Resources

About Us

Environmental Compliance Software Market by Component (Software, Services), Deployment Mode (Cloud-based, On-premise), Application Organization Size, and End-use Industry— Global Forecast to 2036

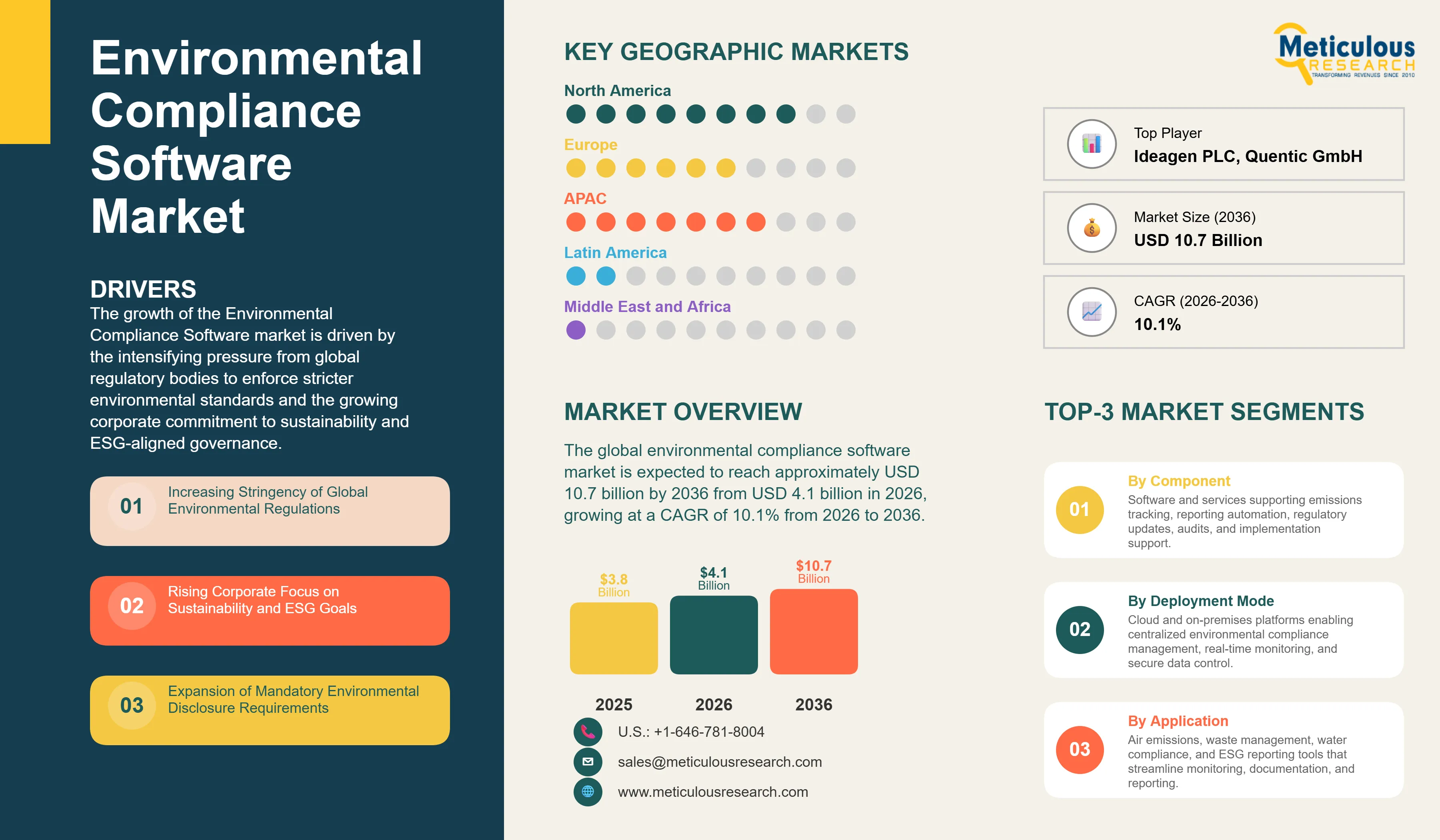

Report ID: MRICT - 1041806 Pages: 290 Feb-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global environmental compliance software market was valued at USD 3.8 billion in 2025. The market is expected to reach approximately USD 10.7 billion by 2036 from USD 4.1 billion in 2026, growing at a CAGR of 10.1% from 2026 to 2036. The growth of the overall market is driven by the intensifying pressure from global regulatory bodies to enforce stricter environmental standards and the growing corporate commitment to sustainability and ESG-aligned governance. As organizations across heavily regulated industries seek to automate compliance tracking, streamline environmental reporting, and reduce the risk of regulatory penalties, environmental compliance software has become a mission-critical tool for managing operational accountability. The rapid expansion of mandatory emissions disclosure frameworks, the increasing complexity of multi-jurisdictional environmental laws, and the widespread integration of AI-driven risk analytics and IoT-enabled monitoring continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Environmental compliance software refers to purpose-built digital platforms that help organizations systematically manage their obligations under environmental laws, regulations, and reporting standards. These solutions provide integrated tools for tracking environmental performance data, automating compliance workflows, managing permits and licenses, conducting audits and inspections, and generating structured reports for submission to regulatory authorities. The market is defined by platforms that combine regulatory intelligence databases, real-time monitoring capabilities, and data analytics to provide organizations with a proactive, rather than reactive, approach to environmental compliance management.

The market includes a wide range of solutions, from standalone emissions tracking and waste management modules designed for single-facility operations to comprehensive, cloud-native platforms that integrate environmental compliance into a broader environmental, health, safety, and quality (EHSQ) management ecosystem. These systems are increasingly being connected with IoT sensors, enterprise resource planning (ERP) systems, and AI-powered analytics engines to enable continuous monitoring of environmental parameters, automated incident detection, and predictive risk assessment. Leading platforms such as Cority's CorityOne, Sphera's SpheraCloud, and Enablon's suite of EHSQ modules are increasingly designed to cover the full compliance lifecycle, from data collection and regulatory mapping to audit management and board-level sustainability disclosures.

The global regulatory landscape is evolving at an unprecedented pace. Frameworks such as the EU's Corporate Sustainability Reporting Directive (CSRD), the U.S. Securities and Exchange Commission's (SEC) climate-related disclosure rules, and the continued expansion of the EU Emissions Trading System (EU ETS) are compelling organizations to formalize their environmental reporting processes and invest in robust compliance infrastructure. At the same time, growing investor and consumer scrutiny of corporate environmental performance is reinforcing the business case for environmental compliance software beyond mere regulatory obligation. Organizations that have traditionally relied on manual spreadsheet-based processes are rapidly transitioning to digital platforms to meet the speed, accuracy, and auditability demands of modern environmental governance.

AI-Powered Regulatory Intelligence and Predictive Compliance Analytics

Software vendors across the industry are rapidly embedding AI and machine learning capabilities into their environmental compliance platforms, shifting organizations from manual, rule-based compliance tracking toward intelligent, predictive governance systems. Cority's recent integration of machine learning to automatically map regulatory standards to operational activities and Intelex's launch of AI-powered analytics for predictive risk and compliance management represent the broader industry shift toward automated regulatory intelligence. These advances allow compliance teams to identify gaps in real time, model compliance risk scenarios, and trigger corrective actions before regulatory violations occur. The convergence of AI with large structured regulatory databases — covering thousands of environmental statutes across dozens of jurisdictions — is making comprehensive, multi-site compliance management practical and cost-effective even for globally distributed organizations.

Expansion of ESG Reporting and Carbon Management Capabilities

The rapid formalization of ESG reporting obligations is fundamentally reshaping the environmental compliance software market, as vendors invest heavily in carbon accounting, Scope 1, 2, and 3 emissions tracking, and sustainability disclosure modules. VelocityEHS released a new ESG reporting suite in early 2025 that brings together carbon accounting, climate-risk modeling, and resource efficiency tracking in a single cloud-based environment. Cority's recent acquisitions of Greenstone and Reporting 21 reflect a broader strategy to build integrated ESG data management capabilities alongside traditional compliance functions. These developments are making environmental compliance platforms the natural home for sustainability reporting processes that were previously managed through fragmented third-party tools. The growing alignment of compliance software with disclosure frameworks such as the TCFD, GRI, and CSRD is accelerating platform consolidation and driving organizations toward unified EHSQ and ESG management ecosystems.

IoT Integration and Real-Time Environmental Monitoring

Growing demand for continuous, site-level environmental monitoring is driving deep integration between compliance software platforms and industrial IoT sensors and connected monitoring instruments. Collaborations such as the one between VelocityEHS and Honeywell — which expands real-time site monitoring through integration with Honeywell's industrial sensor and analytics devices — reflect a market-wide trend toward always-on compliance infrastructure. These integrations allow organizations in emissions-intensive sectors such as oil & gas, chemicals, and utilities to monitor air quality, water discharge, and hazardous material handling continuously, replacing periodic manual sampling with automated, audit-ready data streams. The ability to connect real-time operational data to regulatory thresholds and automated alerts is transforming environmental compliance from a periodic reporting exercise into a continuous operational discipline.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 10.7 Billion |

|

Market Size in 2026 |

USD 4.1 Billion |

|

Market Size in 2025 |

USD 3.8 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 10.1% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Deployment Mode, Application, Organization Size, End-use Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Tightening Global Environmental Regulations and Mandatory Disclosure Requirements

A key driver of the environmental compliance software market is the accelerating pace of environmental regulatory reform across major economies. The EU's Corporate Sustainability Reporting Directive, which substantially widens the scope and frequency of mandatory environmental disclosures for large and mid-sized companies, is compelling European multinationals to automate compliance workflows that were previously handled manually. In the United States, the EPA continues to update and enforce standards under the Clean Air Act, the Clean Water Act, and the Resource Conservation and Recovery Act (RCRA), each demanding precise, auditable data management that organizations increasingly rely on compliance software to deliver. Regulatory obligations governing greenhouse gas emissions, hazardous waste disposal, wastewater treatment, and air quality monitoring are growing more complex and more strictly enforced simultaneously — a combination that is making investment in dedicated environmental compliance platforms a financial and operational necessity rather than an optional efficiency measure.

Opportunity: ESG-Driven Investment and Supply Chain Environmental Due Diligence

The growing emphasis on ESG performance as a factor in investment decisions, credit ratings, and procurement requirements is creating significant growth opportunities for the environmental compliance software market. Institutional investors and major procurement organizations are increasingly requiring their portfolio companies and suppliers to demonstrate measurable environmental compliance standards, driving demand for software platforms that can centralize, standardize, and externally communicate environmental performance data. The development of supply chain due diligence regulations, including the EU's Corporate Sustainability Due Diligence Directive, is extending environmental compliance obligations beyond a company's direct operations to encompass their upstream and downstream value chains. This expansion creates compelling demand for platforms that can integrate supplier data, automate third-party compliance assessments, and generate structured reports aligned with international environmental standards — requirements that leading software vendors are actively building into their product roadmaps.

Why Does the Software Segment Lead the Market?

The software segment accounts for the largest share of the global environmental compliance software market in 2026. This dominance reflects the central role of purpose-built compliance platforms in automating the collection, organization, analysis, and reporting of environmental data across complex, multi-facility operations. Organizations in regulated industries are increasingly retiring legacy spreadsheet-based processes in favor of cloud-native software platforms that offer pre-configured regulatory content, automated workflow management, and real-time performance dashboards. The depth and breadth of functionality offered by leading platforms — spanning air emissions calculations, waste tracking, permit condition monitoring, and sustainability disclosures in a single system — makes software the core investment driver for environmental compliance technology budgets.

The services segment, encompassing professional implementation services, system integration support, training, and ongoing managed services, is expected to grow at a steady pace during the forecast period. As organizations deploy increasingly complex, enterprise-grade compliance platforms, demand for specialized implementation expertise and continuous regulatory update services is growing alongside software licensing revenue.

How Does the Cloud-Based Segment Dominate?

Based on deployment mode, the cloud-based segment holds the largest share of the overall market in 2026. This is primarily due to the significant operational and economic advantages that cloud deployment offers over traditional on-premise installations, particularly for organizations managing compliance across multiple facilities or geographies. Cloud-based platforms allow vendors to push regulatory content updates — reflecting new or amended environmental statutes — directly to users without requiring disruptive software upgrades, ensuring that compliance teams always work with current regulatory requirements. The scalability of cloud infrastructure also supports the large and growing volumes of environmental monitoring data that IoT-enabled sites are generating.

The on-premise deployment segment, while declining as a share of the overall market, continues to hold relevance for organizations in sectors with specific data sovereignty requirements or stringent cybersecurity policies, such as defense-adjacent manufacturing and certain regulated utilities. However, the increasing availability of private cloud and hybrid deployment models is narrowing the functional gap between cloud-native and on-premise alternatives, further accelerating the overall shift toward cloud adoption.

Why Does the Air Emissions Management Segment Lead the Market?

The air emissions management segment commands the largest share of the global environmental compliance software market in 2026. This dominance reflects the central role of air quality and greenhouse gas regulations in shaping compliance obligations across energy, manufacturing, chemicals, and oil & gas industries. Stringent emissions reporting requirements under frameworks such as the EU ETS, the U.S. EPA's Greenhouse Gas Reporting Program (GHGRP), and equivalent national regulations in major industrial economies are driving sustained investment in software platforms that can automate emissions calculations, manage monitoring equipment calibrations, and generate regulatory submissions in jurisdiction-specific formats. Vendors such as Enviance and Sphera have built deep expertise in air emissions compliance, establishing strong market positions in this high-priority application area.

The sustainability and ESG reporting segment is expected to grow at the fastest pace during the forecast period. The convergence of mandatory ESG disclosure requirements with voluntary sustainability reporting frameworks is creating a new category of compliance software demand, as organizations seek platforms capable of managing Scope 1, 2, and 3 emissions inventories alongside traditional regulatory compliance obligations. The rapid growth of corporate net-zero commitments and the increasing expectation for third-party-assured sustainability disclosures are making ESG reporting functionality a decisive purchasing factor for large enterprise buyers.

How Does the Large Enterprise Segment Drive the Market?

The large enterprise segment holds the majority share of the global environmental compliance software market in 2026. Large organizations, with their multi-site global operations and extensive exposure to complex, overlapping environmental regulations across multiple jurisdictions, represent the most demanding and highest-value buyers in this market. The need to standardize compliance processes, consolidate environmental data from distributed operational sites, and produce harmonized reports for multiple regulatory authorities simultaneously makes purpose-built compliance software an operational necessity at enterprise scale.

The small and medium enterprise (SME) segment, however, is expected to grow at a faster rate during the forecast period, driven by the increasing availability of cloud-based subscription models that reduce the upfront investment and IT infrastructure burden traditionally associated with enterprise compliance software. The growing extension of mandatory environmental reporting obligations — particularly supply chain due diligence requirements that flow down from large corporate buyers to their smaller suppliers — is bringing compliance software adoption to a broader base of smaller organizations that were previously below the regulatory threshold for formal compliance management systems.

Why Does the Manufacturing Segment Lead the Market?

The manufacturing segment commands the largest share of the global environmental compliance software market in 2026. This position reflects the sector's broad and intensive exposure to environmental regulations spanning air emissions, wastewater discharge, hazardous waste management, and chemical inventory reporting. Manufacturers face compliance obligations under some of the most comprehensive and actively enforced bodies of environmental law globally, including the U.S. EPA's Toxics Release Inventory (TRI) reporting program, the EU's Integrated Pollution Prevention and Control (IPPC) framework, and equivalent industrial environmental permitting regimes across Asia-Pacific, Latin America, and the Middle East. The diversity of compliance obligations across different manufacturing sub-sectors — from discrete manufacturing in automotive and electronics to process manufacturing in food, beverages, and personal care — has driven demand for configurable, modular compliance platforms that can be adapted to sector-specific requirements.

The oil & gas and chemicals & petrochemicals segments are also significant contributors to overall market revenue, supported by the particularly rigorous emissions monitoring, waste management, and chemical reporting obligations that apply to these sectors. The utilities & energy segment is expected to grow steadily through 2036, fueled by the integration of renewable energy assets into national grids and the growing complexity of environmental compliance requirements associated with energy transition infrastructure, including large-scale battery storage, hydrogen production, and offshore wind development.

How is North America Maintaining Dominance in the Global Environmental Compliance Software Market?

North America holds the largest share of the global environmental compliance software market in 2026. This dominance is primarily attributed to the maturity of the U.S. environmental regulatory framework, the strong enforcement posture of the EPA, and the extensive compliance obligations imposed on manufacturing, oil & gas, chemicals, and utilities sectors that form a large part of the North American industrial base. The U.S. also benefits from the presence of several leading environmental compliance software vendors, including Cority Software Inc., VelocityEHS Holdings Inc., Benchmark Digital Partners LLC, and ERA Environmental Management Solutions, which have built their platforms in close alignment with EPA reporting formats, permit management workflows, and hazardous waste tracking requirements. Canada's own tightening environmental standards, particularly those related to greenhouse gas emissions and industrial wastewater management, further support regional market growth.

Which Factors Support Europe and Asia-Pacific Market Growth?

Europe represents a substantial and growing share of the global market, driven by the unprecedented scope of mandatory environmental reporting obligations being introduced under the CSRD, the EU Taxonomy Regulation, and the continuing expansion of the EU ETS. Countries including Germany, France, the Netherlands, and the UK are home to a large base of manufacturing, chemical, and energy companies that face demanding, overlapping environmental compliance requirements at the national and EU level. European-headquartered vendors such as Quentic GmbH and Ideagen PLC have built strong regional footholds, while global platforms from Enablon (Wolters Kluwer, Netherlands) and Sphera Solutions are increasingly orienting their regulatory content libraries around European compliance requirements.

Asia-Pacific is expected to be the fastest-growing regional market during the forecast period, supported by China's increasingly rigorous industrial pollution control regime, India's expanding environmental compliance mandate under the Ministry of Environment, Forest and Climate Change, and the growing alignment of manufacturing sectors across Southeast Asia with international environmental standards demanded by global customers and export market regulations. The large and growing industrial base across these markets, combined with rapidly rising regulatory expectations, positions Asia-Pacific as the most dynamic growth geography for environmental compliance software through 2036.

Companies such as Cority Software Inc., Enablon (Wolters Kluwer N.V.), Sphera Solutions, Inc., and Intelex Technologies ULC lead the global environmental compliance software market with comprehensive, enterprise-grade platforms that span the full range of environmental compliance, safety management, and sustainability reporting functions. Established players including VelocityEHS Holdings Inc., Benchmark Digital Partners LLC (formerly Gensuite), ETQ LLC (part of Hexagon AB), and Dakota Software Corporation focus on delivering deep functional capabilities in specific application areas such as chemical compliance, air emissions management, and regulatory audit management, serving industries from process manufacturing to oil & gas. Emerging and specialized vendors such as ERA Environmental Management Solutions, Ideagen PLC, Quentic GmbH, IsoMetrix, and ProcessMAP Corporation are strengthening the competitive landscape through innovation in AI-driven compliance analytics, mobile-first audit tools, and regulatory intelligence automation, while also expanding their geographic footprints to address the rapidly growing compliance software markets in Europe and Asia-Pacific.

The global environmental compliance software market is expected to grow from USD 4.1 billion in 2026 to USD 10.7 billion by 2036.

The global environmental compliance software market is projected to grow at a CAGR of 10.1% from 2026 to 2036.

The software segment is expected to dominate the market in 2026. The services segment is projected to grow steadily through the forecast period as demand for implementation support, system integration, and managed regulatory update services grows alongside platform adoption.

AI and IoT integration are enabling organizations to move from periodic, manual compliance reporting to continuous, automated environmental monitoring and predictive risk management. AI-powered regulatory intelligence tools automatically map changing regulatory requirements to operational activities, while IoT sensor integration enables real-time environmental performance data to flow directly into compliance dashboards — reducing manual data entry, improving data accuracy, and enabling proactive corrective action before regulatory thresholds are breached.

Cloud-based deployment holds the largest share of the global market in 2026. The scalability, lower upfront cost, and the ability to push real-time regulatory content updates directly to users make cloud-based platforms the preferred choice for organizations managing compliance across multiple facilities or geographic regions.

North America holds the largest share of the global environmental compliance software market in 2026, primarily attributed to the mature and actively enforced U.S. environmental regulatory framework, the high industrial compliance burden across manufacturing and energy sectors, and the presence of several leading software vendors headquartered in the region.

The leading companies include Cority Software Inc., Enablon (Wolters Kluwer N.V.), Sphera Solutions, Inc., Intelex Technologies ULC, VelocityEHS Holdings Inc., Benchmark Digital Partners LLC, ETQ LLC (Hexagon AB), and Dakota Software Corporation.

Published Date: Aug-2025

Published Date: Jan-2025

Published Date: Sep-2024

Published Date: Jun-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates