Resources

About Us

Batch Coding Machines Market Size, Share & Trends Analysis, by Product Type, Automation Level (Automatic, Semi Automatic, Manual), Application (Primary Packaging, Secondary Packaging, Tertiary Packaging), End use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

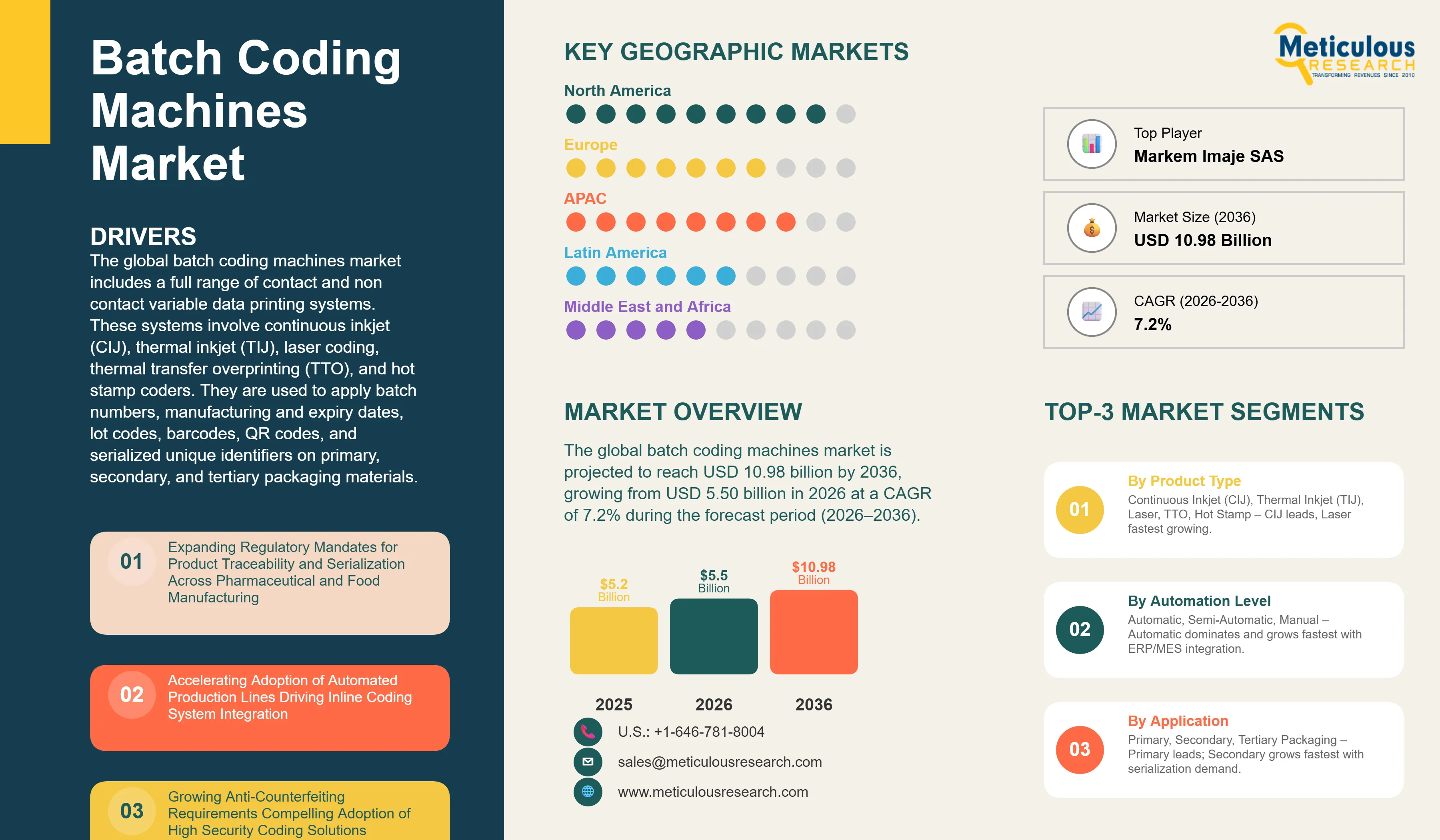

Report ID: MRCHM - 1041878 Pages: 278 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global batch coding machines market was valued at USD 5.20 billion in 2025. The market is projected to reach USD 10.98 billion by 2036, growing from USD 5.50 billion in 2026 at a CAGR of 7.2% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global batch coding machines market includes a full range of contact and non contact variable data printing systems. These systems involve continuous inkjet (CIJ), thermal inkjet (TIJ), laser coding, thermal transfer overprinting (TTO), and hot stamp coders. They are used to apply batch numbers, manufacturing and expiry dates, lot codes, barcodes, QR codes, and serialized unique identifiers on primary, secondary, and tertiary packaging materials. These machines are installed across the food and beverage, pharmaceutical and healthcare, cosmetics and personal care, electronics, automotive, and chemical and industrial sectors. Where, clear, durable, and machine readable product identification is a regulatory requirement and an operational necessity.

The growth of the batch coding machines market is primarily driven by tightening product traceability and anti counterfeiting regulations across major manufacturing economies, which are compelling operators to upgrade from basic contact type coders to advanced non contact and automated coding solutions. Regulatory frameworks such as the U.S. Drug Supply Chain Security Act (DSCSA) now fully in effect for manufacturers and wholesale distributors as of mid 2025 require unit level serialization with unique identifiers and electronic interoperable traceability, placing direct demand on precision batch coding and marking equipment. Parallel mandates including the European Union Falsified Medicines Directive (EU FMD) and the EU's Regulation (EU) No 1169/2011 on food information to consumers are similarly expanding compliance driven procurement of coding machines across Europe.

In addition, the broad shift toward automated and high speed production lines in food processing and pharmaceutical packaging, coupled with the growing need for integration of coding systems with plant level manufacturing IT infrastructure, is driving investment in intelligent, networked coding machines capable of real time data exchange and remote diagnostics.

Despite strong growth prospects, the market faces challenges related to the relatively high capital investment is required for laser and advanced inkjet coding systems compared to conventional contact coders, mainly for small and medium sized manufacturers in emerging economies. The technical complexity associated with integrating batch coding systems into existing packaging lines, along with the ongoing need for operator training and fluid/consumable management in inkjet based systems is posing barriers for adoption in cost sensitive segments.

The ongoing industry wide transition from consumable heavy inkjet and thermal transfer technologies toward laser based coding presents a significant growth opportunity for manufacturers offering CO2, fiber, and UV laser systems, as these platforms eliminate recurring ink and ribbon expenses while delivering permanent, tamper evident marks compatible with modern anti counterfeiting requirements. The rapid digitalization of manufacturing operations is further creating opportunities for smart, IoT enabled coding systems that integrate with cloud based production monitoring platforms. Additionally, the expansion of pharmaceutical and food processing investments across Southeast Asia, India, and the Middle East is opening new regional addressable markets for both global and local coding machine manufacturers.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 10.98 Billion |

|

Market Size in 2026 |

USD 5.50 Billion |

|

Market Size in 2025 |

USD 5.20 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 7.2% |

|

Dominating Product Type |

Continuous Inkjet (CIJ) Coding Machines |

|

Fastest Growing Product Type |

Laser Coding Machines |

|

Dominating Automation Level |

Automatic Batch Coding Machines |

|

Fastest Growing Automation Level |

Automatic Batch Coding Machines |

|

Dominating Application |

Primary Packaging |

|

Fastest Growing Application |

Secondary Packaging |

|

Dominating End Use |

Food & Beverage |

|

Fastest Growing End Use |

Pharmaceutical & Healthcare |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Expanding Pharmaceutical and Food Traceability Regulations Driving Accelerated Adoption of Advanced Coding Solutions

Regulatory requirements for product serialization and traceability are becoming the most important factor driving demand for precision batch coding machines in the pharmaceutical and food manufacturing sectors around the world. In the United States, the Drug Supply Chain Security Act (DSCSA) requires unit level serialization using unique identifiers. These identifiers include the Global Trade Item Number (GTIN), serial number, lot number, and expiry date, all encoded in 2D DataMatrix barcodes. This requirement started for manufacturers and repackagers in May 2025 and for wholesale distributors in August 2025. This change has driven pharmaceutical manufacturers and their contract packaging partners to invest in high resolution coding systems that can generate and verify serialized 2D barcodes quickly on production lines. As a result, they are replacing older hot stamp and low resolution inkjet coders with precise CIJ, TIJ, and laser coding platforms.

In parallel, the European Union Falsified Medicines Directive (EU FMD), which mandates 2D DataMatrix serialization on prescription medicines with mandatory verification against the European Medicines Verification System (EMVS), driving the adoption of coding equipment upgrades across European pharmaceutical manufacturers and packaging contractors. Beyond pharmaceuticals, food labeling regulations including the EU Food Information Regulation and the U.S. Food Safety Modernization Act (FSMA) are expanding the scope of mandatory date, lot, and origin coding on food products, broadening the addressable market for compliant coding solutions. Emerging regulatory serialization programs in markets including Brazil's SNCM, Indonesia's BPOM pharmaceutical track and trace framework, and GCC country level product traceability mandates are further expanding the geographic reach of compliance driven coding equipment demand, mostly benefiting suppliers with globally certified coding systems and multilingual software interfaces.

Accelerating Shift from Consumable Dependent Technologies Toward Laser Coding Systems

The transition from consumable intensive inkjet and thermal transfer overprinting (TTO) technologies toward laser coding systems is accelerating across food & beverage and pharmaceutical primary packaging operations, driven by the compelling total cost of ownership advantage of ink free and ribbon free laser marking over multi year production horizons. Laser coding systems including CO2 laser coders for non metallic substrates such as films, glass, and cartons; fiber laser systems for metals and rigid plastics; and UV laser platforms for sensitive or delicate substrates operate without inks, solvents, or ribbons, eliminating recurring consumable procurement costs that represent a significant component of ongoing operating expenditure for CIJ and TTO users.

The case for laser coding has become stronger with new compact laser platforms that reached their print speeds over 150 meters per minute. This helps them to make a practical choice for inline use of high speed CIJ systems in beverage and dairy packaging, where lasers were once seen as too slow. These laser marked codes are permanent and resist abrasion, moisture, and chemicals. Such features are especially important in export packaging and cold chain food distribution. Major coding machine manufacturers like Videojet Technologies, Domino Printing Sciences, and Macsa ID have added compact, production ready CO2 and UV laser coders to their portfolios. These are designed for direct use in flexible packaging and bottling lines. The environmental aspect is also becoming important. Manufacturers that follow ISO 14001 environmental management standards highlight the removal of chemical inks and solvent waste as a real contribution to their sustainability goals.

Industry 4.0 Integration and Smart Coding Systems Transforming Batch Coding from a Peripheral Tool to a Core Manufacturing Data Node

The integration of IoT connectivity, cloud based production management, and artificial intelligence into batch coding platforms is primarily redefining the operational role of coding machines within modern manufacturing environments. Historically positioned as peripheral marking tools operating in relative isolation from plant control systems, next generation batch coding machines from manufacturers including Videojet Technologies, Markem Imaje, and Domino Printing Sciences are now being deployed as fully networked data nodes within Industry 4.0 compliant production architectures, enabling bidirectional communication with ERP, MES, and quality management systems for real time coding data synchronization and automated compliance verification.

IoT enabled coding systems transmit operational data including print quality metrics, consumable consumption rates, and equipment health indicators to cloud based monitoring dashboards, enabling predictive maintenance interventions that reduce unplanned production downtime. AI powered vision inspection modules, increasingly offered as integrated add ons by coding system vendors, perform automated code quality verification at line speed, detecting misprints, smears, and incomplete barcode symbologies before non conforming packs reach downstream packaging stages. This shift toward intelligent, integrated coding infrastructure is particularly pronounced among multinational food & beverage and pharmaceutical manufacturers managing multi site production networks, where remote monitoring and centralized coding data management deliver measurable reductions in coding errors, material waste, and regulatory non compliance risk. The convergence of coding intelligence with broader digital manufacturing platforms is expected to raise switching costs and deepen vendor relationships as buyers seek end to end production data solutions rather than standalone marking hardware.

By Product Type: In 2026, the Continuous Inkjet (CIJ) Coding Machines Segment to Dominate the Global Batch Coding Machines Market

Based on product type, the global batch coding machines market is segmented into continuous inkjet (CIJ) coding machines, thermal inkjet (TIJ) coding machines, laser coding machines, thermal transfer overprinting (TTO) machines, hot stamp coders, and other product types. In 2026, the continuous inkjet (CIJ) coding machines segment is expected to account for the largest share of the global batch coding machines market. The dominant position of this segment reflects the unmatched versatility of CIJ technology across packaging substrates — including glass, PET, HDPE, flexible films, and paperboard cartons — the deep entrenchment of CIJ systems within the installed base of food, beverage, and pharmaceutical production lines globally, and the broad portfolio of production ready CIJ platforms offered by leading manufacturers such as Videojet Technologies' 1000 Line series, Domino Printing Sciences' Ax Series, Markem Imaje's 9000 series, and Hitachi's PX series, all of which offer validated compatibility with industry standard production line configurations.

However, the laser coding machines segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the accelerating shift among food & beverage and pharmaceutical manufacturers toward consumable free, low maintenance coding platforms that deliver permanent, high resolution marks without recurring ink or solvent procurement costs, alongside the growing availability of compact CO2 and UV laser coders designed for direct inline integration with flexible film and bottling lines at production speeds that are now competitive with CIJ technology.

By Automation Level: In 2026, the Automatic Batch Coding Machines Segment to Hold the Largest Share

Based on automation level, the global batch coding machines market is segmented into automatic, semi automatic, and manual batch coding machines. In 2026, the automatic batch coding machines segment is expected to account for the largest share of the global batch coding machines market. This dominance reflects the widespread deployment of inline automatic coding systems within high volume production environments across food processing, beverage bottling, pharmaceutical packaging, and consumer goods manufacturing, where continuous inline coding at production line speed is operationally essential. Automatic systems integrated directly into filling, packaging, and cartoning lines eliminate manual handling requirements, ensure consistent code placement and quality, and enable real time integration with production control and quality management systems.

The automatic batch coding machines segment is also projected to register the highest CAGR during the forecast period, driven by manufacturers' continuing capital investment in production automation, the rising cost of unskilled labor in key manufacturing economies, and the growing integration of coding systems with ERP and MES platforms that require fully automated data flow without manual operator input for code selection or job changeover.

By Application: In 2026, the Primary Packaging Segment to Account for the Largest Share

Based on application, the global batch coding machines market is segmented into primary packaging, secondary packaging, and tertiary packaging. In 2026, the primary packaging segment is expected to account for the largest share of the global batch coding machines market, reflecting the universal regulatory requirement to apply batch, date, and serialization codes directly on the immediate packaging in contact with or closest to the product across virtually all food, pharmaceutical, and consumer goods categories. Primary packaging coding demands the highest precision and substrate compatibility, making it the principal application driving the adoption of CIJ, TIJ, and laser coding technologies by manufacturers across all end use industries.

However, the secondary packaging segment is projected to register the highest CAGR during the forecast period, driven by the expanding adoption of full serialization and aggregation requirements under pharmaceutical traceability mandates such as the DSCSA and EU FMD, which require coded secondary packaging (cartons) to carry unique identifiers that are electronically linked to unit level primary pack serial numbers, creating incremental coding equipment demand at the carton and folding box packaging stage.

By End use Industry: In 2026, the Food & Beverage Segment to Hold the Largest Share

Based on end use industry, the global batch coding machines market is segmented into food & beverage, pharmaceutical & healthcare, cosmetics & personal care, electronics & electrical, automotive, chemical & industrial, and other end use industries. In 2026, the food & beverage segment is expected to account for the largest share of the global batch coding machines market, reflecting the food & beverage industry's position as the highest volume consumer of batch coding equipment globally, driven by the mandatory application of manufacturing dates, best before dates, lot codes, and regulatory product information on every unit of packaged food and beverage product across all major markets. The combination of very high production volumes, continuous line operation requirements, and increasingly stringent food labeling regulations across North America, Europe, and Asia Pacific makes food & beverage manufacturers the single largest and most active procurer of new and replacement coding machine installations.

However, the pharmaceutical & healthcare segment is projected to register the highest CAGR during the forecast period, driven by the accelerating global rollout of pharmaceutical serialization and traceability mandates — including the DSCSA in the United States, EU FMD across European member states, and emerging serialization frameworks across Asia Pacific, the Middle East, and Latin America — that require pharmaceutical manufacturers to upgrade their coding infrastructure to high resolution systems capable of generating and verifying serialized 2D DataMatrix barcodes and unique identifiers at production line speeds.

Based on geography, the global batch coding machines market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global batch coding machines market. This dominant position is driven by the United States' advanced regulatory framework for product traceability and serialization — including the fully enforced DSCSA for pharmaceuticals and the FSMA's traceability and lot coding requirements for food manufacturers — which directly mandates investment in high specification batch coding equipment across large and mid size manufacturers. The presence of leading batch coding machine manufacturers and their North American commercial operations, including Videojet Technologies (Wheeling, Illinois), Markem Imaje, Matthews Marking Systems, and Diagraph (a division of Illinois Tool Works), further supports North America's market leadership through close customer relationships and rapid service infrastructure.

However, the Asia Pacific batch coding machines market is expected to grow at the fastest CAGR from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of food processing, pharmaceutical manufacturing, and consumer goods production capacity across China, India, Japan, and Southeast Asia; the progressive tightening of product labeling and traceability regulations across these markets that is compelling manufacturers to upgrade from basic contact coders to advanced non contact systems; and the growing penetration of multinational food & beverage and pharmaceutical companies establishing regional manufacturing bases in Asia Pacific that bring their global coding technology standards with them, pulling demand for advanced CIJ, laser, and TTO systems supplied by their established global coding equipment vendors.

The global batch coding machines market is moderately consolidated at the premium technology tier, with Videojet Technologies, Markem Imaje, and Domino Printing Sciences collectively holding substantial combined market share through their broad product portfolios spanning CIJ, laser, TTO, and TIJ technologies, deep global service networks, and established validation relationships with multinational food and pharmaceutical manufacturers. At the regional and specialized tier, a broader set of manufacturers — including Hitachi Industrial Equipment Systems, Leibinger Group, Macsa ID, REA Elektronik, and Control Print — compete effectively on the basis of application specific product specialization, regional service capability, and competitive pricing in local markets.

Key competitive factors in this market include the breadth and performance of the product portfolio across coding technologies, the quality and geographic reach of after sales service and consumables supply, software capabilities for MES/ERP integration and remote connectivity, validated compliance with pharmaceutical regulatory coding requirements, and the ability to offer complete end of line coding and inspection solutions that reduce the number of equipment vendors a manufacturer needs to manage.

Large industrial technology groups such as Danaher Corporation — which owns both Videojet Technologies and Linx Printing Technologies — and Dover Corporation, which owns Markem Imaje, compete through scale, R&D investment, and global distribution infrastructure. Brother Industries competes through its ownership of Domino Printing Sciences, whose Ax Series CIJ and laser platforms have strong installed bases across European and Asia Pacific food and pharmaceutical manufacturers.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global batch coding machines market include Videojet Technologies Inc. (U.S.), Markem Imaje SAS (France), Domino Printing Sciences plc (U.K.), Linx Printing Technologies Ltd. (U.K.), Hitachi Industrial Equipment Systems Co., Ltd. (Japan), Keyence Corporation (Japan), Matthews Marking Systems (U.S.), Leibinger Group (Germany), Macsa ID S.A. (Spain), Control Print Limited (India), REA Elektronik GmbH (Germany), cab Produkttechnik GmbH & Co. KG (Germany), Squid Ink Manufacturing Inc. (U.S.), Diagraph Corporation (U.S.), and Zanasi S.r.l. (Italy), among others.

The global batch coding machines market is expected to reach USD 10.98 billion by 2036 from an estimated USD 5.50 billion in 2026, at a CAGR of 7.2% during the forecast period 2026–2036.

In 2026, the continuous inkjet (CIJ) coding machines segment is expected to hold the largest share of the global batch coding machines market, attributed to CIJ technology's versatility across packaging substrates and its deep penetration in existing food, beverage, and pharmaceutical production line installations globally.

The laser coding machines segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating shift toward consumable free, low maintenance coding solutions with superior mark permanence and growing compatibility with high speed flexible packaging and bottling line formats.

In 2026, the automatic batch coding machines segment is expected to hold the largest share of the global batch coding machines market, reflecting the near universal deployment of inline automatic coding within high volume food, pharmaceutical, and consumer goods packaging operations.

In 2026, the primary packaging segment is expected to hold the largest share of the global batch coding machines market, driven by the universal regulatory requirement to apply batch, expiry, and serialization codes directly on immediate product packaging across all major end use industries.

The pharmaceutical & healthcare segment is projected to register the highest CAGR during the forecast period, driven by the ongoing global rollout of pharmaceutical serialization and traceability mandates that require manufacturers to upgrade their coding infrastructure to high resolution, interoperable serialization capable systems.

The growth of this market is primarily driven by expanding regulatory mandates for product traceability and serialization across pharmaceutical and food sectors, the accelerating adoption of automated and smart coding systems integrated with Industry 4.0 manufacturing infrastructure, and the growing shift from consumable based inkjet and TTO systems to laser coding platforms that offer significant long term operating cost advantages.

Key players in the global batch coding machines market include Videojet Technologies Inc. (U.S.), Markem Imaje SAS (France), Domino Printing Sciences plc (U.K.), Linx Printing Technologies Ltd. (U.K.), Hitachi Industrial Equipment Systems Co., Ltd. (Japan), Keyence Corporation (Japan), Matthews Marking Systems (U.S.), Leibinger Group (Germany), Macsa ID S.A. (Spain), Control Print Limited (India), REA Elektronik GmbH (Germany), cab Produkttechnik GmbH & Co. KG (Germany), Squid Ink Manufacturing Inc. (U.S.), Diagraph Corporation (U.S.), and Zanasi S.r.l. (Italy).

Asia Pacific is expected to register the highest growth rate in the global batch coding machines market during the forecast period 2026–2036, driven by expanding FMCG and pharmaceutical manufacturing capacity and rising regulatory pressure for product identification across China, India, Japan, and Southeast Asia.

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates