Resources

About Us

Pharmaceutical Automation Market Size, Share, Forecast, & Trends Analysis by Offering (Solutions and Services), Mode of Automation (Semi-automatic Systems and Fully Automatic Systems), End User (Pharmaceutical Industry and Biotech Industry), & Geography – Global Forecast to 2036

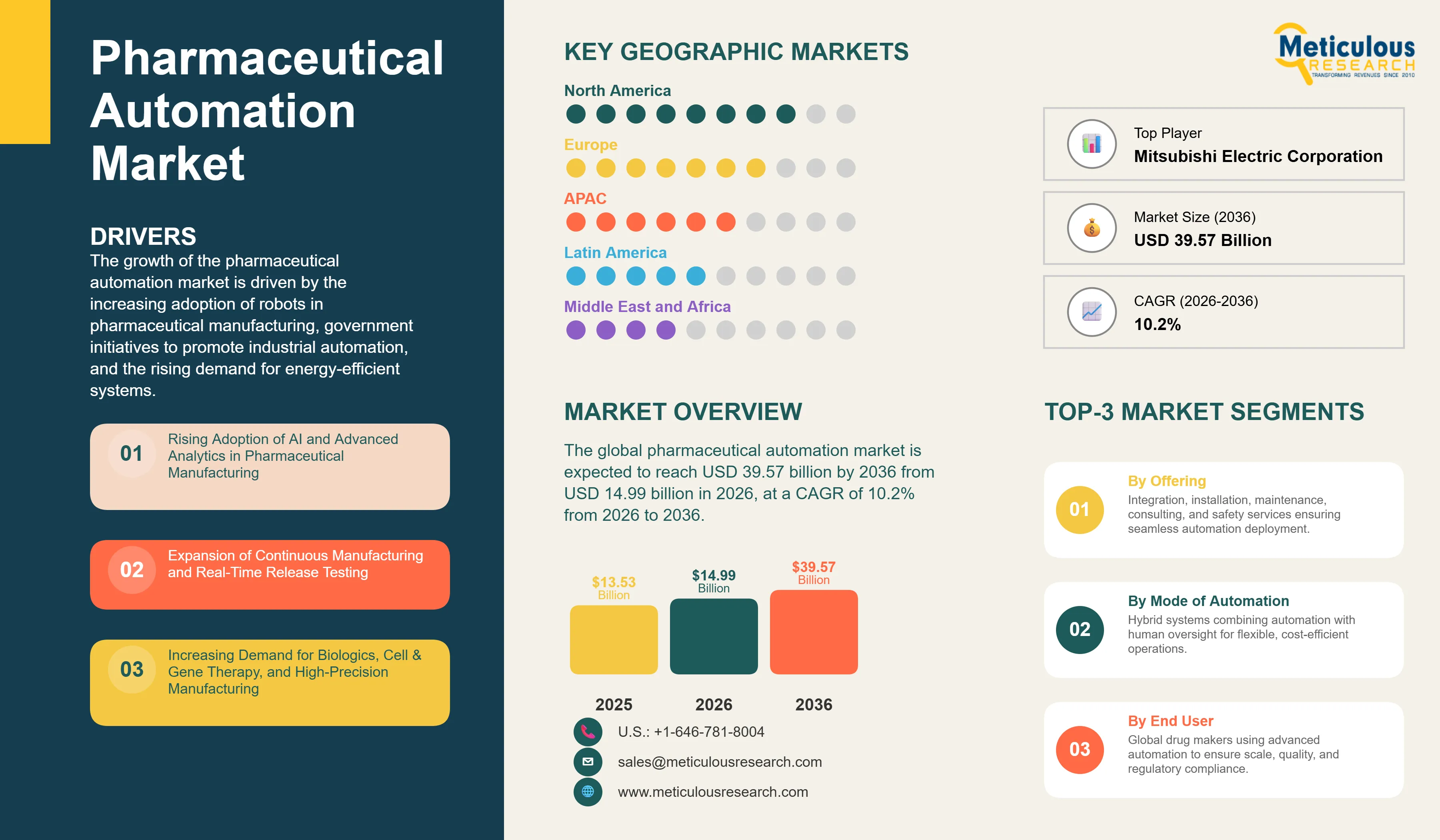

Report ID: MRSE - 104594 Pages: 330 Mar-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global pharmaceutical automation market was valued at USD 13.53 billion in 2025. This market is expected to reach USD 39.57 billion by 2036 from USD 14.99 billion in 2026, at a CAGR of 10.2% from 2026 to 2036.

The growth of the pharmaceutical automation market is driven by the increasing adoption of robots in pharmaceutical manufacturing, government initiatives to promote industrial automation, and the rising demand for energy-efficient systems. The combination of Pharma 4.0 technologies, encompassing artificial intelligence, machine learning, Industrial Internet of Things (IIoT), digital twins, and advanced robotics, with pharmaceutical manufacturing processes is fundamentally transforming how pharmaceutical and biotech companies design, operate, and optimize their production environments. AI algorithms are increasingly being applied in pharmaceutical automation to analyze large manufacturing datasets, predict process outcomes, enable real-time release testing, and streamline quality control workflows. Siemens AG, for instance, leveraged its Digital Process Twin technology at Johnson & Johnson Innovative Medicine in Belgium, achieving 35% reductions in switch time and total development costs while cutting solvent consumption by 30%.

Rising global demand for pharmaceuticals, driven by aging populations, the growing prevalence of chronic diseases, accelerating biopharmaceutical drug development, and the continued expansion of generic and biosimilar manufacturing, is necessitating significantly higher production throughput and the stringent quality assurance that automated systems uniquely deliver. Furthermore, the rising demand for IIoT in pharmaceutical manufacturing is expected to generate substantial growth opportunities for market players throughout the forecast period.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The pharmaceutical automation market encompasses the hardware, software, and services that enable automated control, monitoring, and execution of processes across pharmaceutical manufacturing, quality control, laboratory operations, packaging, and supply chain management. Key solution categories within this market include enterprise-level controls (ERP, PLM, and MES platforms), plant instrumentation (industrial robots, sensors, machine vision systems, motors & drives), and plant-level controls (SCADA, DCS, and PLC systems). The market serves two primary end-user segments: the pharmaceutical industry, encompassing manufacturers of prescription drugs, generics, OTC medications, and active pharmaceutical ingredients (APIs); and the biotech industry, encompassing manufacturers of biopharmaceuticals, monoclonal antibodies, cell and gene therapies, and other biological products.

Accelerating Integration of AI and Digital Twin Technologies in Pharmaceutical Manufacturing

The increasing integration of artificial intelligence (AI), machine learning (ML), and digital twin technologies into pharmaceutical manufacturing systems is a major technology trend driving the pharmaceutical automation market. AI and ML algorithms are increasingly deployed across pharmaceutical production environments to analyze real-time process data from sensors and control systems, predict deviations, optimize critical process parameters, and support continuous process verification models aligned with regulatory expectations.

Digital twin technology, enabling the creation of virtual replicas of physical manufacturing processes and facilities, allows pharmaceutical manufacturers to simulate, test, and optimize processes prior to physical deployment. This approach reduces engineering complexity, shortens technology transfer timelines, and improves process robustness. Major automation providers, including Siemens and Rockwell Automation, have expanded pharmaceutical-focused digitalization platforms such as AI-enabled MES, SCADA, and DCS systems to deliver real-time manufacturing intelligence that supports both operational excellence and compliance objectives.

Growing Adoption of Collaborative Robots (Cobots) in Cleanroom and Sterile Manufacturing

The growing adoption of collaborative robots (cobots) alongside traditional industrial robots is another key trend in pharmaceutical automation. Unlike conventional industrial robots that require safety enclosures and segregation from personnel, cobots are designed to operate safely in proximity to human workers, making them particularly suitable for pharmaceutical cleanroom and sterile environments.

Cobots are increasingly deployed for applications such as sterile compounding, vial and syringe handling, labeling and inspection, material transfer within controlled environments, and quality control sample preparation. The adoption of collaborative robotic systems is driven by the need to improve workplace safety, address skilled labor shortages, enhance sterility assurance, and increase process efficiency in complex pharmaceutical operations.

While traditional articulated and SCARA robots continue to account for the majority of robotic installations in pharmaceutical manufacturing, mainly in packaging and high-speed material handling, collaborative robotic systems are projected to grow faster as pharmaceutical manufacturers seek greater flexibility and human-machine integration in production workflows.

The global pharmaceutical automation market was valued at USD 13.53 billion in 2025. This market is expected to reach USD 39.57 billion by 2036 from USD 14.99 billion in 2026, at a CAGR of 10.2% from 2026 to 2036.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 39.57 Billion |

|

Market Size in 2025 |

USD 13.53 Billion |

|

Market Size in 2026 |

USD 14.99 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 10.2% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Offering: Solutions (Enterprise-level Controls [PLM, ERP, MES], Plant Instrumentation [Robots, Sensors, Machine Vision Systems, Motors & Drives, Relays & Switches], Plant-level Controls [SCADA, DCS, PLC]) and Services (Integration & Installation, Maintenance & Support, Advisory/Training/Consulting, Safety & Security) By Mode of Automation: Semi-automatic Systems, Fully Automatic Systems By End User: Large Pharmaceutical Manufacturers, CDMOs, Biotech By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Why Does the Solutions Segment Dominate the Pharmaceutical Automation Market?

Based on offering, the solutions segment is expected to account for the largest share of the global pharmaceutical automation market in 2026. This is primarily attributed to the increasing demand for comprehensive automation solutions to ensure high-quality and reliable pharmaceutical manufacturing, the rising need for real-time monitoring and predictive maintenance capabilities, and the growing need for operational efficiency while reducing operational costs and unplanned downtime. Within the solutions segment, plant instrumentation, encompassing robots, sensors, machine vision systems, motors & drives, and relays & switches, represents the largest sub-segment, driven by the accelerating adoption of robotics across pharmaceutical production environments. Plant-level controls (SCADA, DCS, PLC) and enterprise-level controls (ERP, PLM, MES) collectively form the software and control intelligence layer of pharmaceutical automation, with MES platforms such as Rockwell Automation’s PharmaSuite enabling production operations management for regulatory compliance and operational excellence.

The solutions segment is also projected to grow at the fastest CAGR during the forecast period, driven by continuous advancement of AI-powered automation solutions for pharmaceutical processes. The services segment, comprising integration & installation, maintenance & support, advisory/training/consulting, and safety & security services, while representing a smaller market share, is critical to enabling successful deployment and sustained operation of pharmaceutical automation solutions and represents a growing revenue stream for automation vendors as the installed base expands.

Why Does the Semi-automatic Systems Segment Dominate the Pharmaceutical Automation Market?

Based on mode of automation, the semi-automatic systems segment is expected to account for the largest share of the global pharmaceutical automation market in 2026. This is mainly due to the effectiveness of these systems in streamlining pharmaceutical manufacturing processes while retaining human oversight, a balance that is essential for maintaining quality control in pharmaceutical manufacturing, where human judgment, exception handling, and operator expertise remain important complements to automated process execution. Semi-automatic systems offer a more accessible entry point for pharmaceutical manufacturers transitioning from manual to automated operations, with lower initial CAPEX requirements and simpler regulatory validation compared to fully automatic systems.

However, the fully automatic systems segment is projected to grow at the fastest CAGR during the forecast period, driven by the increasing adoption of fully automatic systems by large-scale pharmaceutical companies seeking to maximize throughput through the complete automation of feeding, assembly, filling, packaging, and inspection processes. The growing investment in automated cell culture bioreactors, automated sterile filling lines, and continuous manufacturing platforms in the biopharmaceutical industry is a key driver of the growth in adoption of the fully automatic systems.

Why Do Large Pharmaceutical Manufacturers Dominate the Pharmaceutical Automation Market?

Based on end user, large pharmaceutical manufacturers are expected to account for the largest share of the global pharmaceutical automation market in 2026. This dominance is primarily attributed to the scale and complexity of their global manufacturing operations, which require advanced automation to ensure consistent product quality, regulatory compliance, and operational efficiency.

Stringent regulatory frameworks, including cGMP requirements and inspection standards set by agencies such as the U.S. FDA and the European Medicines Agency (EMA), necessitate robust process control, data integrity, and traceability across pharmaceutical production facilities. As a result, large pharmaceutical companies are increasingly deploying automation platforms incorporating distributed control systems (DCS), manufacturing execution systems (MES), robotics, machine vision, spectroscopy, and chromatography-based inspection technologies to detect defects, impurities, and process deviations in real time.

In addition, the integration of artificial intelligence (AI) and advanced analytics into manufacturing environments enables predictive maintenance, automated deviation detection, and optimization of critical process parameters. These capabilities support continuous process verification and real-time release testing, which are becoming increasingly important in modern pharmaceutical manufacturing.

Large pharmaceutical manufacturers are also investing heavily in automation to support expanding portfolios that include specialty drugs, biologics, and personalized medicine, all of which require highly controlled and flexible production systems.

Growing Automation Demand Among CDMOs and Advanced Therapy Companies

Contract development and manufacturing organizations (CDMOs) is a rapidly growing end-user segment, driven by the outsourcing of drug development and manufacturing activities by both large pharmaceutical and emerging biotech companies. CDMOs must maintain high levels of automation to ensure multi-client production flexibility, regulatory compliance, and efficient batch changeovers across diverse product portfolios.

Biotechnology and advanced therapy companies, including manufacturers of monoclonal antibodies, antibody-drug conjugates (ADCs), cell and gene therapies, and mRNA-based products, are also experiencing strong demand for automation. These manufacturing environments require precise environmental control, sterile processing capabilities, and advanced process monitoring systems. The increasing commercialization of biologics and advanced therapies is therefore driving demand for modular, flexible, and highly automated cleanroom-grade manufacturing solutions.

Based on geography, Europe is expected to account for the largest share of the global pharmaceutical automation market in 2026. The large share of this region is driven by its highly developed pharmaceutical manufacturing ecosystem, with major production hubs in Germany, Switzerland, Italy, France, Belgium, Ireland, the U.K., and the Netherlands. The strong adoption of Industry 4.0 and Pharma 4.0 technologies, including process analytical technology (PAT), real-time monitoring systems, and advanced manufacturing control platforms, continues to drive automation investments across pharmaceutical facilities in the region.

In addition, technological advancements in artificial intelligence, robotics, digitalization, and continuous manufacturing, combined with EU-level and national initiatives promoting industrial digital transformation, are further strengthening position of Europe in the global pharmaceutical automation market. The presence of major automation vendors headquartered in the region, including Siemens AG (Germany), Schneider Electric SE (France), and ABB Ltd (Switzerland), also strengthens collaboration between automation providers and leading pharmaceutical manufacturers.

Asia-Pacific, on the other hand, is projected to register the highest CAGR during the forecast period, driven by the rapid expansion and modernization of pharmaceutical manufacturing facilities across China, India, Japan, South Korea, and Singapore. Increasing investments in advanced automation technologies, rising domestic and export pharmaceutical production, and government-backed initiatives to strengthen manufacturing competitiveness are accelerating the adoption of automation solutions. China’s efforts to align manufacturing standards with international GMP requirements, India’s Production Linked Incentive (PLI) scheme supporting pharmaceutical manufacturing expansion, and Japan’s broader digital transformation agenda are collectively driving regional growth.

North America ranks among the leading regional markets, driven by the concentration of major pharmaceutical and biotechnology companies and automation vendors such as Rockwell Automation, Honeywell, Emerson Electric, and GE Vernova (formerly GE industrial segments). The highly regulated manufacturing environment and emphasis on data integrity and compliance continue to drive steady demand for advanced automation solutions in the region.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by leading market participants in the pharmaceutical automation market between 2023 and 2026. The key players profiled in the pharmaceutical automation market report include Siemens AG (Germany), Emerson Electric Co. (U.S.), Mitsubishi Electric Corporation (Japan), ABB Ltd (Switzerland), FANUC CORPORATION (Japan), Honeywell International Inc. (U.S.), KUKA AG (Germany), Schneider Electric SE (France), Rockwell Automation, Inc. (U.S.), YASKAWA Electric Corporation (Japan), Yokogawa Electric Corporation (Japan), OMRON Corporation (Japan), Advantech Co., Ltd. (Taiwan), Fuji Electric Co., Ltd. (Japan), and Syntegon Technology GmbH (Germany), among others.

Pharmaceutical Automation Market, by Offering

The global pharmaceutical automation market is projected to reach USD 39.57 billion by 2036 from USD 14.99 billion in 2026, at a CAGR of 10.2% during the forecast period from 2026 to 2036.

In 2026, the solutions segment is expected to account for the largest share of the pharmaceutical automation market. This dominance is driven by strong demand for integrated automation platforms, including distributed control systems (DCS), manufacturing execution systems (MES), robotics, plant instrumentation, and enterprise-level control solutions.

The growth of the pharmaceutical automation market is driven by increasing adoption of robotics and advanced control systems, government initiatives promoting industrial digitalization, rising demand for high-quality and energy-efficient manufacturing systems, and stricter regulatory compliance requirements. Furthermore, the accelerating adoption of Industrial Internet of Things (IIoT) solutions and Pharma 4.0 frameworks integrating AI, digital twins, and connected automation systems is expected to create significant growth opportunities for market participants.

Major companies operating in the pharmaceutical automation market include Siemens AG (Germany), Emerson Electric Co. (U.S.), Mitsubishi Electric Corporation (Japan), ABB Ltd (Switzerland), FANUC CORPORATION (Japan), Honeywell International Inc. (U.S.), KUKA AG (Germany), Schneider Electric SE (France), Rockwell Automation, Inc. (U.S.), YASKAWA Electric Corporation (Japan), Yokogawa Electric Corporation (Japan), OMRON Corporation (Japan), Advantech Co., Ltd. (Taiwan), Fuji Electric Co., Ltd. (Japan), and Syntegon Technology GmbH (Germany), among others.

Europe is expected to account for the largest share of the global pharmaceutical automation market during the forecast period, driven by its advanced pharmaceutical manufacturing infrastructure, widespread adoption of Industry 4.0 technologies, strong implementation of process analytical technologies (PAT), and supportive industrial digitalization policies.

Asia-Pacific is projected to register the highest CAGR during the forecast period, supported by the rapid modernization of pharmaceutical manufacturing facilities in China, India, Japan, and South Korea, increasing investments in advanced automation technologies, and expanding pharmaceutical production capacity across the region.

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates