Resources

About Us

Oilfield Services Market by Type (Pressure Pumping, Oil Country Tubular Goods, Well Intervention and Coiled Tubing, Drilling and Completion Fluid, Well Completion, Seismic Testing), Location (Onshore and Offshore), and Geography - Global Forecast to 2036

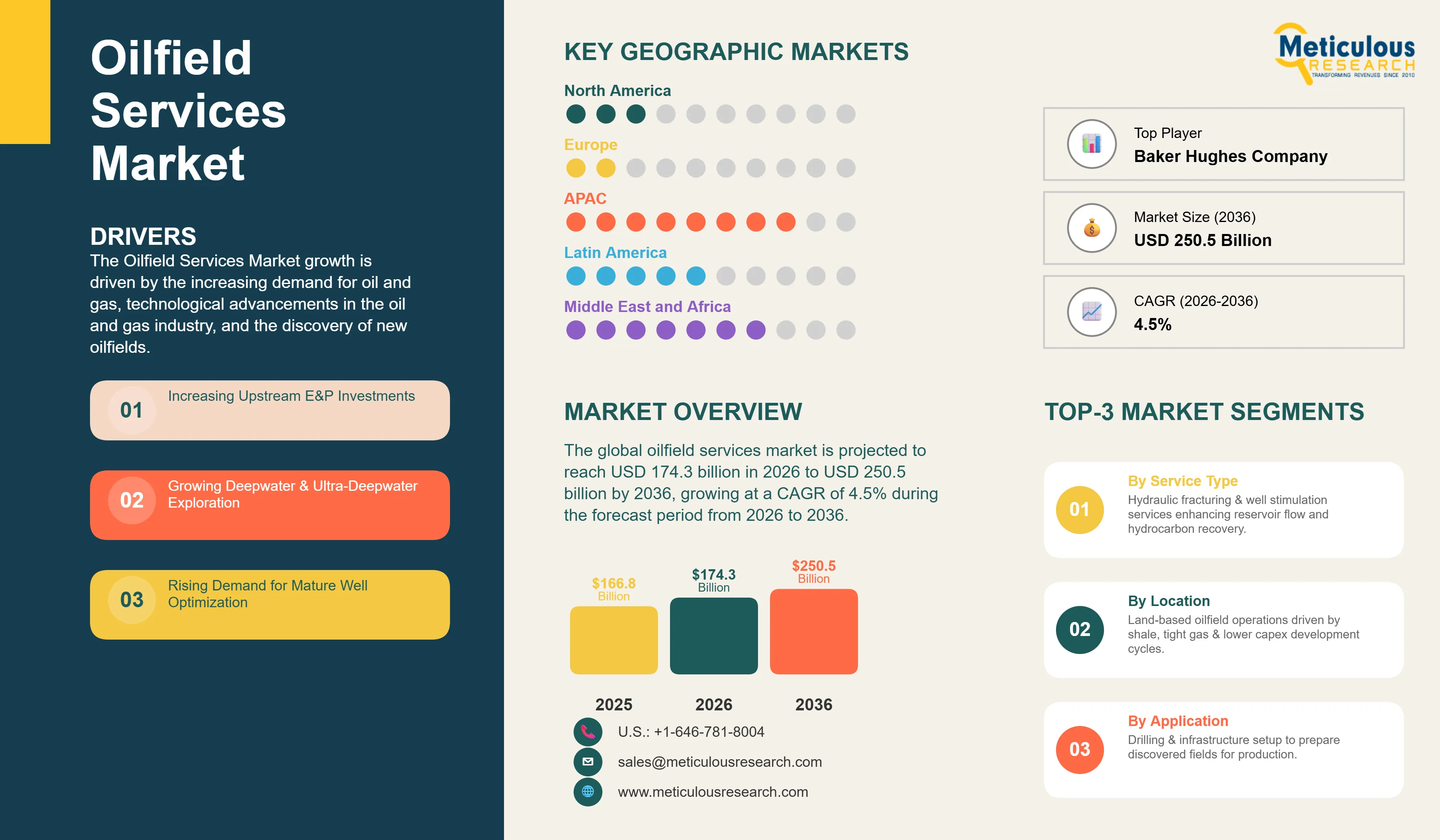

Report ID: MRSE - 104262 Pages: 230 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 48 Hours Download Free Sample ReportThe global oilfield services market is valued at USD 166.8 billion in 2025 and is projected to reach USD 174.3 billion in 2026. The market is further expected to reach USD 250.5 billion by 2036, growing at a CAGR of 4.5% during the forecast period from 2026 to 2036. The market growth is driven by the increasing demand for oil and gas, technological advancements in the oil and gas industry, and the discovery of new oilfields.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The oilfield services market includes a broad range of specialized services that support upstream oil & gas operations, including exploration, drilling, well completion, intervention, and production optimization. These services play a critical role in enhancing hydrocarbon recovery, improving operational efficiency, and extending the lifecycle of mature oilfields. The market is characterized by the presence of several global and regional service providers offering integrated and technologically advanced solutions across the upstream value chain. The growing global demand for energy, coupled with increasing investments in upstream exploration & production (E&P) activities and the development of unconventional and deepwater reserves, is expected to drive the growth of the oilfield services market over the forecast period.

Digitization to Achieve Cost Optimization

Oil & gas operators are increasingly leveraging digital oilfield technologies to enhance operational efficiency, reduce non-productive time (NPT), and optimize well lifecycle costs across upstream operations. The growing deployment of advanced data analytics, artificial intelligence (AI), cloud computing, and Industrial Internet of Things (IIoT) platforms is enabling real-time monitoring of drilling and production activities, predictive maintenance of critical equipment, and improved reservoir performance management.

According to industry bodies such as the Society of Petroleum Engineers (SPE), digital drilling and automated well placement technologies can reduce non-productive time by up to 20%–25%, while predictive maintenance solutions have demonstrated the potential to lower equipment-related downtime by nearly 30% across offshore assets. In addition, the adoption of real-time drilling optimization platforms, such as AI-enabled autonomous directional drilling systems deployed by leading service providers, has resulted in 10%–15% improvements in rate of penetration (ROP) and measurable reductions in well delivery time in unconventional and deepwater environments.

Furthermore, digital production optimization platforms, including remote well monitoring systems and automated artificial lift management solutions, are enabling operators to enhance recovery rates from mature fields while minimizing field intervention costs. These integrated digital oilfield deployments are supporting centralized decision-making through real-time data visualization and reservoir modeling, ultimately improving asset utilization and operational efficiency.

As a result, the increasing integration of automation and intelligent analytics across exploration & production (E&P) workflows is emerging as a key trend driving the demand for technologically advanced oilfield services globally.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 250.5 Billion |

|

Market Size in 2026 |

USD 166.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.5% |

|

Dominating Service Type |

Pressure Pumping |

|

Leading Location |

Onshore |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Drivers: Increasing Global Demand for Oil & Gas

The increasing global demand for crude oil and natural gas remains one of the primary factors driving investments in upstream exploration and production (E&P) activities, thereby supporting the growth of the oilfield services market. Rapid industrialization, urbanization, and rising energy consumption across emerging economies, particularly in Asia-Pacific and the Middle East, are contributing to the growing demand for hydrocarbons. In response, national and international oil companies are increasing capital expenditure toward the development of unconventional reserves, offshore fields, and mature asset optimization. This growing emphasis on maintaining production levels and improving recovery rates is expected to drive demand for drilling, completion, intervention, and production-related oilfield services over the forecast period.

Why is Pressure Pumping the Dominant Service Type in the Market?

Pressure pumping services account for the largest share of the global oilfield services market, primarily due to their critical role in hydraulic fracturing and well stimulation activities associated with unconventional resource development. The increasing deployment of horizontal drilling and multi-stage hydraulic fracturing techniques in shale formations, particularly across North America and parts of Asia-Pacific, is driving demand for high-pressure pumping solutions. These services are essential for enhancing reservoir permeability and maximizing hydrocarbon recovery from tight oil and gas formations. Moreover, advancements in electric fracturing fleets and automated pumping systems are enabling operators to improve pumping efficiency, reduce fuel consumption, and lower emissions, further contributing to the growing adoption of pressure pumping services across upstream operations.

Which Location Segment is Expected to Dominate the Oilfield Services Market?

The onshore segment is expected to account for the largest share of the global oilfield services market in 2026. This dominance is primarily attributed to the increasing development of unconventional hydrocarbon resources such as shale oil, tight gas, and coalbed methane, particularly across North America, China, and Argentina. Onshore oilfield operations typically involve lower capital investment and shorter project cycles compared to offshore developments, making them more economically viable for operators seeking to optimize production amid volatile crude oil prices. Additionally, the growing adoption of horizontal drilling and hydraulic fracturing techniques in land-based fields is driving demand for drilling, completion, pressure pumping, and well intervention services across onshore assets.

However, the offshore segment is projected to witness steady growth over the forecast period, driven by increasing investments in deepwater and ultra-deepwater exploration activities across regions such as the Middle East, West Africa, and Latin America. Offshore projects require advanced subsea production systems, well completion technologies, and remotely operated intervention solutions to address complex geological conditions and high-pressure environments. As a result, the development of offshore reserves is expected to drive demand for technologically advanced oilfield services, particularly in subsea installation, formation evaluation, and well stimulation applications.

Furthermore, the growing focus on maximizing output from mature offshore fields through enhanced oil recovery (EOR) techniques and digital production optimization platforms is expected to support long-term growth in offshore oilfield service demand.

The key players profiled in the global oilfield services market report include SLB (Schlumberger Limited), Baker Hughes Company, Halliburton Company, Weatherford International plc, China Oilfield Services Limited (COSL), National Oilwell Varco, Inc., TechnipFMC plc, Aker Solutions ASA, Saipem S.p.A., Superior Energy Services, Inc., Oil States International, Inc., Archer Limited, Nabors Industries Ltd., Patterson-UTI Energy, Inc., Helmerich & Payne, Inc., and Welltec A/S, among others.

The global oilfield services market is valued at USD 166.8 billion in 2026 and is expected to reach approximately USD 250.5 billion by 2036.

The market is expected to grow at a CAGR of 4.5% from 2026 to 2036.

SLB (Schlumberger Limited), Baker Hughes Company, Halliburton Company, Weatherford International plc, China Oilfield Services Limited (COSL), National Oilwell Varco, Inc., TechnipFMC plc, Aker Solutions ASA, Saipem S.p.A., Superior Energy Services, Inc., Oil States International, Inc., Archer Limited, Nabors Industries Ltd., Patterson-UTI Energy, Inc., Helmerich & Payne, Inc., and Welltec A/S, among others.

The main factors include the increasing demand for oil and gas and technological advancements in the oil and gas industry.

North America is expected to lead the market, driven by the presence of a large number of oil and gas reserves and the increasing use of hydraulic fracturing.

Published Date: Jan-2025

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates