Resources

About Us

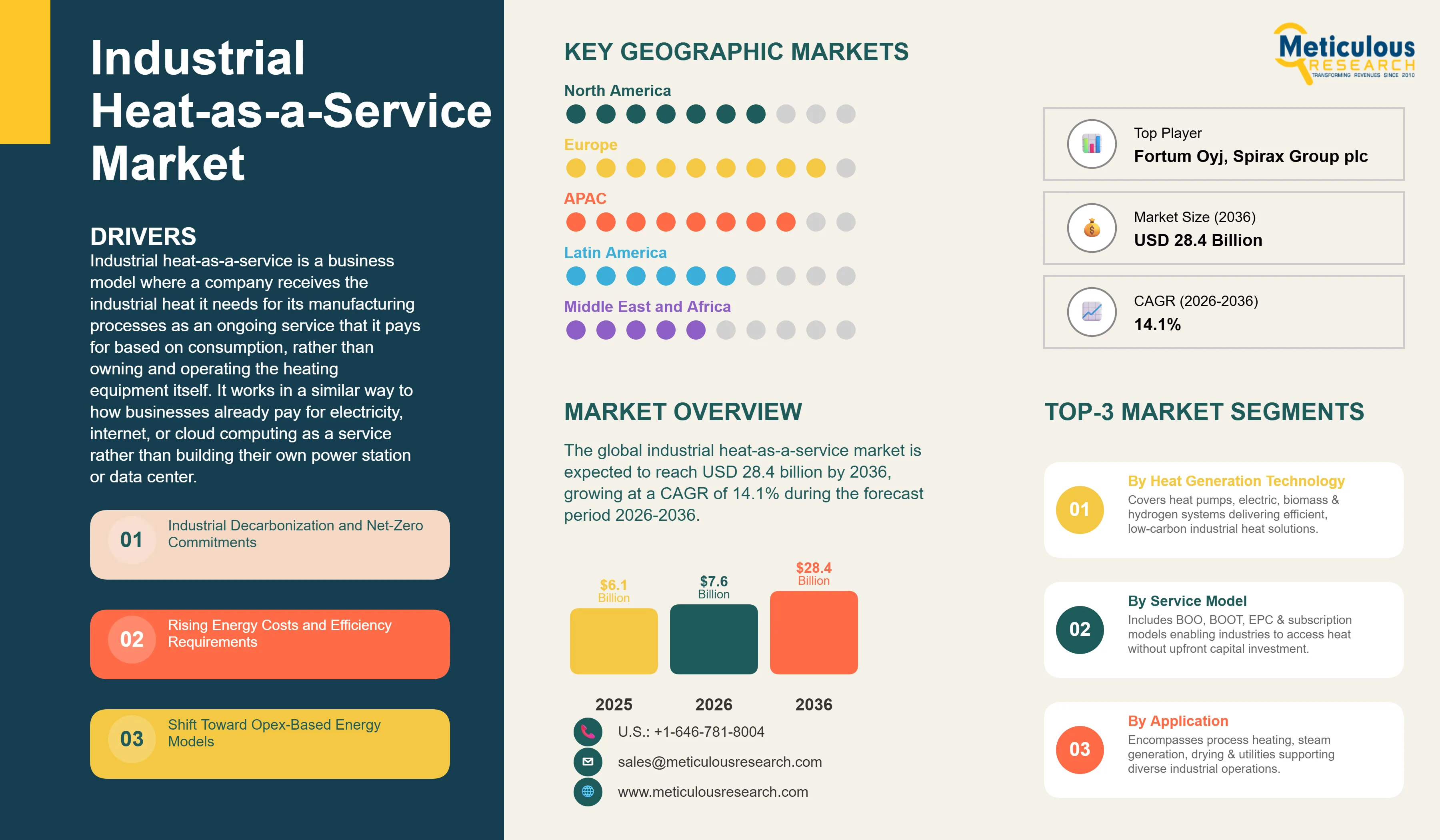

The global industrial heat-as-a-service market was valued at USD 6.1 billion in 2025. This market is expected to reach USD 28.4 billion by 2036 from an estimated USD 7.6 billion in 2026, growing at a CAGR of 14.1% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Industrial heat-as-a-service is a business model where a company receives the industrial heat it needs for its manufacturing processes as an ongoing service that it pays for based on consumption, rather than owning and operating the heating equipment itself. It works in a similar way to how businesses already pay for electricity, internet, or cloud computing as a service rather than building their own power station or data center. An energy service company builds, owns, and operates the heat generation system, which might use industrial heat pumps, electric boilers, biomass burners, or hydrogen combustion equipment, and then sells the heat output to the industrial customer at a contracted price per unit of heat delivered. The industrial company benefits from getting the heat it needs without having to invest capital in heating equipment, manage its operation, or deal with its eventual replacement, while also gaining access to cleaner heat sources that might be too expensive or technically complex to install and operate independently.

The market is growing because industrial heat demand represents approximately 20% of total global energy consumption and is one of the most challenging sectors to decarbonize, creating very large commercial opportunities for service providers that can deliver clean industrial heat at competitive prices. Factory processes including cooking, drying, sterilizing, distilling, forming metals, and producing chemicals all require heat at temperatures ranging from below 100 degrees Celsius up to over 1,000 degrees Celsius, and the vast majority of this heat is currently produced by burning natural gas, coal, or oil. Industrial companies facing growing carbon pricing costs, net-zero commitments, and energy price volatility are looking for ways to both decarbonize their heat supply and convert the significant capital cost of heating infrastructure into a more predictable operating expense, both of which the heat-as-a-service model addresses directly.

Two significant opportunities are shaping the market's development. The availability of low-carbon heat technologies, particularly industrial heat pumps that can deliver heat below 200 degrees Celsius at efficiencies three to five times higher than direct electric heating, is creating a compelling clean heat option for a large share of industrial heat demand and making the economics of heat-as-a-service agreements more attractive to both providers and customers. In addition, the integration of digital monitoring and smart energy management with heat-as-a-service contracts is enabling providers to continuously optimize heat delivery efficiency, detect equipment problems before they cause service interruptions, and demonstrate verified performance against contractual obligations in ways that were previously very difficult, building the trust and transparency required for long-term service agreements.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 28.4 Billion |

|

Market Size in 2026 |

USD 7.6 Billion |

|

Market Size in 2025 |

USD 6.1 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 14.1% |

|

Dominating Heat Generation Technology |

Industrial Heat Pumps |

|

Fastest Growing Heat Generation Technology |

Hydrogen-Based Heating Systems |

|

Dominating Service Model |

Build-Own-Operate (BOO) |

|

Fastest Growing Service Model |

Subscription-Based Models |

|

Dominating Application |

Process Heating |

|

Fastest Growing Application |

Steam Generation |

|

Dominating End-Use Industry |

Chemicals & Petrochemicals |

|

Fastest Growing End-Use Industry |

Pharmaceuticals |

|

Dominating Temperature Range |

Medium Temperature (100-400°C) |

|

Fastest Growing Temperature Range |

High Temperature (>400°C) |

|

Dominating Fuel Type |

Electricity |

|

Fastest Growing Fuel Type |

Hydrogen |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Energy Service Companies Expanding from Buildings into Industrial Heat

The most commercially important structural trend in the industrial heat-as-a-service market is the expansion of established energy service companies from their traditional building energy management business into industrial heat as a natural extension of their service capabilities. Companies including ENGIE, Veolia, and Siemens Energy have built large and profitable businesses providing energy-as-a-service to commercial and institutional building owners, covering electricity, heating, cooling, and energy efficiency services under long-term performance contracts. The same fundamental business model, where the ESCO invests in energy infrastructure, manages its operation, and sells the energy service rather than the equipment, transfers naturally to industrial heat applications with the primary difference being the much higher heat temperatures and larger volumes required by industrial processes compared with building heating.

ENGIE's industrial energy services business, which covers heat supply, steam generation, and combined heat and power for large industrial customers in Europe, North America, and Asia, is one of the most commercially advanced examples of industrial heat-as-a-service at scale. Veolia's industrial energy services division similarly offers heat and utility supply services to industrial customers across Europe. The commercial experience these companies have accumulated in structuring long-term energy service contracts, managing performance risk, financing energy infrastructure investment, and integrating digital monitoring into service delivery is a significant competitive asset that makes them the likely market leaders as industrial heat-as-a-service scales up through the forecast period.

Industrial Heat Pumps Unlocking Clean Heat at Commercially Viable Cost

The rapid improvement in industrial heat pump technology and its commercial deployment at manufacturing facilities across Europe and Asia is creating the clean heat generation technology that the heat-as-a-service market needs to offer genuinely low-carbon industrial heat at competitive prices. Industrial heat pumps work by using electricity to extract heat from a lower-temperature source such as waste water, ambient air, or waste heat streams and upgrade it to the temperatures required for industrial processes, achieving heat output of three to five kilowatt-hours for every kilowatt-hour of electricity input. When powered by renewable electricity, an industrial heat pump delivers clean, carbon-free heat at a cost that is competitive with or increasingly cheaper than natural gas boilers, particularly in Europe where natural gas prices remain elevated and where carbon pricing is progressively increasing the cost of fossil fuel combustion.

Alfa Laval, Danfoss, and Mitsubishi Heavy Industries are among the leading industrial heat pump manufacturers developing systems capable of delivering heat at temperatures up to 160 to 180 degrees Celsius, covering the large majority of low and medium temperature industrial process heat demand. The IEA estimates that industrial heat pumps could provide approximately 20% of global industrial heat demand if deployed at full potential, representing an enormous addressable market. For heat-as-a-service providers, industrial heat pumps represent the lowest-carbon and increasingly lowest-operating-cost heat generation technology for the large low and medium temperature heat segment, making them the primary technology choice for new heat-as-a-service projects targeting food and beverage, chemical, pharmaceutical, and textile customers whose processes operate below 200 degrees Celsius.

EU Industrial Decarbonization Policy Creating Mandatory Demand

The European Union's Industrial Emissions Directive, the Energy Efficiency Directive, and the EU Emissions Trading System are collectively creating a regulatory environment in which large industrial companies in Europe face growing financial penalties for carbon-intensive heat supply, progressively stronger requirements to improve energy efficiency, and mandatory reporting obligations that create pressure to demonstrate credible decarbonization pathways. The EU ETS carbon price, which has risen substantially over the past five years to levels that make gas-fired industrial heat meaningfully more expensive than its face fuel cost when carbon costs are included, is directly improving the financial competitiveness of low-carbon heat-as-a-service offerings relative to conventional gas boiler operations.

The EU's RE-PowerEU plan, which accelerated renewable energy deployment targets in response to the Russian gas supply disruption, has also specifically highlighted industrial heat electrification and industrial heat pumps as priority areas for policy support. Several EU member states including Germany, the Netherlands, Denmark, and Sweden have developed specific national support programs for industrial heat decarbonization that provide grants, subsidized loans, and regulatory fast-tracking for industrial heat pump and clean heat projects. These policy instruments are directly funding and enabling heat-as-a-service projects that would not yet be commercially viable without support, establishing the operational track record and commercial structures that the market needs to scale up through the forecast period.

Industrial Decarbonization and Net-Zero Commitments

The primary driver of the industrial heat-as-a-service market is the growing pressure on industrial companies to reduce carbon dioxide emissions from their manufacturing operations, with heat generation representing one of the largest and most technically challenging sources of industrial carbon emissions to address. Large industrial companies including major chemical producers, food and beverage companies, pharmaceutical manufacturers, and paper mills have made public net-zero emission commitments that require them to fundamentally change how they generate the heat their processes depend on, transitioning away from natural gas and coal boilers toward low-carbon heat sources. The heat-as-a-service model is commercially attractive for these decarbonization programs because it allows an industrial company to replace fossil fuel heating with low-carbon heat supply without having to bear the full capital cost of the new heat generation infrastructure itself, converting a large capital investment into a manageable operating expense while the ESCO bears the investment risk, technology risk, and performance responsibility. Carbon pricing systems in the EU, UK, Canada, and other jurisdictions are making the financial case for switching to clean heat-as-a-service progressively stronger as the effective cost of carbon-intensive heat supply increases each year.

Shift Toward Opex-Based Energy Models

A broader trend across corporate capital management is the preference for converting capital-intensive asset ownership into operating expenditure through service models, which is driving adoption of heat-as-a-service in the same way that it has driven cloud computing, equipment leasing, and facilities management outsourcing across other sectors. A manufacturing company whose core expertise is making food, chemicals, textiles, or pharmaceuticals typically has no strategic advantage in owning and operating boilers, heat pumps, or steam generation equipment. Converting industrial heat from a capital-intensive asset the company owns to a service it buys allows the company to free up balance sheet capital for investment in its core manufacturing and product development activities, reduce the operational complexity of managing energy infrastructure, and transfer the risk of energy infrastructure investment, technology obsolescence, and maintenance reliability to a service provider with genuine expertise in energy systems operation. Chief financial officers and boards at industrial companies increasingly recognize the balance sheet and risk management advantages of service models for non-core infrastructure, creating a financial management driver for heat-as-a-service adoption that operates alongside the sustainability and energy cost drivers.

Integration of Waste Heat Recovery Systems

One of the most economically attractive heat-as-a-service opportunities is the recovery and utilization of heat that is currently wasted from industrial processes and could be captured and reused either within the same facility or supplied to neighboring businesses through industrial heat networks. Many industrial processes including data centers, food processing plants, glass manufacturing, and metal casting release large amounts of waste heat to the atmosphere through cooling towers or exhaust stacks that could be captured with heat exchangers and heat pumps and reused for lower-temperature heating applications. An energy service company that invests in waste heat recovery infrastructure at an industrial facility and supplies the recovered heat back to the facility or to district heating networks at a service price lower than the cost of alternative heat generation can create a genuinely win-win commercial arrangement where the industrial customer reduces its heat costs and the ESCO generates revenue from heat that was previously wasted. The Danish district heating system, which supplies heat from multiple industrial waste heat sources to residential and commercial buildings in Copenhagen and other cities, is the world's most advanced example of this waste heat recovery service model and is providing a commercial template that other European countries and increasingly Asian markets are looking to replicate.

Digital Optimization and Smart Energy Management

The integration of advanced sensors, real-time energy monitoring, digital twins, and AI-based energy optimization with heat-as-a-service contracts is creating a new generation of intelligent heat service offerings that can deliver measurably superior performance, efficiency, and reliability compared with conventionally operated industrial heating systems. A smart heat-as-a-service system continuously monitors heat generation equipment performance, fuel consumption, heat delivery temperatures and volumes, and the industrial process's heat demand pattern, using AI optimization to adjust heat generation in real time to minimize energy waste, predict maintenance requirements before failures occur, and verify that contractual performance obligations are being met. For industrial customers, the digital monitoring capability provides full transparency into their heat supply performance and energy costs in a way that self-operated heating systems rarely deliver, making service contracts easier to justify to finance and sustainability teams. For heat-as-a-service providers, digital optimization reduces operating costs by improving efficiency and reducing unplanned maintenance, improving the economics of service contracts and creating a technical differentiation that is difficult for competitors without equivalent digital capabilities to match. Honeywell, Siemens Energy, Schneider Electric, and Johnson Controls are all investing in digital energy management platforms that integrate with their heat-as-a-service offerings.

By Heat Generation Technology: In 2026, Industrial Heat Pumps to Dominate

Based on heat generation technology, the global market is segmented into electric heating systems, industrial heat pumps, biomass and bioenergy systems, waste heat recovery systems, hydrogen-based heating systems, and solar thermal systems. In 2026, the industrial heat pumps segment is expected to account for the largest share of the global industrial heat-as-a-service market. Industrial heat pumps have become the preferred heat generation technology for the growing number of heat-as-a-service projects targeting the large low and medium temperature industrial heat market, because their energy efficiency of 300 to 500% compared with direct electric heating makes them the most cost-competitive clean heat option for process temperatures below approximately 180 degrees Celsius. The combination of declining heat pump equipment costs, rising natural gas prices and carbon costs in Europe, and growing availability of renewable electricity is progressively making industrial heat pump-based service offerings financially competitive with conventional gas boiler heat supply across a widening range of industrial applications.

However, the hydrogen-based heating systems segment is projected to register the highest CAGR during the forecast period. Green hydrogen produced by electrolysis of water using renewable electricity can be burned in specially designed hydrogen burners or fuel cells to deliver clean high-temperature heat above 400 degrees Celsius that heat pumps cannot economically produce, covering the high-temperature industrial heat demand that accounts for a significant share of total industrial heat consumption in sectors including steel, cement, glass, and ceramics. As green hydrogen production costs fall with electrolyzer scale-up and the hydrogen supply chain develops across Europe and Asia-Pacific, hydrogen-based heat-as-a-service contracts for high-temperature industrial applications are expected to grow from their currently very early commercial stage to a meaningful market segment through the forecast period.

By Service Model: In 2026, Build-Own-Operate to Hold the Largest Share

Based on service model, the global market is segmented into build-own-operate, build-own-operate-transfer, energy performance contracts, and subscription-based models. In 2026, the build-own-operate segment is expected to account for the largest share of the global industrial heat-as-a-service market. The BOO model, where the ESCO builds, owns, and permanently operates heat generation infrastructure at or near the industrial customer's site and sells heat output under a long-term supply agreement, is the most commercially established and most widely adopted service model in the market. BOO agreements provide the revenue certainty over long contract periods of 10 to 20 years that heat infrastructure investment requires for financial viability, and the permanent ownership by the ESCO aligns incentives for optimizing long-term equipment performance and efficiency.

However, the subscription-based models segment is projected to register the highest CAGR during the forecast period. Simpler subscription or pay-per-heat-unit pricing models with shorter commitment periods and more standardized contract terms are attracting smaller industrial customers and those who prefer flexibility over the lowest possible heat price, expanding the addressable market for heat-as-a-service beyond the large enterprises that traditional BOO contracts are designed for.

By Application: In 2026, Process Heating to Hold the Largest Share

Based on application, the global industrial heat-as-a-service market is segmented into process heating, steam generation, drying and dehydration processes, space heating and utilities, and cooling and integrated thermal systems. In 2026, the process heating segment is expected to account for the largest share of the global industrial heat-as-a-service market. Direct process heating, which includes heating raw materials, reaction vessels, and product streams to the temperatures required for chemical reactions, food processing, material forming, and other manufacturing operations, represents the majority of total industrial heat demand and the largest total addressable market for heat-as-a-service offerings across all temperature ranges. The three-tier breakdown of process heating into low, medium, and high temperature applications reflects the very different technologies and economics applicable to each temperature range, from heat pumps at lower temperatures to biomass and hydrogen at higher temperatures.

However, the steam generation segment is projected to register the highest CAGR during the forecast period. Steam is used very extensively across industrial manufacturing for heating, sterilization, driving turbines for combined heat and power, and numerous specific process applications in food, pharmaceutical, chemical, and paper manufacturing. Steam generation as a service, where an ESCO installs and operates a steam generation system, including the boiler, pipework, and controls, and sells steam output by the tonne rather than fuel to the industrial customer, is one of the most commercially well-established heat-as-a-service applications and is growing rapidly as industrial customers seek to decarbonize their steam supply by switching from gas boilers to electric or biomass steam generation under service contracts.

By End-Use Industry: In 2026, Chemicals and Petrochemicals to Hold the Largest Share

Based on end-use industry, the global industrial heat-as-a-service market is segmented into food and beverage, chemicals and petrochemicals, pulp and paper, textile, pharmaceuticals, metals and mining, and others. In 2026, the chemicals and petrochemicals segment is expected to account for the largest share of the overall market. The chemicals and petrochemicals industry is the world's largest consumer of industrial heat, requiring heat across a very wide range of temperatures for distillation, reaction, drying, and material processing, and it is also one of the sectors facing the strongest regulatory pressure to decarbonize under European and international climate frameworks. The very large heat consumption per facility and the sophisticated energy procurement capabilities of major chemical companies make this sector the highest-revenue end-use industry in the market.

However, the pharmaceuticals segment is projected to register the highest CAGR during the forecast period. Pharmaceutical manufacturing facilities have very stringent process requirements including precise temperature control, validated clean steam quality, and documented energy management that make heat-as-a-service offerings with strong digital monitoring and verification capabilities particularly well-suited to their needs. The rapid expansion of biopharmaceutical manufacturing capacity globally and the high value of pharmaceutical production that justifies premium pricing for reliable, high-quality heat supply create conditions for strong growth in pharmaceutical heat-as-a-service adoption.

Industrial Heat-as-a-Service Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global industrial heat-as-a-service market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the overall market. Europe leads the market because it has the most developed regulatory framework for industrial decarbonization, the most advanced energy service company ecosystem, the highest carbon pricing levels that make clean heat economically competitive with fossil fuel heat, and the strongest government support programs for industrial heat electrification and heat pump deployment. Germany, the Netherlands, Denmark, Sweden, and the UK are the most active markets for industrial heat-as-a-service, driven by their strong industrial base, high energy costs, ambitious national climate targets, and well-developed ESCO industries. ENGIE operates large industrial heat networks and supply contracts across France, Belgium, and Germany. Veolia provides industrial utility services including heat supply to major manufacturing companies across Europe. Danish companies including Danfoss and Alfa Laval have built strong positions in industrial heat pump supply that supports local deployment programs. The Netherlands' industrial energy transition programs specifically targeting chemical cluster decarbonization in the Rotterdam and Chemelot industrial parks are among the most ambitious industrial heat decarbonization programs in the world and are generating significant heat-as-a-service market activity. Sweden's long experience with district heating and combined heat and power provides commercial and regulatory precedents that are informing the development of industrial heat-as-a-service commercial structures.

However, the Asia-Pacific industrial heat-as-a-service market is expected to grow at the fastest CAGR during the forecast period. China's industrial sector is the world's largest consumer of industrial heat by total volume, and China's dual carbon goals of peak emissions by 2030 and carbon neutrality by 2060 are creating growing policy and regulatory pressure on energy-intensive industries to reduce fossil fuel heat consumption. Chinese energy companies and local government energy service platforms are developing heat-as-a-service offerings for industrial parks and manufacturing clusters, and several pilot programs for electric and biomass industrial heat service contracts have been established in leading industrial regions. India's very large and energy-intensive textile, chemical, and food processing industries represent a substantial long-term addressable market for clean heat services as the country develops its industrial energy transition policy framework. Japan's sophisticated industrial energy management culture, well-developed ESCO industry through companies including Mitsubishi Heavy Industries and Osaka Gas, and strong government programs for industrial decarbonization make it one of the most technically advanced Asia-Pacific markets for industrial heat-as-a-service. South Korea and Australia are also growing markets with active industrial decarbonization programs.

North America is a growing and commercially important market for industrial heat-as-a-service, primarily driven by the U.S. where the Inflation Reduction Act's industrial decarbonization incentives including investment tax credits for heat pumps, clean hydrogen production credits, and industrial efficiency grants are improving the economics of clean heat-as-a-service investments substantially. Honeywell, Siemens Energy, Schneider Electric, and Johnson Controls are all active in the U.S. industrial energy services market and are expanding their heat-as-a-service capabilities. Canada's industrial decarbonization programs and carbon pricing system create similar policy drivers for clean industrial heat adoption. Latin America and the Middle East and Africa represent earlier-stage markets where the heat-as-a-service model is less established but where growing energy costs, sustainability commitments from large industrial corporations, and the economic advantage of service models in capital-constrained environments are creating growing commercial interest.

The industrial heat-as-a-service market includes large integrated energy companies and utilities that provide industrial heat as part of broader energy service portfolios, specialist energy service companies focused on industrial energy management, equipment manufacturers that have extended into service models, and smaller specialist firms targeting specific industrial sectors or temperature ranges. Competition is based on the breadth and cleanliness of heat generation technology portfolio, the ability to finance long-term infrastructure investment, digital monitoring and performance verification capability, contract structuring and risk management experience, and geographic reach across industrial customer locations.

ENGIE is the largest provider of industrial heat-as-a-service globally, with operations across Europe, North America, and Asia covering industrial heat networks, combined heat and power, and process heat services for major manufacturing customers. Veolia's industrial utilities division provides heat, steam, and utility services to large industrial customers across Europe including at several major chemical industrial parks. Fortum, the Finnish utility, operates large-scale heat services for industrial customers across the Nordic countries and has been expanding into industrial heat pump-based services. Siemens Energy and Honeywell provide digital energy management platforms that underpin smart heat-as-a-service contract monitoring and optimization. Spirax Group specializes in steam system services for industrial customers and is well-positioned for the growing steam-as-a-service segment. Thermax Limited is India's leading industrial energy and environment solutions company with a growing heat-as-a-service portfolio for Indian manufacturing customers.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' service portfolios, geographic presence, technology capabilities, and recent strategic developments. Some of the key players operating in the global industrial heat-as-a-service market include ENGIE (France), Veolia Environment S.A. (France), Siemens Energy AG (Germany), Fortum Oyj (Finland), EDF Energy (UK), Orsted A/S (Denmark), Enel X (Italy), Johnson Controls International plc (Ireland), Schneider Electric SE (France), Honeywell International Inc. (U.S.), Spirax Group plc (UK), Thermax Limited (India), Alfa Laval AB (Sweden), Danfoss A/S (Denmark), and Mitsubishi Heavy Industries Ltd. (Japan), among others.

The global industrial heat-as-a-service market is expected to reach USD 28.4 billion by 2036 from an estimated USD 7.6 billion in 2026, at a CAGR of 14.1% during the forecast period 2026-2036.

In 2026, the industrial heat pumps segment is expected to hold the largest share of the global market, driven by heat pumps being the most energy-efficient and cost-competitive clean heat generation technology for the large low and medium temperature industrial heat market where their three-to-five-times electrical efficiency advantage over direct electric heating makes them financially compelling.

The hydrogen-based heating systems segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by green hydrogen being the primary clean heat technology for high-temperature industrial processes above 400 degrees Celsius where heat pumps are not economically practical, and by the developing green hydrogen supply chain and falling electrolyzer costs progressively improving hydrogen heat economics.

In 2026, the process heating segment is expected to hold the largest share of the global industrial heat service market, reflecting direct process heating representing the majority of total industrial heat demand across all temperature ranges and all manufacturing industries.

The market is primarily driven by industrial companies' growing pressure to decarbonize their manufacturing heat supply under net-zero commitments and carbon pricing frameworks, and by the financial and operational advantages of the service model that allows companies to access clean heat infrastructure without capital investment while converting a large fixed cost into a predictable and flexible operating expense aligned with their production volumes.

Key players are ENGIE (France), Veolia Environment S.A. (France), Siemens Energy AG (Germany), Fortum Oyj (Finland), EDF Energy (UK), Orsted A/S (Denmark), Enel X (Italy), Johnson Controls International plc (Ireland), Schneider Electric SE (France), Honeywell International Inc. (U.S.), Spirax Group plc (UK), Thermax Limited (India), Alfa Laval AB (Sweden), Danfoss A/S (Denmark), and Mitsubishi Heavy Industries Ltd. (Japan), among others.

Asia-Pacific is expected to register the highest growth rate in the global market during the forecast period 2026-2036, driven by China's very large industrial heat consumption and dual carbon policy targets, Japan's sophisticated ESCO industry and industrial decarbonization programs, and India's rapidly growing industrial sector with increasing energy cost and sustainability pressures on its manufacturing base.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Industrial Decarbonization and Net-Zero Commitments

4.2.1.2 Rising Energy Costs and Efficiency Requirements

4.2.1.3 Shift Toward Opex-Based Energy Models

4.2.1.4 Increasing Adoption of Electrification and Renewable Heat

4.2.2 Restraints

4.2.2.1 High Initial Infrastructure Investment

4.2.2.2 Long-Term Contract Complexity

4.2.2.3 Limited Awareness in Developing Markets

4.2.3 Opportunities

4.2.3.1 Integration of Waste Heat Recovery Systems

4.2.3.2 Adoption of Low-Carbon Heat Technologies (Heat Pumps, Hydrogen)

4.2.3.3 Expansion in Energy-Intensive Industries

4.2.3.4 Digital Optimization and Smart Energy Management

4.2.4 Challenges

4.2.4.1 Performance Risk and Contractual Obligations

4.2.4.2 Technology Integration Across Legacy Systems

4.3 Technology Landscape

4.3.1 Electric Boilers and Resistance Heating

4.3.2 Industrial Heat Pumps

4.3.3 Biomass and Bioenergy Systems

4.3.4 Waste Heat Recovery Technologies

4.3.5 Hydrogen-Based Heating Systems

4.3.6 Thermal Energy Storage Systems

4.4 Heat-as-a-Service Value Chain

4.4.1 Heat Generation Infrastructure Providers

4.4.2 Energy Service Companies (ESCOs)

4.4.3 Digital Monitoring and Control Providers

4.4.4 Industrial Customers

4.4.5 Financing and Investment Partners

4.5 Value Chain Analysis

4.5.1 Equipment Manufacturers

4.5.2 Energy Service Providers

4.5.3 EPC Contractors

4.5.4 Industrial End Users

4.5.5 Financing Institutions

4.6 Regulatory and Policy Landscape

4.6.1 Carbon Pricing and Emission Regulations

4.6.2 Energy Efficiency Directives

4.6.3 Industrial Decarbonization Policies

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth in Energy-as-a-Service Models

4.8.2 Strategic Partnerships and ESCO Expansion

4.8.3 Investments in Clean Heat Technologies

4.9 Cost and Pricing Analysis

4.9.1 Pricing Models (Pay-per-Use, Subscription, Performance-Based)

4.9.2 Heat Cost per MWh Analysis

4.9.3 Capex vs Opex Comparison

5. Industrial Heat-as-a-Service Market, by Heat Generation Technology

5.1 Introduction

5.2 Electric Heating Systems

5.3 Industrial Heat Pumps

5.4 Biomass and Bioenergy Systems

5.5 Waste Heat Recovery Systems

5.6 Hydrogen-Based Heating Systems

5.7 Solar Thermal Systems

6. Industrial Heat-as-a-Service Market, by Service Model

6.1 Introduction

6.2 Build-Own-Operate (BOO)

6.3 Build-Own-Operate-Transfer (BOOT)

6.4 Energy Performance Contracts (EPC)

6.5 Subscription-Based Models

7. Industrial Heat-as-a-Service Market, by Application

7.1 Introduction

7.2 Process Heating (Largest Segment)

7.2.1 Low-Temperature Heating (<100°C)

7.2.2 Medium-Temperature Heating (100-400°C)

7.2.3 High-Temperature Heating (>400°C)

7.3 Steam Generation

7.3.1 Industrial Boilers

7.3.2 Combined Heat and Power (CHP) Systems

7.4 Drying and Dehydration Processes

7.4.1 Food Drying

7.4.2 Chemical Processing

7.5 Space Heating and Utilities

7.5.1 Industrial Buildings

7.5.2 Warehouses

7.6 Cooling and Integrated Thermal Systems

7.6.1 Absorption Cooling

7.6.2 Combined Heating and Cooling

8. Industrial Heat-as-a-Service Market, by End-Use Industry

8.1 Introduction

8.2 Food & Beverage

8.3 Chemicals & Petrochemicals

8.4 Pulp & Paper

8.5 Textile Industry

8.6 Pharmaceuticals

8.7 Metals & Mining

8.8 Others

9. Industrial Heat-as-a-Service Market, by Temperature Range

9.1 Introduction

9.2 Low Temperature (<100°C)

9.3 Medium Temperature (100-400°C)

9.4 High Temperature (>400°C)

10. Industrial Heat-as-a-Service Market, by Fuel Type

10.1 Introduction

10.2 Electricity

10.3 Biomass

10.4 Natural Gas

10.5 Hydrogen

10.6 Others

11. Industrial Heat-as-a-Service Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Denmark

11.3.6 Sweden

11.3.7 Italy

11.3.8 Spain

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Australia

11.4.6 Indonesia

11.4.7 Thailand

11.4.8 Vietnam

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Egypt

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 ENGIE

13.2 Veolia Environment S.A.

13.3 Siemens Energy AG

13.4 Fortum Oyj

13.5 EDF Energy

13.6 Orsted A/S

13.7 Enel X

13.8 Johnson Controls International plc

13.9 Schneider Electric SE

13.10 Honeywell International Inc.

13.11 Spirax Group plc

13.12 Thermax Limited

13.13 Alfa Laval AB

13.14 Danfoss A/S

13.15 Mitsubishi Heavy Industries Ltd.

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Feb-2026

Published Date: Jan-2026

Published Date: Apr-2025

Subscribe to get the latest industry updates