Resources

About Us

Molecular Beam Epitaxy System Market by Product (Normal MBE, Laser MBE), End User Industry (Electronics, Aeronautics, Energy and Power), Epitaxy Types (Homoepitaxy, Heteroepitaxy), and Applications (Electronic, Optics) - Global Forecast to 2036

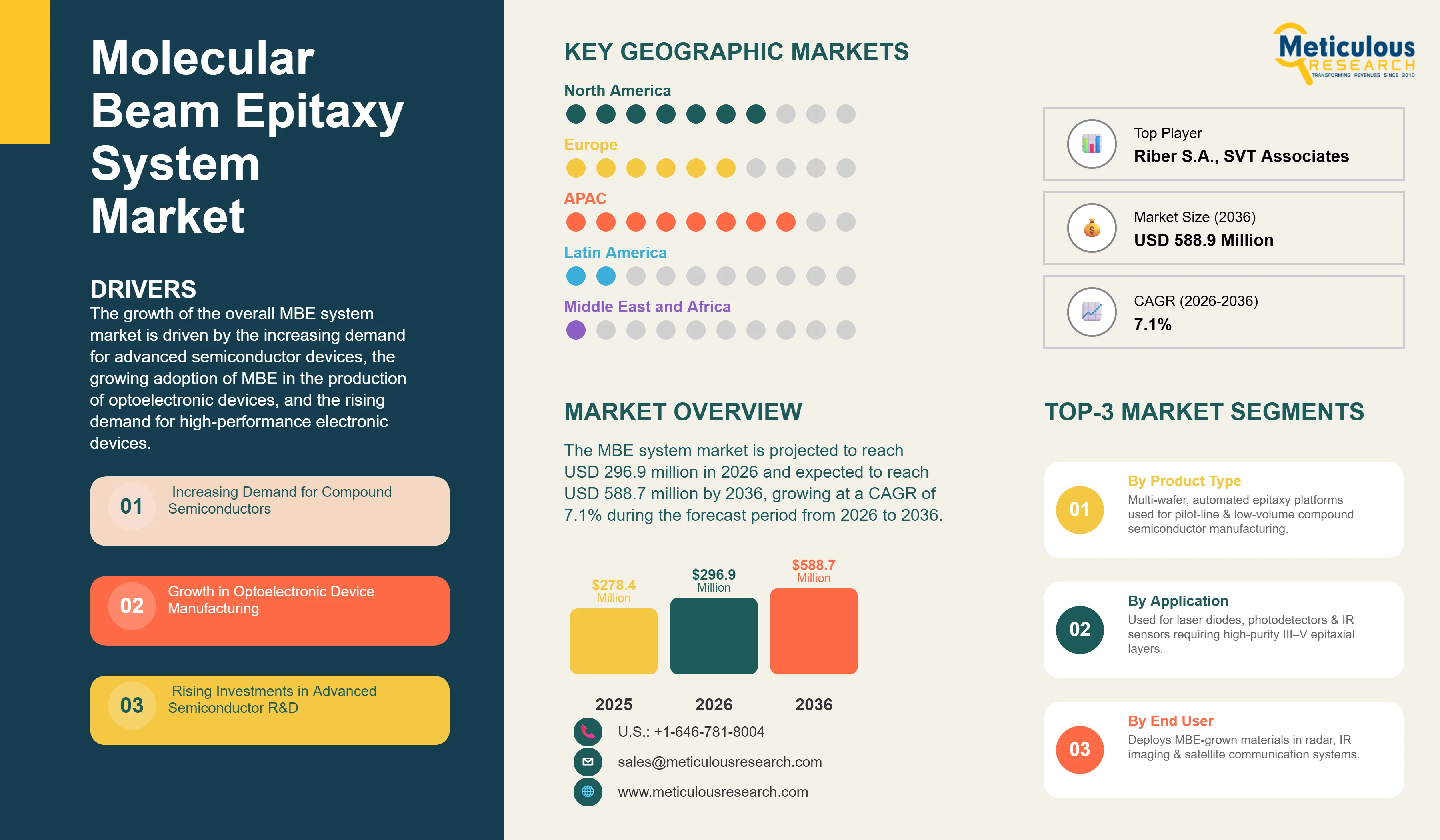

Report ID: MRHC - 104296 Pages: 150 Feb-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 48 Hours Download Free Sample ReportThe global molecular beam epitaxy (MBE) system market is valued at USD 278.4 million in 2025 and is projected to reach USD 296.9 million in 2026. The market is further expected to reach USD 588.7 million by 2036, growing at a CAGR of 7.1% during the forecast period from 2026 to 2036. The growth of the overall MBE system market is driven by the increasing demand for advanced semiconductor devices, the growing adoption of MBE in the production of optoelectronic devices, and the rising demand for high-performance electronic devices.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Molecular Beam Epitaxy (MBE) is a precision thin-film deposition technology used for the growth of ultra-high purity crystalline layers under ultra-high vacuum (UHV) conditions. The technique enables atomic-level control over material composition and thickness, making it critical for the fabrication of advanced compound semiconductor devices such as high-electron-mobility transistors (HEMTs), laser diodes, infrared detectors, and quantum well structures. MBE systems are widely utilized in the development of III–V semiconductor materials including gallium arsenide (GaAs), indium phosphide (InP), and gallium nitride (GaN), which are essential for high-frequency, high-power, and optoelectronic device applications.

The growing demand for advanced semiconductor components in telecommunications, aerospace & defense, and photonics is supporting increased investments in compound semiconductor fabrication technologies. For instance, according to the Semiconductor Industry Association (SIA), global semiconductor sales grew by over 19% in 2024, driven largely by demand for high-performance computing and wireless communication infrastructure. In addition, government-backed initiatives such as the U.S. CHIPS and Science Act and the European Union’s European Chips Act are encouraging investments in next-generation semiconductor R&D facilities, many of which incorporate MBE platforms for material innovation and device prototyping.

Growing Demand for III–V Compound Semiconductors

The increasing demand for III–V compound semiconductors such as GaAs and InP is emerging as a key trend driving the adoption of MBE systems globally. These materials offer superior electron mobility, direct bandgap properties, and higher thermal stability compared to conventional silicon-based semiconductors, making them well-suited for radio-frequency (RF), optoelectronic, and high-speed communication applications.

The rapid deployment of 5G infrastructure is significantly contributing to the demand for GaAs- and InP-based RF front-end components used in base stations and mobile devices. According to the Global Mobile Suppliers Association (GSA), more than 300 commercial 5G networks had been launched worldwide by the end of 2024, accelerating the production of RF filters, amplifiers, and photonic integrated circuits that rely on III–V epitaxial layers grown using MBE technology.

Furthermore, the growing adoption of photonic devices in data centers and optical communication networks is driving investments in InP-based laser and detector manufacturing. In 2023, several leading compound semiconductor foundries announced capacity expansions for III–V wafer fabrication to support next-generation optical transceivers for hyperscale data infrastructure. As MBE remains a preferred method for research-scale and pilot-line production of high-performance III–V materials, these developments are expected to support steady demand for advanced epitaxy systems over the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 588.7 Million |

|

Market Size in 2026 |

USD 296.9 Million |

|

Revenue Growth Rate (2026-2036) |

CAGR of 7.1% |

|

Dominating Product |

Production MBE Systems |

|

Leading End User |

Electronics Industry |

|

Leading Geographic Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Drivers: Increasing Demand for Advanced Semiconductor Devices

The increasing demand for advanced compound semiconductor devices such as high-electron-mobility transistors (HEMTs), heterojunction bipolar transistors (HBTs), quantum cascade lasers (QCLs), and infrared photodetectors is a key factor driving the adoption of molecular beam epitaxy (MBE) systems. These devices are extensively utilized in high-frequency and high-power applications across wireless communication infrastructure, satellite systems, defense radar platforms, and optical sensing technologies.

For instance, GaAs- and InP-based RF components grown using epitaxial deposition technologies are widely used in 5G base stations and mobile communication modules to support high-frequency signal transmission. Additionally, MBE-grown III–V semiconductor layers are increasingly being used in advanced photonic integrated circuits (PICs) and infrared imaging systems deployed in aerospace & defense applications. As the demand for high-speed communication and precision sensing technologies continues to grow, semiconductor manufacturers and research institutions are increasing investments in epitaxial growth platforms to support next-generation device development, thereby driving demand for MBE systems.

Opportunity: Expansion of GaN-Based Power Electronics

The growing development of gallium nitride (GaN)-based power electronic devices presents significant growth opportunities for MBE system manufacturers. GaN materials are increasingly being adopted in electric vehicles (EVs), renewable energy converters, and high-efficiency power management systems due to their superior thermal conductivity, breakdown voltage, and switching efficiency compared to silicon-based semiconductors.

MBE technology enables precise heterostructure formation for GaN-on-Si and GaN-on-SiC substrates used in power amplifiers and high-voltage switching devices. In recent years, several semiconductor research consortia and government-funded laboratories have initiated pilot-scale production of GaN-based HEMTs for electric mobility and aerospace applications. These developments are expected to create new demand for advanced epitaxy platforms capable of producing defect-controlled compound semiconductor layers.

Why are Production MBE Systems the Dominant Product in the Market?

Production MBE systems accounts for the largest share of the overall MBE system market in 2026, due to their increasing deployment in pilot-line and low-to-medium volume manufacturing environments for compound semiconductor devices. Unlike research-grade platforms, production MBE systems are equipped with multi-wafer handling capabilities, automated growth control, and in-situ monitoring technologies that enable improved process repeatability and material uniformity.

These systems are primarily used in the fabrication of optoelectronic components such as laser diodes, photodetectors, and RF amplifiers that require high-purity epitaxial layers with precise compositional control. With growing demand for photonic devices in data communication, sensing, and defense electronics, semiconductor manufacturers are increasingly adopting production-scale MBE platforms to support industrial-grade epitaxial growth processes.

Which End User Segment is Expected to Dominate the Market?

The electronics & semiconductor industry is expected to account for the largest share of the global MBE system market in 2026. This is primarily attributed to the increasing utilization of epitaxially grown III–V semiconductor materials in the development of RF communication devices, optoelectronic components, and advanced logic systems.

In addition, research institutes and universities represent a significant end-user segment due to ongoing material science research related to quantum computing, spintronics, and nanophotonic devices. Government-funded semiconductor R&D initiatives across North America, Europe, and Asia-Pacific are supporting the deployment of compact and cluster-based MBE systems for material innovation and device prototyping.

Which Region is Expected to Dominate the Global Molecular Beam Epitaxy System Market?

Asia-Pacific is expected to account for the largest share of the global molecular beam epitaxy system market during the forecast period. This dominance is primarily attributed to the strong presence of semiconductor manufacturing hubs in countries such as China, Japan, South Korea, and Taiwan, along with increasing investments in compound semiconductor fabrication for telecommunications and consumer electronics applications.

Furthermore, government-led semiconductor development programs across the region are supporting the establishment of advanced research facilities equipped with epitaxial growth platforms. For instance, national initiatives aimed at strengthening domestic semiconductor supply chains in China and South Korea are encouraging investments in next-generation material processing technologies, including MBE systems, for RF and photonic device applications.

North America and Europe are also expected to witness steady growth, driven by increased funding for aerospace & defense electronics and quantum computing research, where precision epitaxial growth is critical for device performance.

The key players profiled in the global molecular beam epitaxy system market report include Veeco Instruments Inc., Riber S.A., DCA Instruments Oy, SVT Associates, Inc., Dr. Eberl MBE-Komponenten GmbH, SKY Technology Development Co., Ltd., Scienta Omicron GmbH, SemiTEq JSC, Pascal Co., Ltd., and EIKO Engineering Co., Ltd., among others.

The global molecular beam epitaxy system market is valued at USD 296.9 million in 2026 and is expected to reach approximately USD 588.7 million by 2036.

The market is expected to grow at a CAGR of 7.1% from 2026 to 2036.

The key players include Veeco Instruments, Inc., Riber, and Omicron Electronics GmbH.

The main factors include the increasing demand for advanced semiconductor devices and the growing adoption of MBE in the production of optoelectronic devices.

North America is expected to lead the market, driven by the presence of a large number of semiconductor companies and a strong focus on research and development.

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates