Resources

About Us

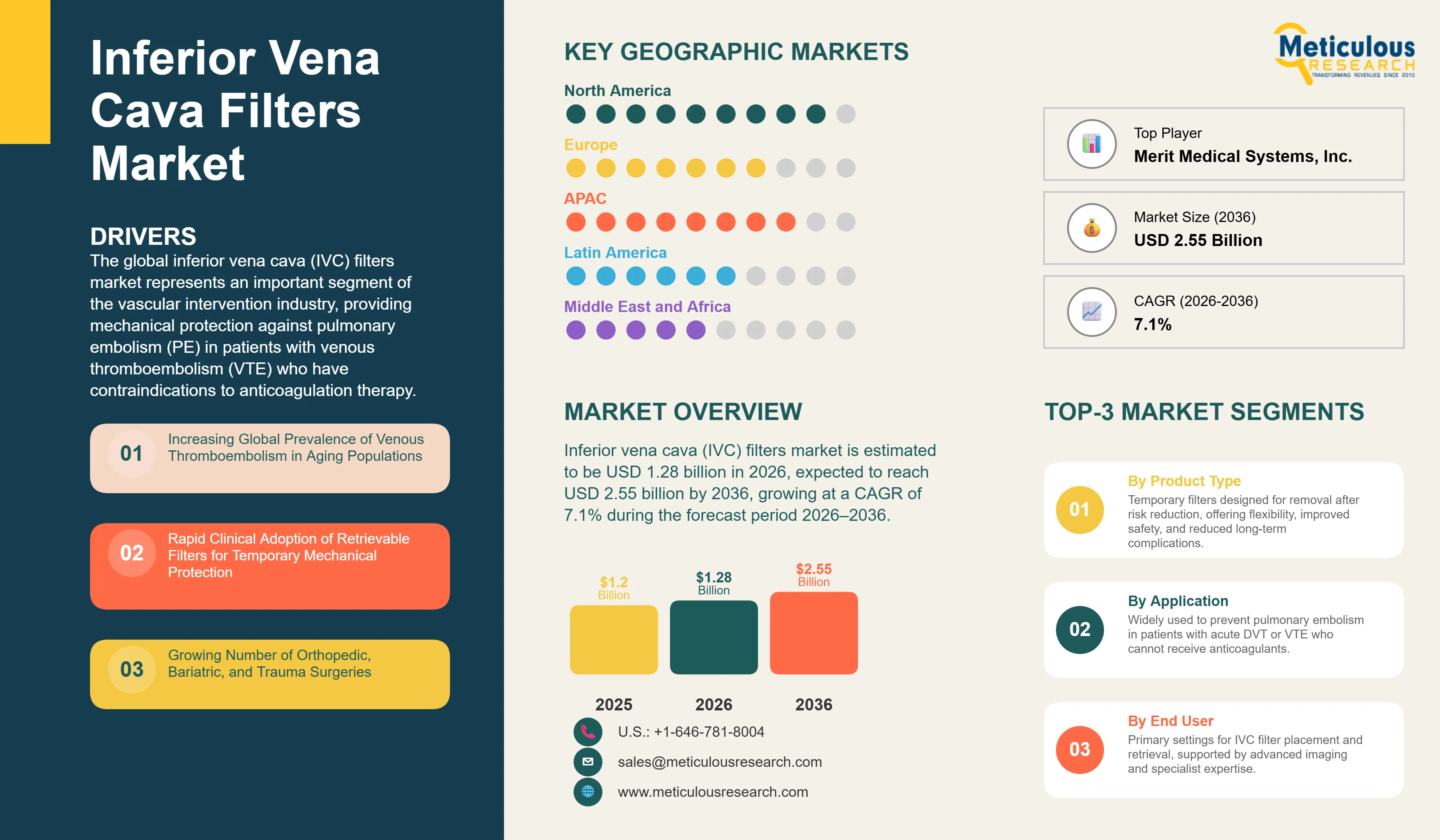

The global inferior vena cava (IVC) filters market is estimated to be USD 1.28 billion in 2026. This market is expected to reach USD 2.55 billion by 2036, growing at a CAGR of 7.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global inferior vena cava (IVC) filters market represents an important segment of the vascular intervention industry, providing mechanical protection against pulmonary embolism (PE) in patients with venous thromboembolism (VTE) who have contraindications to anticoagulation therapy. IVC filters are small metallic devices implanted within the inferior vena cava to capture thrombi originating from deep vein thrombosis (DVT) before they can migrate to the lungs. Demand for these devices is supported by the substantial global burden of VTE and the growing elderly population undergoing major orthopedic, bariatric, cancer, and trauma procedures. According to the U.S. Centers for Disease Control and Prevention (CDC), up to 900,000 people in the United States are affected by VTE annually, resulting in an estimated 60,000–100,000 deaths, while approximately one-quarter of pulmonary embolism cases present with sudden death as the first symptom. Furthermore, more than one-third of VTE cases are associated with recent hospitalization, highlighting the importance of prophylactic strategies in high-risk patients.

The market has evolved considerably with the transition from permanent filters toward retrievable and bioconvertible designs, which provide temporary protection during periods of elevated thromboembolic risk while reducing long-term complications. Current clinical practice guidelines issued by the Society of Interventional Radiology (SIR), developed in collaboration with the American Heart Association (AHA), American College of Cardiology (ACC), and other professional societies, recommend IVC filter placement primarily in patients with acute DVT or PE who cannot receive anticoagulant therapy or who develop contraindications to anticoagulation. The guidelines also emphasize structured follow-up and timely retrieval of temporary devices to minimize complications and improve clinical outcomes. Continued innovation aimed at enhancing filter stability, biocompatibility, and retrieval success is expected to support steady market growth over the forecast period.

Drivers: Rising VTE Incidence and the Shift Toward Versatile Retrievable Filter Systems

The growth of the global IVC filters market is primarily driven by the increasing clinical burden of venous thromboembolism and the widespread adoption of retrievable devices that offer improved patient safety profiles.

Increasing Global Prevalence of Venous Thromboembolism in Aging Populations

Venous thromboembolism (VTE), comprising deep vein thrombosis and pulmonary embolism, is a major global health concern, particularly among the elderly. As the global population ages, the incidence of VTE is rising due to increased comorbidities, higher rates of hospitalization, and more frequent major surgeries. In patients where pharmacological anticoagulation is contraindicated—such as those with active bleeding or high surgical risk—IVC filters provide a critical mechanical barrier against life-threatening PE. The growing number of patients requiring this specialized protection is a fundamental driver for the sustained demand for IVC filters across all major healthcare markets.

Rapid Clinical Adoption of Retrievable Filters for Temporary Mechanical Protection

The evolution of retrievable IVC filters has significantly expanded the market by addressing the long-term safety concerns associated with permanent implants. Retrievable filters offer the flexibility to provide protection during the acute phase of VTE and can be removed once the patient can safely resume anticoagulation. This versatility aligns with current clinical best practices that emphasize minimizing the duration of metallic implants in the venous system. The increasing procedural focus on timely retrieval and the development of devices with higher retrieval success rates even after extended dwell times are accelerating the adoption of these versatile systems over traditional permanent filters.

Restraints: Navigating Long-Term Device Complications and Increasing Regulatory Scrutiny

Despite their life-saving potential, the IVC filters market faces challenges related to long-term device complications and a rigorous regulatory environment focused on ensuring timely retrieval.

Concerns Regarding Long-Term Device Complications and Low Retrieval Rates

A major restraint for the market is the risk of long-term complications associated with IVC filters that are not retrieved, including filter migration, fracture, IVC perforation, and recurrent thrombosis. Historical data indicating low retrieval rates for temporary filters have led to significant clinical and regulatory concern. These complications have resulted in numerous legal challenges and a more cautious approach to filter placement among some clinicians. The need for robust follow-up programs to ensure retrieval remains a significant operational challenge for healthcare providers, potentially limiting the growth of prophylactic filter use.

Stringent Regulatory Oversight and FDA Safety Communications

The IVC filters market is subject to intense regulatory oversight, particularly following safety communications from the FDA and other global health authorities regarding the risks of leaving retrievable filters in place longer than necessary. These communications have led to more stringent indications for filter placement and a greater emphasis on documenting the clinical rationale for each procedure. While intended to improve patient safety, this increased scrutiny can lead to a more conservative use of IVC filters and higher administrative burdens for manufacturers and healthcare facilities, impacting overall market growth.

Opportunities: Expanding Prophylactic Use and Advancing Biocompatible Filter Technologies

Future growth opportunities in the IVC filters market are centered on expanding indications for prophylactic PE prevention and developing innovative, highly biocompatible device designs.

Expansion of Prophylactic Indications in High-Risk Surgical and Trauma Patients

There is a significant opportunity for market expansion in the prophylactic use of retrievable IVC filters for high-risk patients who do not yet have VTE but are at extreme risk of PE and cannot receive anticoagulation. This includes patients undergoing major bariatric or orthopedic surgeries and those with severe multi-system trauma. As more clinical evidence emerges supporting the safety and efficacy of short-term mechanical protection in these specific scenarios, the volume of prophylactic placements is expected to grow, offering a new pathway for market penetration beyond traditional therapeutic indications.

Development of Advanced Biocompatible and Easily Retrievable Filter Designs

Innovations in material science and device design present a major opportunity for manufacturers. The development of filters with improved biocompatibility and advanced structural designs that reduce the risk of migration and perforation can significantly enhance patient outcomes. Furthermore, creating devices that are easier to retrieve even in the presence of tilting or thrombus accumulation can address one of the biggest clinical hurdles in the market. Manufacturers that can provide next-generation filters with superior retrieval profiles are likely to gain a significant competitive advantage in an increasingly safety-conscious market.

Intensified Clinical Focus on Systematic Filter Retrieval Programs

A major trend in 2026 is the increasing adoption of structured IVC filter retrieval programs aimed at improving patient follow-up and reducing long-term device-related complications. This shift has been reinforced by the U.S. FDA, which issued safety communications recommending removal of retrievable filters once protection from pulmonary embolism is no longer required. In its 2020 clinical practice guideline, the Society of Interventional Radiology (SIR), in collaboration with the American Heart Association (AHA), American College of Cardiology (ACC), and Society for Vascular Surgery (SVS), recommended structured follow-up programs to enhance retrieval rates and detect complications. Studies cited by SIR indicate that retrieval rates historically remained below 50%, prompting hospitals to deploy automated registries and dedicated coordinators. The emphasis on complete placement-to-retrieval management is increasing procedural volumes and favoring devices with high retrieval success and long indwell reliability.

Rising Utilization of Specialized Outpatient Vascular Clinics for Elective Retrieval

The migration of elective IVC filter retrieval procedures toward specialized outpatient vascular centers and ambulatory settings is another important trend shaping the market. According to the U.S. Centers for Medicare & Medicaid Services (CMS), the number of procedures approved for Ambulatory Surgical Centers (ASCs) has expanded significantly over the past decade as healthcare systems pursue lower-cost care delivery. In parallel, the Centers for Disease Control and Prevention (CDC) estimates that up to 900,000 Americans experience venous thromboembolism annually, creating a substantial patient population requiring follow-up management. Specialized vascular clinics are increasingly performing elective retrieval procedures due to shorter procedure times, lower costs, and improved patient convenience. This transition is fostering integrated vascular care networks and supporting demand for retrieval systems and advanced filter technologies designed for efficient outpatient intervention.

Analysis by Product Type

Based on product type, the retrievable IVC filters segment is expected to hold the largest share of the global inferior vena cava filters market in 2026. This dominant position is driven by the superior clinical flexibility of these devices, which allow for temporary mechanical protection during acute risk periods without the permanent risks associated with long-term metallic implants. The ability to remove the filter once anticoagulation is safe aligns with the 'leave nothing behind' philosophy increasingly adopted in vascular care. Furthermore, the retrievable IVC filters segment is also projected to register the highest CAGR during the forecast period. The continuous refinement of retrieval techniques and the development of next-generation filters with improved retrieval success rates are accelerating the clinical shift away from permanent devices.

Analysis by Application

By application, the treatment of venous thromboembolism (VTE) segment is expected to hold the largest share in 2026. This segment's leadership is substantiated by the high prevalence of acute VTE in hospitalized and elderly populations, where IVC filters are a life-saving necessity for patients with contraindications to anticoagulation. However, the prophylactic PE prevention segment is projected to grow at the fastest CAGR during the forecast period. This growth is fueled by the expanding use of retrievable filters in high-risk surgical and trauma patients to prevent fatal PE during temporary periods of anticoagulation contraindication, representing a significant area of market expansion.

Analysis by End User

By end user, the hospitals & cardiac centers segment is expected to hold the largest share in 2026. The vast majority of IVC filter procedures are performed in hospital-based interventional radiology suites that have the necessary imaging technology and specialized expertise for both placement and complex retrieval. However, the specialty vascular clinics segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward performing elective retrieval procedures in outpatient settings to improve healthcare efficiency and reduce costs is driving the rapid growth of this specialized segment.

Geographic Analysis: North American Market Dominance and Asia-Pacific's Rapid Infrastructure Expansion

Largest Share: North America

North America is expected to dominate the global inferior vena cava (IVC) filters market in 2026, accounting for approximately 45–50% of global revenue. The region's leadership is supported by a high burden of venous thromboembolism (VTE), advanced interventional radiology infrastructure, and strong clinical guideline adoption. According to the U.S. Centers for Disease Control and Prevention (CDC), as many as 900,000 Americans experience VTE annually, resulting in an estimated 60,000–100,000 deaths. In addition, the American Joint Replacement Registry (AJRR) reported more than 3.7 million hip and knee arthroplasty procedures performed cumulatively in the United States through 2023, contributing to a large population at risk of postoperative thromboembolic events. Clinical practice guidelines published by the Society of Interventional Radiology (SIR), in collaboration with the American Heart Association (AHA), American College of Cardiology (ACC), and Society for Vascular Surgery (SVS), have further standardized the use and retrieval of IVC filters in appropriately selected patients. The presence of leading manufacturers and a highly developed healthcare infrastructure also reinforce the region's dominant position. Key companies operating in the North American market include Medtronic plc, Becton, Dickinson and Company (BD), Boston Scientific Corporation, Cook Medical, Cordis, and Argon Medical Devices, Inc.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global inferior vena cava filters market, with a CAGR of 8.9% during the forecast period. This rapid expansion is driven by the aging population in countries like Japan and China, increasing healthcare expenditure, and the modernization of hospital infrastructure. Growing awareness of pulmonary embolism as a preventable cause of hospital mortality is also a significant factor accelerating the adoption of advanced interventional procedures. Key companies operating in the Asia Pacific market are Terumo Corporation, Lifetech Scientific, and various regional partners for global medical device leaders.

The global inferior vena cava filters market is characterized by a concentrated competitive landscape featuring major global medical device corporations and specialized interventional players. Competition is primarily focused on improving the long-term safety and retrieval reliability of temporary filters. Key players are investing in advanced material technologies and structural designs that minimize the risk of filter tilting, migration, and perforation. There is also a significant emphasis on developing comprehensive follow-up and retrieval support systems to assist healthcare facilities in managing their filter programs. Strategic developments often involve acquisitions of smaller companies with innovative filter designs or specialized vascular access technologies. Furthermore, manufacturers are increasingly focusing on large-scale clinical registries to provide robust real-world data on the long-term performance and retrieval success of their devices, which is critical for gaining clinician trust and maintaining regulatory compliance in a safety-focused market.

Medtronic plc, Becton, Dickinson and Company (BD), Boston Scientific Corporation, Cook Medical, Argon Medical Devices, Inc., Cordis, B. Braun Melsungen AG, ALN International (ALN Implants Chirurgicaux), Koninklijke Philips N.V. (Philips Volcano), Terumo Corporation, Merit Medical Systems, Inc., Lifetech Scientific (Shenzhen) Co., Ltd., MicroPort Scientific Corporation, Rex Medical, L.P., Braile Biomédica S.A., Nipro Corporation, Shanghai Kindly Medical Instruments Co., Ltd., Zhejiang Shape Memory Alloy Co., Ltd., Qingdao Bright Medical Manufacturing Co., Ltd., Changzhou Zhiye Medical Devices Co., Ltd.

The global market is estimated at USD 1.28 billion in 2026, with a projected growth to USD 2.55 billion by 2036, at a CAGR of 7.1%.

Primary drivers include the rising incidence of VTE in aging populations and the shift toward versatile retrievable filter systems.

Major restraints include concerns regarding long-term device complications and stringent regulatory oversight focused on retrieval rates.

Opportunities lie in expanding prophylactic indications in high-risk patients and developing advanced biocompatible filter designs.

Retrievable IVC filters are expected to hold the largest share due to their clinical flexibility and reduced long-term safety risks.

Prophylactic PE prevention is projected to grow at the fastest CAGR, driven by its expanding use in high-risk surgical and trauma patients.

Hospitals & cardiac centers are expected to hold the largest share as the primary setting for specialized interventional procedures.

North America is expected to dominate the market due to high clinical awareness and established guidelines for PE prevention.

Asia Pacific is projected to witness the fastest growth, fueled by an aging population and modernization of hospital infrastructure.

Key trends include the prioritization of systematic filter retrieval programs and the growth of outpatient vascular centers.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Increasing Global Prevalence of Venous Thromboembolism in Aging Populations

4.2.1.2. Rapid Clinical Adoption of Retrievable Filters for Temporary Mechanical Protection

4.2.2. Restraints

4.2.2.1. Concerns Regarding Long-Term Device Complications and Low Retrieval Rates

4.2.2.2. Stringent Regulatory Oversight and FDA Safety Communications

4.2.3. Opportunities

4.2.3.1. Expansion of Prophylactic Indications in High-Risk Surgical and Trauma Patients

4.2.3.2. Development of Advanced Biocompatible and Easily Retrievable Filter Designs

4.2.4. Trends

4.2.4.1. Intensified Clinical Focus on Systematic Filter Retrieval Programs

4.2.4.2. Rising Utilization of Specialized Outpatient Vascular Clinics for Elective Retrieval

4.3. Porter's Five Forces Analysis

4.4. Regulatory Outlook and Reimbursement Landscape

4.5. Value Chain Analysis

5. Global Inferior Vena Cava Filters Market, by Product Type

5.1. Retrievable IVC Filters

5.2. Permanent IVC Filters

6. Global Inferior Vena Cava Filters Market, by Application

6.1. Treatment of Venous Thromboembolism (VTE)

6.2. Prophylactic PE Prevention

7. Global Inferior Vena Cava Filters Market, by End User

7.1. Hospitals & Cardiac Centers

7.2. Specialty Vascular Clinics

7.3. Ambulatory Surgical Centers (ASCs)

8. Global Inferior Vena Cava Filters Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Key Players Strategies

9.2. Market Share Analysis

9.3. Strategic Developments

9.4. Competitive Benchmarking

10. Company Profiles

10.1. Medtronic plc

10.2. Becton, Dickinson and Company (BD)

10.3. Boston Scientific Corporation

10.4. Cook Medical

10.5. Argon Medical Devices, Inc.

10.6. Cordis

10.7. B. Braun Melsungen AG

10.8. ALN International (ALN Implants Chirurgicaux)

10.9. Koninklijke Philips N.V. (Philips Volcano)

10.10. Terumo Corporation

10.11. Merit Medical Systems, Inc.

10.12. Lifetech Scientific (Shenzhen) Co., Ltd.

10.13. MicroPort Scientific Corporation

10.14. Rex Medical, L.P.

10.15. Braile Biomédica S.A.

10.16. Nipro Corporation

10.17. Shanghai Kindly Medical Instruments Co., Ltd.

10.18. Zhejiang Shape Memory Alloy Co., Ltd.

10.19. Qingdao Bright Medical Manufacturing Co., Ltd.

10.20. Changzhou Zhiye Medical Devices Co., Ltd.

11. Appendix

11.1. Abbreviations

11.2. Disclaimer

12. Key Questions Answered

Published Date: May-2024

Published Date: Jan-2025

Published Date: Jul-2026

Subscribe to get the latest industry updates