Resources

About Us

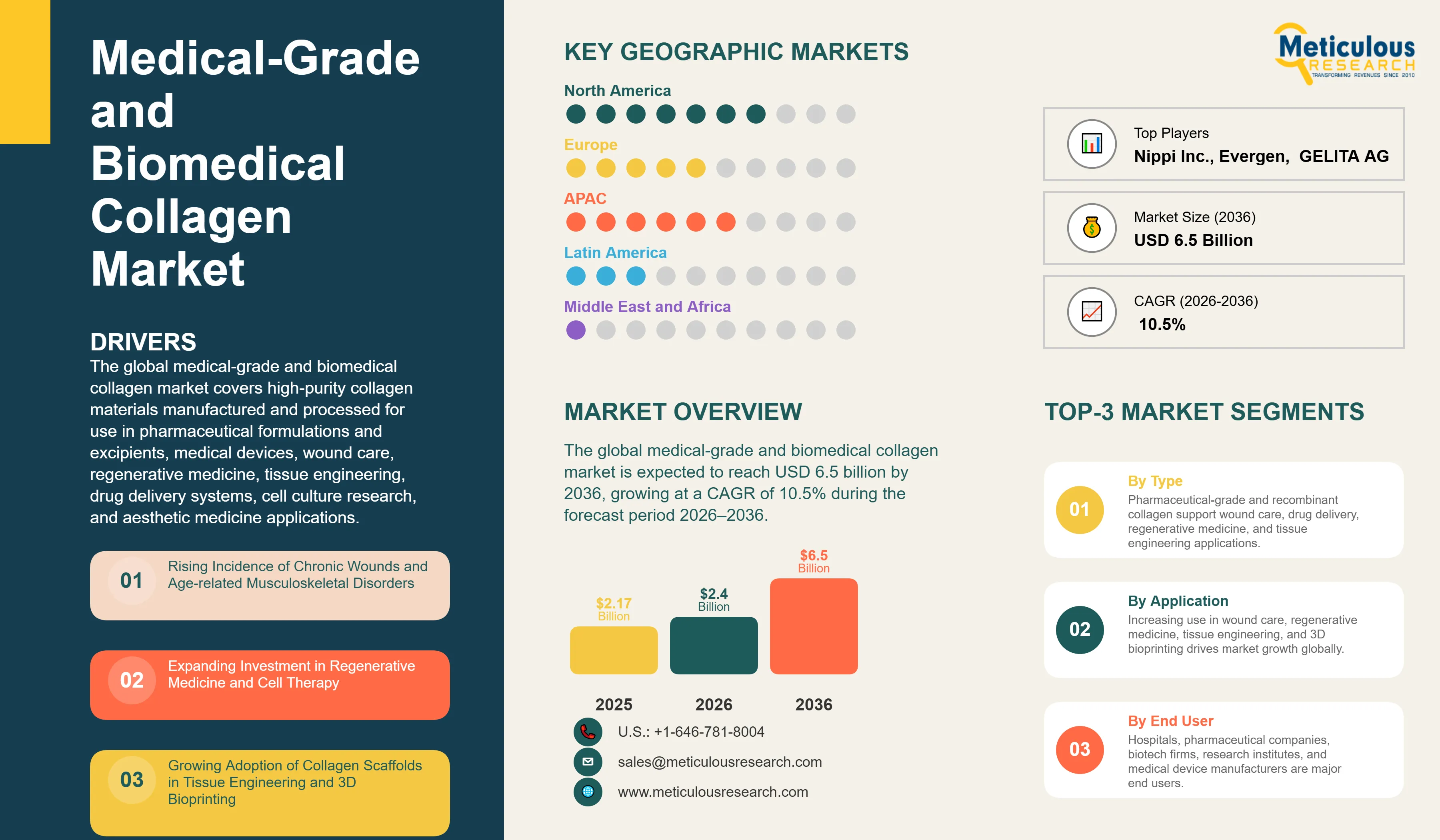

Medical-Grade and Biomedical Collagen Market Size, Share & Trends Analysis by Product Grade (Pharmaceutical-Grade, Medical Device-Grade), Source, Extraction Methodology, Physical Form, Application, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

Report ID: MRHC - 1041997 Pages: 378 May-2026 Formats*: PDF Category: Healthcare Delivery: 2 to 4 Hours Download Free Sample ReportThe global medical-grade and biomedical collagen market was valued at USD 2.4 billion in 2026. This market is expected to reach USD 6.5 billion by 2036, growing at a CAGR of 10.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global medical-grade and biomedical collagen market covers high-purity collagen materials manufactured and processed for use in pharmaceutical formulations and excipients, medical devices, wound care, regenerative medicine, tissue engineering, drug delivery systems, cell culture research, and aesthetic medicine applications. Unlike conventional collagen used in food, nutraceutical, or cosmetic products, medical-grade and pharmaceutical-grade collagen must meet stringent requirements for purity, biocompatibility, sterility, low endotoxin levels, and regulatory compliance, enabling its use in regulated healthcare settings.

The growth of the overall market is primarily driven by the increasing demand for advanced biomaterials in tissue repair, the rising adoption of collagen in pharmaceutical manufacturing and biologics research, and the growing investment in regenerative medicine and recombinant collagen technologies. The rising incidence of chronic wounds, an aging global population, and the growing prevalence of musculoskeletal disorders are expanding the clinical need for collagen-based biomaterials. In addition, growing investment in regenerative therapeutics, 3D bioprinting, and organ-on-chip technologies is accelerating the adoption of collagen in next-generation healthcare applications. The increasing use of collagen in drug delivery systems, microencapsulation, and GMP-compliant manufacturing for advanced therapy medicinal products (ATMPs) is further strengthening overall market demand.

However, the growth of this market is restrained by the high cost and complexity of medical-grade collagen production, stringent regulatory requirements, long product approval timelines, and challenges associated with raw material traceability and BSE/TSE risk management obligations. Moreover, maintaining standardized purity, immunogenicity, and structural integrity during large-scale production remains a persistent challenge for market participants operating across the divergent regulatory frameworks of the U.S., Europe, and Japan.

On the other hand, emerging opportunities in atelocollagen, marine collagen, recombinant and animal-free collagen, and specialized bioinks for 3D bioprinting are creating meaningful new growth avenues for market participants. The expanding commercial deployment of recombinant collagen platforms and the growing emphasis on sustainable biomaterial sourcing are expected to redefine competitive positioning across the value chain over the forecast period.

Recombinant and Animal-Free Collagen Gaining Strategic Momentum Across Clinical and Biomedical Applications

The shift toward recombinant and animal-free collagen is one of the most consequential developments currently reshaping the competitive and technological landscape of the medical-grade and biomedical collagen market. Growing concerns regarding zoonotic disease transmission, immunogenicity risks, and batch variability inherent to animal-derived collagen are accelerating both investment and commercialization activity in recombinant protein engineering and fermentation-based collagen production.

Recombinant collagen platforms offer significant advantages over conventional bovine or porcine sources, including the elimination of BSE/TSE risk, improved lot-to-lot consistency, and the ability to engineer customizable collagen sequences with defined biological functionality. These properties are particularly valuable in regenerative medicine, tissue engineering, cell therapies, and 3D bioprinting applications, where structural and immunological precision are critical to clinical performance.

The growing focus on sustainable and precision biomaterials in pharmaceutical and medical device manufacturing is further reinforcing demand for animal-free collagen grades. This trend is expected to attract continued investment and commercial scale-up activity over the forecast period, positioning recombinant collagen as a high-growth segment within the broader market.

3D Bioprinting and Organ-on-Chip Technologies Expanding Collagen's Role in Next-Generation Biomedical Platforms

The expanding adoption of 3D bioprinting and organ-on-chip platforms is opening a structurally new growth avenue for medical-grade collagen, extending its application well beyond traditional wound care and pharmaceutical excipient uses. Collagen-based bioinks are increasingly recognized as foundational materials for biofabrication processes, given their favorable gelation properties, biocompatibility, and ability to support cell adhesion, proliferation, and tissue organization within three-dimensional printed constructs.

Increasing investments in cell therapies, engineered tissue constructs, and personalized medicine platforms are accelerating demand for collagen materials that combine high biological functionality with the processing compatibility required for precision bioprinting workflows. The development of customized collagen architectures incorporating tunable mechanical properties and enhanced cellular signaling capabilities is further expanding the range of applications addressable through advanced collagen formats such as bioinks, fibers, and engineered collagen constructs.

This trend is expected to remain a key factor driving both product development activity and commercial market expansion throughout the forecast period, as biofabrication technologies continue to mature toward broader clinical and industrial adoption.

Growing Deployment of Collagen in Drug Delivery and Advanced Pharmaceutical Manufacturing

The increasing integration of collagen into drug delivery systems, microencapsulation platforms, and GMP-compliant manufacturing workflows for advanced therapy medicinal products is progressively strengthening demand for pharmaceutical-grade and specialty bioactive collagen across the broader pharmaceutical and biopharmaceutical sector. Collagen's natural biocompatibility, biodegradability, and favorable interactions with biological tissues make it well suited for controlled-release formulations, injectable drug carriers, and stabilization matrices for sensitive biologic compounds.

The expanding regulatory infrastructure for ATMPs in the U.S., Europe, and Japan is creating a more defined commercial pathway for collagen used in next-generation pharmaceutical manufacturing, reinforcing demand for high-purity, GMP-compliant collagen raw materials with validated safety and traceability profiles. This trend is expected to sustain steady demand growth within the pharmaceutical excipients and drug delivery application segments over the coming decade.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 6.5 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 10.5% |

|

Dominating Product Grade |

Pharmaceutical-Grade Collagen |

|

Fastest Growing Product Grade |

Recombinant/Synthetic Collagen (Animal-Free Medical Grade) |

|

Dominating Source |

Bovine |

|

Fastest Growing Source |

Recombinant/Fermentation-Derived (Animal-Free) |

|

Dominating Extraction Methodology |

Acid-Soluble Collagen |

|

Fastest Growing Extraction Methodology |

Advanced Green and Sustainable Extraction Technologies |

|

Dominating Physical Form |

Lyophilized Powder |

|

Fastest Growing Physical Form |

Other Advanced Formats (Bioinks, Fibers, Engineered Constructs) |

|

Dominating Application |

Wound Care |

|

Fastest Growing Application |

Regenerative Medicine |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on product grade, the global medical-grade and biomedical collagen market is segmented into pharmaceutical-grade collagen, medical device-grade collagen, research-grade collagen, recombinant/synthetic collagen (animal-free medical grade), and specialty bioactive collagen (atelocollagen/pepsin-soluble collagen).

In 2026, the pharmaceutical-grade collagen segment is expected to account for the largest share of the global medical-grade and biomedical collagen market. The large share of this segment is primarily attributed to the extensive use of pharmaceutical-grade collagen in excipients, capsule formulations, stabilizers, drug delivery systems, and injectable formulations, as well as its broad adoption across pharmaceutical manufacturing and wound care applications. Established regulatory pathways, large-scale production capabilities, and comparatively lower costs relative to specialty bioactive or recombinant collagen further support its dominant market position.

However, the recombinant/synthetic collagen (animal-free medical grade) segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is primarily driven by the increasing demand for animal-free biomaterials, advancements in recombinant protein engineering, and rising adoption in regenerative medicine, tissue engineering, 3D bioprinting, and next-generation medical devices. Concerns regarding zoonotic disease transmission, batch variability in animal-derived collagen, and the growing focus on sustainable and precision biomaterials are further accelerating investments and commercialization efforts in recombinant collagen technologies.

Based on source, the global medical-grade and biomedical collagen market is segmented into bovine, porcine, marine/fish, equine, recombinant/fermentation-derived (animal-free), and other sources.

In 2026, the bovine segment is expected to account for the largest share of the global medical-grade and biomedical collagen market. The large share of this segment is primarily attributed to the high collagen yield, favorable mechanical properties, and extensive historical use of bovine-derived collagen across wound care, medical devices, pharmaceutical formulations, tissue engineering, and regenerative medicine applications. Well-established extraction technologies, broad regulatory familiarity, comparatively lower production costs, and the widespread commercial availability of bovine dermis and tendon as raw materials continue to support the segment's dominance.

However, the recombinant/fermentation-derived (animal-free) segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is primarily driven by the increasing demand for highly reproducible and animal-free biomaterials, growing concerns regarding zoonotic disease transmission and immunogenicity associated with animal-derived collagen, and advancements in synthetic biology and recombinant protein production technologies.

Based on application, the global medical-grade and biomedical collagen market is segmented into wound care, tissue engineering, regenerative medicine, medical implants, drug delivery and microencapsulation, pharmaceutical excipient applications, cell culture and research, and cosmetic and aesthetic medicine.

In 2026, the wound care segment is expected to account for the largest share of the global medical-grade and biomedical collagen market. The large share of this segment is primarily attributed to the extensive use of collagen-based dressings, matrices, and scaffolds in chronic wound management, burn treatment, diabetic foot ulcers, pressure ulcers, and surgical wound healing applications. The growing prevalence of chronic diseases, an increasing aging population, rising volume of surgical procedures, and the proven ability of collagen to promote tissue regeneration and accelerated healing continue to support the dominant position of wound care within the broader application landscape.

However, the regenerative medicine segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is primarily driven by increasing adoption of cell therapies, stem cell research, tissue regeneration approaches, and advanced biomaterials designed to repair or restore damaged tissues and organs. Rising investments in regenerative therapeutics, expanding clinical research in tissue engineering, advancements in biomaterial science, and growing demand for personalized healthcare solutions are collectively accelerating the use of collagen in regenerative medicine applications.

Based on geography, the global medical-grade and biomedical collagen market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global medical-grade and biomedical collagen market. The large share of this region is primarily attributed to the strong presence of advanced healthcare infrastructure, high adoption of collagen-based wound care and regenerative medicine products, and significant investments in biomedical research, tissue engineering, and biopharmaceutical development. The presence of major medical device and biotechnology companies, favorable reimbursement frameworks, increasing prevalence of chronic wounds, and extensive research funding for regenerative therapies and biomaterials further support North America's dominant market position.

However, the Asia Pacific region is projected to register the highest CAGR during the forecast period. The rapid growth of this region is primarily driven by expanding healthcare expenditure, increasing demand for advanced wound care and regenerative medicine solutions, and growing investments in biotechnology, stem cell research, and biomedical manufacturing capabilities. The rising aging population, increasing volume of surgical procedures, improving access to advanced healthcare, and the emergence of China, Japan, South Korea, and India as major hubs for biomaterials research and medical manufacturing are accelerating adoption of medical-grade and biomedical collagen products across the region.

The competition within the global medical-grade and biomedical collagen market is primarily driven by product purity and regulatory compliance capabilities, manufacturing scalability, raw material sourcing strategies, and the depth of application-specific product portfolios across wound care, regenerative medicine, and pharmaceutical manufacturing end markets.

GELITA AG maintains a strong position through its broad portfolio of pharmaceutical and medical-grade gelatin and collagen products, supported by extensive GMP manufacturing infrastructure and long-standing relationships across pharmaceutical and medical device customer segments. Rousselot/Nextida holds a significant presence through its high-purity pharmaceutical-grade collagen and gelatin offerings, with a growing focus on biomedical and life sciences applications through dedicated product development programs.

Nippi Inc. and Koken Co., Ltd. occupy leading positions within the Japanese market and the broader Asia Pacific region, supported by specialized product portfolios for tissue engineering, regenerative medicine, and cell culture research applications. Integra LifeSciences maintains a strong finished-product presence through its established portfolio of collagen-based wound care and regenerative tissue products, while DSM-Firmenich Biomedical and Evonik Industries AG are advancing specialty collagen and biomedical polymer offerings targeting drug delivery and advanced therapy manufacturing applications.

Some of the key players operating in the global medical-grade and biomedical collagen market include GELITA AG (Germany), Rousselot/Nextida (Netherlands), Nitta Gelatin Inc. (Japan), Weishardt (France), Nippi Inc. (Japan), Koken Co., Ltd. (Japan), Advanced BioMatrix, Inc. (U.S.), Evergen Biotechnologies, Inc. (U.S.), Integra LifeSciences Corporation (U.S.), DSM-Firmenich Biomedical (Netherlands), Evonik Industries AG (Germany), and Guangdong Victory Biotech Co., Ltd. (China), among others.

The global medical-grade and biomedical collagen market is expected to reach USD 6.5 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 10.5% during the forecast period 2026–2036.

In 2026, the pharmaceutical-grade collagen segment is expected to hold the largest share of the global medical-grade and biomedical collagen market, driven by extensive use in pharmaceutical excipients, capsule formulations, drug delivery systems, and wound care applications.

The recombinant/synthetic collagen (animal-free medical grade) segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by increasing demand for animal-free biomaterials and growing adoption in regenerative medicine, tissue engineering, and 3D bioprinting applications.

In 2026, the bovine segment is expected to hold the largest share of the global medical-grade and biomedical collagen market.

In 2026, the wound care segment is expected to hold the largest share of the global medical-grade and biomedical collagen market.

The growth of this market is primarily driven by the rising incidence of chronic wounds and age-related musculoskeletal disorders expanding demand for collagen-based biomaterials, expanding investment in regenerative medicine and cell therapy, growing adoption of collagen scaffolds in tissue engineering and 3D bioprinting, increasing use of collagen in drug delivery and microencapsulation, and the expansion of GMP-compliant collagen supply for pharmaceutical and ATMP manufacturing.

Key players operating in the medical-grade and biomedical collagen market include GELITA AG (Germany), Rousselot/Nextida (Netherlands), Nitta Gelatin Inc. (Japan), Weishardt (France), Nippi Inc. (Japan), Koken Co., Ltd. (Japan), Advanced BioMatrix, Inc. (U.S.), Evergen Biotechnologies, Inc. (U.S.), Integra LifeSciences Corporation (U.S.), DSM-Firmenich Biomedical (Netherlands), Evonik Industries AG (Germany), Guangdong Victory Biotech Co., Ltd. (China), MiMedx Group, Inc. (U.S.), Organogenesis Holdings Inc. (U.S.), and Smith+Nephew plc (U.K.).

Asia Pacific is expected to register the highest growth rate in the global medical-grade and biomedical collagen market during the forecast period 2026–2036.

Published Date: Feb-2026

Published Date: Sep-2013

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates