revenue water reduction initiatives, regulatory compliance, and digital water infrastructure upgrades.

The growth of this market is driven by the increasing urgency to reduce non-revenue water losses, the need to modernize aging water infrastructure, rising government investment in water resilience and smart city programs, and escalating global water stress.

Key players operating in the smart water management market include IBM Corporation (U.S.), ABB Ltd. (Switzerland), Honeywell International Inc. (U.S.), Schneider Electric SE (France), Cisco Systems, Inc. (U.S.), Sensus (U.S.), Mueller Water Products, Inc. (U.S.), Trimble Inc. (U.S.), Arad Group (Israel), Oracle Corporation (U.S.), Badger Meter, Inc. (U.S.), Landis+Gyr Group AG (Switzerland), Kamstrup A/S (Denmark), SUEZ SA (France), HydroPoint (U.S.), Siemens AG (Germany), Itron, Inc. (U.S.), Endress+Hauser AG (Switzerland), Neptune Technology Group Inc. (U.S.), and Xylem Inc. (U.S.), among others.

Asia-Pacific is projected to register the highest CAGR during the forecast period (2026–2036), driven by rapid urbanization, industrial expansion, large-scale government investment in smart water and smart city programs across China, India, Japan, South Korea, and Southeast Asia, and increasing pressure from water scarcity and climate variability.

Published Date: Mar-2024

Published Date: Jun-2024

Published Date: Oct-2022

Published Date: Jan-2023

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates