Resources

About Us

Biosimulation Market by Product & Service (Software, Services), Application (Drug Development, Drug Discovery, Personalized Medicine, Others), and End User (Pharmaceutical & Biotechnology Companies, CROs, Academic & Research Institutes) – Global Forecast to 2036

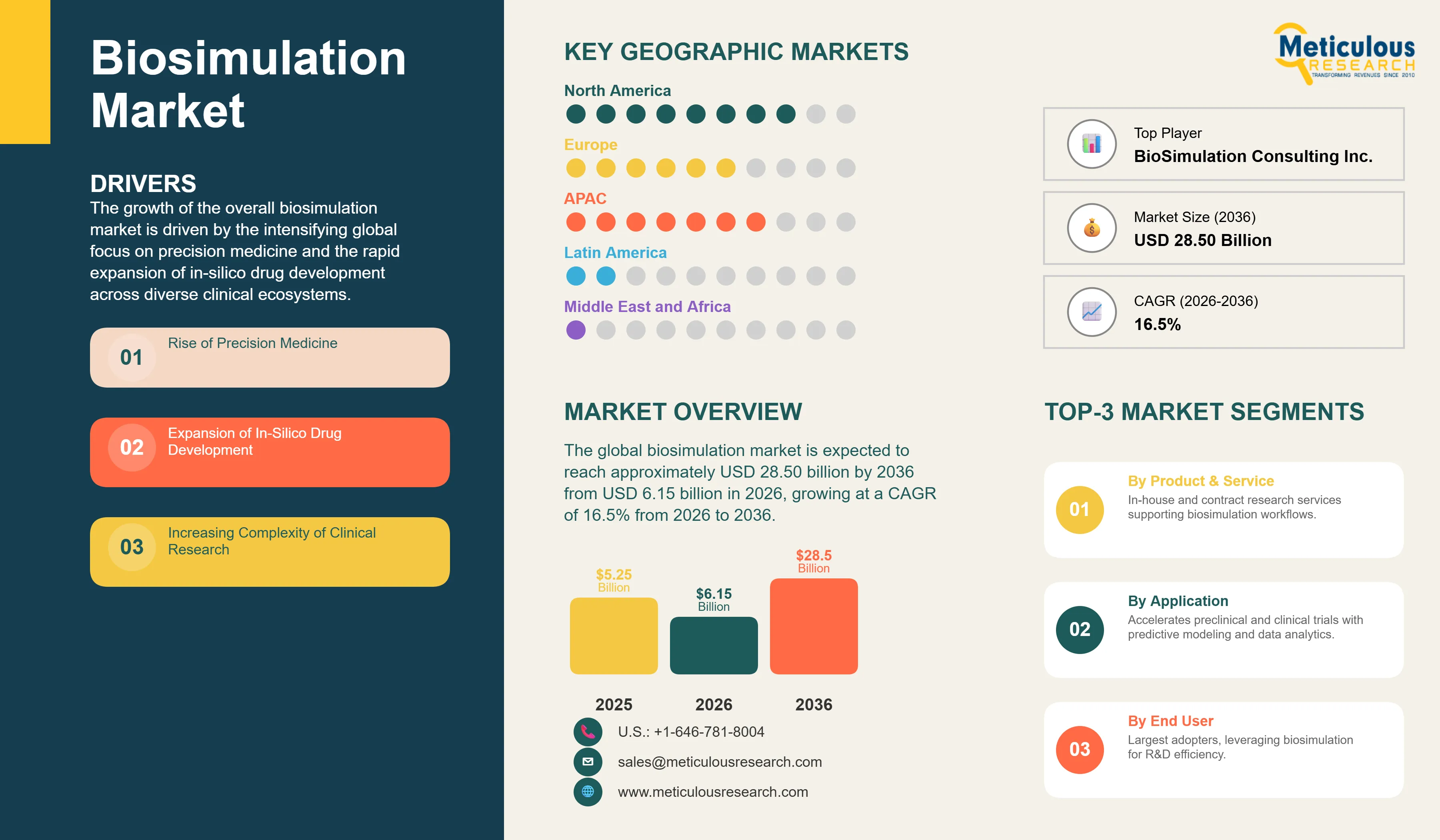

Report ID: MRHC - 1041757 Pages: 278 Feb-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global biosimulation market was valued at USD 5.25 billion in 2025. The market is expected to reach approximately USD 28.50 billion by 2036 from USD 6.15 billion in 2026, growing at a CAGR of 16.5% from 2026 to 2036. The growth of the overall biosimulation market is driven by the intensifying global focus on precision medicine and the rapid expansion of in-silico drug development across diverse clinical ecosystems. As pharmaceutical providers seek to integrate more intelligence into their R&D architectures and address the increasing demand for reduced trial costs and accelerated time-to-market, advanced biosimulation platforms have become essential for maintaining computational efficiency and predictive accuracy. The rapid expansion of artificial intelligence (AI) and the increasing need for high-performance pharmacokinetic and pharmacodynamic modeling continue to fuel significant growth of this market across all major geographic regions.

In terms of revenue, the global biosimulation market is projected to reach USD 28.50 billion by 2036

The market is expected to grow at a CAGR of 16.5% from 2026 to 2036.

North America dominates the global biosimulation market with the largest market share in 2026, driven by massive investments in biotech R&D and the presence of leading technology innovators in the United States and Canada.

Asia-Pacific is expected to witness the fastest growth during the forecast period, supported by aggressive digital transformation initiatives and the rapid adoption of advanced clinical services in China, India, and Japan.

By product & service, the software segment holds the largest market share in 2026, particularly in supporting molecular modeling and trial design in diverse research environments.

By application, the drug development segment holds the largest market share in 2026, due to its proven efficacy in handling high-volume clinical data and providing scalable, predictive results for regulatory submissions.

By end user, the pharmaceutical & biotechnology companies segment holds the largest share of the overall market in 2026.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Biosimulation systems represent critical digital frameworks used to provide high-dimensional biological data storage while allowing for efficient predictive modeling and trial management throughout the drug lifecycle. These systems include specialized algorithms such as PBPK and PK/PD modeling, which are designed to withstand high-frequency computational usage and fit into diverse machine learning ecosystems. The market is defined by high-efficiency modules such as real-time toxicity prediction and automated lead optimization protocols, which significantly enhance research precision and system durability in complex clinical applications. These systems are indispensable for developers seeking to optimize their internal research architecture and meet aggressive model performance targets.

The market includes a diverse range of solutions, ranging from simple molecular modeling libraries for basic research to complex multilayer management systems for high-performance global enterprises and professional clinical services. These systems are increasingly integrated with advanced components such as digital twin capabilities and AI-powered data sharding to provide services such as patient-specific response prediction and improved trial stability. The ability to provide stable, high-precision results while minimizing computational downtime has made advanced biosimulation technology the choice for industries where data intelligence and scalability are paramount.

The global technology sector is pushing hard to modernize clinical capabilities, aiming to meet AI-driven automation and hyper-connected intelligence targets. This drive has increased the adoption of high-density software platforms, with advanced data analytics techniques helping to stabilize predictive yields for ultra-fine biological architectures. At the same time, the rapid growth in the personalized medicine and professional utility markets is increasing the need for high-reliability, clinically-proven data management solutions.

Proliferation of Digital Twins and AI Integration

Manufacturers across the software industry are rapidly shifting to data-optimized architectures, moving well beyond traditional statistical designs toward high-speed, low-latency predictive setups. Certara’s latest Simcyp platforms deliver significantly higher simulation efficiency for biotech startups, while Simulations Plus’s recent updates have slashed operational costs in commercial trials. The real game-changer comes with “smart” modeling featuring integrated digital twin capabilities that maintain peak performance even in data-heavy clinical environments. These advancements make high-precision data management practical and cost-effective for everyone from clinical researchers to global technology giants chasing operational excellence and lower system weight.

Innovation in Cloud-Native and Multi-Modal Research Platforms

Innovation in cloud-native and multi-modal research platforms is rapidly driving the biosimulation market, as management devices become more interactive and multi-functional. Equipment suppliers are now designing units that combine the structural integrity of traditional laboratory research with the versatility of virtual search in a single assembly, saving valuable architectural space and simplifying data logistics. These systems often involve advanced cloud-native and time-release data technology capable of handling ultra-fine transaction flows without compromising system security or clinical reliability.

At the same time, growing focus on data sovereignty is pushing manufacturers to develop software solutions tailored to privacy-preserving principles. These systems help reduce data exposure through efficient encryption processes and the use of adaptive digital substrates. By combining high-density data delivery with robust environmental performance, these new designs support both technological advancement and corporate data ethics, strengthening the resilience of the broader technology value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 28.50 Billion |

|

Market Size in 2026 |

USD 6.15 Billion |

|

Market Size in 2025 |

USD 5.25 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 16.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product & Service, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Precision Medicine Boom and Rise of In-Silico Trials

A key driver of the biosimulation market is the rapid movement of the global technology industry toward data-backed, highly functional clinical infrastructure. Global demand for seamless predictive access, effective model support, and trial-monitoring software systems has created significant incentives for the adoption of biosimulation products. The trend toward “intelligent” research and the integration of AI into daily digital patches drive organizations toward scalable solutions that biosimulation technology can uniquely provide. It is estimated that as developer adoption of automated routines rises and diagnostic tools become more decentralized through 2036, the need for robust, effective management platforms increases significantly; therefore, software modules and cloud-based delivery, with their ability to ensure high-density data delivery, are considered a crucial enabler of modern clinical design strategies.

Opportunity: Personalized Healthcare and Edge Intelligence Expansion

The rapid growth of the personalized healthcare market and edge computing technologies provides great opportunities for the biosimulation market. Indeed, the global surge in genomic, proteomic, and metabolic analysis has created a compelling demand for systems that can replace traditional manual testing and integrate seamlessly into digital subscription models. These applications require high reliability, data transparency, and the ability to handle high-volume transaction environments, all attributes that are met with advanced software solutions. The edge intelligence market is set to expand significantly through 2036, with biosimulation products poised for an expanding share as developers seek to maximize model loyalty and minimize data waste. Furthermore, the increasing demand for AI-driven patient stratification and virtual try-on tools is stimulating demand for modular software solutions that provide high-speed results and design flexibility.

Why Does Software Lead the Market?

The software segment accounts for a significant portion of the overall biosimulation market in 2026. This is mainly attributed to the versatile use of this technology in supporting molecular modeling and complex remote diagnostics within extremely diverse environments, such as in oncology research and neurological studies. These systems offer the most comprehensive way to ensure data integrity across diverse high-frequency applications. The pharmaceutical and biotech sectors alone consume a large share of software production, with major projects in North America and Asia Pacific demonstrating the technology’s capability to handle high-density data requirements. However, the services segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust contract research in smart cities, clinical procedures, and luxury technology systems.

How Does the Drug Development Segment Dominate?

Based on application, the drug development segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of clinical trial projects and the rigorous performance standards required for modern technology networks. Current large-scale research hubs are increasingly specifying high-density management platforms to ensure compliance with global performance standards and developer expectations for faster, visible results.

The personalized medicine segment is expected to witness steady growth during the forecast period. The shift toward secure patient data management and the complexity of specialized research suites are pushing the requirement for advanced active systems that can handle varied data types and mechanical stresses while ensuring absolute reliability for safety-critical technology systems.

Why Do Pharmaceutical & Biotechnology Companies Lead the Market?

The pharmaceutical & biotechnology companies segment commands the largest share of the global biosimulation market in 2026. This dominance stems from its superior data management capacity, data consistency, and excellent mechanical properties, making it the technology of choice for high-performance technology systems. Large-scale operations in drug discovery, trial optimization, and high-end beauty drive demand, with advanced platforms from suppliers like Certara and Simulations Plus enabling reliable performance in extreme environments. However, the CRO segment is poised for steady growth through 2036, fueled by expanding applications in commercial logistics and simple delivery formulations. Manufacturers face mounting pressure to optimize costs for high-volume, less demanding applications, where standardized software modules provide a cost-effective alternative for basic technology connectivity.

How is North America Maintaining Dominance in the Global Biosimulation Market?

North America holds the largest share of the global biosimulation market in 2026. The largest share of this region is primarily attributed to the massive investments in biotech R&D and the presence of the world’s largest technology hubs, particularly in the United States and Canada. The U.S. alone accounts for a significant portion of global software production, with its position as a leading exporter of high-end technology driving sustained growth. The presence of leading manufacturers like Certara and Simulations Plus and a well-developed technology supply chain provides a robust market for both standard and high-density software solutions.

Which Factors Support Asia-Pacific and Europe Market Growth?

Asia-Pacific and Europe together account for a substantial share of the global biosimulation market. The growth of these markets is mainly driven by the need for technological modernization in the professional, luxury, and commercial technology sectors. The demand for advanced software systems in Asia-Pacific is mainly due to its large-scale digital transformation projects and the presence of innovators like various emerging manufacturers.

In Europe, the leadership in data privacy engineering and the push for clinical innovation are driving the adoption of high-reliability technology products. Countries like Germany, the UK, and France are at the forefront, with significant focus on integrating smart software solutions into daily routines and advanced technology treatments to ensure the highest levels of performance and reliability.

The companies such as Certara, Inc., Simulations Plus, Inc., Dassault Systèmes (BIOVIA), and Schrödinger, Inc. lead the global biosimulation market with a comprehensive range of management and search solutions, particularly for large-scale clinical and high-speed technology applications. Meanwhile, players including Genedata AG, Physiomics plc, Rosa & Co. LLC, and BioSimulation Consulting Inc. focus on specialized mass-market and high-density formulations targeting the professional and commercial sectors. Emerging manufacturers and integrated players such as Aitia, VeriSIM Life, and SimBioSys are strengthening the market through innovations in hybrid search technology and modular software platforms.

The global biosimulation market is expected to grow from USD 6.15 billion in 2026 to USD 28.50 billion by 2036.

The global biosimulation market is projected to grow at a CAGR of 16.5% from 2026 to 2036.

Software is expected to dominate the market in 2026 due to its superior ability to support molecular modeling and trial diagnostics. However, services is projected to be the fastest-growing segment owing to its increasing adoption in contract research, professional services, and luxury technology where high active delivery is required.

AI and digital twins are transforming the biosimulation landscape by demanding higher data integrity, lower latency, and improved search repair. These technologies drive the adoption of advanced materials like cloud-native platforms and digital twin-compliant modules, enabling technology manufacturers to support the complex formulations and high-frequency requirements of next-generation technology products.

North America holds the largest share of the global biosimulation market in 2026. The largest share of this region is primarily attributed to the massive investments in biotech R&D and the presence of the world's largest technology hubs in the U.S. and Canada. Asia-Pacific and Europe together account for a substantial share, driven by high-end applications in professional and luxury technology.

The leading companies include Certara, Inc., Simulations Plus, Inc., Dassault Systèmes, Schrödinger, Inc., and Genedata AG.

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates