Resources

About Us

AI Workflow Automation Market Size, Share & Trends Analysis by Offering, Technology, Deployment, Organization Size, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

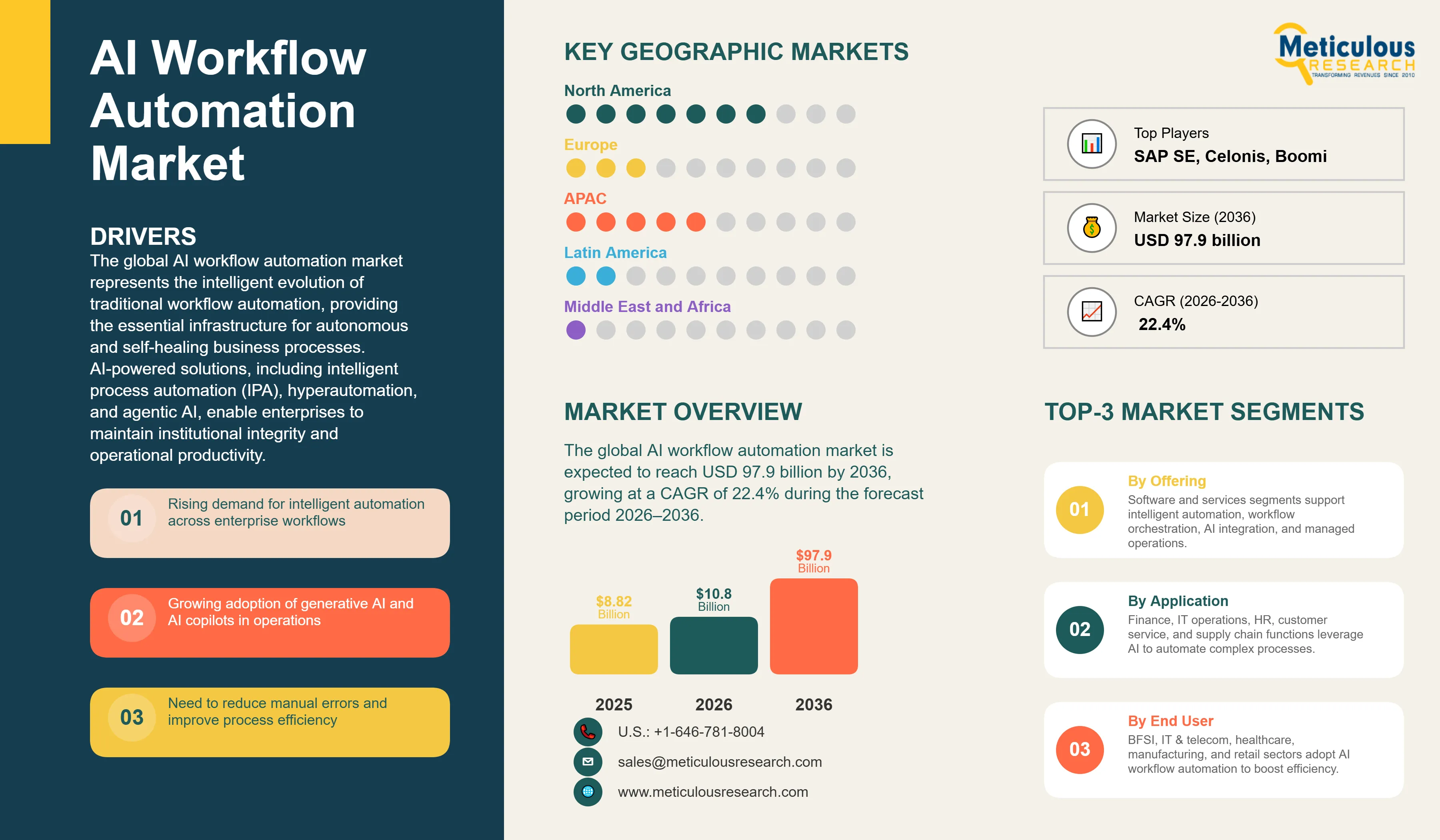

Report ID: MRAUTO - 1042035 Pages: 287 Jun-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global AI workflow automation market is valued at USD 10.8 billion in 2026. This market is expected to reach USD 97.9 billion by 2036, growing at a CAGR of 22.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global AI workflow automation market represents the intelligent evolution of traditional workflow automation, providing the essential infrastructure for autonomous and self-healing business processes. AI-powered solutions, including intelligent process automation (IPA), hyperautomation, and agentic AI, enable enterprises to maintain institutional integrity and operational productivity. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to address process inefficiencies and the increasing demand for autonomous decision-making. According to industry reports, AI workflow automation is essential for reducing human error and improving enterprise throughput.

The transition toward agentic AI and autonomous workflows is essential for improving organizational agility and process intelligence in the digital economy. Modern AI workflow automation solutions leverage large language models (LLMs) and multi-agent systems to provide a unified orchestration of complex tasks, ensuring that stakeholders have immediate access to actionable insights. As organizations transition toward hyperautomation models, the demand for AI-driven orchestration platforms that can demonstrably reduce operational costs and improve resource utilization is expected to surge.

Drivers: Accelerating Digital Transformation through Intelligent Process Automation and Agentic AI

The primary driver for the AI workflow automation market is the escalating global cost of manual operations and the increasing complexity of digital business environments, which necessitates a more efficient and intelligent approach to process management. According to industry benchmarks, process bottlenecks and manual data entry account for significant annual losses in enterprise budgets. This financial burden is driving the adoption of intelligent workflow automation to manage the high volume of transactions and decision-making tasks. Furthermore, the shift toward generative AI and the increasing demand for AI copilots are significant drivers. Government initiatives promoting digital transformation and the adoption of sovereign AI solutions are compelling organizations to invest in AI workflow orchestration that can seamlessly integrate with broader enterprise resource planning (ERP) and CRM ecosystems.

Restraints: Data Privacy Concerns and Legacy System Integration Challenges

Market growth is restrained by significant concerns related to data privacy and security in AI-driven environments and the technical challenges of achieving seamless integration across disparate legacy IT systems and fragmented data silos. For many organizations, the initial capital investment and the need for specialized AI talent to manage complex autonomous workflows can be a significant barrier. Additionally, the 'black box' nature of some AI decision engines often leads to trust issues, making it difficult to achieve full-scale autonomous adoption. Concerns regarding the ethical use of AI and the potential for algorithmic bias also act as deterrents to market expansion. Furthermore, the significant organizational change management and process re-engineering required for successful hyperautomation can lead to slower adoption rates.

Opportunities: Advancing Generative AI Integration and Autonomous Multi-Agent Systems

The integration of generative AI and multi-agent systems into workflow automation platforms offers substantial growth opportunities. Generative AI-powered tools can analyze complex business data and unstructured content to identify potential workflow optimizations, facilitating more precise decision automation. By 2026, AI-driven process mining is being used to discover hidden inefficiencies and optimize automated business workflows, enabling proactive resource distribution and improving operational intelligence. Furthermore, the shift toward low-code and no-code automation platforms provides organizations with superior agility and faster time-to-market. This democratization of automation facilitates real-time collaboration among diverse business units, supporting enterprise-wide digital transformation, which is particularly beneficial for scaling hyperautomation initiatives.

Evolution toward Agentic AI and Self-Healing Autonomous Workflows

A key trend in 2026 is the transition from rule-based workflow automation and standalone RPA deployments toward agentic AI-driven workflow orchestration. Organizations are increasingly deploying AI agents capable of reasoning across enterprise data sources, coordinating multi-step tasks, and adapting workflows based on real-time conditions. Gartner projects that 40% of enterprise applications will incorporate task-specific AI agents by 2026, compared with less than 5% in 2025, reflecting rapid enterprise adoption of agent-based automation architectures. IDC further estimates that over 50% of enterprise applications already include AI assistants or AI advisors, while approximately 20% have integrated more advanced AI agent capabilities. These developments are accelerating demand for autonomous and self-healing workflows that improve operational resilience, reduce manual intervention, and enhance process efficiency across enterprise environments.

Integration of Generative AI Copilots and Decision Engines

The integration of generative AI copilots and AI-powered decision engines into workflow automation platforms is becoming a core enterprise investment area. Organizations are embedding LLM-based assistants directly into business processes to support document processing, workflow recommendations, knowledge retrieval, and operational decision-making. According to Gartner, 72% of supply chain organizations have already deployed generative AI initiatives, while most enterprise applications are expected to include embedded AI assistants as a standard capability. At the same time, organizations are moving beyond productivity-focused copilots toward decision-centric automation models, particularly in regulated industries and public-sector environments. Gartner forecasts that at least 80% of government organizations will deploy AI agents to automate routine decision-making by 2028, highlighting the growing role of AI-driven decision support in enterprise workflow execution and governance.

Software

Based on offering, the software segment is expected to hold the largest share in 2026. This dominance is driven by the increasing demand for intelligent process automation (IPA) platforms and AI-driven decision engines. Integrated software provides a centralized 'source of truth' for business data and process status, enabling more efficient regional workflow coordination. Key sub-segments include AI-powered workflow orchestration platforms, which manage complex task dependencies, and generative AI automation tools, which handle unstructured data processing. Real-time workflow intelligence dashboards are also essential for providing business leaders with immediate access to critical operational data.

Services

The services segment is growing in importance as organizations seek expert guidance for organizational change management and technical integration. This includes strategic consulting, custom AI implementation, and post-deployment support. As AI workflow solutions become more complex, the need for comprehensive maintenance and AI-governance services is becoming a critical success factor for enterprises. Managed automation services are also gaining traction, providing organizations with access to specialized AI talent and scalable automation infrastructure.

Based on technology, the intelligent process automation (IPA) and hyperautomation segments are expected to account for the largest shares in 2026, reflecting the critical need for seamless integration of AI and RPA. The agentic AI and multi-agent systems segments are projected to witness the fastest growth, as enterprises prioritize autonomous workflows and self-healing processes. The integration of generative AI (LLMs) and process mining tools is also significant, providing the infrastructure for real-time workflow intelligence and decision automation. Decision engines and AI copilots are also gaining traction, supporting faster and more accurate operational responses.

North America is expected to remain the largest regional market for AI workflow automation in 2026, accounting for approximately 44% of global revenue. Regional leadership is driven by strong enterprise adoption of generative AI, a mature software ecosystem, and significant investments in intelligent automation and hyperautomation initiatives across large enterprises. The United States continues to lead global enterprise software spending and hosts many of the industry's leading vendors, including Microsoft, ServiceNow, Salesforce, UiPath, Automation Anywhere, Appian, and Pegasystems. Continued investment in AI-enabled productivity, workflow modernization, and operational efficiency is expected to support sustained market growth across the U.S. and Canada.

Asia Pacific is projected to register the fastest growth during the forecast period, supported by rapid digital transformation initiatives, expanding cloud adoption, and increasing enterprise investment in AI technologies. Major economies such as China, India, Japan, South Korea, and Singapore are accelerating the deployment of intelligent automation solutions across manufacturing, financial services, telecommunications, healthcare, and public-sector operations. Government-led digitalization programs, growing AI infrastructure investments, and the increasing adoption of cloud-native business applications are expected to drive demand for AI-powered workflow orchestration and process automation platforms throughout the region.

The competitive landscape of the global AI workflow automation market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end intelligent care orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI agents and their ability to provide seamless integration with ERP, CRM, and other enterprise management platforms. Strategic acquisitions of niche AI and process mining companies are a common trend as vendors seek to enhance their diagnostic and automation capabilities. The market is also seeing increased collaboration between automation vendors and cloud providers to ensure seamless enterprise-wide orchestration.

Key players operating in the global market include Microsoft Corporation (U.S.), IBM Corporation (U.S.), UiPath Inc. (U.S.), ServiceNow, Inc. (U.S.), SAP SE (Germany), Salesforce, Inc. (U.S.), Appian Corporation (U.S.), Pegasystems Inc. (U.S.), Automation Anywhere, Inc. (U.S.), Oracle Corporation (U.S.), Blue Prism (SS&C Technologies) (U.K.), and various emerging technology providers specializing in agentic AI and generative AI automation tools.

The market is projected to reach USD 97.9 billion by 2036, growing at a CAGR of 10.8% from 2026 to 2036.

The AI workflow automation market is emerging as one of the fastest-growing segments within the broader workflow automation industry. Growth is being driven by enterprise demand for intelligent decision-making, generative AI-powered assistants, process intelligence, and agentic automation capabilities that extend beyond traditional rule-based workflow management. Consequently, AI-enabled solutions are expected to capture an increasing share of workflow automation spending over the forecast period.

Enterprises report a significant reduction in process cycle times and an improvement in operational intelligence and resource utilization.

The Agentic AI and Multi-Agent Systems segments are expected to grow the fastest.

The majority of new enterprise workflow automation deployments in 2026 are expected to include embedded AI functionality, as leading vendors increasingly integrate generative AI, machine learning, process intelligence, and autonomous decision-support capabilities into their platforms.

North America holds the largest share, estimated at 44.2% in 2026, driven by early adoption of generative AI.

AI enables the discovery of hidden inefficiencies and optimizes automated business workflows, facilitating proactive resource distribution.

Hyperautomation is a major growth driver, pushing organizations to automate as many business and IT processes as possible using AI.

The BFSI and IT & telecommunications segments are the primary adopters, managing the highest volumes of complex workflows.

The top 5 players are Microsoft, IBM, UiPath, ServiceNow, and SAP.

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates