Resources

About Us

Water and Wastewater Treatment Technologies Market, by Type (Membrane Separation & Filtration, Sludge Management, Activated Sludge, Clarification, Electrochemical Water Treatment, Membrane Bioreactor (MBR), UV and Ozone, Dissolved Air Flotation), Application (Municipal, Residential, Industrial), and Geography – Global Forecast to 2036

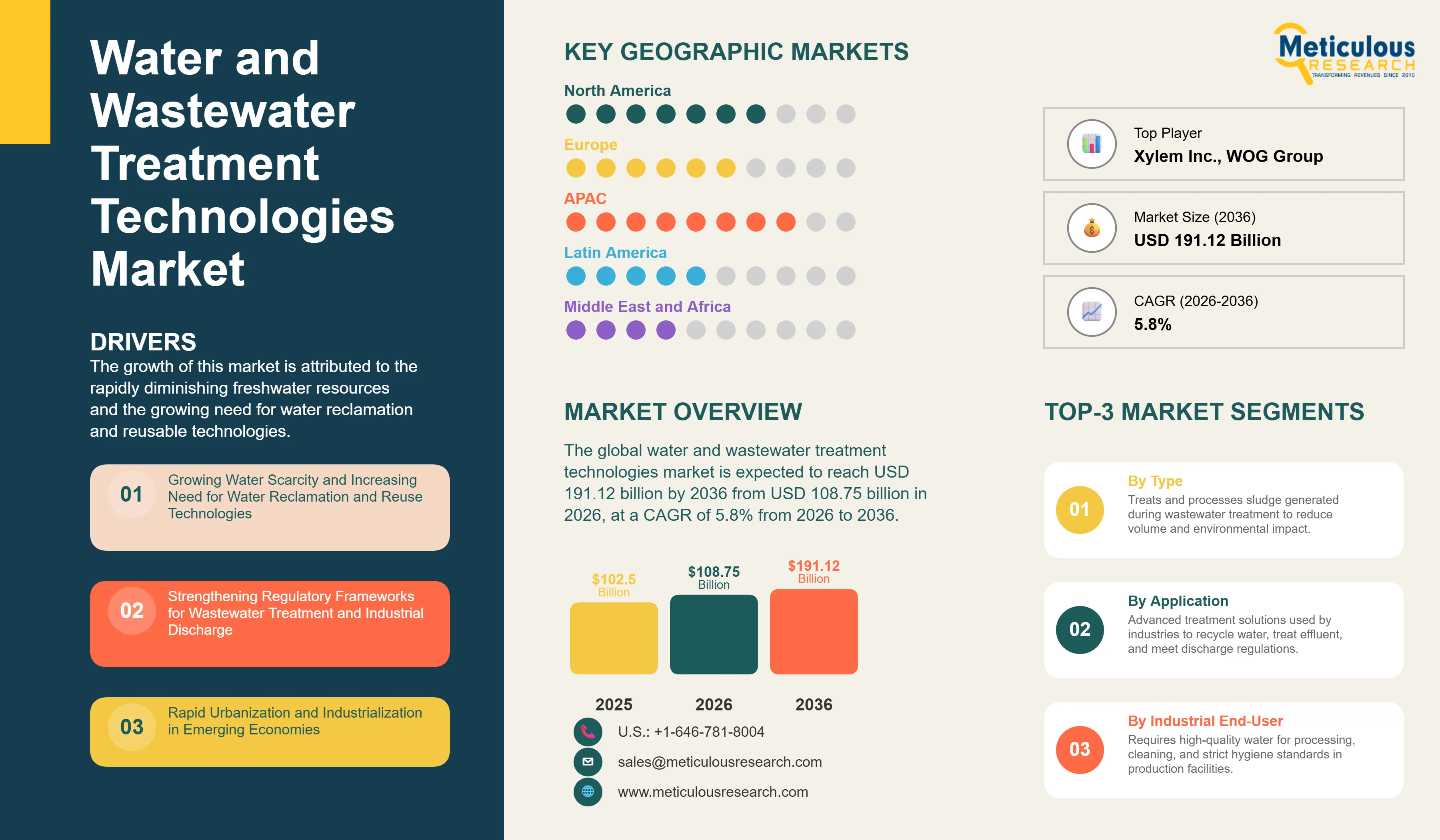

Report ID: MROTH - 104613 Pages: 250 Feb-2026 Formats*: PDF Category: Others Delivery: 24 to 48 Hours Download Free Sample ReportThe global water and wastewater treatment technologies market was valued at USD 102.50 billion in 2025. This market is expected to reach USD 191.12 billion by 2036 from USD 108.75 billion in 2026, at a CAGR of 5.8% from 2026 to 2036.

The growth of this market is attributed to the rapidly diminishing freshwater resources and the growing need for water reclamation and reusable technologies. According to the 2025 AQUASTAT Water Data Snapshot published by the Food and Agriculture Organization of the United Nations (FAO), renewable water availability per person declined by a further 7% over the past decade, while pressure on already scarce freshwater resources is intensifying in several regions. According to a joint report by the World Health Organization (WHO) and UNICEF published during World Water Week in August 2025, 2.1 billion people, representing approximately one in four people globally, still lack access to safely managed drinking water, underscoring the enormous unmet demand for effective water treatment infrastructure worldwide.

Additionally, the increasing severity of water stress driven by population growth, rapid urbanization, industrial expansion, and climate change is pushing governments, utilities, and industries to invest in advanced water treatment technologies that can recover, reclaim, and recirculate water resources. The growing regulatory emphasis on industrial wastewater discharge standards, the accelerating rollout of PFAS-related regulations in North America and Europe, and the increasing adoption of membrane bioreactors, advanced oxidation processes, and digital water management platforms are expected to offer significant growth opportunities for the players in this market. However, the lack of awareness of appropriate water treatment techniques in developing markets, the high capital cost of advanced wastewater treatment technologies, and the aging and deterioration of existing water infrastructure are major challenges to the growth of this market.

Market Highlights: Water and Wastewater Treatment Technologies

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Water and wastewater treatment technologies include a broad range of physical, chemical, and biological processes designed to remove contaminants, suspended solids, dissolved compounds, and pathogens from water and wastewater streams, enabling safe discharge to the environment or reclamation for potable, industrial, and agricultural reuse. The market is segmented by treatment technologies into membrane separation and filtration (reverse osmosis, ultrafiltration, microfiltration, and nanofiltration), sludge management, activated sludge biological treatment, membrane bioreactors, clarification, electrochemical treatment, advanced oxidation processes, UV and ozone disinfection, dissolved air flotation, activated carbon adsorption, chlorination, and industrial demineralization, deployed across municipal water and wastewater utilities, residential water purification, and a wide range of industrial applications.

The market is undergoing a significant technological transformation driven by the combination of regulatory tightening, escalating water stress, and the increasing adoption of digital technologies in water treatment operations. The recast Urban Wastewater Treatment Directive (EU) 2024/3019 entered into force on January 1, 2025, strengthening treatment requirements and extending coverage to agglomerations with population equivalents of 1,000 or more, with phased implementation timelines extending through 2045 depending on facility size and pollutant type. In April 2024, the U.S. Environmental Protection Agency (EPA) finalized the National Primary Drinking Water Regulation establishing Maximum Contaminant Levels of 4.0 parts per trillion for PFOA and PFOS, alongside standards for three additional PFAS substances, with ongoing evaluation of further expansions. These regulatory developments are increasing investment in advanced membrane filtration, granular activated carbon, ion-exchange, and electrochemical treatment technologies capable of removing persistent organic contaminants, micropollutants, and "forever chemicals" from water and wastewater streams.

In 2024 and 2025, major players continued to invest in technology innovation and strategic market positioning. Veolia has advanced its membrane bioreactor portfolio with energy-optimized designs supporting operational efficiency goals. In March 2025, DuPont Water Solutions launched WAVE PRO, an advanced online modeling tool to optimize ultrafiltration water treatment systems. In June 2025, Solenis and NCH Corporation announced a definitive merger agreement, which was completed in November 2025 to form a diversified global water treatment and hygiene solutions provider. In July 2025, H2O America announced a $540 million acquisition of Quadvest to upgrade water infrastructure in the Houston metro area, reflecting the scale of capital investment in municipal water infrastructure modernization. Xylem continues to advance anaerobic membrane bioreactor (AnMBR) technology for resource recovery through biogas production, supporting the growing industry focus on the water-energy nexus and circular resource management.

What are the Key Trends in the Water and Wastewater Treatment Technologies Market?

Growing Adoption of Membrane Bioreactors and Advanced Filtration Technologies

The growing adoption of membrane bioreactors (MBRs) and advanced membrane filtration technologies is a significant trend in the water and wastewater treatment technologies market. MBR systems, which combine conventional activated sludge biological treatment with membrane filtration to produce high-quality effluent in a compact footprint, are increasingly displacing conventional activated sludge systems in municipal wastewater treatment upgrades and new industrial treatment installations. Key drivers include the EU's recast Urban Wastewater Treatment Directive (EU 2024/3019), which entered into force in January 2025, the U.S. Environmental Protection Agency's updated water reuse guidance under the National Water Reuse Action Plan framework, and stricter industrial discharge enforcement across Asia-Pacific. Leading technology providers including Xylem, Veolia, and Hitachi have advanced their MBR portfolios with energy-optimized designs and enhanced nutrient removal capabilities to support regulatory compliance and operational efficiency goals. The growing commercialization of anaerobic MBR technology for biogas production reflects the expanding focus on resource recovery from wastewater treatment processes.

Increasing Integration of Artificial Intelligence and Digital Water Management Platforms

The increasing integration of artificial intelligence (AI), IoT-based monitoring, and digital water management platforms into water and wastewater treatment operations is a rapidly growing trend in the market. AI-enabled treatment platforms draw upon real-time sensor data including influent quality, microbial activity, flow rates, and chemical dosing parameters to dynamically optimize treatment processes, improve energy efficiency, and enhance environmental compliance. Veolia's AQUAVISTA™ digital platform and similar offerings from Xylem, SUEZ, and DuPont enable utilities to leverage predictive analytics for proactive maintenance, energy optimization, and regulatory reporting. Industry deployments indicate growing adoption of smart water technologies in municipal systems globally, with real-time water quality monitoring sensors increasingly integrated into treatment infrastructure to support data-driven operational decisions and resilience planning.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 191.12 Billion |

|

Market Size in 2025 |

USD 102.50 Billion |

|

Market Size in 2026 |

USD 108.75 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 5.8% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Type: Membrane Separation & Filtration, Sludge Management Technology, Activated Sludge, Clarification, Gas Separation, Electrochemical Water Treatment Technology, Electrochemical Scale Treatment Systems, Activated Carbon Technology, Chlorination, Industrial Demineralization, Membrane Bioreactor (MBR), UV and Ozone, Dissolved Air Flotation, Other Treatment Technologies By Application: Municipal, Residential, Industrial (Food & Beverages, Pharmaceuticals & Chemicals, Power Generation, Pulp & Paper, Oil & Gas, Mining, Petrochemical, Electronics & Semiconductors, Other Industrial Applications) By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Growing Water Scarcity and Increasing Need for Water Reclamation and Reuse Technologies

The rapidly diminishing availability of fresh water resources globally is a primary driver of the water and wastewater treatment technologies market. According to the 2025 AQUASTAT Water Data Snapshot released by the FAO, renewable freshwater availability per person declined by 7% over the past decade, with pressure on already scarce freshwater resources intensifying across Northern Africa, Western Asia, and parts of Asia-Pacific and Latin America. The UN World Water Development Report indicates that roughly half of the world’s population experiences severe water scarcity for at least part of the year. Only 0.5% of water on Earth is useable and available freshwater, and climate change, population growth, and economic development are placing increasing pressure on this finite resource, compelling governments, utilities, and industries to invest in technologies that can treat, reclaim, and reuse water across municipal, residential, and industrial applications.

The growing population continues to build pressure on water resources that are already under massive strain. Technologies that promote more efficient use of already available water, including advanced membrane filtration, biological treatment, water reuse systems, and zero-liquid-discharge technologies, are gaining significant investment and adoption globally. Water scarcity, energy savings objectives, and increasingly complex industrial wastewater treatment demands are pushing organizations to implement advanced techniques to optimize both environmental and economic performance.

Strengthening Regulatory Frameworks for Wastewater Treatment and Industrial Discharge

The strengthening of wastewater treatment and water quality regulations across North America, Europe, and Asia-Pacific is driving mandatory investment in advanced treatment technologies across municipal, industrial, and residential applications. The European Union’s recast Urban Wastewater Treatment Directive (2024) requires all urban areas with population equivalents above 1,000 to achieve at least secondary treatment by 2035, with additional requirements for nutrient removal and micropollutant elimination at larger installations. In the U.S., the EPA’s reaffirmation and expansion of PFAS maximum contaminant levels in May 2025 is compelling water utilities and industrial facilities to invest in advanced treatment technologies, such as nanofiltration, reverse osmosis, granular activated carbon, and ion-exchange systems capable of meeting the new standards. Stricter industrial discharge enforcement in Asia-Pacific is similarly driving adoption of advanced biological, membrane, and chemical treatment technologies across manufacturing, petrochemical, electronics, and food processing sectors.

Growing Demand for Energy-Efficient and Advanced Water Treatment Technologies

The growing demand for energy-efficient, resource-recovering, and technologically advanced water treatment systems presents a significant opportunity for technology developers and players across the water and wastewater treatment technologies market. Industrial wastewater treatment operations are among the most energy-intensive processes in manufacturing, and the growing cost of energy, combined with sustainability mandates and carbon reduction commitments, is driving demand for low-energy membrane systems, anaerobic biological treatment technologies, and AI-optimized operational platforms that reduce both energy consumption and chemical usage. Low-pressure ultrafiltration and microfiltration units now operate with 40–60% lower pressures than older models, offering significant energy savings, particularly in decentralized and energy-constrained environments. The growing focus on the water-energy nexus, including the recovery of biogas energy from anaerobic treatment of organic wastewater, is further expanding the value proposition of advanced treatment technologies.

Why Does the Membrane Separation & Filtration Segment Dominate the Water and Wastewater Treatment Technologies Market?

Based on type, in 2026, the membrane separation & filtration segment is expected to account for the largest share of the overall water and wastewater treatment technologies market. This market is also projected to grow at the fastest CAGR during the forecast period. The dominant market share of this segment is attributed to the growing emphasis on reducing chemical usage in water treatment, the rising demand for low energy-consuming water treatment processes, the relatively low installation costs compared to multi-stage chemical treatment alternatives, and the broad applicability of membrane technologies across municipal drinking water production, wastewater reuse, industrial process water, and desalination applications.

The growing adoption of PFAS and micropollutant removal regulations in the U.S. and Europe is further driving the demand for nanofiltration and reverse osmosis systems, as these membrane technologies provide the highest levels of contaminant rejection among commercially available treatment options. The growing integration of AI-driven predictive maintenance and digital twin modeling, such as DuPont’s WAVE PRO ultrafiltration optimization tool launched in March 2025, is enhancing the operational efficiency and lifecycle performance of membrane treatment systems, further driving the growth of this segment.

Why Does the Industrial Segment Dominate the Water and Wastewater Treatment Technologies Market?

Based on application, in 2026, the industrial segment is expected to account for the largest share of the overall water and wastewater treatment technologies market, and is also projected to grow at the fastest CAGR during the forecast period. The large market share of this segment is attributed to the growing industrialization and urbanization, the rising focus on water quality from the industrial sector, the growing necessity for recycling and reusing water in water-intensive manufacturing processes, and the increasing advancements in industrial wastewater treatment technologies. Industries including food & beverages, pharmaceuticals & chemicals, power generation, oil & gas, petrochemicals, electronics & semiconductors, and mining are major users of specialized water treatment systems required to meet increasingly stringent industrial discharge standards and internal water efficiency targets.

Within industrial applications, the food & beverages segment represents a significant sub-segment, driven by the high volumes of process water and wastewater generated in food processing operations and the stringent hygiene and quality standards applicable to food-contact water. The electronics & semiconductors industry is also a significant and growing industrial application, with semiconductor fabrication facilities requiring ultrapure water treatment systems and advanced wastewater treatment to manage high-purity process water streams and toxic metal-bearing effluents.

U.S. Water and Wastewater Treatment Technologies Market Size and Growth 2026 to 2036

The U.S. water and wastewater treatment technologies market is projected to grow at a steady CAGR from 2026 to 2036, driven by significant federal and state-level investment in water infrastructure modernization, the accelerating enforcement of PFAS regulations under the EPA’s expanded National Primary Drinking Water Regulation, and the growing adoption of advanced membrane filtration, biological treatment, and digital water management technologies. North America has a well-developed regulatory environment for water quality and wastewater discharge, with the Clean Water Act and Safe Drinking Water Act providing foundational compliance frameworks that drive investment in treatment infrastructure. In July 2025, H2O America announced the investment of USD 540 million in acquiring and upgrading water infrastructure in Houston, Texas, reflecting the scale of capital investment in U.S. municipal water infrastructure.

How is Asia-Pacific Maintaining Dominance in the Water and Wastewater Treatment Technologies Market?

Based on geography, in 2026, Asia-Pacific is expected to account for the largest share of the global water and wastewater treatment technologies market, and is also projected to register the fastest CAGR during the forecast period. The large share of this region is mainly attributed to the combination of the large and rapidly expanding installed base of municipal and industrial water treatment infrastructure, the rapidly growing population and urbanization rates across China, India, Indonesia, and Southeast Asia, the high levels of industrial activity generating significant volumes of wastewater requiring treatment, and the significant government investment in water infrastructure driven by both environmental necessity and economic development priorities.

China is expected to dominate the water and wastewater treatment technologies market within Asia-Pacific due to its enormous population base, the scale of its industrial water treatment requirements, and the ambitious targets set under its national water pollution prevention and control programs. China is also expected to witness significant growth during the forecast period, driven by the continued investment in smart water management, desalination, and advanced wastewater reclamation infrastructure. The increasing number of investments in water infrastructure by public sector organizations in developing countries such as India, Indonesia, and Malaysia, and the rising demand for water treatment technologies to provide clean and potable water to rapidly urbanizing populations, are additional factors driving the fastest regional growth in Asia-Pacific.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by the leading market participants in the water and wastewater treatment technologies market between 2023 and 2026. The key players profiled in the water and wastewater treatment technologies market report are Suez S.A. (France), Veolia Environnement S.A. (France), Xylem Inc. (U.S.), DuPont de Nemours, Inc. (U.S.), United Utilities Group PLC (U.K.), Kingspan Group plc (U.K.), The Dow Chemical Company (U.S.), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), BioMicrobics, Inc. (U.S.), Trojans Technologies Inc. (Canada), Thermax Limited (India), WOG Group (India), SWA Water Technologies PTY LTD. (Australia), Burns & McDonnell (U.S.), Solenis LLC (U.S.), and Pentair plc (U.K./U.S.), among others.

Water and Wastewater Treatment Technologies Market, by Type

Water and Wastewater Treatment Technologies Market, by Application

Water and Wastewater Treatment Technologies Market, by Geography

This study offers a detailed assessment of the water and wastewater treatment technologies market, including market sizes and forecasts by value for various segmentations such as type, application, and geography. The study also involves the value analysis of various segments at regional and country levels.

The global water and wastewater treatment technologies market is projected to reach USD 191.12 billion by 2036, at a CAGR of 5.8% during the forecast period from 2026 to 2036.

In 2026, the membrane separation & filtration segment is estimated to account for the largest share of the water and wastewater treatment technologies market. The growing emphasis on reducing chemical usage in water treatment, the rising demand for low energy-consuming treatment processes, the accelerating regulatory requirements for PFAS and micropollutant removal, low installation costs, and broad applicability across municipal, industrial, and desalination applications are the primary factors contributing to the largest market share and fastest projected growth of the membrane separation & filtration segment.

The industrial application segment is projected to showcase the highest growth opportunities, driven by growing industrialization and urbanization, the rising focus on water quality and compliance from the industrial sector, the growing necessity for recycling and reusing water in manufacturing processes, and the increasing advancements in industrial wastewater treatment technologies. Within industrial applications, the food & beverages and electronics & semiconductors sub-segments represent significant and growing opportunities.

The growth of this market is attributed to rapidly diminishing freshwater resources and the growing need for water reclamation and reuse technologies. Additionally, the growing demand for energy-efficient and advanced water treatment technologies, the strengthening of regulatory frameworks for industrial discharge and PFAS removal, and the increasing adoption of digital and AI-driven water management platforms are expected to create significant growth opportunities for market participants. The high capital cost of advanced wastewater treatment technologies and the lack of awareness in developing markets can restrain growth. The aging and deterioration of existing water infrastructure in mature markets represents a major challenge, but also an opportunity for technology providers offering cost-effective modernization and retrofit solutions.

The key players operating in the water and wastewater treatment technologies market are Suez S.A. (France), Veolia Environnement S.A. (France), Xylem Inc. (U.S.), DuPont de Nemours, Inc. (U.S.), United Utilities Group PLC (U.K.), Kingspan Group plc (U.K.), The Dow Chemical Company (U.S.), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), BioMicrobics, Inc. (U.S.), Trojan Technologies Inc. (Canada), Thermax Limited (India), WOG Group (India), SWA Water Technologies PTY LTD. (Australia), Burns & McDonnell (U.S.), Solenis LLC (U.S.), and Pentair plc (U.K./U.S.), among others.

Asia-Pacific currently accounts for the largest share of the global water and wastewater treatment technologies market and is also expected to register the fastest CAGR during the forecast period, driven by the rapid expansion of industrial and municipal water treatment infrastructure in China, India, Indonesia, and Southeast Asia, large-scale government investment in smart water management and infrastructure development, and the rising demand for water treatment technologies to serve rapidly urbanizing populations. North America represents the second-largest regional market, with the United States driving significant investment in water infrastructure modernization, PFAS remediation, and advanced treatment technology adoption, supported by federal and state-level regulatory mandates and capital investment programs.

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates