Resources

About Us

Intravascular Imaging Market Size, Share & Trends Analysis by Technology (IVUS, OCT, NIRS, Multi-modality), Product (Catheters, Consoles, Software), Application, End User, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

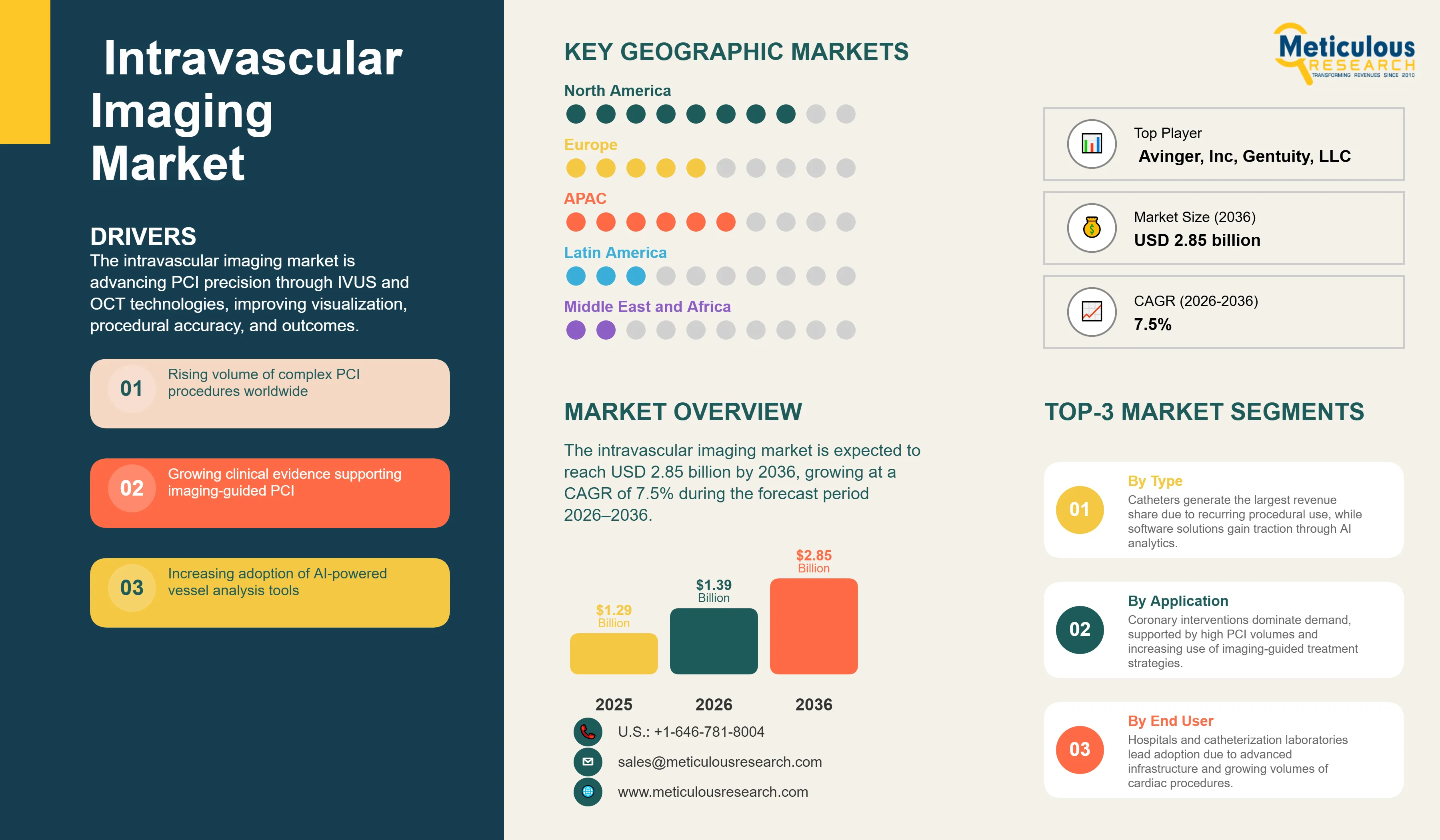

Report ID: MRHC - 1042016 Pages: 280 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global intravascular imaging market was valued at USD 1.39 billion in 2026. This market is expected to reach USD 2.85 billion by 2036, growing at a CAGR of 7.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global intravascular imaging market is witnessing a paradigm shift in interventional cardiology, moving from angiography-guided procedures to precision percutaneous coronary intervention (PCI). Coronary artery disease (CAD) remains the leading cause of mortality worldwide, affecting more than 240 million people globally and accounting for approximately 9 million deaths annually, according to estimates from the Global Burden of Disease (GBD) study and the World Health Organization. Intravascular imaging technologies, including Intravascular Ultrasound (IVUS) and Optical Coherence Tomography (OCT), provide clinicians with high-resolution, cross-sectional visualization of the vessel wall and lumen that cannot be achieved through conventional 2D angiography. This enhanced visualization is particularly valuable given that more than 15 million PCI procedures are performed globally each year, creating a significant need for technologies that improve procedural accuracy and outcomes.

The clinical adoption of intravascular imaging is fundamentally supported by a growing body of evidence demonstrating improved patient outcomes. Recent landmark trials, such as ILUMIEN IV and RENOVATE-COMPLEX-PCI, have shown that imaging-guided PCI is associated with a 38% reduction in target vessel failure compared to angiography-guided procedures. These findings have led to stronger recommendations in clinical guidelines from the American Heart Association (AHA) and the European Society of Cardiology (ESC). Consequently, the market is experiencing robust demand for both established IVUS systems and newer, ultra-high-resolution OCT platforms. The integration of Artificial Intelligence (AI) and automated vessel analysis tools is further accelerating adoption by reducing procedural time and minimizing the inter-observer variability in image interpretation.

The technological ecosystem is characterized by a high degree of innovation, with major manufacturers focusing on multi-modality integration and simplified workflows. Modern imaging consoles are increasingly capable of supporting both IVUS and OCT catheters, providing interventionalists with the flexibility to choose the best modality for each specific case. Furthermore, the development of combined IVUS-NIRS (Near-Infrared Spectroscopy) catheters allows for the simultaneous assessment of vessel structure and lipid-rich plaque composition, offering a comprehensive diagnostic tool for high-risk patients. The market for disposable imaging catheters remains the primary revenue driver, supported by the rising volume of PCI procedures globally.

Geographically, the market exhibits significant variation in adoption rates. North America remains the largest market by value, driven by high healthcare spending and a robust infrastructure for complex cardiac care. However, Japan stands as the global leader in per-capita adoption, with over 80% of PCIs being imaging-guided due to early clinical integration and favorable reimbursement policies. The Asia-Pacific region, led by China and India, is projected to be the fastest-growing market, fueled by the rapid expansion of cardiac catheterization labs and an increasing burden of cardiovascular diseases. As healthcare systems worldwide move toward value-based care, the role of intravascular imaging in ensuring procedural success and reducing long-term complications is expected to become even more prominent.

The primary driver for the intravascular imaging market is the growing volume of complex percutaneous coronary interventions (PCI). According to the World Health Organization, cardiovascular diseases account for approximately 17.9 million deaths annually worldwide, while coronary artery disease remains the leading cause of cardiovascular mortality. Additionally, the global population aged 65 years and older is projected to increase from approximately 857 million in 2021 to nearly 1.6 billion by 2050, according to the United Nations, contributing to a higher prevalence of multi-vessel disease, severe calcification, and chronic total occlusions that require precise intravascular imaging guidance. Furthermore, strong clinical evidence from major randomized controlled trials has established imaging-guided PCI as a superior strategy for reducing Major Adverse Cardiovascular Events (MACE), driving broader physician adoption. The integration of AI-powered automated lumen and stent analysis is also accelerating market growth by simplifying image interpretation and improving procedural efficiency, with studies demonstrating procedure time reductions of up to 20–25% in selected imaging workflows.

The high cost of imaging catheters and the specialized hardware required for intravascular imaging act as significant restraints, particularly in cost-sensitive healthcare systems. The additional cost of a single-use imaging catheter can range from $600 to $1,000, which may not be fully reimbursed in all regions. Furthermore, the technical learning curve associated with interpreting OCT and IVUS images requires specialized training for interventionalists and catheterization lab staff. In high-volume centers, the perceived impact on procedural efficiency and 'door-to-balloon' time can also slow the adoption of routine imaging.

Significant opportunities exist in the expansion of intravascular imaging into peripheral vascular interventions. The rising prevalence of Peripheral Artery Disease (PAD) and the need for precision treatment in complex iliofemoral and popliteal lesions present a high-growth market for dedicated peripheral imaging catheters. Additionally, the development of cloud-based tele-proctoring and remote assistance tools allows for specialist support in lower-volume centers, expanding the reach of high-tech cardiac care. The potential for 'fusion imaging'—combining intravascular data with 3D angiographic reconstruction—offers another avenue for technological differentiation.

A critical challenge is the significant disparity in reimbursement policies for intravascular imaging across different geographic regions. While some countries provide dedicated codes for imaging, others bundle it into the overall PCI payment, creating a financial disincentive for adoption. Managing the cybersecurity and data privacy of connected imaging consoles in a hospital network is also an evolving challenge for manufacturers. Furthermore, the ongoing competition between IVUS and OCT modalities requires companies to continuously innovate and demonstrate the unique clinical value of their specific technology for different patient populations.

The most prominent trend in the market is the integration of Artificial Intelligence (AI) into intravascular imaging platforms. AI algorithms are now capable of performing automated lumen detection, stent apposition assessment, and calcification quantification in real-time. This trend is significantly reducing the 'interpretation gap' and making high-resolution imaging more accessible to a broader range of interventionalists, ultimately leading to more standardized and optimized procedural outcomes.

There is a growing trend toward the development of hybrid imaging systems that combine the strengths of different technologies. For example, combined IVUS-OCT or IVUS-NIRS systems allow for the simultaneous assessment of vessel structure and plaque composition. Major players are focusing on creating universal, software-defined consoles that can support multiple catheter types and receive regular updates, providing hospitals with a more sustainable and versatile investment in intravascular imaging technology.

Based on technology, the market is segmented into Intravascular Ultrasound (IVUS), Optical Coherence Tomography (OCT), Near-Infrared Spectroscopy (NIRS), and Multi-modality Imaging. In 2026, the IVUS segment is expected to hold the largest share of the market. This dominance is due to its long-standing clinical history, versatility in treating both coronary and peripheral diseases, and the ability to image through blood without the need for saline flushing. IVUS remains the gold standard for assessing vessel size and plaque burden in daily interventional practice.

The Optical Coherence Tomography (OCT) segment is projected to register the fastest CAGR during the forecast period. OCT's ultra-high resolution (10-20 microns) provides unparalleled detail of the vessel surface, making it superior for assessing stent apposition and identifying thrombus or dissection. The rapid integration of AI-guided automated analysis is further driving the adoption of OCT in complex PCI cases.

Based on application, the market is segmented into Coronary Interventions and Peripheral Interventions. In 2026, the Coronary Interventions segment is expected to hold the largest share of the market. The vast majority of intravascular imaging is performed during PCI for coronary artery disease, where precision is critical for ensuring long-term stent patency. The high volume of coronary procedures globally ensures this segment remains the primary revenue driver.

The Peripheral Interventions segment is projected to witness the fastest growth during the forecast period. The increasing focus on treating Peripheral Artery Disease (PAD) and the development of specialized peripheral imaging catheters are driving adoption in this segment. Precision treatment of complex iliofemoral and popliteal lesions is becoming a priority for vascular surgeons and interventionalists.

North America is expected to hold the largest share of the global intravascular imaging market in 2026, driven by high adoption of advanced PCI technologies and a robust reimbursement framework in the United States. More than 40% of the global market share is concentrated in this region, supported by a high volume of complex cardiac procedures and the presence of leading medical device manufacturers. The key companies operating in the North American market are Abbott Laboratories, Boston Scientific, and Philips Healthcare.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Japan is already a global leader in imaging-guided PCI, with over 80% adoption. Meanwhile, China and India are experiencing rapid expansion in healthcare infrastructure and an increasing burden of cardiovascular diseases, leading to a rising volume of catheterization labs. The key companies operating in the Asia-Pacific market are Terumo Corporation, Abbott, and various emerging domestic manufacturers in China.

The global intravascular imaging market is highly consolidated, with a few major players dominating the landscape through extensive R&D and strategic acquisitions. Abbott Laboratories, Boston Scientific, and Philips Healthcare are the clear market leaders, accounting for the vast majority of global sales. Competition is centered on technological differentiation, particularly in the areas of AI-guided analysis, image resolution, and procedural workflow integration. The ability to offer a comprehensive portfolio of both catheters and consoles is a key competitive advantage.

Strategic partnerships with AI software developers and academic research institutes are common as companies seek to integrate advanced analytics into their platforms. Clinical trial results continue to play a critical role in market positioning, with manufacturers investing heavily in large-scale studies to demonstrate the long-term clinical benefits of their specific imaging modality. Key players in the global intravascular imaging market include Abbott Laboratories, Boston Scientific Corporation, Royal Philips (Philips Healthcare), Terumo Corporation, Infraredx, Inc. (Nipro Corporation), and ACIST Medical Systems (Bracco Group).

The market is projected to reach USD 2,854.6 million by 2036, growing at a CAGR of 7.5% from 2026 to 2036.

Intravascular Ultrasound (IVUS) is expected to hold the largest share in 2026 due to its versatility and history.

The growing volume of complex PCIs and strong clinical evidence supporting improved patient outcomes are the primary drivers.

The Peripheral Interventions segment is expected to grow the fastest due to the rising focus on PAD treatment.

AI simplifies image interpretation, reduces procedural time by up to 25%, and improves diagnostic accuracy.

Japan has the highest adoption rate globally, with over 80% of PCIs being imaging-guided.

It is associated with a 38% reduction in target vessel failure and significantly lower MACE rates compared to angiography.

OCT offers much higher resolution (10-20 microns) compared to IVUS (100-150 microns), allowing for better surface detail.

High procedural costs, reimbursement disparities, and the technical learning curve for image interpretation are the main restraints.

The market is led by Abbott Laboratories, Boston Scientific, Philips Healthcare, and Terumo Corporation.

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: May-2024

Published Date: Mar-2019

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates