Resources

About Us

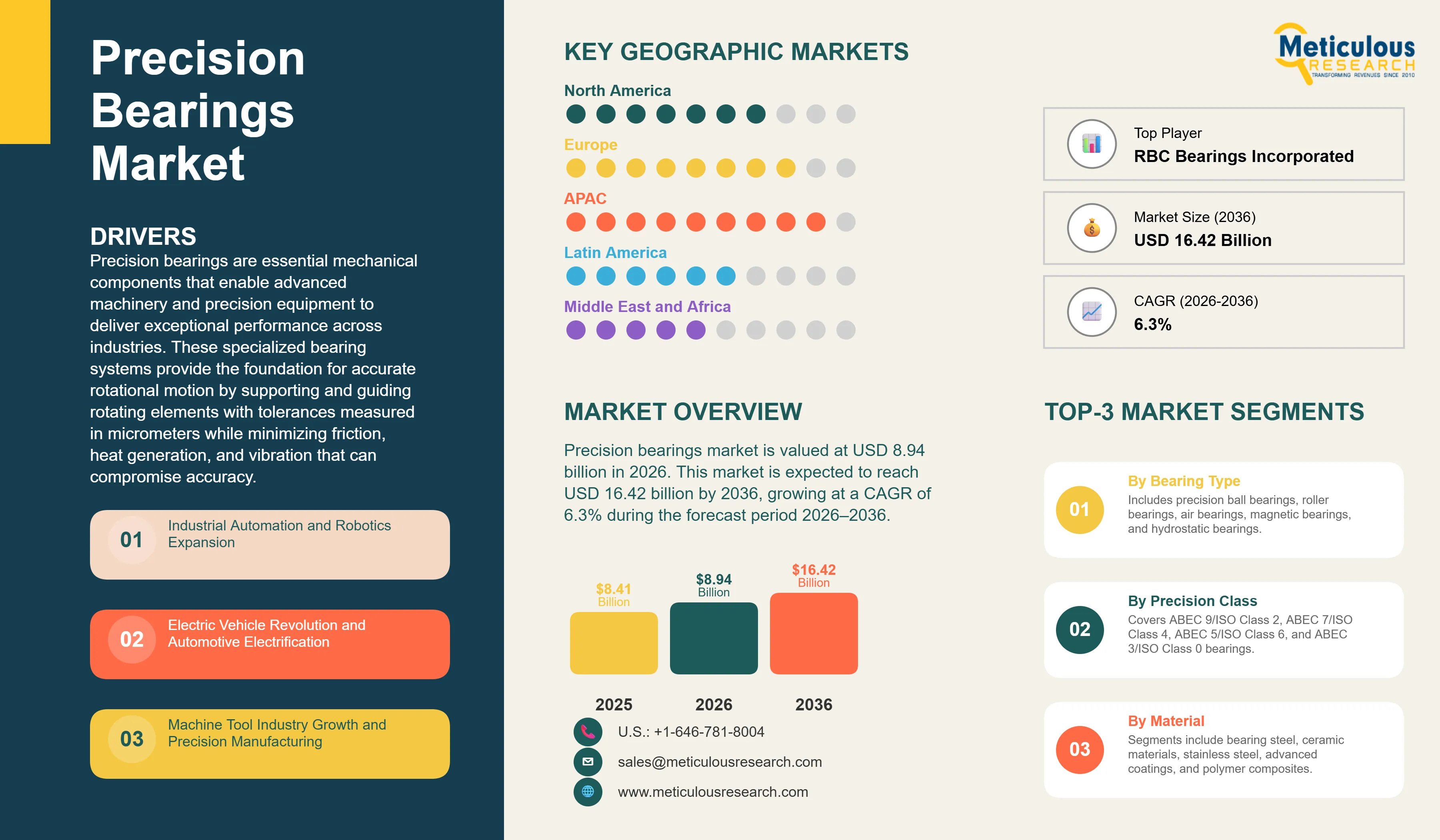

Precision Bearings Market Size, Share, & Forecast by Bearing Type (Ball, Roller, Air), Material, Precision Class (ABEC), and Application (Spindles, Robotics) – Global Forecast (2026-2036)

Report ID: MROTH - 1041679 Pages: 273 Jan-2026 Formats*: PDF Category: Others Delivery: 24 to 72 Hours Download Free Sample ReportThe global precision bearings market is valued at USD 8.94 billion in 2026. This market is expected to reach USD 16.42 billion by 2036, growing at a CAGR of 6.3% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Precision bearings are essential mechanical components that enable advanced machinery and precision equipment to deliver exceptional performance across industries. These specialized bearing systems provide the foundation for accurate rotational motion by supporting and guiding rotating elements with tolerances measured in micrometers while minimizing friction, heat generation, and vibration that can compromise accuracy. The challenge in precision machinery is maintaining highly accurate rotational performance under varying loads, speeds, and operating environments. Consequently, precision bearings are indispensable in applications ranging from submicron-accuracy machine tool spindles and nanometer-scale semiconductor manufacturing equipment to aerospace systems and industrial robots. According to the International Federation of Robotics (IFR), global industrial robot installations reached 553,000 units in 2022 and the active installed base exceeded 3.9 million units worldwide, creating substantial demand for high-precision bearings used in robotic joints, reducers, and motion-control systems. In addition, the Semiconductor Industry Association (SIA), citing World Semiconductor Trade Statistics (WSTS), reported that global semiconductor sales reached USD 627.6 billion in 2024, highlighting the expanding need for ultra-clean and vibration-free equipment used in wafer fabrication and inspection processes.

Several key trends are reshaping the precision bearings market. The industry is witnessing increasing adoption of hybrid and full ceramic bearing technologies, which provide superior speed capability, thermal stability, and corrosion resistance. Rising industrial automation and robotics are driving demand for smooth and highly precise motion-control systems, while expanding semiconductor manufacturing capacity is creating requirements for ultra-low vibration and contamination-free bearing solutions. The rapid electrification of the automotive sector is opening new opportunities for high-speed electric motors and transmission systems, and the emergence of smart bearings integrated with sensors is supporting condition monitoring and predictive maintenance. According to the International Federation of Robotics, annual robot installations are expected to exceed 700,000 units by 2027, reflecting accelerating automation across manufacturing industries. Meanwhile, smart bearing technologies are gaining momentum as manufacturers increasingly adopt Industry 4.0 practices to reduce downtime and improve operational efficiency. The convergence of stringent manufacturing requirements, rapid automation, advanced material technologies, and digitalization has transformed precision bearings from conventional mechanical components into strategic enablers of competitive advantage in precision manufacturing and high-technology applications.

The precision bearings market is changing. It is moving toward higher performance specifications, better materials, and intelligent bearing systems that can monitor conditions. Modern precision bearings are pushing the limits of traditional performance. Innovations such as ultra-high precision grades (ABEC 9 and ISO Class 2) allow for submicron runout in demanding applications. Improvements in bearing steel metallurgy are increasing fatigue life and thermal resistance. Hybrid designs that combine steel rings with ceramic rolling elements offer better speed capability and reduced friction. Surface technologies, like diamond-like carbon (DLC) coatings, help minimize wear and energy loss. Meanwhile, the integration of sensors for monitoring temperature, vibration, and load, along with wireless connectivity, is changing bearings from passive mechanical parts to smart assets that support predictive maintenance and better equipment performance. The rise of Industry 4.0 technologies is reinforcing this trend. According to the International Federation of Robotics (IFR), the global operational stock of industrial robots surpassed 4 million units in 2023. This highlights the growing need for smart and reliable motion-control components.

Ceramic bearing technology is advancing quickly and becoming more accepted in high-performance applications. Silicon nitride (Si3N4) rolling elements have several advantages over traditional bearing steel. They are much lighter, harder, more wear-resistant, have lower thermal expansion, provide electrical insulation, and resist corrosion. These features make hybrid and ceramic bearings ideal for electric vehicle traction motors, high-speed machine tool spindles, aerospace parts, and semiconductor manufacturing equipment, which all require clean and low-vibration operation. The rapid growth of electric mobility is boosting demand for these solutions. According to the International Energy Agency (IEA), global electric vehicle sales surpassed 17 million units in 2024, accounting for over 20% of total vehicle sales worldwide. At the same time, the Semiconductor Industry Association (SIA) reported, citing World Semiconductor Trade Statistics (WSTS), that global semiconductor sales reached around USD 628 billion in 2024. This growth drives investment in advanced wafer fabrication equipment where high-precision bearings are essential. Rising production volumes and better ceramic manufacturing processes are also helping close the cost gap for hybrid bearing designs.

Machine tool spindle applications continue to push innovation in precision bearings and remain a key segment. Modern CNC machining centers, grinding machines, and ultra-precision manufacturing equipment need spindle bearings that deliver submicron runout accuracy, high-speed operations that exceed 30,000 rpm in some cases, high stiffness to withstand cutting forces, thermal stability, and long service life to reduce downtime. Angular contact ball bearings are the top choice for machine tool spindles because they balance radial and axial load capacity, speed capability, and precision. Matched bearing sets arranged in tandem, back-to-back, or face-to-face configurations are often used to maximize rigidity and accuracy. Ongoing demand from aerospace, automotive, and medical device manufacturing supports this segment. According to the German Machine Tool Builders' Association (VDW), global machine tool production reached around EUR 97 billion in 2024, with China, Japan, and Germany as leading manufacturing countries. The ongoing shift toward high-speed machining, tighter tolerances, and automated production systems is likely to sustain demand for more sophisticated precision bearing technologies.

|

Parameter |

Details |

|

Market Size Value in 2026 |

USD 8.94 Billion |

|

Revenue Forecast in 2036 |

USD 16.42 Billion |

|

Growth Rate |

CAGR of 6.3% from 2026 to 2036 |

|

Base Year for Estimation |

2025 |

|

Historical Data |

2021–2025 |

|

Forecast Period |

2026–2036 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2036 |

|

Report Coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments Covered |

Bearing Type, Precision Class, Material, Application, Industry Vertical, Region |

|

Regional Scope |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Countries Covered |

U.S., Canada, Germany, U.K., France, Italy, Spain, Sweden, Japan, China, South Korea, Taiwan, India, Singapore, Brazil, Mexico, Saudi Arabia, UAE |

|

Key Companies Profiled |

NSK Ltd., SKF AB, Schaeffler Technologies AG & Co. KG, NTN Corporation, JTEKT Corporation, Timken Company, Minebea Mitsumi Inc., THK Co. Ltd., C&U Group, ZWZ Bearing Co. Ltd., LYC Bearing Corporation, GMN Paul Müller Industrie GmbH & Co. KG, Barden Precision Bearings (Schaeffler), RBC Bearings Incorporated, Kaydon Corporation (SKF), SNR Bearings (NTN), FAG (Schaeffler), IKO International Inc., Nachi-Fujikoshi Corp., Koyo Bearings (JTEKT) |

Driver: Industrial Automation and Robotics Expansion

The rapid growth of industrial automation and robotics is a key factor driving demand for precision bearings in manufacturing. According to the International Federation of Robotics (IFR), annual installations of industrial robots reached a record 553,000 units in 2022, and the global operational stock surpassed 4.2 million units in 2023. IFR forecasts suggest that yearly installations will keep increasing and could exceed 700,000 units by 2027. Industrial robots depend on precision bearings in joint mechanisms, speed reducers, wrists, linear axes, and end-effectors to provide accurate and repeatable motion. High-performance bearing types, like angular contact ball bearings and crossed roller bearings, are commonly used in harmonic drive and RV reducer systems to ensure stiffness, low friction, and minimal vibration. The large number of installed robots around the globe also creates ongoing demand for bearing replacement and maintenance throughout the equipment's lifecycle. The rising use of collaborative robots (cobots) is boosting demand for high-quality precision bearings. According to the International Federation of Robotics, cobots made up about 10.5% of all industrial robot installations in 2023, showing their increasing presence in electronics, automotive, logistics, and small-scale manufacturing. Because cobots are built to work safely alongside humans, they need smooth and highly precise motion, which places a greater focus on bearings that offer low friction, reduced vibration, and long-term reliability. Beyond robotics, the wider automation trend includes CNC machine tools, automated assembly systems, packaging machinery, semiconductor manufacturing equipment, and medical device production systems. All these rely on precision bearings for accurate motion control. The International Labour Organization (ILO) notes that many developed economies face aging workforces and labor shortages. This situation is accelerating investments in automation technologies. At the same time, manufacturers want greater productivity, improved quality, and safer operations in dangerous environments. These factors are driving ongoing investment in automation equipment, which is increasing the demand for precision bearing solutions.

Opportunity: Semiconductor Manufacturing Equipment Expansion

The rapid growth of semiconductor manufacturing capacity around the world offers a major chance for suppliers of ultra-precision bearings used in fabrication equipment. Semiconductor production tools, including lithography systems, wafer inspection equipment, deposition systems, and wafer-handling robotics, need bearings that provide extremely high positioning accuracy, clean operation, low vibration, and outstanding reliability. These factors help maintain high manufacturing yields and uptime. Precision bearings are crucial in these systems because even slight motion deviations can impact process accuracy and device performance.

The global semiconductor industry is experiencing an exceptional wave of investment fueled by rising demand for AI accelerators, high-performance computing, automotive electronics, and 5G infrastructure. Government efforts also aim to boost domestic chip production. In the United States, the CHIPS and Science Act offers about $52.7 billion in manufacturing incentives and research funding. Similar programs have started in the European Union, Japan, South Korea, Taiwan, and China to increase semiconductor capacity. According to SEMI, over 100 new semiconductor fabrication plants are expected to open worldwide between 2024 and 2030. Additionally, total fab investments are likely to surpass $1 trillion during this time. The Semiconductor Industry Association (SIA), referencing World Semiconductor Trade Statistics (WSTS), stated that global semiconductor sales reached around $628 billion in 2024 and are expected to keep rising, leading to more spending on equipment.

The shift towards more advanced process technologies, such as 5 nm, 3 nm, and upcoming 2 nm nodes, is increasing the requirements for lithography, metrology, and wafer-handling equipment. In these areas, motion accuracy and vibration control are critical. Suppliers that can deliver ultra-clean precision bearings with low particle generation, minimal outgassing, and proven reliability in semiconductor environments are well placed to seize premium opportunities in this valuable market. As semiconductor manufacturers keep investing in next-generation fabs and process technologies, the demand for specialized precision bearing solutions is expected to grow throughout the forecast period.

By Bearing Type

Precision ball bearings are expected to account for the largest share of the global precision bearings market in 2026. Their high-speed capability, low friction, and ability to support both radial and axial loads make them suitable for machine tools, robotics, aerospace systems, and precision machinery. Among them, angular contact ball bearings represent the largest sub-segment owing to their widespread use in machine tool spindles and robotic reducers. Meanwhile, hybrid bearings, which combine steel rings with silicon nitride ceramic balls, are the fastest-growing category due to their superior speed capability, electrical insulation, and extended service life, particularly in electric vehicle motors and aerospace applications.

By Precision Class (ABEC/ISO)

The ABEC 7 (ISO Class 4) segment is expected to dominate the market in 2026 because it offers an optimal balance between performance and cost. These bearings are widely used in industrial robots, machine tools, precision gearboxes, and aerospace equipment. While ABEC 9 bearings are preferred for ultra-precision applications, ABEC 7 grades satisfy the requirements of most high-precision industrial systems.

By Material

Bearing steel (AISI 52100/100Cr6) is expected to maintain the largest market share owing to its excellent fatigue resistance, hardness, and cost-effectiveness. Continuous advances in metallurgy and heat treatment have further improved performance and durability. However, ceramic bearings, particularly hybrid designs using silicon nitride rolling elements, are projected to witness the fastest growth. Their low density, electrical insulation, corrosion resistance, and high-speed capability make them increasingly attractive for electric vehicles, semiconductor equipment, aerospace systems, and high-speed machine tools.

By Application

Machine tool spindles are expected to remain the leading application segment in 2026, supported by ongoing demand for high-speed and high-precision machining in automotive, aerospace, and medical device manufacturing. Angular contact ball bearings are widely used in CNC machining centers, grinding machines, and milling equipment because of their high stiffness and accuracy. The electric vehicle motors and drivetrains segment is anticipated to register the fastest growth. According to the International Energy Agency (IEA), global electric vehicle sales exceeded 17 million units in 2024, increasing demand for high-speed, electrically insulated, and low-friction bearing solutions used in traction motors and e-axles.

Regional Insights

Asia-Pacific is expected to hold the largest share of the global precision bearings market in 2026, supported by its strong presence in machine tools, industrial robotics, semiconductor manufacturing, and automotive production. China, Japan, and South Korea are major manufacturing hubs, while leading bearing producers such as NSK, NTN, JTEKT, Nachi-Fujikoshi, and MinebeaMitsui are headquartered in the region. According to the International Federation of Robotics (IFR), China possesses the world's largest installed base of industrial robots, while the region also accounts for a significant portion of global semiconductor fabrication capacity and EV production.

Europe is projected to grow at a healthy pace due to its advanced manufacturing base, strong automotive and aerospace industries, and emphasis on Industry 4.0 technologies. Germany remains the region's largest market, supported by its machine tool sector and the presence of major bearing manufacturers such as Schaeffler and SKF. North America represents an important market driven by aerospace and defense, medical devices, semiconductor manufacturing, and reshoring initiatives. Investments stimulated by the U.S. CHIPS and Science Act and expansion plans by Intel, TSMC, Samsung, and Micron are expected to strengthen demand for high-performance precision bearings in semiconductor equipment and advanced manufacturing applications.

The major players in the precision bearings market include NSK Ltd. (Japan), SKF AB (Sweden), Schaeffler Technologies AG & Co. KG (Germany), NTN Corporation (Japan), JTEKT Corporation (Japan), Timken Company (U.S.), Minebea Mitsumi Inc. (Japan), THK Co. Ltd. (Japan), C&U Group (China), ZWZ Bearing Co. Ltd. (China), LYC Bearing Corporation (China), GMN Paul Müller Industrie GmbH & Co. KG (Germany), Barden Precision Bearings (Schaeffler) (U.S./Germany), RBC Bearings Incorporated (U.S.), Kaydon Corporation (SKF) (U.S.), SNR Bearings (NTN) (France), FAG (Schaeffler) (Germany), IKO International Inc. (Japan), Nachi-Fujikoshi Corp. (Japan), and Koyo Bearings (JTEKT) (Japan), among others.

The precision bearings market is expected to grow from USD 8.94 billion in 2026 to USD 16.42 billion by 2036.

The precision bearings market is expected to grow at a CAGR of 6.3% from 2026 to 2036.

The major players in the precision bearings market include NSK Ltd., SKF AB, Schaeffler Technologies AG & Co. KG, NTN Corporation, JTEKT Corporation, Timken Company, Minebea Mitsumi Inc., THK Co. Ltd., C&U Group, ZWZ Bearing Co. Ltd., LYC Bearing Corporation, GMN Paul Müller Industrie GmbH & Co. KG, Barden Precision Bearings (Schaeffler), RBC Bearings Incorporated, Kaydon Corporation (SKF), SNR Bearings (NTN), FAG (Schaeffler), IKO International Inc., Nachi-Fujikoshi Corp., and Koyo Bearings (JTEKT), among others.

The key factors driving the precision bearings market include the rapid expansion of industrial automation and robotics, with annual robot installations exceeding 550,000 units worldwide according to the International Federation of Robotics (IFR). Growing adoption of electric vehicles is increasing demand for high-speed and electrically insulated bearings used in traction motors and e-axles, while rising precision requirements in machine tools and advanced manufacturing are supporting demand for high-performance bearing solutions. Additional growth is being fueled by expanding semiconductor fabrication capacity, increasing aerospace and defense applications, advances in ceramic and hybrid bearing technologies, and the integration of smart sensors that enable condition monitoring and predictive maintenance.

Asia-Pacific region will lead the global precision bearings market in 2026 due to massive machine tool production, industrial robot deployment, and semiconductor manufacturing concentration, and is expected to maintain the largest market share during the forecast period 2026 to 2036.

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Apr-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates