Resources

About Us

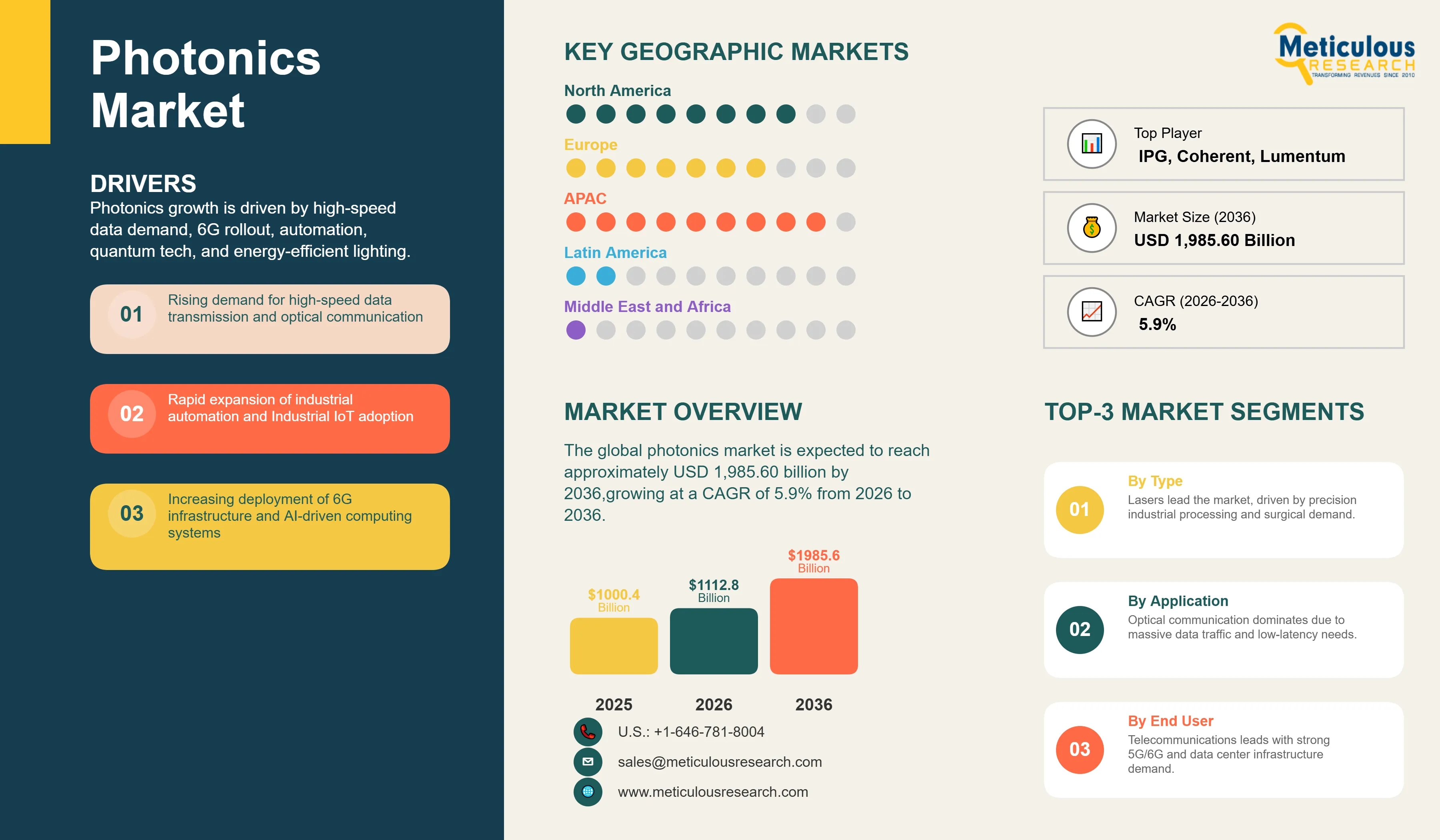

The global photonics market was valued at USD 1,000.40 billion in 2025. The market is expected to reach approximately USD 1,985.60 billion by 2036 from USD 1,112.80 billion in 2026, growing at a CAGR of 5.9% from 2026 to 2036. The growth of the overall photonics market is driven by the intensifying global focus on high-speed data transmission and the rapid expansion of the industrial automation and quantum computing sectors. As manufacturers seek to integrate more precision into manufacturing processes and address the increasing demand for energy-efficient lighting and display solutions, advanced photonic systems have become essential for maintaining operational efficiency and technological superiority. The rapid expansion of the 6G infrastructure and the increasing need for high-performance optical sensors and lasers continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Photonics systems are critical technological frameworks used to generate, manipulate, and detect light while allowing for high-speed data transfer and precision measurement throughout various industrial processes. These systems include lasers, sensors, and optical fibers, which are designed to withstand extreme operating conditions and fit into diverse technological ecosystems. The market is defined by high-efficiency components such as vertical-cavity surface-emitting lasers (VCSELs) and silicon photonic integrated circuits, which significantly enhance signal integrity and processing performance in data-intensive applications. These systems are indispensable for manufacturers seeking to optimize their internal hardware architecture and meet aggressive digital transformation targets.

The market includes a diverse range of technologies, ranging from simple light-emitting diodes for basic illumination to complex multilayer photonic integrated circuits for high-performance computing and quantum defense. These systems are increasingly integrated with advanced components such as adaptive optics and ultra-fast modulators to provide services such as real-time environmental sensing and improved spectral efficiency. The ability to provide stable, high-precision results while minimizing energy consumption has made advanced photonics products the technology of choice for industries where data throughput and reliability are paramount.

The global technology sector is pushing hard to modernize infrastructure capabilities, aiming to meet AI-driven processing and hyper-connected communication targets. This drive has increased the adoption of high-density optical interconnects, with advanced light-steering techniques helping to stabilize data transmission yields for ultra-fast network architectures. At the same time, the rapid growth in the autonomous vehicle and professional medical markets is increasing the need for high-reliability, LiDAR-based sensing and non-invasive diagnostic solutions.

Proliferation of Silicon Photonics and Quantum Integration

Manufacturers across the technology industry are rapidly shifting to light-optimized architectures, moving well beyond traditional electronic designs toward high-speed, low-power photonic setups. Intel’s latest silicon photonics engines deliver significantly higher bandwidth for data centers, while Hamamatsu’s recent installations have slashed detection limits in quantum sensing trials. The real game-changer comes with “smart” photonic circuits featuring integrated quantum key distribution capabilities that maintain peak security even in computationally noisy environments. These advancements make high-precision optical processing practical and cost-effective for everyone from tech startups to global aerospace giants chasing operational excellence and lower system latency.

Innovation in Miniaturized and Flexible Optical Systems

Innovation in miniaturized and flexible optical systems is rapidly driving the photonics market, as sensing devices become more compact and multi-functional. Equipment suppliers are now designing units that combine the structural integrity of traditional bulky optics with the versatility of flexible waveguides in a single assembly, saving valuable space and simplifying system logistics. These systems often involve advanced nano-fabrication and meta-surface technology capable of handling ultra-fine light beams without compromising signal strength or measurement reliability.

At the same time, growing focus on green technology is pushing manufacturers to develop photonics solutions tailored to energy-saving principles. These systems help reduce power waste through efficient light conversion processes and the use of recyclable optical substrates. By combining high-density light delivery with robust environmental performance, these new designs support both technological advancement and corporate sustainability, strengthening the resilience of the broader industrial value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 1,985.60 Billion |

|

Market Size in 2026 |

USD 1,112.80 Billion |

|

Market Size in 2025 |

USD 1,025.40 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 5.9% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Type, Application, End-User Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Digital Transformation and Rise of Industrial IoT

A key driver of the photonics market is the rapid movement of the global industrial sector toward data-backed, highly functional automation. Global consumer demand for high-speed internet, effective 3D sensing, and health-monitoring wearables has created significant incentives for the adoption of photonics products. The trend toward “smart” manufacturing and the integration of photonics into daily industrial workflows drive manufacturers toward scalable solutions that photonics can uniquely provide. It is estimated that as industrial adoption of automated routines rises and diagnostic tools become more decentralized through 2036, the need for robust, effective optical components increases significantly; therefore, lasers and sensors, with their ability to ensure high-density data delivery, are considered a crucial enabler of modern industrial design strategies.

Opportunity: 6G Deployment and Biophotonics Expansion

The rapid growth of the 6G network market and biophotonics technologies provides great opportunities for the photonics market. Indeed, the global surge in data consumption has created a compelling demand for systems that can replace traditional copper-based transmission and integrate seamlessly into ultra-broadband models. These applications require high reliability, signal transparency, and the ability to handle high-volume data environments, all attributes that are met with advanced photonics solutions. The biophotonics market is set to expand significantly through 2036, with photonics products poised for an expanding share as manufacturers seek to maximize diagnostic accuracy and minimize patient recovery time. Furthermore, the increasing demand for AI-driven optical computing and virtual reality tools is stimulating demand for modular photonics solutions that provide high-speed results and design flexibility.

Why Do Lasers Lead the Market?

The lasers segment accounts for a significant portion of the overall photonics market in 2026. This is mainly attributed to the versatile use of this technology in supporting high-precision cutting and complex surgical procedures within extremely diverse environments, such as in heavy industrial plants and specialized medical clinics. These systems offer the most comprehensive way to ensure material integrity across diverse high-frequency applications. The automotive and aerospace sectors alone consume a large share of laser production, with major projects in Asia Pacific and North America demonstrating the technology’s capability to handle high-density power requirements. However, the sensors and detectors segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust environmental sensing in autonomous systems, smart cities, and advanced security platforms.

How Does the Optical Communication Segment Dominate?

Based on application, the optical communication segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of global data traffic and the rigorous performance standards required for modern telecommunication networks. Current large-scale data centers are increasingly specifying high-density optical interconnects to ensure compliance with global data standards and consumer expectations for faster, low-latency connectivity.

The medical technology segment is expected to witness the fastest growth during the forecast period. The shift toward non-invasive diagnostics and the complexity of robotic surgery suites are pushing the requirement for advanced photonic systems that can handle varied biological tissues and mechanical stresses while ensuring absolute reliability for safety-critical medical systems.

Why Does Telecommunications Lead the Market?

The telecommunications segment commands the largest share of the global photonics market in 2026. This dominance stems from its superior data handling capacity, signal consistency, and excellent transmission properties, making it the technology of choice for high-performance network infrastructure. Large-scale operations in 5G/6G deployment, cloud computing, and global internet services drive demand, with advanced optical modules from suppliers like Broadcom and Cisco enabling reliable performance in extreme data environments.

However, the industrial segment is poised for steady growth through 2036, fueled by expanding applications in smart factories and precision manufacturing. Manufacturers face mounting pressure to optimize costs for high-volume, less demanding applications, where standardized photonic sensors provide a cost-effective alternative for basic industrial connectivity.

How is Asia Pacific Maintaining Dominance in the Global Photonics Market?

Asia Pacific holds the largest share of the global photonics market in 2026. The largest share of this region is primarily attributed to the massive industrialization and the presence of the world’s largest electronics manufacturing hubs, particularly in China, Japan, and Taiwan. China alone accounts for a significant portion of global photonics production, with its position as a leading exporter of consumer electronics driving sustained growth. The presence of leading manufacturers like Hamamatsu and a well-developed semiconductor supply chain provides a robust market for both standard and high-density photonic solutions.

Which Factors Support North America and Europe Market Growth?

North America and Europe together account for a substantial share of the global photonics market. The growth of these markets is mainly driven by the need for technological modernization in the aerospace, defense, and professional medical sectors. The demand for advanced photonics systems in North America is mainly due to its large-scale R&D projects and the presence of innovators like IPG Photonics and Coherent Corp.

In Europe, the leadership in optical engineering and the push for industrial automation innovation are driving the adoption of high-reliability photonics products. Countries like Germany, France, and the UK are at the forefront, with significant focus on integrating smart photonic solutions into daily industrial routines and advanced medical treatments to ensure the highest levels of performance and reliability.

The companies such as Hamamatsu Photonics K.K., IPG Photonics Corporation, Coherent Corp., and Lumentum Holdings Inc. lead the global photonics market with a comprehensive range of laser and sensor solutions, particularly for large-scale industrial and high-speed communication applications. Meanwhile, players including Broadcom Inc., Cisco Systems, Inc., ASML Holding N.V., and Trumpf Group focus on specialized semiconductor and high-density formulations targeting the manufacturing and telecommunications sectors. Emerging manufacturers and integrated players such as Effect Photonics, Infinera Corporation, and Thorlabs, Inc. are strengthening the market through innovations in integrated photonics and modular optical platforms.

The global photonics market is expected to grow from USD 1,112.80 billion in 2026 to USD 1,985.60 billion by 2036.

The global photonics market is projected to grow at a CAGR of 5.9% from 2026 to 2036.

Lasers are expected to dominate the market in 2026 due to their superior ability to support high-precision manufacturing and medical procedures. However, sensors and detectors are projected to be the fastest-growing segment owing to their increasing adoption in autonomous systems, IoT, and smart infrastructure where high-resolution sensing is required.

AI and Silicon Photonics are transforming the photonics landscape by demanding higher signal integrity, lower power consumption, and improved processing speed. These technologies drive the adoption of advanced materials like indium phosphide and silicon-on-insulator, enabling hardware manufacturers to support the complex architectures and high-frequency requirements of next-generation computing products.

Asia Pacific holds the largest share of the global photonics market in 2026. The largest share of this region is primarily attributed to the massive industrialization and the presence of the world’s largest electronics manufacturing hubs in China, Japan, and Taiwan. North America and Europe together account for a substantial share, driven by high-end applications in aerospace, defense, and medical technology.

The leading companies include Hamamatsu Photonics K.K., IPG Photonics Corporation, Coherent Corp., Lumentum Holdings Inc., and Broadcom Inc.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Industry Trends

3.4. Value Chain Analysis

3.5. Porter's Five Forces Analysis

3.6. PESTLE Analysis

4. Global Photonics Market, By Product Type

4.1. Introduction

4.2. Lasers

4.2.1. Gas Lasers

4.2.2. Solid-State Lasers

4.2.3. Fiber Lasers

4.2.4. Diode Lasers

4.2.5. Others

4.3. LEDs (Light Emitting Diodes)

4.3.1. High-Brightness LEDs

4.3.2. Organic LEDs (OLEDs)

4.3.3. Ultraviolet LEDs (UV-LEDs)

4.3.4. Others

4.4. Sensors & Detectors

4.4.1. Image Sensors (CMOS, CCD)

4.4.2. Photodetectors

4.4.3. Optical Sensors

4.4.4. Others

4.5. Optical Components & Systems

4.5.1. Optical Fibers & Waveguides

4.5.2. Lenses, Prisms & Mirrors

4.5.3. Modulators & Switches

4.5.4. Filters & Gratings

4.6. Others

5. Global Photonics Market, By Application

5.1. Introduction

5.2. Optical Communication

5.3. Displays

5.4. Lighting

5.5. Medical Technology (Biophotonics)

5.6. Manufacturing (Industrial Photonics)

5.7. Information Technology

5.8. Photovoltaic (Solar Energy)

5.9. Others

6. Global Photonics Market, By End-User Industry

6.1. Introduction

6.2. Telecommunications

6.3. Healthcare

6.4. Industrial (Automotive, Aerospace, Manufacturing)

6.5. Consumer Electronics

6.6. Aerospace & Defense

6.7. Automotive

6.8. Energy & Utilities

6.9. Others

7. Global Photonics Market, By Region

7.1. Introduction

7.2. North America

7.2.1. U.S.

7.2.2. Canada

7.2.3. Mexico

7.3. Europe

7.3.1. Germany

7.3.2. France

7.3.3. U.K.

7.3.4. Italy

7.3.5. Spain

7.3.6. Russia

7.3.7. Rest of Europe

7.4. Asia-Pacific

7.4.1. China

7.4.2. Japan

7.4.3. India

7.4.4. South Korea

7.4.5. Taiwan

7.4.6. Australia

7.4.7. Rest of Asia-Pacific

7.5. Latin America

7.5.1. Brazil

7.5.2. Argentina

7.5.3. Colombia

7.5.4. Chile

7.5.5. Peru

7.5.6. Rest of Latin America

7.6. Middle East & Africa

7.6.1. Saudi Arabia

7.6.2. U.A.E.

7.6.3. South Africa

7.6.4. Israel

7.6.5. Turkey

7.6.6. Egypt

7.6.7. Qatar

7.6.8. Rest of Middle East & Africa

8. Competitive Landscape

8.1. Market Share Analysis

8.2. Competitive Benchmarking

8.3. Key Strategies (Expansions, M&A, Product Launches)

8.4. Competitive Dashboard

8.4.1. Industry Leader

8.4.2. Market Differentiators

8.4.3. Vanguards

8.4.4. Emerging Companies

9. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments)

9.1. Hamamatsu Photonics K.K.

9.2. IPG Photonics Corporation

9.3. Coherent Corp.

9.4. Lumentum Holdings Inc.

9.5. Broadcom Inc.

9.6. Cisco Systems, Inc.

9.7. ASML Holding N.V.

9.8. Trumpf Group

9.9. Jenoptik AG

9.10. Newport Corporation (MKS Instruments)

9.11. Thorlabs, Inc.

9.12. Effect Photonics

9.13. Infinera Corporation

9.14. Excelitas Technologies Corp.

9.15. Schott AG

10. Appendix

10.1. Questionnaire

10.2. Available Customization

Published Date: Apr-2026

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Jun-2022

Published Date: Feb-2026

Subscribe to get the latest industry updates