Resources

About Us

Subscription & Membership Platforms for Content Creators Market Size, Share, & Forecast by Platform Type (Patreon, Substack, Custom), Creator Type, Pricing Model, and Exclusive Content Offering – Global Forecast (2026-2036)

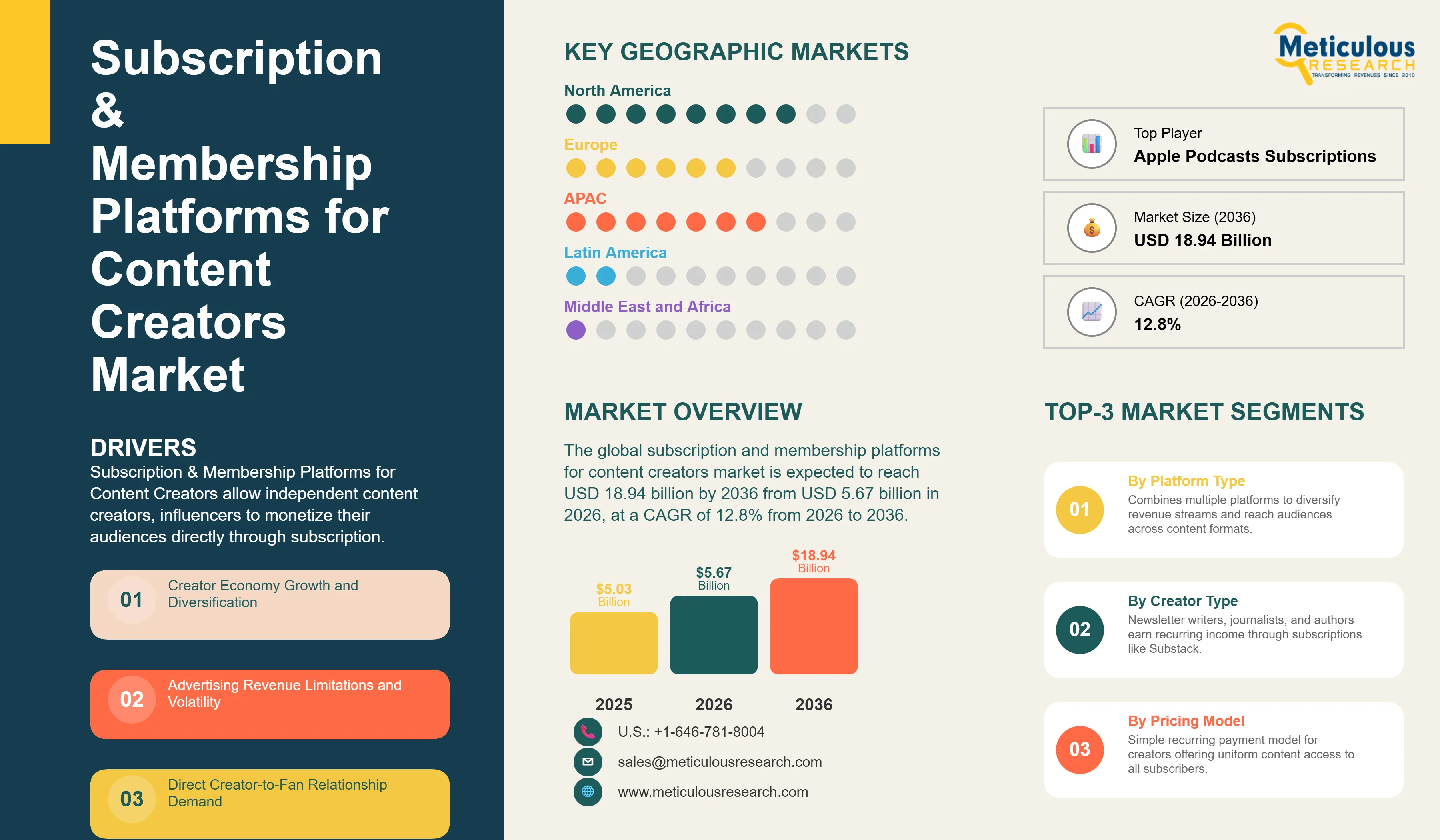

Report ID: MRICT - 1041693 Pages: 281 Jan-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global subscription and membership platforms for content creators market is expected to reach USD 18.94 billion by 2036 from USD 5.67 billion in 2026, at a CAGR of 12.8% from 2026 to 2036.

Subscription and Membership Platforms for Content Creators are digital infrastructure solutions that allow independent content creators, influencers, artists, writers, podcasters, educators, and media professionals to monetize their audiences directly through subscription and membership-based models, without the need for intermediaries or advertising-based revenue streams. These niche platforms offer end-to-end solutions such as subscriber management systems that handle recurring payments, tiered membership models with varying levels of access, exclusive content delivery through paywall-protected areas, community engagement tools such as forums, messaging, and live sessions, analytics dashboards that track subscriber acquisition, retention, and revenue, payment management and payouts that handle international transactions, content hosting and distribution for video, audio, text, and digital downloads, and social media and marketing integrations for audience acquisition. These platforms, through their facilitation of direct economic engagement between creators and their fans, power the "creator economy," which is estimated to include over 50 million creators worldwide, by providing them with alternative monetization streams that are not dependent on advertising, sponsorships, or algorithmic support, while also allowing fans to engage more intimately with their favorite creators through exclusive content, community access, and direct support.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Subscription and Membership Platforms for Content Creators represent foundational infrastructure enabling the "creator economy" revolution—the transformation of content creation from hobby or advertising-dependent activity to sustainable independent profession. These platforms address the fundamental challenge that content creators face: monetizing audiences in an era where free content dominates and advertising revenue is uncertain, platform-controlled, and often insufficient for sustainable income. By facilitating direct economic relationships between creators and their most engaged fans willing to pay for exclusive content, early access, community participation, or simply to support creators they value, these platforms enable business models independent of advertising, algorithms, or traditional media gatekeepers. The platforms' economic model is typically commission-based (5-12% of transaction value plus payment processing fees), aligning platform success with creator success and creating virtuous cycles where platform improvements attract more creators, growing the ecosystem.

Several transformative trends are reshaping the subscription platforms market, including the proliferation of "super fans" willing to pay significantly for close creator connections and exclusive experiences, the fragmentation of media consumption creating opportunities for niche creators building devoted audiences, the integration of Web3 technologies including NFTs and tokenized memberships creating new monetization models, the advancement of AI tools enabling creators to produce higher-quality content more efficiently, and the evolution toward "creator stacks"—combinations of multiple platforms and tools optimizing different aspects of creator businesses. The convergence of creator economy growth—estimated to be a $100+ billion market globally—platform technology maturation, changing consumer attitudes toward paying creators, and creator desires for independence from traditional media has elevated subscription platforms from niche tools to essential infrastructure supporting millions of creative professionals.

The subscription and membership platforms market is experiencing rapid evolution toward more sophisticated, creator-focused solutions offering comprehensive business management beyond simple paywall functionality. Modern platforms incorporate advanced capabilities including AI-powered content recommendations personalizing member experiences, predictive analytics forecasting subscriber churn and revenue, automated community management tools moderating discussions and fostering engagement, multi-format content support enabling video, audio, text, live streams, and digital products in unified offerings, advanced analytics providing insights into content performance, subscriber demographics, and revenue optimization, mobile-first experiences recognizing mobile consumption dominance, and integration with creator tools including email marketing, social media scheduling, and merchandise platforms creating unified creator operations.

Platform differentiation is intensifying as competition increases, with platforms specializing by creator type, content format, or unique features. Patreon maintains broad creator appeal through comprehensive features and community, Substack dominates newsletter monetization through simple, writer-friendly design, OnlyFans (despite adult content association) demonstrates subscription model power for exclusive content, Ko-fi and Buy Me a Coffee target tip-jar and supporter models, Memberful and Ghost enable self-hosted subscriptions for brand-conscious creators, Circle and Mighty Networks emphasize community features, and YouTube Channel Memberships and Twitch Subscriptions leverage existing platform audiences. This specialization creates opportunities for platforms targeting specific niches—video creators, podcasters, educators, artists—with tailored features rather than one-size-fits-all approaches.

The tiered membership model has emerged as best practice, with most successful creators offering 2-4 subscription tiers providing different value levels. Typical structures include basic tier ($3-5/month) providing early access and exclusive content, mid-tier ($10-15/month) adding community access and behind-the-scenes content, premium tier ($25-50+/month) offering personalized interactions, video calls, or consulting, and potentially ultra-premium tiers ($100+/month) for intensive experiences or business services. This tiering maximizes revenue by capturing willingness-to-pay across audience segments—casual supporters at low prices, devoted fans at mid-tier, and super-fans at premium—while giving creators flexibility in value delivery.

|

Parameter |

Details |

|

Market Size Value in 2026 |

USD 5.67 Billion |

|

Revenue Forecast in 2036 |

USD 18.94 Billion |

|

Growth Rate |

CAGR of 12.8% from 2026 to 2036 |

|

Base Year for Estimation |

2025 |

|

Historical Data |

2021–2025 |

|

Forecast Period |

2026–2036 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2036 |

|

Report Coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, trends |

|

Segments Covered |

Platform Type, Creator Type, Pricing Model, Exclusive Content Offering, Revenue Size, Region |

|

Regional Scope |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Countries Covered |

U.S., Canada, U.K., Germany, France, Spain, Italy, Netherlands, India, China, Japan, South Korea, Indonesia, Brazil, Mexico, Australia |

|

Key Companies Profiled |

Patreon Inc., Substack Inc., OnlyFans, Ko-fi, Memberful (Patreon), Ghost Foundation, Buy Me a Coffee, Gumroad, Circle.so, Mighty Networks, Podia, Teachable, Thinkific, Kajabi, ConvertKit, Steady HQ, YouTube (Google), Twitch (Amazon), Facebook/Meta Subscriptions, Apple Podcasts Subscriptions |

Custom self-hosted platforms are gaining traction among established creators willing to invest in proprietary infrastructure for greater control and economics. Platforms like Ghost, Memberful, and WordPress plugins enable creators to build subscription businesses on their own domains, controlling branding, customer relationships, and data while avoiding platform dependencies. The trade-off involves higher technical requirements and upfront costs but lower ongoing fees (no 5-12% platform commission) and complete business ownership. This segment is growing particularly among creators with established audiences willing to follow them off third-party platforms and creators building long-term brand value justifying infrastructure investment.

Community features are becoming increasingly central to subscription platforms, recognizing that exclusive content alone may not sustain long-term subscribers. Platforms are adding discussion forums, chat capabilities, live events, member directories, and collaborative features enabling member-to-member connections. This "community-as-a-service" approach transforms subscriptions from pure content access to membership in exclusive communities, increasing perceived value and subscriber retention. Creators building engaged communities report higher renewal rates and lower churn than those focused solely on content delivery.

Driver: Creator Economy Growth and Diversification

The explosive global growth of the creator economy creates fundamental demand for monetization platforms as millions of individuals pursue content creation as full-time or part-time income sources. Estimates suggest 50+ million people globally identify as creators, with 2+ million earning income from creative pursuits. This creator population explosion is driven by technology democratization making content production accessible through smartphones and free editing tools, platform algorithms enabling audience building without traditional gatekeepers, COVID-19 accelerating digital content consumption and online income interest, and cultural shifts valuing creative pursuits and digital entrepreneurship. As creator populations grow, the subset pursuing professional income and seeking sustainable monetization beyond advertising increases proportionally, driving subscription platform adoption.

Driver: Advertising Revenue Limitations and Volatility

Growing creator frustration with advertising-dependent business models drives subscription platform adoption as creators seek revenue predictability and independence from platform algorithm changes. Advertising revenue faces multiple challenges including platform algorithm changes that can devastate reach overnight, advertiser brand safety concerns limiting monetization for controversial or niche content, low CPMs for small to mid-size creators making sustainable income difficult, and audience ad fatigue reducing engagement. Subscription models offer compelling alternatives providing predictable recurring revenue independent of view counts, direct economic relationships with most engaged fans, higher per-subscriber revenue than per-viewer ad revenue, and business model diversification reducing platform dependency.

Opportunity: Expansion into Emerging Markets and Creator Populations

The expansion of creator economies in emerging markets creates substantial growth opportunities as platforms and creators tap vast populations with growing digital access and disposable income. Markets including India, Indonesia, Brazil, Mexico, and others represent opportunities including massive creator populations with India alone estimated at 10+ million creators, growing middle classes with increasing disposable income for digital subscriptions, rapid digital payment adoption through mobile wallets and UPI-style systems, and high mobile internet penetration enabling content creation and consumption. Platforms localizing for these markets through regional payment methods, local currency support, and language localization can capture large, fast-growing creator populations.

Opportunity: Enterprise and B2B Creator Services

The evolution of creator businesses toward professional operations creates opportunities for premium platform services, tools, and B2B offerings beyond consumer subscriptions. Opportunities include white-label platforms for media companies and brands launching creator programs, enterprise features for large creator organizations including team collaboration, advanced analytics, and custom integrations, professional services including consulting, legal, and financial services for creators, and creator financing including advances against future subscription revenue. These B2B services can command premium pricing and provide platform revenue diversification beyond consumer subscription commissions.

By Platform Type:

In 2026, the Third-Party Hosted Platforms segment (Patreon, Substack, Ko-fi style) is estimated to hold the largest share of the overall subscription and membership platforms market, driven by ease of use with minimal technical knowledge required, established platform brands with creator trust and audience familiarity, comprehensive feature sets including payment processing, content hosting, community tools, and analytics, and network effects as platform communities attract new creators and subscribers. These platforms handle technical infrastructure, compliance, and operations, allowing creators to focus on content. They typically charge 5-12% commission plus payment processing fees but provide turnkey solutions. Patreon serves 250,000+ creators across diverse categories, Substack focuses on newsletter creators with streamlined writing-focused interface, OnlyFans despite adult content association demonstrates subscription model power, and YouTube/Twitch memberships leverage existing platform audiences.

The Custom Self-Hosted Platforms segment is expected to grow at the highest CAGR during the forecast period, driven by creator desire for brand control and business ownership, avoidance of 5-12% platform fees improving economics for high-earning creators, data ownership and direct customer relationships, and advanced customization enabling unique brand experiences. Solutions including Ghost, Memberful, and WordPress plugins enable creators to build subscription businesses on their own domains. This requires higher technical capability and upfront investment but provides long-term advantages for creators building enduring brands. The segment particularly attracts established creators with substantial audiences willing to migrate and creators in niches where brand control matters.

The Hybrid and Multi-Platform segment is emerging as creators use multiple platforms simultaneously—Patreon for tiered memberships, Substack for newsletters, Ko-fi for tips, YouTube memberships for video exclusives—creating diversified revenue streams and reaching audiences across platforms.

By Creator Type:

In 2026, the Video Content Creators segment is estimated to dominate the overall market, reflecting the massive population of YouTube, TikTok, and Instagram creators monetizing through membership platforms, high audience engagement with video content driving willingness to pay, and strong exclusive video content value proposition through early access, extended cuts, behind-the-scenes footage, and ad-free viewing. Video creators represent the largest creator category and video subscriptions command premium pricing given production value. Platforms serving this segment include Patreon (many video creators), YouTube Channel Memberships (integrated with existing YouTube audiences), and specialized video platforms.

The Written Content Creators segment (newsletter writers, journalists, authors) is experiencing rapid growth during the forecast period, driven by Substack's success demonstrating newsletter monetization viability, journalist migration from traditional media seeking independent income, reader willingness to pay for quality journalism, analysis, and niche expertise, and relatively low content production costs for written content. Substack has enabled thousands of writers to build sustainable newsletter businesses, some earning six-figure incomes. The segment benefits from subscription fatigue driving selective high-quality subscription choices where written content offers depth algorithms don't reward.

The Podcasters segment is growing as creators monetize through early access, ad-free episodes, exclusive content, and community features. The Visual Artists and Illustrators segment leverages platforms for digital art sales, early access, process videos, and tutorial content. The Educators and Course Creators segment uses membership platforms for course delivery, though often migrate to dedicated course platforms (Teachable, Kajabi) as businesses scale.

By Pricing Model:

In 2026, the Tiered Subscription segment is expected to witness the highest growth rate, driven by revenue optimization through price discrimination capturing willingness-to-pay across audience segments, flexibility attracting casual supporters ($3-5), devoted fans ($10-20), and super-fans ($50+), and proven effectiveness with successful creators typically earning 40-60% of revenue from higher tiers despite fewer subscribers. Typical structures offer 2-4 tiers with progressive benefits. This model maximizes lifetime value per subscriber and provides clear upgrade paths increasing average revenue per user over time.

The Single-Tier Subscription segment maintains presence particularly for simple creator offerings where tiering complexity isn't justified. Substack's default model uses single pricing, though creators can create multiple publications at different prices. Single-tier simplicity appeals to creators preferring straightforward offerings and audiences not wanting choice complexity.

The Pay-What-You-Want segment (Ko-fi, Buy Me a Coffee) enables supporters to choose payment amounts, maximizing accessibility while capturing higher payments from generous fans. This model works particularly well for tip-jar style support rather than exclusive content access.

The Lifetime Access segment offers one-time payments for permanent membership, trading recurring revenue for upfront capital and simplified subscriber management, appealing to audiences hesitant about recurring subscriptions and creators building course-style libraries where ongoing production is less critical.

By Exclusive Content Offering:

In 2026, the Early Access segment is estimated to account for significant share, providing subscribers with content before public release, creating value without additional production since content eventually goes public. This model maintains free content availability while monetizing most engaged fans willing to pay for immediacy. It's particularly popular with video creators and podcasters.

The Exclusive/Behind-the-Scenes Content segment provides content available only to subscribers, including process videos, outtakes, extended interviews, personal updates, and creator life glimpses creating parasocial intimacy. This requires additional production but delivers strong value justifying higher pricing tiers.

The Community Access segment monetizes exclusive communities where subscribers interact with creators and each other, recognizing community value often exceeds content value for retention. Platforms emphasizing this include Circle, Mighty Networks, and Discord integrations with subscription platforms.

The Personalized Experiences segment offers highest-tier benefits including one-on-one calls, personalized content, consulting, or physical merchandise, targeting super-fans willing to pay premium prices for direct creator connection.

Regional Insights:

In 2026, North America is estimated to account for the largest share of the global subscription and membership platforms market, driven by most mature creator economy with established infrastructure and professional creators, high consumer willingness to pay for digital subscriptions with subscription fatigue yet selective quality subscriptions maintained, strong platform presence with Patreon, Substack, and others headquartered in U.S., and high disposable incomes supporting creator memberships. The U.S. dominates regional market with estimated 5-10 million creators and millions of paying subscribers supporting creator economy. Platform innovation, creator professionalization, and cultural acceptance of creator support models drive market maturity.

Asia-Pacific is expected to grow at the highest CAGR during the forecast period, driven by massive creator populations with India, Indonesia, Southeast Asia, and China representing tens of millions of creators, rapid digital payment adoption through UPI in India, digital wallets across region, and mobile payment proliferation, growing middle classes with disposable income for entertainment and content subscriptions, and localized platform development including Patreon-style platforms tailored to regional markets. India represents particularly significant opportunity with 10+ million creators, growing English and regional language content consumption, and increasing monetization interest. China's creator ecosystem, while distinct due to platform restrictions, represents massive opportunity for domestic platforms including WeChat subscriptions and specialized creator platforms.

Europe represents significant market driven by strong media and entertainment creator communities particularly in U.K., Germany, France, mature digital subscription culture with news, streaming, and content subscription acceptance, Patreon, Substack, and Ko-fi adoption across European creators, and multilingual content creating diverse niches. The U.K. leads European market through creator concentration and cultural similarities to U.S. market. European privacy regulations (GDPR) influence platform design emphasizing data protection and user rights.

Major players include Patreon Inc. (U.S.), Substack Inc. (U.S.), OnlyFans (U.K.), Ko-fi (U.K.), Memberful/Patreon (U.S.), Ghost Foundation (Singapore), Buy Me a Coffee (Poland), Gumroad (U.S.), Circle.so (U.S.), Mighty Networks (U.S.), Podia (U.S.), Teachable (U.S.), Thinkific (Canada), Kajabi (U.S.), ConvertKit (U.S.), Steady HQ (Germany), YouTube/Google (U.S.), Twitch/Amazon (U.S.), Facebook/Meta Subscriptions (U.S.), and Apple Podcasts Subscriptions (U.S.), among others.

The market is expected to grow from USD 5.67 billion in 2026 to USD 18.94 billion by 2036.

The market is expected to grow at a CAGR of 12.8% from 2026 to 2036.

Major players include Patreon, Substack, OnlyFans, Ko-fi, Ghost, Gumroad, Circle.so, Mighty Networks, Podia, Teachable, YouTube, Twitch, and others.

Main factors include creator economy growth with 50+ million global creators, advertising revenue limitations driving subscription models, consumer willingness to pay for quality content and creator support, emerging market expansion with massive creator populations in Asia-Pacific, and platform innovation enabling sophisticated monetization tools.

North America is estimated to account for the largest share in 2026 due to mature creator economy and high consumer subscription adoption, while Asia-Pacific is expected to register the highest growth rate during 2026-2036.

Published Date: Jul-2026

Published Date: May-2025

Published Date: May-2023

Published Date: Aug-2025

Published Date: Sep-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates