Resources

About Us

Sacral Neuromodulation Market Size, Share & Trends Analysis by Product Type, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

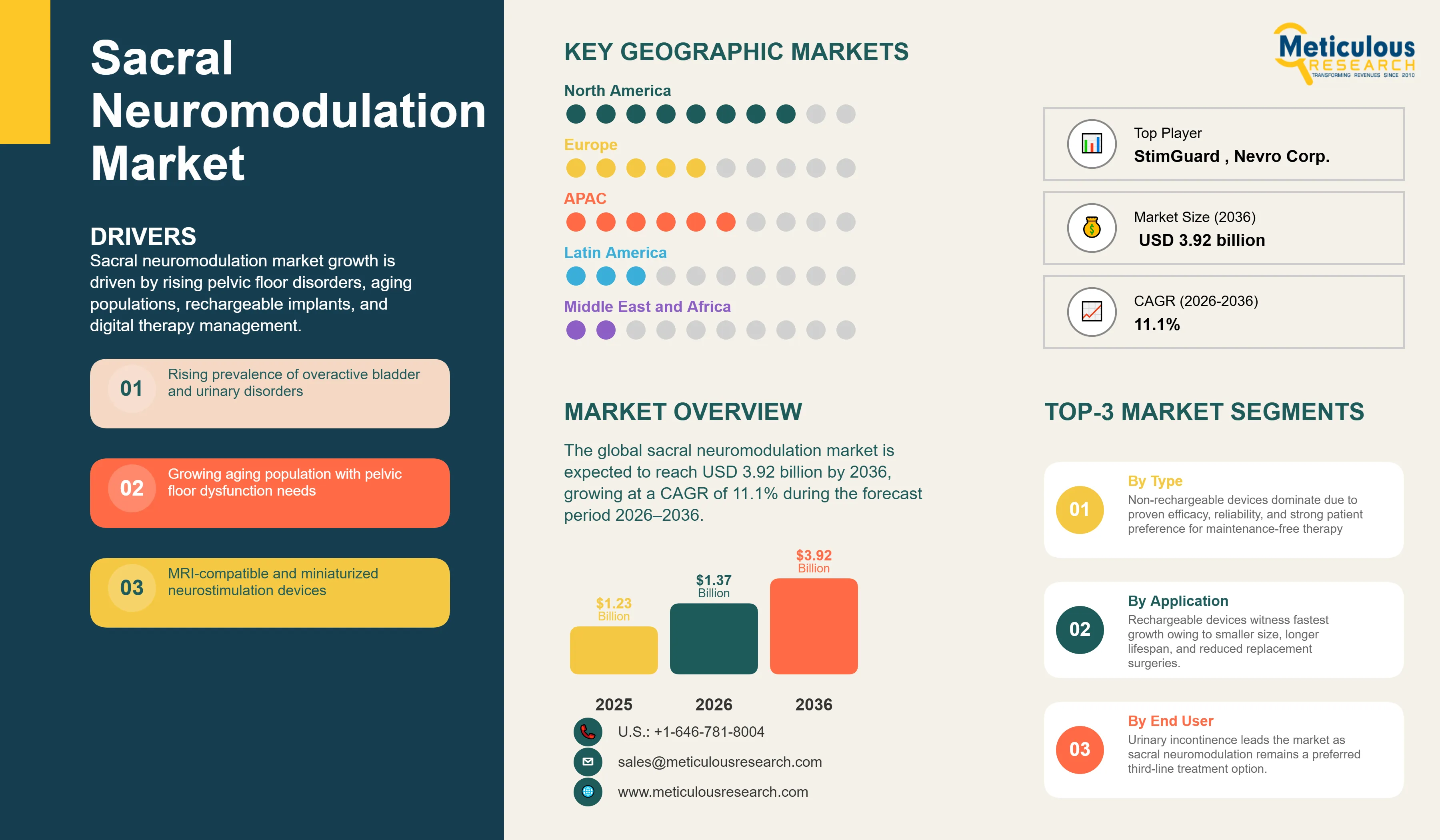

Report ID: MRHC - 1042079 Pages: 268 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global sacral neuromodulation market is estimated to be USD 1.37 million in 2026. This market is expected to reach USD 3.92 billion by 2036, growing at a CAGR of 11.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global sacral neuromodulation market is undergoing a significant transformation, driven by the rapid evolution of implantable neurostimulation technologies and a growing clinical emphasis on treating refractory bladder and bowel dysfunction. Sacral neuromodulation (SNM), also known as sacral nerve stimulation (SNS), has emerged as a highly effective third-line therapy for patients who have failed conservative treatments for overactive bladder, non-obstructive urinary retention, and fecal incontinence. The market is primarily fueled by the rising global prevalence of pelvic floor disorders, an aging population, and the increasing adoption of minimally invasive surgical techniques. Technological innovations, such as the introduction of miniaturized, MRI-compatible, and rechargeable pulse generators, are redefining the clinical standard of care. These advancements address previous limitations regarding device size and the need for surgical battery replacements, thereby enhancing patient acceptance and long-term therapeutic compliance. Clinical guidelines from the American Urological Association (AUA), the International Continence Society (ICS), and the International Neuromodulation Society (INS) increasingly position SNM as a cornerstone of advanced pelvic health management. As healthcare systems shift toward value-based care, the development of more ergonomic implant tools and simplified procedural workflows is facilitating the migration of SNM therapy to specialized clinics and ambulatory settings. The integration of digital health platforms for remote patient monitoring and personalized therapy adjustment is further expected to enhance the precision and consistency of sacral neuromodulation, driving sustained market growth through 2036.

The growth of the global sacral neuromodulation market is primarily driven by the escalating incidence of chronic bladder and bowel issues and the rapid clinical adoption of next-generation, patient-friendly implantable devices.

Rising Global Incidence of Refractory Overactive Bladder and Fecal Incontinence in Aging Populations

A major driver for the market is the increasing global prevalence of refractory overactive bladder (OAB) and fecal incontinence, particularly among the aging population. According to the International Continence Society and the World Health Organization, overactive bladder affects an estimated 500 million people worldwide, making it one of the most prevalent chronic urological conditions. Furthermore, studies indicate that fecal incontinence affects approximately 2–10% of the adult population globally, with prevalence increasing substantially among older adults and long-term care populations. The aging demographic is expected to further accelerate demand; according to the United Nations, the global population aged 65 years and older is projected to reach nearly 1.6 billion by 2050. As pelvic floor disorders significantly impact quality of life, physical health, and social well-being, demand for effective long-term treatment options continues to rise. In addition, growing awareness of advanced neurostimulation therapies and reduced stigma surrounding bladder and bowel dysfunction are contributing to higher diagnosis rates and increased adoption of sacral neuromodulation procedures.

Technological Advancements in MRI-Compatible and Miniaturized Implantable Pulse Generators

The market is significantly driven by the introduction of MRI-compatible and miniaturized implantable pulse generators (IPGs). These technological breakthroughs address two of the most significant historical barriers to SNM adoption: the need for device removal during MRI scans and the discomfort associated with larger implants. Modern systems, such as those developed by Axonics and Medtronic, offer full-body MRI compatibility and significantly smaller footprints, which improve patient comfort and reduce the risk of skin erosion or pocket complications. The improved safety profiles and reduced maintenance requirements of these advanced systems are encouraging their widespread clinical adoption, serving as a fundamental driver for market expansion.

Despite its clinical efficacy, the adoption of sacral neuromodulation is hindered by the high cost of therapy and the complex regulatory and reimbursement landscapes in many global markets.

Significant Capital Investment and High Procedural Costs for Implantable SNM Systems

A major restraint for the market is the high cost associated with sacral neuromodulation therapy, including the price of the implantable devices, surgical fees, and long-term follow-up care. The significant capital investment required for these advanced neurostimulation platforms can be a barrier for healthcare facilities, particularly in emerging markets or regions with constrained healthcare budgets. Furthermore, the high cost of specialized disposables and the potential need for surgical revisions or battery replacements (for non-rechargeable systems) can impact the overall cost-effectiveness of the therapy, potentially limiting its availability to larger, well-funded medical centers.

Stringent Regulatory Requirements and Varied Global Reimbursement Policies

The global sacral neuromodulation market is also impacted by stringent regulatory requirements and the variability of reimbursement policies across different countries. Obtaining regulatory approvals for new neurostimulation devices is a lengthy and costly process, requiring extensive clinical evidence of safety and efficacy. Additionally, the lack of standardized reimbursement for SNM in certain regions can deter healthcare providers from offering the therapy and limit patient access. These regulatory and financial hurdles remain significant challenges for manufacturers and can restrain the rapid adoption of new SNM technologies in several international markets.

Future growth opportunities in the sacral neuromodulation market are centered on the expansion into underserved geographic regions and the integration of advanced digital health solutions to optimize therapy management.

Increasing Penetration in Emerging Markets with Growing Pelvic Health Awareness

There is a significant opportunity for market growth driven by the increasing penetration of SNM therapy in emerging markets, particularly in Asia-Pacific and Latin America. As healthcare infrastructure improves and awareness of pelvic floor disorders grows in these regions, the demand for advanced urological treatments is expected to rise. Manufacturers that can offer cost-effective neurostimulation solutions and provide comprehensive clinical training to local healthcare professionals are well-positioned to capitalize on this untapped potential. The rising middle-class population and increasing healthcare expenditure in these economies are further facilitating the adoption of advanced medical technologies.

Integration of Digital Health Platforms and AI for Personalized Therapy Optimization

The integration of digital health platforms and artificial intelligence (AI) for remote patient monitoring and therapy optimization represents a major opportunity. Advanced software solutions can allow healthcare providers to monitor device performance and patient outcomes in real-time, enabling proactive adjustments to stimulation parameters. This personalized approach can improve therapeutic efficacy, reduce the need for in-person clinic visits, and enhance the overall patient experience. Manufacturers that develop integrated digital ecosystems around their neurostimulation hardware are likely to lead the next phase of market innovation and differentiation.

Accelerating Clinical Transition toward Long-Life Rechargeable Sacral Neuromodulation Systems

A prominent trend in 2026 is the accelerating transition toward long-life rechargeable sacral neuromodulation systems. This shift is driven by the desire to eliminate the need for surgical battery replacements and to provide patients with smaller, more comfortable implants. Modern rechargeable systems offer significantly longer device lifespans, often exceeding 15 years, and feature rapid, patient-friendly charging mechanisms. This trend is particularly strong among younger and more active patients who seek a sustainable, long-term solution for their bladder or bowel dysfunction, reflecting a broader market shift toward therapy longevity and patient comfort.

Migration of SNM Procedures to Specialized Pelvic Health Clinics and Ambulatory Surgical Centers (ASCs)

The market is witnessing an increasing trend toward the migration of sacral neuromodulation procedures from hospital operating rooms to specialized pelvic health clinics and ambulatory surgical centers (ASCs). This shift is enabled by the development of simplified, more ergonomic implant tools and the growing clinical preference for minimally invasive, outpatient-based care. Specialized centers offer a more efficient procedural workflow and can provide high-quality care at a lower cost than traditional hospital settings. This trend is reshaping the competitive landscape, as manufacturers increasingly focus on providing comprehensive solutions and support services tailored to the needs of outpatient facilities.

Analysis by Product Type

Based on product type, the non-rechargeable sacral neuromodulation devices segment is expected to hold the largest share of the global sacral neuromodulation market in 2026. This leadership is substantiated by the established long-term clinical track record of primary cell systems and a strong patient preference for 'set-and-forget' devices that do not require regular maintenance. However, the rechargeable sacral neuromodulation devices segment is projected to register the highest CAGR during the forecast period. The demand for miniaturized implants and the clinical benefit of a significantly longer device lifespan (up to 15-20 years) are driving rapid adoption among younger, active patients seeking sustainable, long-term therapy.

Analysis by Application

By application, the urinary incontinence segment is expected to hold the largest share in 2026. This is driven by the high global prevalence of refractory overactive bladder and the position of SNM as a standard third-line therapy in clinical guidelines. However, the fecal incontinence segment is projected to register the highest CAGR during the forecast period. Increasing clinical awareness, reduced social stigma, and an expanding body of evidence supporting SNM's efficacy in bowel control are significantly accelerating adoption in this application area.

Analysis by End User

By end user, the hospitals segment is expected to hold the largest share in 2026, as the primary setting for complex neurostimulation implants requiring sterile environments and comprehensive surgical support. However, the specialized clinics & ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward minimally invasive, outpatient-based procedures and the development of simplified implant tools are enabling specialized centers to offer SNM therapy more efficiently.

Largest Share: North America

North America is expected to dominate the global sacral neuromodulation market in 2026. This leading position is attributed to its advanced healthcare infrastructure, high awareness of pelvic floor disorders, and favorable reimbursement landscape, specifically CMS coverage in the U.S. The region benefits from the presence of industry leaders like Medtronic and Axonics and the early adoption of new technologies like MRI-compatible rechargeable devices. Data from the National Institutes of Health (NIH) and the American Urological Association (AUA) indicate a high and consistent demand for SNM therapy among patients with refractory bladder and bowel issues.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global sacral neuromodulation market during the forecast period. This rapid expansion is driven by an aging population, rising healthcare expenditures, and increasing awareness of advanced urological treatments in countries like China, India, and Japan. The expansion of specialized pelvic health centers and the entry of global manufacturers into these high-growth markets are significantly accelerating adoption. Clinical reports from regional urological societies highlight a significant surge in the adoption of neurostimulation therapies across major APAC economies.

The global sacral neuromodulation market is characterized by intense competition between established neurostimulation giants and innovative pelvic health firms. Competition is primarily focused on enhancing the longevity and safety of implants and improving the patient experience through miniaturization and simplified maintenance. Key players are investing heavily in R&D to develop next-generation MRI-compatible systems and high-performance rechargeable platforms to capture the growing outpatient market. Strategic developments often involve acquisitions of specialized neurostimulation technology firms and partnerships with leading pelvic health clinics to validate new treatment protocols. Furthermore, there is a growing focus on providing integrated digital solutions that combine remote patient monitoring, data analytics, and personalized therapy adjustment. Manufacturers are also increasingly focusing on comprehensive clinical training programs and patient support services to ensure the successful implementation of their technologies in diverse healthcare settings, which is critical for maintaining market leadership in this rapidly evolving field.

Medtronic plc, Axonics, Inc. (Acquired by Boston Scientific), Boston Scientific Corporation, Laborie Medical Technologies Corp., Abbott Laboratories, Nevro Corp., Johnson & Johnson (Ethicon/Biosense Webster), LivaNova PLC, Biotronik SE & Co. KG, Mainstay Medical, Saluda Medical, Nalu Medical, Inc., BlueWind Medical, Valencia Technologies, StimGuard, Cogentix Medical, Uroplasty, Inc., Cyberonics, Inc., St. Jude Medical, Nuvectra Corporation.

The global market is estimated at USD 1.37 billion in 2026, with a projected growth to USD 3.92 billion by 2036, at a CAGR of 11.1%.

Primary drivers include the rising global incidence of refractory pelvic floor disorders and the rise of miniaturized, MRI-compatible neurostimulation systems.

Major restraints include the high capital costs of neurostimulation therapy and the complex regulatory and reimbursement hurdles in global markets.

Opportunities lie in the expansion into emerging pelvic health markets and the integration of digital health platforms for remote patient monitoring.

Non-rechargeable devices are expected to hold the largest share due to their established clinical record and patient preference for maintenance-free systems.

Rechargeable sacral neuromodulation devices are projected to grow at the fastest CAGR, driven by miniaturization and longer device lifespans.

Urinary incontinence is expected to hold the largest share, supported by high global prevalence and its position as a standard third-line therapy.

North America is expected to dominate the market due to advanced infrastructure, high awareness, and favorable reimbursement policies.

Asia-Pacific is projected to witness the fastest growth, fueled by an aging population and increasing awareness of advanced urological treatments.

Key trends include the shift toward long-life rechargeable implants and the migration of procedures to specialized pelvic health clinics and ASCs.

Published Date: Jan-2025

Published Date: Dec-2017

Published Date: Sep-2024

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates