Resources

About Us

Electrical Substation Automation Market by Component (Hardware, Software, Services), Communication Technology (Wired, Wireless), Substation Type (Transmission Substation, Distribution Substation), Installation (New Installation, Retrofit), and End-use - Global Forecast to 2036

Report ID: MRSE - 1041749 Pages: 267 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportWhat is the Electrical Substation Automation Market Size?

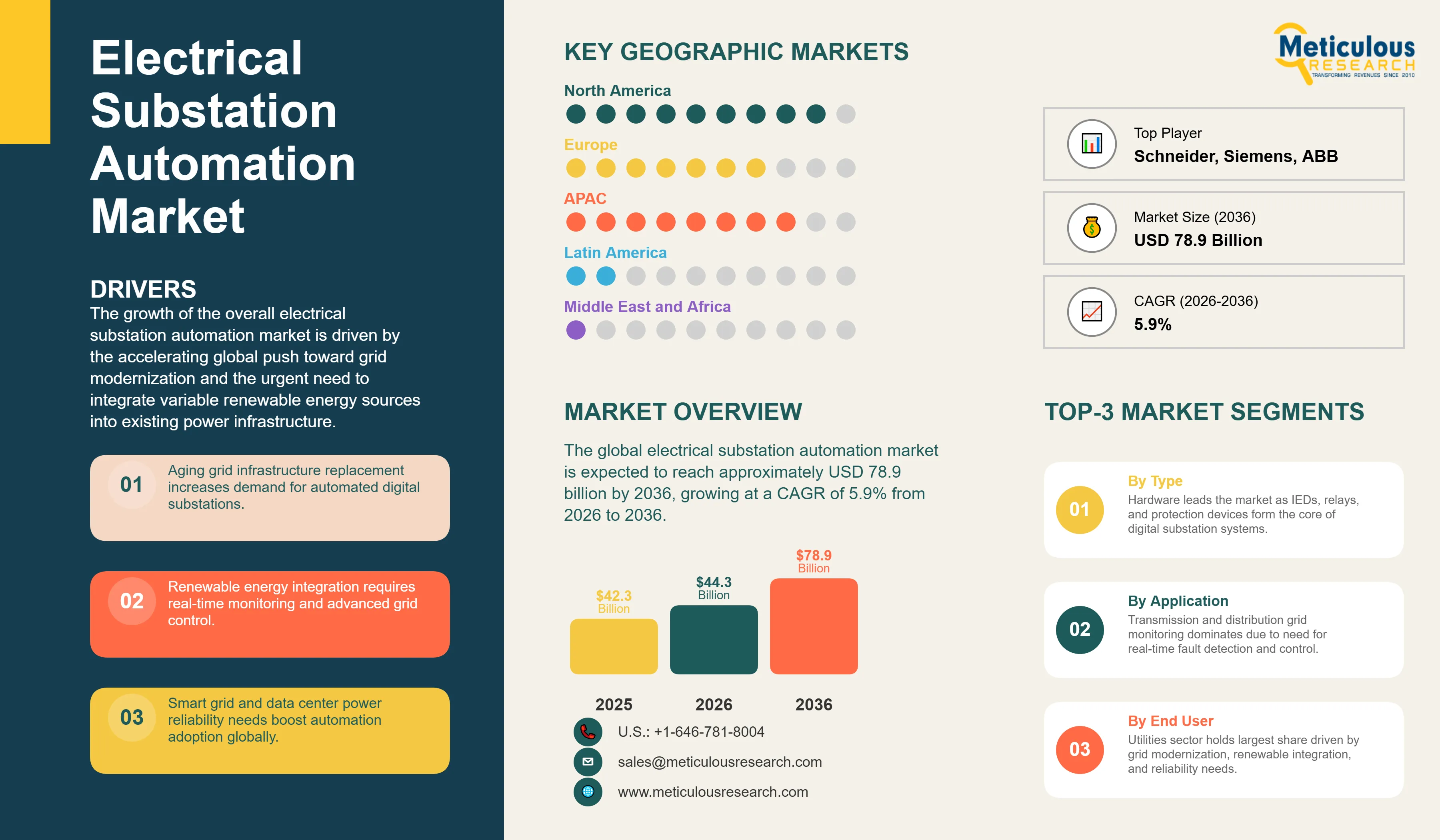

The global electrical substation automation market was valued at USD 42.3 billion in 2025. The market is expected to reach approximately USD 78.9 billion by 2036 from USD 44.3 billion in 2026, growing at a CAGR of 5.9% from 2026 to 2036. The growth of the overall electrical substation automation market is driven by the accelerating global push toward grid modernization and the urgent need to integrate variable renewable energy sources into existing power infrastructure. As utility providers transition from legacy electromechanical systems to intelligent digital platforms, substation automation has emerged as the cornerstone technology for enabling real-time monitoring, advanced fault detection, and seamless remote control capabilities. The rapid deployment of smart grid initiatives and the increasing complexity of distributed energy resources continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Electrical substation automation represents a transformative approach to managing power distribution networks through the integration of intelligent electronic devices, advanced communication protocols, and sophisticated software platforms that enable centralized monitoring and control of substation operations. These systems leverage standardized frameworks such as IEC 61850 to provide interoperable data exchange between protection relays, circuit breakers, transformers, and control units, creating a unified digital environment for optimal grid performance. The market is characterized by cutting-edge technologies including virtualized protection systems, AI-driven predictive maintenance algorithms, and process bus architectures that significantly enhance operational reliability and resource efficiency in high-stakes utility environments. These systems are essential for grid operators seeking to modernize their infrastructure and meet stringent performance and safety requirements.

The market encompasses a comprehensive range of solutions, from basic supervisory control and data acquisition platforms for distribution substations to sophisticated digital substation architectures featuring sampled values, generic object-oriented substation events, and cloud-based analytics. These systems are increasingly enhanced with advanced capabilities such as cyber-secure communication networks, real-time load forecasting, and automated fault isolation to deliver services including dynamic grid optimization and remote diagnostics of electrical assets. The ability to deliver stable, high-precision protection while enabling rapid restoration of service has made substation automation technology the preferred choice for operators where grid resilience and operational excellence are paramount.

The global energy sector is aggressively pursuing infrastructure modernization initiatives, aiming to accommodate bidirectional power flows from distributed generation and achieve ambitious decarbonization targets. This transformation has accelerated the adoption of high-performance automation solutions, with advanced digital substations helping to maintain grid stability during the integration of intermittent renewable sources. At the same time, the exponential growth in data center power consumption and the electrification of transportation are creating unprecedented demand for robust, intelligent electrical infrastructure.

Transition to IEC 61850-Based Digital Substations and Process Bus Architectures

Utilities across the industry are rapidly migrating from copper-intensive conventional designs to fiber-optic-based digital substation architectures, fundamentally transforming protection and control philosophies. Siemens' latest SICAM integrated solutions and ABB's pioneering Relion protection systems demonstrate the industry's shift toward standardized IEC 61850 communication, enabling seamless interoperability between multi-vendor intelligent electronic devices. The revolutionary advancement comes with process bus implementations that digitize voltage and current measurements at the source using optical sensors, transmitting sampled values directly to protection relays and eliminating thousands of copper wires. These innovations make high-speed peer-to-peer communication practical and cost-effective for everyone from regional distribution operators to large-scale transmission system administrators pursuing excellence in grid automation and enhanced cybersecurity.

Integration of Artificial Intelligence for Predictive Maintenance and Self-Healing Grids

Innovation in artificial intelligence algorithms and machine learning analytics is rapidly driving the substation automation market, as asset management strategies become more proactive and grid operations more autonomous. Technology providers like Schneider Electric and General Electric are now deploying platforms that combine the power of real-time data analysis with the intelligence of neural network-based anomaly detection in unified systems, enabling utilities to predict equipment failures weeks in advance and optimize maintenance schedules. These systems often incorporate advanced digital twin technologies and cloud-based analytics capable of processing terabytes of operational data without compromising system security or regulatory compliance.

At the same time, growing emphasis on grid resilience is pushing operators to develop substation automation solutions tailored to autonomous decision-making and rapid fault recovery principles. These systems support self-healing capabilities through automated reconfiguration algorithms and intelligent load transfer mechanisms. By combining high-density data processing performance with sophisticated control logic, these emerging architectures enable both technological advancement and operational excellence, strengthening the resilience of critical energy infrastructure against evolving threats.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 78.9 Billion |

|

Market Size in 2026 |

USD 44.3 Billion |

|

Market Size in 2025 |

USD 42.3 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 5.9% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Communication Technology, Substation Type, Installation, End-use, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Aging Grid Infrastructure and Renewable Energy Integration Mandates

A key driver of the electrical substation automation market is the critical need to replace obsolete electromechanical infrastructure that was never designed to handle current load demands or accommodate bidirectional power flows from distributed generation. Global momentum toward sustainable energy systems, real-time fault detection, and data-driven grid management has created compelling incentives for the deployment of intelligent substation infrastructure. The convergence of variable renewable generation and the modernization of transmission networks drives utilities toward scalable automation solutions that only advanced digital platforms can reliably deliver. It is estimated that as renewable capacity additions accelerate and grid complexity intensifies through 2036, the demand for sophisticated, interoperable automation systems increases exponentially; therefore, high-performance SCADA platforms and IEC 61850-compliant intelligent electronic devices, with their proven ability to manage complex operational workflows, are considered essential enablers of next-generation grid reliability and efficiency.

Opportunity: Data Center Expansion and Critical Infrastructure Protection

The exponential growth of hyperscale data centers and mission-critical facilities presents exceptional opportunities for the electrical substation automation market. Indeed, the global surge in artificial intelligence computing deployments has generated unprecedented demand for systems capable of delivering ultra-reliable power with millisecond-level fault response times and comprehensive real-time monitoring. These applications require absolute uptime guarantees, advanced cybersecurity protocols, and the capability to process high-bandwidth operational telemetry, all attributes that are uniquely addressed by state-of-the-art substation automation solutions. The data center infrastructure market is set to expand dramatically through 2036, with automated substations positioned for substantial growth as operators prioritize resilience and operational visibility. Furthermore, the increasing focus on infrastructure protection and the deployment of microgrids for critical facilities is stimulating demand for modular automation architectures that provide flexible integration and advanced control capabilities.

Why Does the Hardware Segment Lead the Market?

The hardware segment accounts for a significant portion of the overall electrical substation automation market in 2026. This is primarily attributed to the fundamental role of intelligent electronic devices in enabling protection, control, and monitoring functions within modern digital substations. These systems represent the physical foundation ensuring operational integrity across diverse voltage applications. The utilities and industrial sectors alone consume a substantial share of hardware deployments, with major modernization projects in North America and Asia-Pacific demonstrating the technology's capability to support high-density automation requirements and stringent reliability standards. However, the software segment is expected to grow at a rapid CAGR during the forecast period, driven by the increasing need for advanced analytics platforms, cloud-based monitoring solutions, and sophisticated human-machine interfaces in complex grid transformation initiatives.

How Does the Wired Communication Segment Dominate?

Based on communication technology, the wired segment holds the largest share of the overall market in 2026. This is primarily due to the proven reliability of fiber-optic and Ethernet-based networks and the rigorous performance requirements for mission-critical substation communication infrastructure. Current large-scale deployment strategies are increasingly specifying high-bandwidth fiber-optic platforms to ensure compliance with stringent latency standards and cybersecurity expectations for dependable grid operation environments.

The wireless communication segment is expected to witness substantial growth during the forecast period. The evolution toward distributed automation architectures and the complexity of integrating remote monitoring points are driving the requirement for advanced wireless systems capable of supporting mobile workforce applications and temporary installation scenarios while maintaining secure connectivity for operational data transmission.

Why Does the Utilities Segment Lead the Market?

The utilities segment commands the largest share of the global electrical substation automation market in 2026. This dominance stems from its critical responsibility for operating vast transmission and distribution networks, renewable energy interconnections, and bulk power delivery systems, making it the primary end-use sector for comprehensive substation automation. Large-scale modernization programs in grid infrastructure, renewable integration projects, and regulatory compliance initiatives drive sustained demand, with advanced platforms from providers like Hitachi Energy and Schweitzer Engineering Laboratories enabling reliable performance in complex utility environments.

However, the industrial segment is positioned for steady growth through 2036, fueled by expanding manufacturing automation, mining operations, and heavy process industries requiring dedicated electrical infrastructure. Industrial facilities face mounting pressure to enhance power quality and implement predictive maintenance for high-value production lines, where automated substations provide cost-effective solutions for sophisticated electrical management and operational continuity.

How is North America Maintaining Dominance in the Global Electrical Substation Automation Market?

North America holds the largest share of the global electrical substation automation market in 2026. The largest share of this region is primarily attributed to the substantial government funding for grid modernization and the presence of leading technology innovators, particularly in the United States. The United States alone accounts for a significant portion of global substation automation investment, with federal infrastructure programs and utility commitments to digital transformation driving sustained market expansion. The presence of industry leaders like General Electric and Schweitzer Engineering Laboratories combined with a well-established ecosystem of system integrators provides a robust foundation for both conventional upgrades and cutting-edge digital deployments.

Which Factors Support Asia-Pacific and Europe Market Growth?

Asia-Pacific and Europe together represent substantial growth opportunities in the global electrical substation automation market. The expansion of these markets is mainly driven by aggressive infrastructure development and renewable energy integration mandates. The demand for advanced automation systems in Asia-Pacific is predominantly fueled by massive grid expansion projects in China and India, alongside smart city initiatives in Southeast Asian nations.

In Europe, the leadership in sustainable energy policy and the commitment to carbon neutrality targets are accelerating the adoption of intelligent grid solutions. Countries like Germany, France, and the United Kingdom are at the forefront, with significant investments in integrating distributed renewable generation into sophisticated automation frameworks and deploying advanced protection systems to ensure the highest levels of grid stability and operational performance.

The companies such as ABB Ltd., Siemens AG, Schneider Electric SE, and General Electric Company lead the global electrical substation automation market with comprehensive portfolios of hardware, software, and integration services, particularly for large-scale utility applications and complex industrial installations. Meanwhile, players including Hitachi Energy Ltd., Eaton Corporation plc, Honeywell International Inc., and Cisco Systems, Inc. focus on specialized communication infrastructure, cybersecurity solutions, and advanced analytics platforms targeting critical infrastructure and digital transformation initiatives. Emerging manufacturers and technology providers such as Schweitzer Engineering Laboratories, Inc., NR Electric Co., Ltd., Larsen & Toubro Limited, and Emerson Electric Co. are strengthening the market through innovations in intelligent electronic devices, protection relays, and integrated automation architectures.

he global electrical substation automation market is expected to grow from USD 44.3 billion in 2026 to USD 78.9 billion by 2036.

The global electrical substation automation market is projected to grow at a CAGR of 5.9% from 2026 to 2036.

Hardware is expected to dominate the market in 2026 due to its fundamental role in enabling protection and control functions within digital substations. However, the software segment is projected to be the fastest-growing segment owing to increasing demand for advanced analytics, cloud-based platforms, and sophisticated monitoring solutions.

IEC 61850 and digital substations are transforming the automation landscape by enabling standardized interoperability, eliminating proprietary protocols, and supporting advanced process bus architectures. These technologies drive the adoption of fiber-optic communication networks and sampled value transmission, enabling utilities to achieve unprecedented levels of operational flexibility and cybersecurity while reducing engineering complexity and infrastructure footprint.

North America holds the largest share of the global electrical substation automation market in 2026. The largest share of this region is primarily attributed to substantial government infrastructure funding and the presence of leading technology providers.

The leading companies include ABB Ltd., Siemens AG, Schneider Electric SE, General Electric Company, and Hitachi Energy Ltd.

Published Date: Jun-2026

Published Date: May-2024

Published Date: Apr-2022

Published Date: Mar-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates