Resources

About Us

Modular Power Pods Market by Power Source (Battery Energy Storage Pods, Diesel & HVO Generator Pods), Capacity (Below 100 kVA, 100-500 kVA), Application (Primary Power, Backup & Standby Power), End-User Industry (Data Centers & Colocation, Oil & Gas) - Global Forecast to 2036

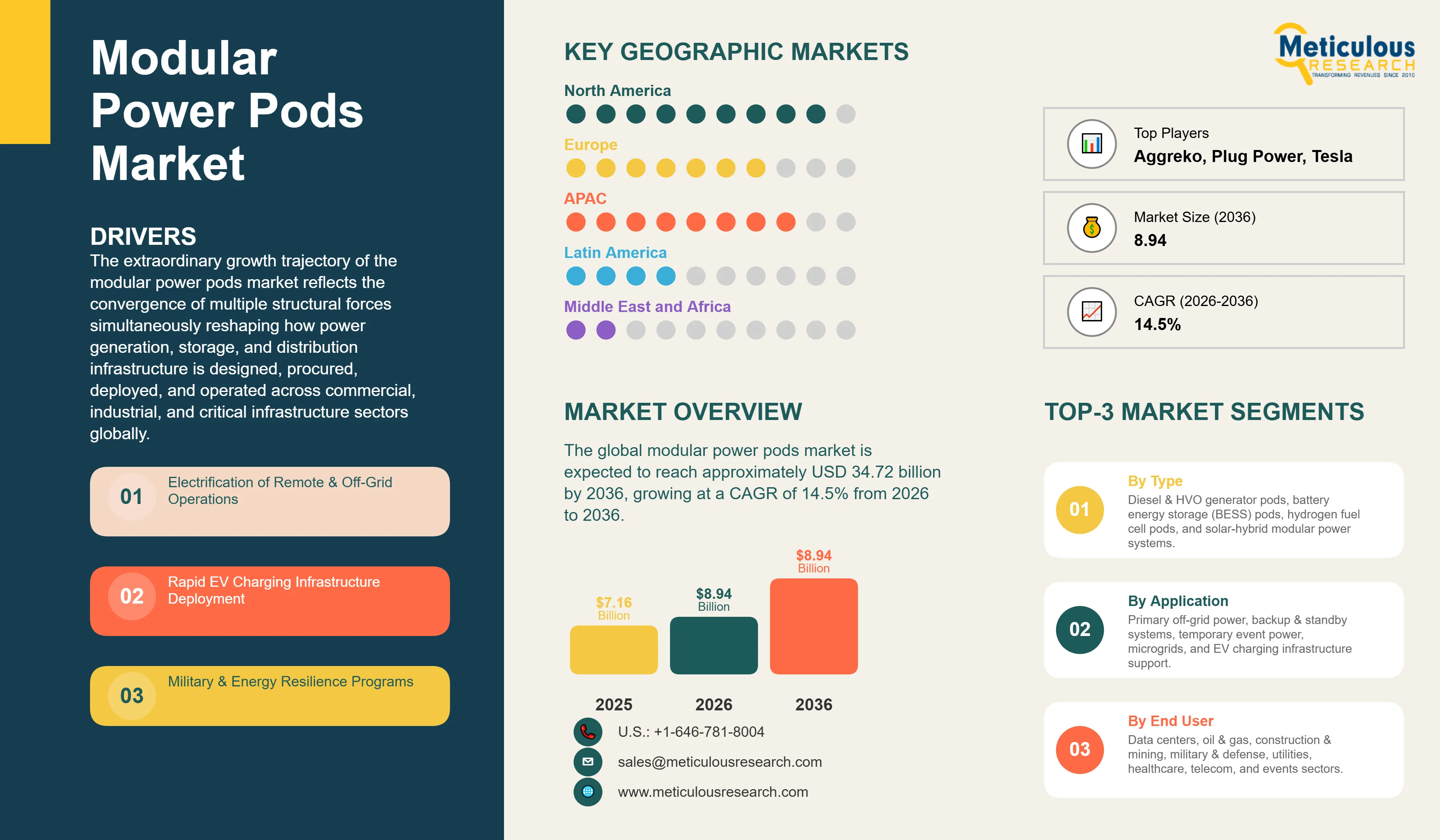

Report ID: MRSE - 1041835 Pages: 298 Mar-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global modular power pods market was valued at USD 7.16 billion in 2025. The market is expected to reach approximately USD 34.72 billion by 2036 from USD 8.94 billion in 2026, growing at a CAGR of 14.5% from 2026 to 2036. The extraordinary growth trajectory of the modular power pods market reflects the convergence of multiple structural forces simultaneously reshaping how power generation, storage, and distribution infrastructure is designed, procured, deployed, and operated across commercial, industrial, and critical infrastructure sectors globally. Modular power pods — factory-assembled, self-contained power generation or energy storage systems integrated within standardized containerized or skid-mounted enclosures incorporating the generator or battery system, switchgear, monitoring electronics, cooling, safety systems, and connectivity interfaces as a fully tested and commissioned unit — deliver fundamentally different deployment economics compared to conventional field-constructed power infrastructure through dramatic reductions in installation time, civil engineering cost, and commissioning complexity. The addressable market for modular power pods spans an extraordinarily diverse range of applications — from temporary construction site power replacing diesel road tankers with clean hybrid systems, through permanent distributed generation for off-grid industrial operations, to multi-megawatt data center power infrastructure where modular pods enable capacity expansion without the 18-24 month construction timelines constraining conventional power infrastructure procurement. The electrification of remote and off-grid industrial operations, the data center capacity explosion driven by artificial intelligence workload growth, the global push for rapid EV charging infrastructure deployment, and the military's embrace of expeditionary power modularity collectively represent a multi-hundred-billion dollar addressable market that modular power pod technology is uniquely positioned to address through its combination of deployment speed, operational flexibility, and increasingly competitive lifecycle economics.

Modular power pods represent a manufacturing and deployment philosophy that applies containerization and factory assembly principles to power infrastructure — treating generating capacity, energy storage, and associated power electronics as discrete, standardized modules that can be manufactured in controlled factory environments, tested to full performance specifications before shipment, transported to deployment sites on standard flatbed trucks or by helicopter, and commissioned in hours to days rather than the months required for field-constructed power infrastructure. The standardized containerized format — most commonly based on ISO shipping container dimensions of 20-foot and 40-foot footprints, though purpose-designed skid-mounted and trailer-mounted configurations address specific application requirements — enables the entire power infrastructure supply chain including transport logistics, site preparation, stacking and interconnection, and eventual redeployment to be planned around a common physical standard that dramatically simplifies project execution across diverse geographies and site conditions.

The modular power pod technology landscape encompasses several distinct power source categories serving different performance requirements and application contexts. Diesel and HVO (hydrotreated vegetable oil) generator pods represent the most mature and widely deployed technology, incorporating single or multiple diesel generator sets within weatherproof, sound-attenuated enclosures with integrated fuel tanks, automatic transfer switching, remote monitoring systems, and all necessary ancillary systems for autonomous operation. Battery energy storage pods integrate lithium-ion battery systems — predominantly lithium iron phosphate chemistry for its superior cycle life, thermal stability, and safety profile — with power conversion systems, battery management electronics, thermal management, and communications interfaces enabling flexible deployment for backup power, peak shaving, frequency regulation, and increasingly as standalone primary power sources in solar hybrid configurations. Natural gas and hydrogen fuel cell pods represent an emerging and rapidly growing category addressing the decarbonization imperative while maintaining the continuous power availability that battery-only systems cannot provide at equivalent cost for multi-day outages. Solar hybrid pods — integrating rooftop or integrated photovoltaic panels with battery storage and optional diesel backup within a containerized system — address remote electrification applications where fuel logistics costs make solar generation economically compelling even at modest sunshine levels.

The competitive landscape of the modular power pods market spans established power equipment manufacturers, specialist containerized power system integrators, and emerging clean energy pod developers. Traditional generator manufacturers including Aggreko, Atlas Copco Power Technique, Caterpillar (CAT Power Systems), Cummins, Kohler Power, and Generac have developed containerized genset pod product lines extending their conventional generator product portfolios into the modular deployment format. Specialist modular power integrators including Power Innovations International, KOHLER Rental Power, Altaaqa Global (a Caterpillar subsidiary), and PowerSecure develop customized containerized power solutions for specific application segments. Battery storage pod specialists including Tesla Energy (Megapack containerized configurations), Fluence, BYD, and CATL are driving the clean energy pod segment with large-format battery pod systems primarily targeting grid-scale and data center applications. Military power pod specialists including DRS Technologies (Leonardo DRS), SFC Energy, and Bren-Tronics develop ruggedized expeditionary power systems meeting military-specification environmental and electromagnetic compatibility requirements.

AI-Driven Data Center Power Demand Creating Unprecedented Modular Deployment Urgency

The artificial intelligence computing revolution — driving exponential growth in data center electricity demand as hyperscale operators deploy massive GPU clusters for AI model training and inference — has created a uniquely powerful growth catalyst for modular power pods by generating power infrastructure procurement urgency that conventional construction timelines fundamentally cannot satisfy. Hyperscale data center operators including Microsoft, Google, Amazon Web Services, and Meta are announcing data center campus investments of USD 5-20 billion each over 3-5 year periods, with electricity demand growth of 20-40% annually at established campuses requiring power capacity additions that must be operational within months — not the 18-24 months required for conventional transformer substations and generator hall construction. Modular power pods — pre-assembled, factory-tested, and deliverable within 8-16 weeks from order — address this temporal mismatch by enabling rapid power capacity additions that maintain alignment with accelerating GPU deployment schedules. Microsoft's Azure campus expansions, Google's data center modernization programs, and the hyperscale colocation operators including Equinix and Digital Realty have deployed multi-megawatt modular UPS and backup generator pod configurations specifically to accelerate capacity availability while permanent infrastructure construction proceeds. The shift toward liquid cooling for AI GPU clusters — with rack power densities increasing from 10-20 kW per rack to 60-120 kW per rack for high-performance AI servers — creates additional power pod demand for precision cooling infrastructure integrated with power systems, as the thermal management requirements of ultra-dense AI computing demand close integration of power delivery and cooling capability that modular pod systems can provide more efficiently than distributed conventional infrastructure.

Hybrid and Hydrogen Fuel Cell Pod Commercialization Accelerating Decarbonization

The commercial maturation of hybrid modular power pods combining renewable generation, battery storage, and low-carbon fuel generation — alongside the emergence of hydrogen fuel cell pods as a genuinely competitive zero-emission primary power solution — is transforming the sustainability profile of the modular power market while expanding the addressable applications beyond the diesel generator replacement incumbent. Solar-diesel-battery hybrid pods have demonstrated 40-80% fuel consumption reductions compared to diesel-only operation in remote mining, oil and gas, and construction applications where solar resources are adequate — creating compelling total cost of ownership advantages through fuel savings that offset the higher capital cost of hybrid systems within 2-4 year payback periods even in fuel-accessible locations, with substantially faster payback in remote locations where fuel delivery costs add USD 0.50-2.00 per liter to the pump price. Hydrogen fuel cell pods — utilizing proton exchange membrane fuel cells consuming hydrogen gas to generate electricity with zero direct emissions and water as the only by-product — have reached commercial deployment readiness for stationary power applications, with companies including Ballard Power Systems, Plug Power, Cummins Fuel Cell Technologies, and AFC Energy offering containerized fuel cell power systems targeting telecoms backup power, remote industrial sites, and military forward operating base electrification. The UK's Net Zero Strategy, the EU's Hydrogen Strategy, and the US Inflation Reduction Act's clean hydrogen production tax credits collectively create policy-driven economic incentives for hydrogen fuel cell pod adoption that are accelerating the transition from diesel generator pods in applications where zero-emission operation is a regulatory or commercial requirement. Ammonia-to-hydrogen cracker pod technology — enabling on-site hydrogen production from liquid ammonia, which has much higher volumetric energy density than compressed or liquid hydrogen — is advancing toward commercial deployment, potentially addressing the hydrogen logistics challenge that has limited fuel cell pod adoption in remote locations where gaseous hydrogen supply chain infrastructure does not exist.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 34.72 Billion |

|

Market Size in 2026 |

USD 8.94 Billion |

|

Market Size in 2025 |

USD 7.16 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Power Source, Capacity, Application, End-User Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Electrification of Remote Operations and Off-Grid Industrial Activity

The primary structural driver of modular power pod market growth is the accelerating electrification of remote and off-grid industrial operations — particularly mining, oil and gas upstream production, forestry, and construction — where modular power pods enable comprehensive site electrification without the transmission grid extension investment that is economically prohibitive at distances exceeding 10-50 kilometers from existing infrastructure depending on load size. The global mining industry's rapid electrification programs — driven by the dual imperatives of reducing diesel fuel operating costs (representing 15-30% of total mining operating costs at remote diesel-dependent sites) and meeting increasingly stringent emissions targets in jurisdictions including Canada, Australia, and Chile — are creating substantial modular power pod demand as mines deploy distributed power pods to replace diesel truck haulage electricity, power underground ventilation fans, and electrify fixed processing infrastructure. The oil and gas industry's remote upstream operations — wellpads, compressor stations, and gas processing facilities located far from grid infrastructure — have historically been exclusively diesel powered, but regulatory pressure to reduce methane flaring, operational pressure to reduce fuel costs, and the availability of natural gas at production facilities as a low-cost fuel for gas generator pods is driving a significant shift toward modular natural gas generator pods and solar-battery-gas hybrid systems. Construction mega-projects — infrastructure developments including tunnels, bridges, highways, dams, and urban development schemes in locations where grid power is unavailable or inadequate for construction equipment loads — represent a large and growing demand center for temporary modular power pods, with project durations of 3-7 years justifying significant investment in modular power infrastructure that can be deployed rapidly, reconfigured as construction phases progress, and redeployed to subsequent projects at the conclusion of each engagement.

Opportunity: EV Charging Infrastructure Rapid Deployment Applications

The global electric vehicle charging infrastructure buildout — requiring tens of millions of charging points worldwide by 2030 across highway corridors, urban parking, commercial fleets, and consumer residences — creates a substantial and rapidly growing market opportunity for modular power pods in locations where grid capacity constraints, high grid connection costs, or insufficient grid infrastructure prevent conventional hardwired EV charging installation at the required power levels. Highway corridor fast charging stations requiring 1-4 MW of total charging capacity in locations where distribution grid infrastructure is inadequate for direct connection represent a particularly compelling modular power pod application: battery storage pods pre-charged during low-demand grid periods or by co-located solar panels can deliver ultra-fast charging capability at locations with limited grid power availability, with the modular format enabling rapid site commissioning compared to months-long grid upgrade timelines. Electric fleet charging depots — truck and bus fleets transitioning to battery electric drivetrains requiring megawatt-scale charging infrastructure at depot locations that may have limited grid capacity — represent a major commercial opportunity where modular battery storage pods acting as demand charge management buffers enable fleet operators to manage peak demand charges that would otherwise make EV fleet economics unworkable. The US Department of Transportation's National Electric Vehicle Infrastructure program, the EU's Alternative Fuels Infrastructure Regulation mandating dense highway fast charging networks, and similar national programs globally are directing tens of billions in EV charging investment that modular power pod solutions are positioned to address across the segments where grid infrastructure constraints create barriers to conventional charging deployment.

Why Do Diesel and HVO Generator Pods Lead the Market?

Diesel and HVO generator pods command approximately 42-46% of total modular power pods market revenue in 2026, reflecting the technology's established market dominance across the full range of primary, backup, and temporary power applications where the combination of high energy density, fuel availability, operational simplicity, and proven reliability make diesel generation the default specification for modular power deployments. The containerized diesel genset format — integrating Cummins, Caterpillar, Perkins, MTU, or Volvo Penta diesel engines with Stamford, Leroy-Somer, or Marathon generators, Deepsea or ComAp automatic control systems, integrated fuel tanks for 8-72 hours autonomous operation, and all ancillary systems within weatherproof acoustic enclosures — has been refined over decades into highly reliable, standardized products available from multiple manufacturers with extensive global support networks. HVO fuel compatibility has significantly extended the environmental acceptability of diesel pod deployments: HVO — a renewable diesel produced from waste fats and vegetable oils — is a drop-in diesel replacement reducing lifecycle CO2 emissions by 70-90% compared to fossil diesel in existing diesel engines without modification, enabling diesel pod operators to achieve substantial carbon footprint reductions while maintaining the operational flexibility and energy density of liquid fuel systems. Battery energy storage pods represent the fastest-growing power source category at approximately 20-22% CAGR, driven by declining lithium-ion battery costs — utility-scale LFP battery system prices declining to USD 80-120/kWh in 2026 from USD 250-350/kWh in 2020 — enabling battery pod systems to achieve grid parity with diesel generation for backup and short-duration primary power applications while delivering operational cost and emissions advantages that are driving progressive displacement of diesel-only backup power systems across telecoms, data center, and commercial facility applications.

How Does the 100-500 kVA Segment Dominate?

The 100-500 kVA capacity segment commands approximately 34-38% of total modular power pods market revenue in 2026, serving the broadest commercial application range including construction site power, telecoms tower clusters, small data center UPS and backup systems, commercial facility temporary power, and light industrial off-grid primary generation. This capacity range corresponds to the power requirements of the majority of modular power applications — a typical mid-size construction site requires 200-400 kVA of peak power, a cluster of 5-10 telecoms towers typically requires 100-250 kVA, and a small commercial data center requires 200-500 kVA of UPS and backup capacity — making 100-500 kVA the most universally applicable modular pod capacity class with the deepest product ecosystems and most competitive pricing from multiple established manufacturers. The below 100 kVA segment serves residential and small commercial applications including telecoms single-tower backup, remote monitoring stations, small construction camps, and military portable power, with lightweight trailer-mounted and skid configurations enabling single-person deployment and operation in the most austere environments. The 500 kVA to 2 MVA segment is the fastest-growing capacity class at approximately 17-19% CAGR, driven primarily by data center modular power infrastructure deployments where individual power pod clusters of 1-2 MVA are deployed as scalable building blocks enabling incremental capacity expansion aligned with IT load growth, and by large mining and oil and gas operations requiring multi-hundred-kilowatt primary power for drilling rigs, processing equipment, and camp facilities. The above 2 MVA segment serves hyperscale data center, large industrial facility, and utility-scale grid stabilization applications, with multi-megawatt battery pod installations and large generator pod arrays configured in power pod clusters managed as unified generation and storage systems.

How Does Data Center Application Drive Market Growth?

The data centers and colocation application represents approximately 28-32% of total modular power pods market revenue in 2026 and demonstrates the highest growth rate among all application segments at approximately 19-21% CAGR, driven by the structural mismatch between conventional power infrastructure construction timelines and the rapidly accelerating power capacity demands of AI computing workloads that require modular solutions enabling capacity addition in weeks rather than years. Primary power applications — where modular generator or battery pods serve as the main power source for off-grid facilities lacking access to utility grid infrastructure — represent the largest application segment by deployed capacity in remote and developing region contexts, encompassing mining operations, oil and gas upstream facilities, telecommunications infrastructure in rural areas, and remote community power systems. Backup and standby power represents the most deeply established modular power pod application across data centers, hospitals, financial institutions, and critical government facilities, where containerized generator pods providing N+1 or 2N redundancy for UPS systems have been standard infrastructure for decades. Temporary and event power represents a large, distinctive application segment served by rental-oriented modular power pod fleets, encompassing construction sites, outdoor events and festivals, film and television production, emergency disaster relief, and planned utility maintenance outages where temporary power supply bridges the gap between normal grid supply and restoration. The EV charging infrastructure application is the fastest-emerging new application segment at approximately 25-27% CAGR, with modular battery pods providing grid-independent or grid-supplementary charging capability at highway fast charging locations, commercial fleet depots, and workplace charging installations where grid capacity constraints would otherwise prevent high-power charging deployment.

Why Do Data Centers Lead the End-User Market?

The data centers and colocation end-user segment commands approximately 26-30% of modular power pods market revenue in 2026, driven by the extraordinary power infrastructure investment associated with hyperscale AI data center buildout programs that collectively represent the largest capital expenditure cycle in the history of digital infrastructure. Hyperscale operators including Microsoft Azure, Google Cloud, Amazon Web Services, and Meta are deploying modular UPS battery pods and backup generator pod arrays as standard infrastructure components for new data center campus construction, with modular pod configurations providing the deployment speed, scalability, and electrical resilience required by the AI computing workloads that are transforming data center power requirements. The oil and gas end-user segment represents the second-largest revenue category, with major operators including Saudi Aramco, Shell, ExxonMobil, and BP deploying modular generator pods extensively across upstream exploration and production operations, pipeline compressor stations, and offshore platforms where modular power provides operational resilience and fuel flexibility advantages over conventional fixed generation infrastructure. Construction and mining represents a large and growing end-user segment where modular power pods serve as the primary power infrastructure for project sites ranging from urban high-rise construction to remote open-pit mining operations, with the temporary and redeployable nature of modular power perfectly matching the project lifecycle of construction and mining operations that require infrastructure mobilization and demobilization as projects progress. The military and defense end-user segment demonstrates consistent and growing procurement as armed forces globally prioritize energy resilience and operational independence through modular expeditionary power systems, with the US Department of Defense's Operational Energy Strategy explicitly targeting modular power pod adoption to reduce battlefield fuel logistics vulnerability and operational energy costs.

How is North America Maintaining Market Leadership?

North America holds approximately 36-40% of the global modular power pods market in 2026, supported by the world's most active hyperscale data center construction market — with Virginia's Northern Virginia data center corridor, Texas's emerging hub, and Pacific Northwest campuses collectively representing the highest concentration of modular power pod deployments globally — combined with the US military's substantial and sustained expeditionary power pod procurement programs and a highly developed oil and gas sector extensively utilizing modular power in Permian Basin, Eagle Ford, and Bakken shale operations. The US data center market's explosive growth — driven by AI infrastructure investment by Microsoft, Google, Amazon, Meta, and the major colocation operators — has created a modular power pod demand surge that is stretching delivery schedules at major suppliers to 20-40 weeks as manufacturing capacity struggles to keep pace with order volumes. Canada's remote mining sector in British Columbia, Ontario, and the Northwest Territories represents a significant modular power pod market, with nickel, copper, gold, and critical mineral mining operations deploying solar-diesel-battery hybrid pods to reduce diesel consumption costs and carbon footprints in operations far from grid infrastructure. The US military's Operational Energy initiative has driven multi-billion dollar procurement of modular power systems through programs including the Joint Expeditionary Power System, Small Tactical Power Generator replacement programs, and microgrid development at Forward Operating Bases, creating a substantial and technically demanding military modular power pod market served by specialized defense contractors.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 17-19% CAGR, driven by China's extraordinary data center and EV charging infrastructure investment, the rapid industrialization of remote resource regions across Australia and Southeast Asia, and India's growing construction and manufacturing sectors adopting modular power solutions. China's data center capacity expansion — driven by domestic AI development programs from Baidu, Alibaba, Tencent, and Huawei alongside national digital infrastructure investment plans — is creating massive modular power pod demand for both UPS battery pod systems and backup generator pod arrays, with domestic manufacturers including Shenzhen-based pod system integrators supplying the majority of Chinese market demand while international players compete in the premium technical specification segments. Australia's remote mining sector — operating iron ore, gold, copper, and lithium mines in some of the world's most resource-rich but grid-isolated regions of Western Australia and Queensland — has become a global showcase for solar-hybrid modular power pod deployments, with operations including Sandfire Resources and OZ Minerals deploying large-scale solar-battery-diesel hybrid microgrids demonstrating 60-80% diesel displacement that is attracting global mining industry attention. India's construction sector — undertaking massive infrastructure development programs including highways, metros, airports, and urban development across tier-2 and tier-3 cities where grid infrastructure is inadequate for construction power loads — is deploying modular generator pods extensively for project site electrification, creating a rapidly growing market for 100-500 kVA diesel pod rentals from domestic and international temporary power providers. Southeast Asian nations including Indonesia, Vietnam, and the Philippines are deploying modular power pods for telecoms tower backup and primary power in areas lacking reliable grid supply, as mobile network operators expand 4G and 5G coverage into rural regions where grid electricity is unreliable or absent.

The global modular power pods market features established power equipment manufacturers, specialist pod system integrators, and clean energy storage companies competing across the full spectrum of power source technologies and application segments. Aggreko plc and Atlas Copco Power Technique (including the Portable Energy division) lead the temporary and rental modular power pod market with global fleet assets serving construction, events, and industrial applications across 100+ countries. Caterpillar Inc. (CAT Electric Power, Altaaqa Global) and Cummins Inc. (Cummins Power Generation) provide large-scale diesel and gas generator pod solutions for permanent and semi-permanent industrial and data center applications. Kohler Power, Generac Holdings, and MTU Onsite Energy (Rolls-Royce Power Systems) serve commercial and industrial generator pod applications with standardized containerized product lines. In battery energy storage pods, Tesla Energy (Megapack), Fluence Energy, BYD Battery Energy Storage Systems, CATL (Electrochemical Energy Storage), and LG Energy Solution supply the large-format battery pod systems deployed for data center backup, grid stabilization, and renewable integration. Hydrogen and fuel cell pod developers including Plug Power, Ballard Power Systems, AFC Energy, and Cummins Fuel Cell Technologies represent the clean energy frontier of the market. Military-grade modular power pod specialists including Leonardo DRS, SFC Energy, and Bren-Tronics serve defense procurement with ruggedized expeditionary power systems meeting MIL-SPEC requirements. Specialist hybrid pod integrators including Power Innovations International, HAAS Alert, and regional specialists in Australia (e.g., Ampcontrol) and Europe (e.g., Martifer Energy) address specific application niches with custom-engineered hybrid energy solutions.

The global modular power pods market is expected to grow from USD 8.94 billion in 2026 to USD 34.72 billion by 2036.

The global modular power pods market is projected to grow at a CAGR of 14.5% from 2026 to 2036.

Diesel and HVO generator pods dominate with approximately 42-46% of revenue through established market leadership across primary, backup, and temporary power applications. Battery energy storage pods demonstrate the fastest growth at 20-22% CAGR driven by LFP battery cost declines making BESS pods increasingly competitive for backup and short-duration primary power while delivering zero-emission operation advantages.

Hyperscale AI computing workloads are driving 20-40% annual electricity demand growth at major data center campuses, creating power infrastructure procurement urgency that conventional construction timelines cannot satisfy. Modular power pods deliverable in 8-16 weeks versus 18-24 months for conventional infrastructure enable operators to maintain alignment between GPU deployment and power capacity availability, making modular pods the preferred solution for AI data center power expansion globally.

North America leads with approximately 36-40% of global market driven by the world's most active hyperscale AI data center construction market, US military expeditionary power programs, and extensive oil and gas sector modular power deployment. Asia-Pacific demonstrates the fastest growth at 17-19% CAGR driven by China's data center and EV charging investment, Australia's remote mining hybrid pod deployments, and India's construction sector modular power adoption.

The leading companies include Aggreko, Atlas Copco Power Technique, Caterpillar (Altaaqa Global), Cummins, Kohler Power, Generac, Tesla Energy (Megapack), Fluence Energy, BYD, CATL, Plug Power, Ballard Power Systems, Leonardo DRS, and specialist hybrid integrators serving specific application niches across temporary, permanent, military, and clean energy pod segments.

Published Date: May-2024

Published Date: May-2024

Published Date: Mar-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates