Resources

About Us

Electric Industrial Kilns Market by Type (Box Kilns, Chamber Kilns, Tunnel Kilns, Rotary Kilns), Heating Technology (Resistance Heating, Induction Heating, Arc Heating), Application (Ceramics, Metallurgy, Glass), and End-use Vertical - Global Forecast to 2036

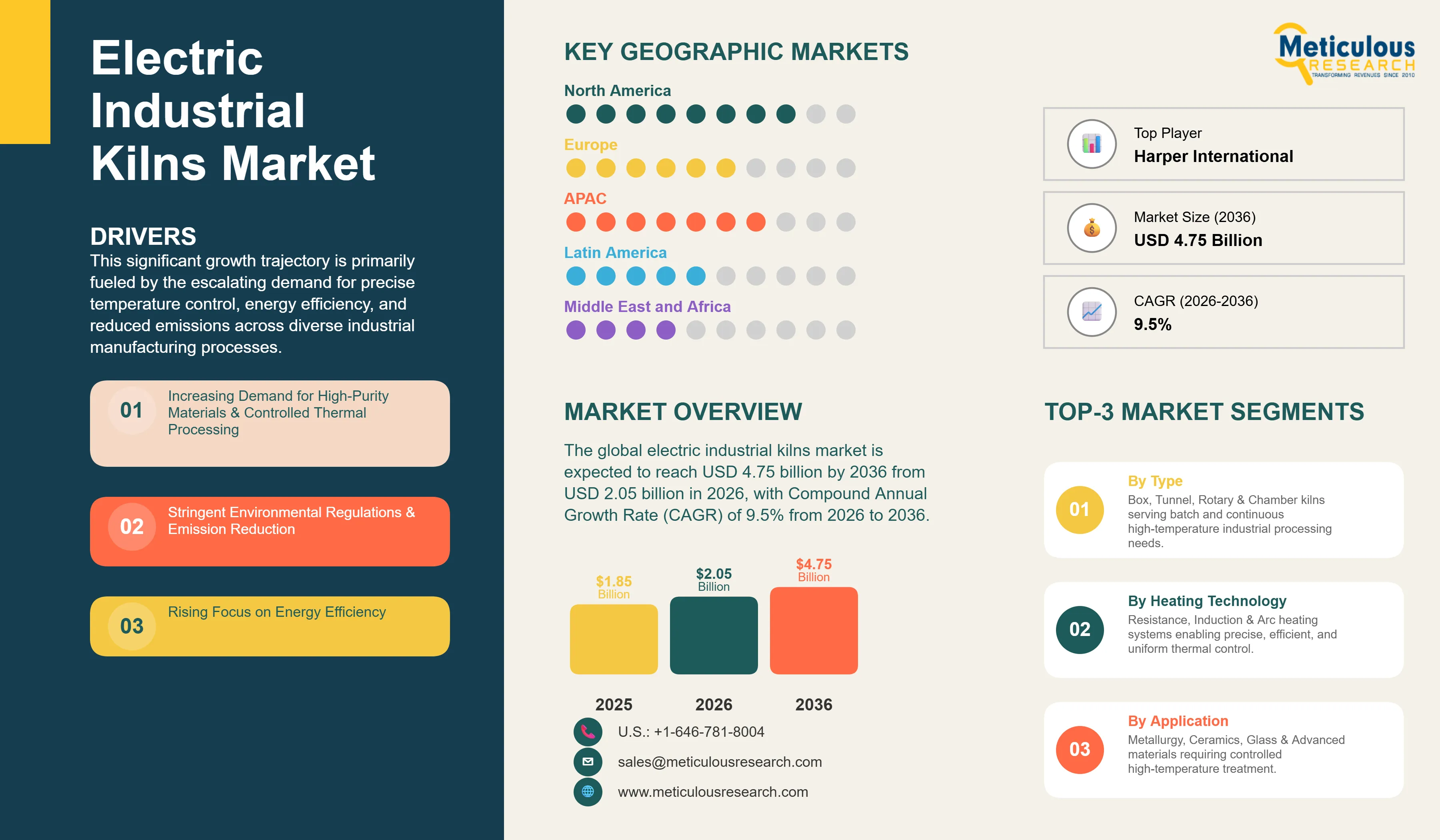

Report ID: MRHC - 1041819 Pages: 295 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global electric industrial kilns market was valued at USD 1.85 billion in 2025.This market is expected to reach USD 4.75 billion by 2036 from USD 2.05 billion in 2026, demonstrating a robust Compound Annual Growth Rate (CAGR) of 9.5% from 2026 to 2036. This significant growth trajectory is primarily fueled by the escalating demand for precise temperature control, energy efficiency, and reduced emissions across diverse industrial manufacturing processes. Key drivers include stringent environmental regulations pushing for the adoption of cleaner heating technologies, the rapid expansion of advanced materials production requiring highly controlled thermal processing, and the increasing automation in industrial settings. Furthermore, continuous advancements in heating element materials, sophisticated control systems, and the seamless integration of Industry 4.0 technologies are collectively enhancing the efficacy and market appeal of electric industrial kilns worldwide.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Electric industrial kilns represent a sophisticated class of thermal processing systems engineered to meticulously provide high-temperature environments for various industrial applications through electrical energy. This mechanism leverages specialized heating technologies, commonly resistance, induction, or arc heating, to achieve precise and controlled temperature profiles. Distinct from fuel-fired kilns, which rely on combustion, electric kilns excel in environments characterized by the need for clean operation, minimal emissions, and exceptionally accurate temperature regulation. These systems are indispensable for meticulously regulating temperatures within sensitive industrial operations, thereby mitigating material contamination, ensuring product consistency, and preserving the intrinsic integrity of advanced materials. The market landscape for these devices is diverse, encompassing robust box and chamber kilns tailored for extensive batch processing and agile tunnel and rotary kilns designed for continuous, high-volume production requirements.

The market is currently experiencing a dynamic phase of continuous innovation, primarily propelled by an industry-wide pursuit of superior energy efficiency, enhanced precision in control, and unwavering operational reliability. Contemporary electric industrial kilns frequently incorporate advanced heating elements boasting augmented thermal stability, sophisticated insulation materials engineered to curtail heat loss, and highly intelligent control mechanisms. These cutting-edge systems are equipped with real-time temperature sensors, advanced programmable logic controllers (PLCs), and seamless IoT connectivity, facilitating remote management, predictive maintenance, and integration into broader manufacturing execution systems (MES). Manufacturers are strategically channeling their research and development efforts towards crafting solutions that not only minimize energy consumption and reduce maintenance overheads but also feature modular designs for effortless integration into existing production lines or as standalone operational units. This emphasis on customization ensures that a broad spectrum of industrial demands can be met, ranging from the exacting standards of advanced ceramics firing to the protective requirements of specialized heat treatment processes.

The global industrial ecosystem is increasingly characterized by an imperative for stringent environmental control, driven by the need to adhere to rigorous quality benchmarks, optimize production workflows, and prolong the operational lifespan of sensitive equipment. Industries spanning ceramics, metallurgy, glass, and advanced materials necessitate exceptionally controlled thermal environments to avert product defects, mitigate safety risks, and prevent material degradation. The escalating awareness regarding the detrimental ramifications of uncontrolled heating—encompassing inconsistent product quality, increased energy consumption, and potential safety hazards—is significantly accelerating the adoption of advanced electric industrial kiln solutions. This burgeoning recognition of electric industrial kilns as a foundational component of modern manufacturing infrastructure is firmly establishing their indispensable role in contemporary industrial operations.

The electric industrial kilns market is currently undergoing a transformative shift, marked by a pronounced emphasis on energy-efficient solutions and the strategic development of sustainable operational practices. This evolution is a direct response to escalating energy costs, increasingly stringent environmental regulations, and a pervasive drive towards corporate sustainability. Industrial entities are actively seeking thermal processing technologies that not only minimize energy consumption but also reduce their ecological footprint, all while maintaining uncompromising standards of precise temperature control. This trend is catalyzing significant innovations in insulation materials, refining heat recovery systems, and fostering the integration of advanced heating element designs, which collectively lead to a substantial reduction in the energy required for high-temperature processing. Furthermore, the emergence of high-performance electric kilns offers an optimized performance envelope across a broader spectrum of industrial applications, delivering enhanced efficiency and operational flexibility, thereby positioning them as a pivotal differentiator in the competitive market landscape.

Another defining trend shaping the electric industrial kilns market is the pervasive integration of Industry 4.0 principles and advanced automation technologies, coupled with continuous advancements in control systems. This dual focus aims to deliver unparalleled precision, facilitate seamless remote management, and elevate overall system performance. Manufacturers are proactively embedding sophisticated sensors, advanced algorithmic intelligence, and robust IoT connectivity into their kiln systems. This technological synergy enables real-time data acquisition pertaining to temperature profiles, energy consumption, and the performance metrics of the kiln. The collected data is subsequently subjected to rigorous analysis via cloud-based platforms and artificial intelligence, yielding actionable insights into system efficiency, predicting impending maintenance requirements, and autonomously adjusting operational parameters to sustain optimal thermal conditions. Concurrently, intensive research and development endeavors are concentrated on engineering novel control interfaces that boast superior user-friendliness, enhanced diagnostic capabilities, and robust integration with broader manufacturing execution systems. These synergistic innovations are culminating in the creation of more compact, inherently efficient, and exceptionally reliable electric industrial kilns, adept at addressing the increasingly rigorous demands of diverse industrial applications.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 4.75 Billion |

|

Market Size in 2026 |

USD 2.05 Billion |

|

Market Size in 2025 |

USD 1.85 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 9.5% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Heating Technology, Application, End-use Vertical, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A primary driver for the electric industrial kilns market is the escalating need for high-purity materials and highly controlled thermal processing environments across a wide array of advanced manufacturing and industrial facilities. Sectors such as aerospace, electronics, medical devices, and advanced ceramics require robust heating solutions to achieve precise material properties, ensure product integrity, and meet stringent quality standards. For instance, in the ceramics industry, precise temperature ramps and soak times are crucial for achieving desired material density and strength. In the metallurgy sector, controlled heat treatment processes are essential for optimizing metal hardness and ductility. The growing complexity of industrial materials and the expansion into high-performance applications further amplify this demand. Conventional fuel-fired kilns often struggle to provide the ultra-clean and precisely controlled atmospheres required by these industries, making electric industrial kilns the preferred solution. The continuous innovation and stringent regulatory requirements in these high-value sectors are significantly fueling the demand for advanced electric industrial kiln systems.

A significant growth opportunity for electric industrial kilns lies in the rapidly expanding battery manufacturing and recycling industries, particularly for electric vehicles (EVs) and energy storage systems. The production of battery components, such as cathodes and anodes, requires highly controlled high-temperature firing processes to achieve optimal electrochemical properties. Electric kilns offer the precision, cleanliness, and scalability necessary for these critical steps, minimizing contamination and ensuring consistent product quality. As global demand for EVs and renewable energy storage surges, so too will the need for efficient and environmentally compliant battery production facilities. Furthermore, the nascent but growing battery recycling sector will increasingly rely on electric kilns for thermal treatment processes to recover valuable materials. This application is particularly critical as the world transitions towards a circular economy and invests heavily in sustainable manufacturing practices. This convergence of battery technology and sustainable industrial practices creates substantial new avenues for market expansion.

The Box Kilns segment accounts for the largest share of the overall electric industrial kilns market in 2026. This dominance is primarily driven by their versatility, ease of operation, and widespread deployment in various batch-processing applications across small to medium-scale industries. Box kilns, also known as chamber kilns, offer excellent temperature uniformity and are suitable for a broad range of materials and processes, including ceramics firing, heat treatment of metals, and laboratory applications. Their relatively lower capital cost and flexibility in handling different load sizes make them an attractive option for manufacturers requiring precise thermal processing without the need for continuous production lines. Industries such as custom ceramics, small-batch metallurgy, and research & development facilities often rely on box kilns for their reliability and adaptability.

The Tunnel Kilns segment is expected to witness steady growth during the forecast period. This growth is fueled by the increasing demand for continuous, high-volume production in industries such as structural ceramics, refractories, and advanced materials. Tunnel kilns offer superior energy efficiency and automation capabilities for large-scale operations, making them ideal for manufacturers focused on maximizing throughput and minimizing labor costs. Their ability to maintain consistent temperature profiles over long production runs makes them indispensable for high-volume thermal processing.

The Resistance Heating segment holds the largest market share in 2026. This dominance is attributed to its cost-effectiveness, reliability, and broad applicability in diverse industrial heating processes requiring uniform temperature distribution and precise control. Resistance heating elements, such as Kanthal or silicon carbide, convert electrical energy directly into heat, which is then transferred to the workload primarily through radiation and convection. This technology is highly reliable, offers excellent temperature uniformity, and can achieve a wide range of temperatures, making it the preferred choice for critical applications in ceramics firing, heat treatment of metals, and glass annealing. Continuous advancements in heating element materials and insulation technologies further reinforce its leading position, offering enhanced efficiency and longevity.

The Induction Heating segment is expected to witness significant growth during the forecast period. This growth is driven by its rapid heating capabilities, energy efficiency, and suitability for specific applications such as metal melting, brazing, and surface hardening. Induction heating offers precise and localized heating, minimizing energy waste and reducing processing times, making it increasingly attractive for specialized metallurgical applications.

The Metallurgy segment commands the largest share of the global electric industrial kilns market in 2026. This leadership stems from the extensive and critical need for precise heat treatment processes in metal production, fabrication, and component manufacturing. Electric industrial kilns are indispensable for various metallurgical applications, including annealing, tempering, hardening, sintering, and brazing, where controlled atmospheres and accurate temperature profiles are crucial for achieving desired material properties. The automotive, aerospace, and machinery manufacturing industries rely heavily on these processes to produce high-strength, durable metal components. The stringent quality requirements and the high value of metallic products drive the adoption of high-performance electric kilns in this sector.

The Ceramics segment is expected to grow at a significant CAGR during the forecast period. The increasing demand for advanced ceramics in electronics, medical, and industrial applications, coupled with the need for precise firing processes to achieve superior material characteristics, is fueling the growth of electric kilns in this sector.

The Automotive sector is expected to account for a substantial share of the overall electric industrial kilns market in 2026. This is primarily due to the critical role of electric kilns in the manufacturing of various automotive components, particularly for heat treatment of metal parts, production of advanced ceramics for sensors and catalytic converters, and increasingly, for the thermal processing of battery components for electric vehicles. The automotive industry’s stringent quality standards, demand for lightweight and high-strength materials, and the accelerating shift towards electrification necessitate highly precise, energy-efficient, and environmentally compliant thermal processing solutions. Electric kilns offer the controlled atmospheres and temperature uniformity essential for these applications, ensuring the reliability and performance of automotive products.

The Aerospace sector is expected to witness robust growth during the forecast period. The demand for high-performance materials, such as advanced composites and superalloys, which require highly specialized and precise thermal processing in electric kilns, is a key driver. The stringent safety and performance requirements in aerospace manufacturing further amplify the need for reliable electric kiln solutions.

The global electric industrial kilns market is expected to grow from USD 2.05 billion in 2026 to USD 4.75 billion by 2036.

The global electric industrial kilns market is projected to grow at a CAGR of 9.5% from 2026 to 2036.

Box Kilns are expected to dominate the market due to their versatility and widespread use in batch processing. The Tunnel Kilns segment is projected to grow rapidly, driven by increasing demand for continuous, high-volume production.

Resistance Heating will be a primary driver for market growth due to its cost-effectiveness, reliability, and broad applicability. Induction Heating is also expected to see significant growth due to its rapid and precise heating capabilities for specialized metallurgical applications.

The Metallurgy segment is expected to hold the largest market share, driven by the critical need for precise heat treatment processes in metal production and fabrication. The Ceramics segment will also see substantial growth due to increasing demand for advanced ceramics.

The Automotive sector is expected to hold a substantial market share, driven by the critical role of electric kilns in component manufacturing and the shift towards electric vehicles. The Aerospace sector will also witness robust growth due to demand for high-performance materials.

Asia-Pacific holds the largest share of the global market in 2026. This dominance is primarily driven by its accelerated industrialization, burgeoning manufacturing sectors, and significant investments in advanced materials production across key economies like China and India.

The leading companies include Nabertherm GmbH, Carbolite Gero Ltd., Harper International, L&L Kiln Mfg., Inc., Cress Manufacturing Company, JPW Industrial Ovens & Furnaces, Paragon Industries, L.P., Thermcraft, Inc., Keith Company, Sentro Tech Corporation, Deltech, Inc., CM Furnaces, Inc., Lucifer Furnaces, Inc., T-M Vacuum Products, Inc., and Vulcan Electric Company.

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates