Resources

About Us

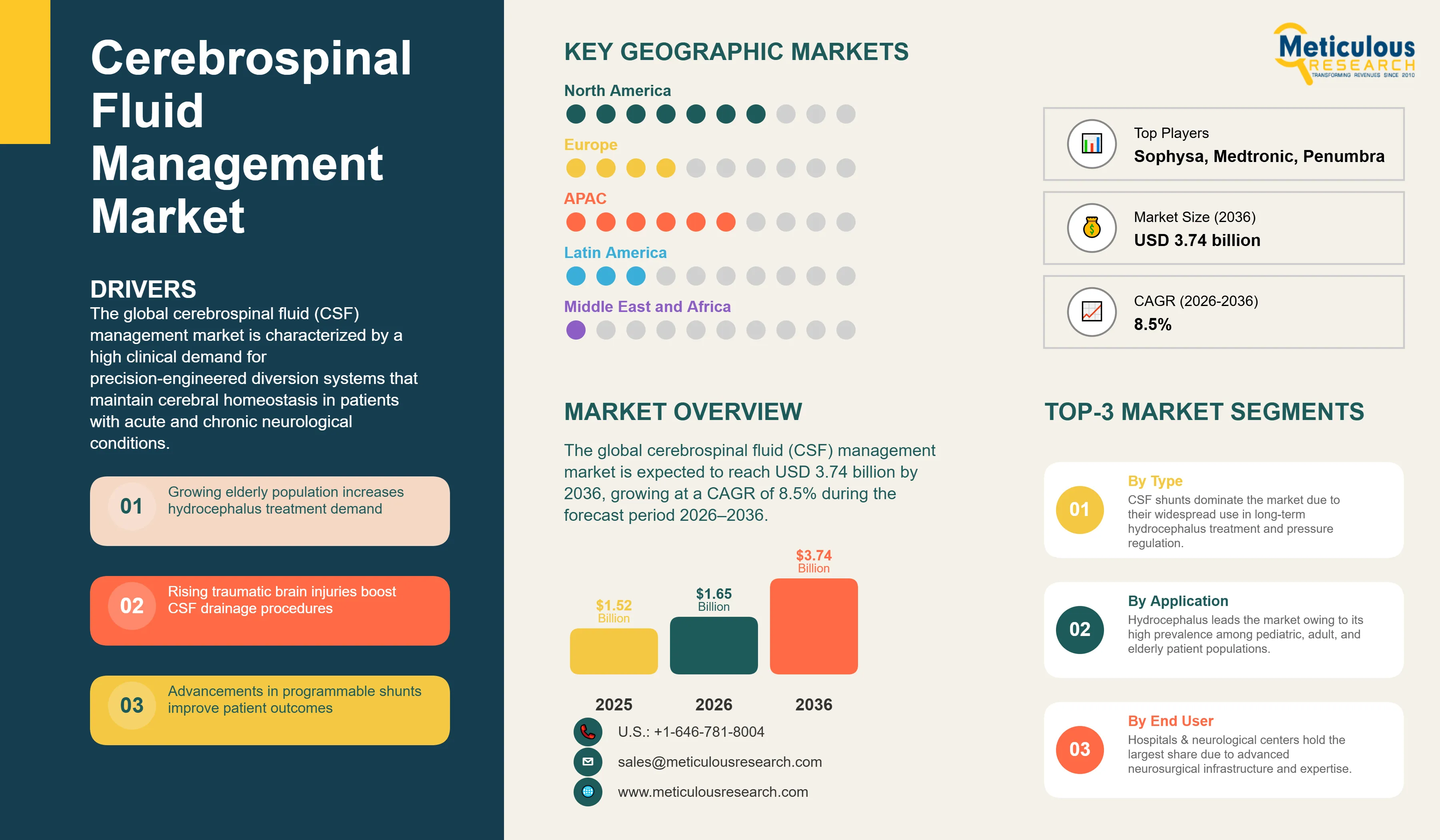

Cerebrospinal Fluid Management Market Size, Share & Trends Analysis by Product Type, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

Report ID: MRHC - 1042070 Pages: 275 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global cerebrospinal fluid (CSF) management market is estimated to be USD 1.65 billion in 2026. This market is expected to reach USD 3.74 billion by 2036, growing at a CAGR of 8.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global cerebrospinal fluid (CSF) management market is characterized by a high clinical demand for precision-engineered diversion systems that maintain cerebral homeostasis in patients with acute and chronic neurological conditions. As a critical component of neurosurgical care, CSF management involves the use of sophisticated shunts and drainage systems to alleviate intracranial pressure and prevent secondary neurological damage. The market is primarily driven by the high global prevalence of hydrocephalus, particularly Normal Pressure Hydrocephalus (NPH) in the aging population, which necessitates long-term management through ventriculoperitoneal and ventriculoatrial shunting. Additionally, the rising incidence of traumatic brain injuries (TBI) and subarachnoid hemorrhages (SAH) is accelerating the adoption of external ventricular and lumbar drainage systems in neurocritical care settings. Technological advancements, such as antimicrobial-impregnated catheters and programmable valve systems, are significantly enhancing the safety and efficacy of CSF diversion, reducing the incidence of shunt failure and infection. Clinical guidelines from the American Association of Neurological Surgeons (AANS) and the European Association of Neurosurgical Societies (EANS) continue to emphasize the importance of standardized CSF management protocols. As the industry focuses on developing minimally invasive implantation techniques and integrated pressure monitoring solutions, the market is expected to witness sustained growth, particularly in emerging economies where specialized neurosurgical infrastructure is rapidly expanding, ensuring consistent market expansion through 2036.

The growth of the global cerebrospinal fluid management market is primarily driven by the increasing prevalence of chronic neurological conditions in the elderly and the rising incidence of acute brain injuries worldwide.

Rising Prevalence of Normal Pressure Hydrocephalus in the Rapidly Aging Global Population

A major driver for the market is the rising prevalence of Normal Pressure Hydrocephalus (NPH) among the elderly, a demographic that is expanding rapidly across the globe. According to the United Nations, the global population aged 65 years and older is projected to increase from approximately 857 million in 2021 to nearly 1.6 billion by 2050, significantly increasing the prevalence of age-related neurological disorders. Studies indicate that Normal Pressure Hydrocephalus affects approximately 0.2–2.9% of adults aged 65 years and older, with prevalence increasing substantially among individuals over the age of 80. NPH often presents with symptoms that can be managed effectively through cerebrospinal fluid (CSF) shunting, leading to growing procedure volumes in developed healthcare markets. Furthermore, increasing clinical awareness and improved diagnostic capabilities are facilitating earlier differentiation of NPH from other neurodegenerative disorders such as Alzheimer's disease and Parkinsonism, supporting timely surgical intervention. This demographic shift is expected to sustain long-term demand for CSF shunting systems, particularly across North America, Europe, and rapidly aging Asia-Pacific countries.

Increasing Global Burden of Traumatic Brain Injuries and Subarachnoid Hemorrhages

The market is significantly driven by the increasing global burden of traumatic brain injuries (TBI) and subarachnoid hemorrhages (SAH), which often require acute cerebrospinal fluid (CSF) diversion to manage life-threatening intracranial hypertension. According to the World Health Organization, road traffic injuries cause approximately 1.19 million deaths annually worldwide, while traumatic brain injury remains one of the leading causes of death and disability among young adults. Furthermore, global epidemiological studies estimate that approximately 27–69 million people sustain a traumatic brain injury each year, creating substantial demand for neurocritical care interventions. Stroke also remains a major contributor to neurological emergencies, with the Global Burden of Disease (GBD) study reporting approximately 12 million new stroke cases annually worldwide. Clinical protocols emphasizing aggressive intracranial pressure management during the acute phase of neurological injury are driving the adoption of external ventricular drainage (EVD) and lumbar drainage systems equipped with advanced monitoring capabilities. This growing burden of neurological trauma and stroke is expected to support continued expansion of the CSF drainage market within neuro-ICU settings.

Despite its clinical necessity, the cerebrospinal fluid management market faces challenges related to the technical limitations of shunting systems and the potential for severe procedural complications.

Persistent Challenges Related to Shunt Obstruction, Disconnection, and Mechanical Failure

A major restraint for the market is the relatively high rate of shunt failure, which often necessitates multiple revision surgeries over a patient's lifetime. Shunt obstruction due to choroid plexus ingrowth, mechanical disconnection, and valve malfunction remain significant clinical challenges that impact long-term patient outcomes. These failures not only increase the financial burden on healthcare systems but also lead to patient and clinician dissatisfaction. The inherent technical complexity of maintaining a permanent diversion pathway in the body over decades is a persistent hurdle that manufacturers are working to overcome through improved material science and valve design.

Risks of Bacterial Meningitis and Ventriculitis Associated with CSF Diversion Procedures

The market is also impacted by the risks of post-procedural infections, such as bacterial meningitis and ventriculitis, which are serious complications of CSF shunting and external drainage. Infections can lead to prolonged hospital stays, increased morbidity, and the need for device removal and replacement. While the development of antimicrobial-impregnated catheters has helped mitigate these risks, the potential for infection remains a primary concern for neurosurgeons. This risk profile necessitates strict adherence to sterile protocols and can restrain the broader adoption of CSF diversion in facilities without specialized neurosurgical support, particularly in resource-limited settings.

Future growth opportunities in the cerebrospinal fluid management market are centered on the development of smart shunting systems and the expansion of specialized neurosurgical services in developing regions.

Development of Advanced Programmable Valves and Integrated Wireless Pressure Monitoring Systems

There is a significant opportunity for market growth driven by the development of more sophisticated programmable valve systems that allow for non-invasive pressure adjustments. Innovations in wireless pressure monitoring integrated directly into the shunt or drainage system are providing clinicians with real-time data on diversion efficacy, potentially reducing the need for diagnostic imaging and revision surgeries. Manufacturers that can provide 'smart' shunting solutions that offer personalized pressure management are well-positioned to lead the premium market segment. This trend toward digitalization and personalization in neurosurgery represents a high-growth opportunity for industry leaders.

Rapid Expansion of Specialized Neurosurgical Centers and Trauma Infrastructure in the APAC Region

The rapid expansion of specialized neurosurgical centers and trauma infrastructure in the Asia-Pacific region represents a major opportunity. Countries like China and India are making significant investments in specialized hospitals to address the rising burden of neurological conditions and trauma. Government initiatives to improve healthcare access and the growing middle class with higher disposable income are accelerating the demand for high-quality CSF management devices. Manufacturers that can provide cost-effective yet reliable diversion systems tailored for these markets are likely to lead the next phase of global market expansion, capitalizing on the high volume of procedures in these populous regions.

Growing Clinical Preference for Antimicrobial-Impregnated and Heparin-Coated Diversion Catheters

A prominent trend in 2026 is the growing clinical preference for antimicrobial-impregnated and heparin-coated diversion catheters to reduce the incidence of procedural infections and catheter-related thrombosis. These advanced materials are becoming the standard of care in many neuro-ICUs, particularly for external ventricular drainage where the risk of infection is highest. Manufacturers are increasingly focusing on incorporating these protective coatings into their entire product lines, aligning with the global clinical emphasis on improving patient safety and reducing healthcare-associated infections (HAIs) in neurosurgical settings.

Shift Toward Minimally Invasive Shunt Placement and the Use of Neuronavigation Systems

The market is witnessing an increasing trend toward the use of minimally invasive techniques for shunt placement, often supported by neuronavigation and intraoperative imaging systems. This approach aims to improve the precision of catheter placement and reduce procedural trauma, potentially leading to lower failure rates and shorter hospital stays. The integration of robotic assistance and advanced visualization tools is further enhancing the ability of neurosurgeons to perform complex diversion procedures with greater accuracy. This trend is driving the demand for specialized neurosurgical instruments and compatible diversion systems that can be easily integrated into digital operating rooms.

Analysis by Product Type

Based on product type, the CSF shunts segment is expected to hold the largest share of the global cerebrospinal fluid management market in 2026. This leadership is substantiated by its status as the primary long-term treatment for hydrocephalus, a chronic condition with a high global prevalence. The consistent demand for initial implantations and subsequent revision surgeries ensures its dominant market position. However, the CSF drainage systems segment is projected to register the highest CAGR during the forecast period. The rising incidence of traumatic brain injuries and strokes, combined with the increasing clinical emphasis on acute intracranial pressure management in neuro-ICUs, is driving the rapid adoption of external drainage technologies.

Analysis by Application

By application, the hydrocephalus segment is expected to hold the largest share in 2026, due to its high prevalence across pediatric and geriatric populations and the chronic nature of the condition requiring long-term management. However, the traumatic brain injury (TBI) & subarachnoid hemorrhage (SAH) segment is projected to register the highest CAGR during the forecast period. The rising global incidence of road traffic accidents and the expansion of specialized trauma care services are significantly accelerating the demand for acute CSF management in these acute neurological trauma cases.

Analysis by End User

By end user, the hospitals & neurological centers segment is expected to hold the largest share in 2026, as these facilities possess the specialized neurosurgical infrastructure and intensive care teams required for CSF diversion procedures. However, the specialty clinics & ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward specialized outpatient neurosurgical care and the increasing volume of routine shunt revisions being performed in ASCs are facilitating rapid growth in this segment.

Largest Share: North America

North America is expected to dominate the global cerebrospinal fluid management market in 2026. This leading position is attributed to its highly advanced neurosurgical infrastructure, high healthcare expenditure, and robust reimbursement policies. The region has a high awareness of Normal Pressure Hydrocephalus (NPH) among the elderly, driving significant procedure volumes. Data from the Hydrocephalus Association highlights the high prevalence of NPH in the U.S. elderly population, which is a major factor driving the high market valuation and the consistent demand for premium shunting systems in the U.S. and Canada.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global cerebrospinal fluid management market, with a CAGR of 7-8% during the forecast period. This rapid expansion is driven by the rapidly aging population in countries like Japan and China, increasing healthcare investments, and the rising burden of road traffic accidents. Government initiatives to improve neurosurgical care and the expansion of specialized hospitals are accelerating the demand for CSF management devices. Reports from the World Health Organization (WHO) and regional health ministries indicate a significant increase in neurosurgical procedure volumes across APAC, directly translating into higher procurement of shunts and drainage systems.

The global cerebrospinal fluid management market is characterized by a high degree of consolidation, with a few major medical technology leaders dominating the shunting and drainage segments. Competition is primarily focused on improving the long-term reliability of shunting systems and reducing procedural complications through advanced material science and valve design. Key players are investing heavily in R&D to develop programmable valves and integrated pressure monitoring solutions to capture the growing premium neurosurgery market. Strategic developments often involve acquisitions of specialized neuro-device firms and partnerships with leading academic medical centers to validate new diversion protocols. Furthermore, there is a growing focus on providing comprehensive neurocritical care solutions that integrate CSF management with other neuro-monitoring parameters. Manufacturers are also increasingly focusing on robust clinical training programs and long-term technical support to ensure the successful implementation and consistent performance of their systems in complex neurosurgical settings, which is critical for maintaining market leadership in this specialized field.

Key players operating in the global market include Medtronic plc (Ireland/US), Integra LifeSciences Corporation (US), B. Braun Melsungen AG (Germany), DePuy Synthes (Johnson & Johnson) (US), Natus Medical Incorporated (US), Sophysa (France), Spiegelberg GmbH & Co. KG (Germany), Möller Medical GmbH (Germany), Christoph Miethke GmbH & Co. KG (Germany), Dispomedica GmbH (Germany), Wellong Instruments Co., Ltd. (China), G. Surgiwear Ltd. (India), Yushin Medical Co., Ltd. (South Korea), Arkis BioSciences (acquired by Integra LifeSciences) (US), Hogy Medical Co., Ltd. (Japan), Bayer AG (Medrad Division) (Germany), Smiths Medical (acquired by ICU Medical) (US), Terumo Corporation (Japan), Minnetronix Medical (US), and Penumbra, Inc. (US). These companies focus on product innovation, strategic collaborations, acquisitions, and geographic expansion to strengthen their market presence and enhance their product portfolios.

The global market is estimated at USD 1.65 billion in 2026, with a projected growth to USD 3.74 billion by 2036, at a CAGR of 8.5%.

Primary drivers include the rising prevalence of hydrocephalus in the aging population and the increasing incidence of traumatic brain injuries.

Major restraints include the high rate of shunt failures requiring revision surgery and the risks of post-procedural infections.

Opportunities lie in the development of programmable valve technologies and the expansion of neurosurgical care in the APAC region.

CSF shunts are expected to hold the largest share as they are the primary long-term treatment for chronic hydrocephalus.

CSF drainage systems are projected to grow at the fastest CAGR, driven by the rising incidence of acute neurological trauma.

Hydrocephalus is expected to hold the largest share due to its high prevalence across all age groups and its chronic nature.

North America is expected to dominate the market due to its advanced neurosurgical infrastructure and high awareness of NPH.

Asia-Pacific is projected to witness the fastest growth, fueled by a rapidly aging population and increasing healthcare investments.

Key trends include the increasing adoption of antimicrobial-impregnated catheters and the shift toward minimally invasive shunt placement.

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates