Resources

About Us

Immunotherapy Platforms Market by Platform Type (Checkpoint Inhibitors, CAR-T & Cellular Therapies), Indication (Oncology - NSCLC, Melanoma, Hematologic Malignancies), Molecule Type, and End User - Global Forecast to 2036

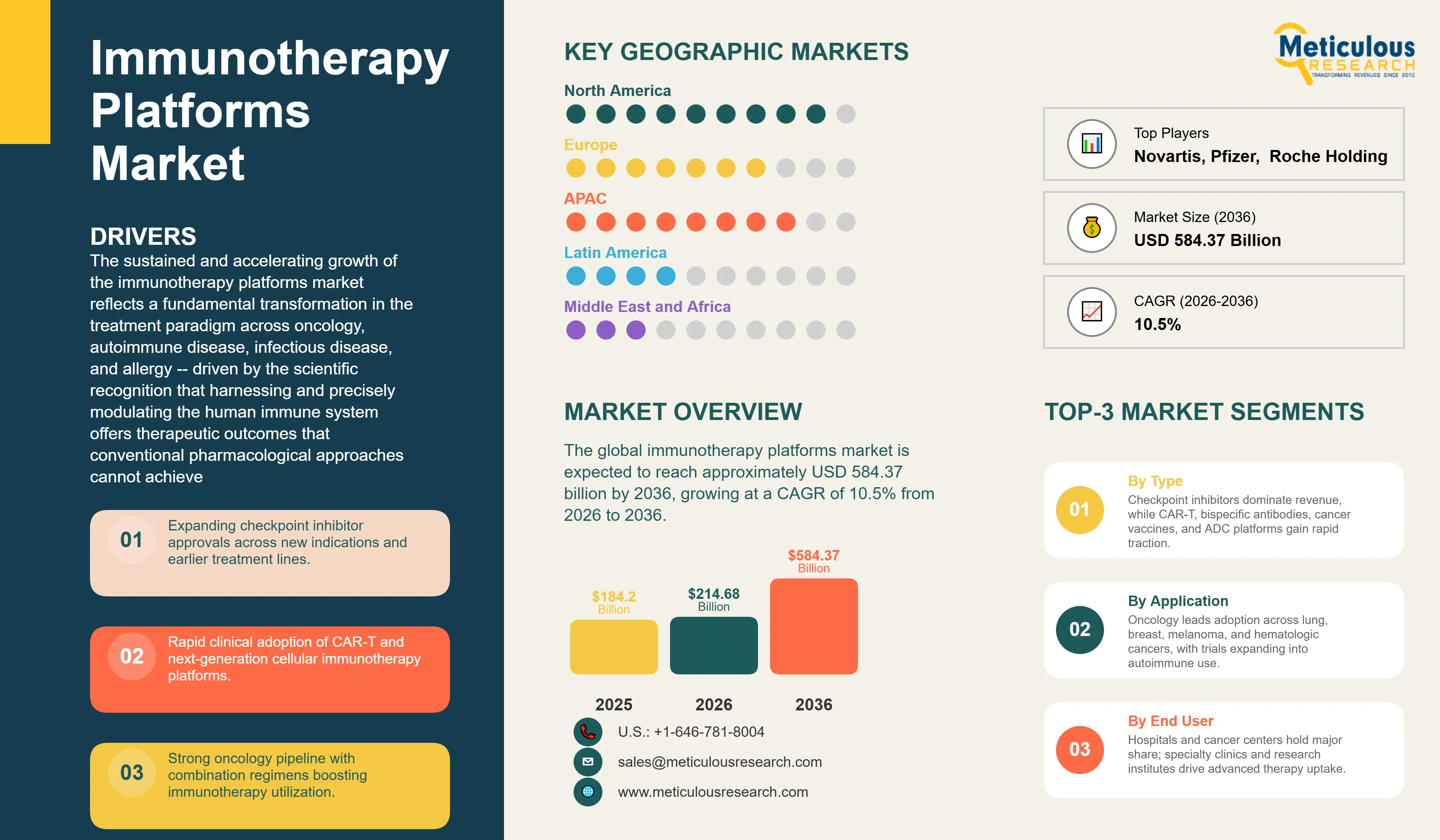

Report ID: MRHC - 1041838 Pages: 320 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global immunotherapy platforms market was valued at USD 184.20 billion in 2025. The market is expected to reach approximately USD 584.37 billion by 2036 from USD 214.68 billion in 2026, growing at a CAGR of 10.5% from 2026 to 2036. The sustained and accelerating growth of the immunotherapy platforms market reflects a fundamental transformation in the treatment paradigm across oncology, autoimmune disease, infectious disease, and allergy -- driven by the scientific recognition that harnessing and precisely modulating the human immune system offers therapeutic outcomes that conventional pharmacological approaches cannot achieve. Immunotherapy has progressed from a narrow set of cytokine therapies and early monoclonal antibodies in the 1990s to the most dynamic and commercially dominant segment of biopharmaceutical innovation, with checkpoint inhibitors, CAR-T cell therapies, cancer vaccines, bispecific antibodies, and antibody-drug conjugates collectively representing dozens of approved products and hundreds of clinical stage assets generating hundreds of billions in annual revenue across global markets. The structural shift toward immunotherapy as the dominant oncology treatment modality -- replacing or supplementing chemotherapy and radiotherapy across an expanding range of cancer types -- is being reinforced by durable response data demonstrating long-term survival benefits in subsets of patients that far exceed outcomes achievable with conventional treatments, creating compelling health-economic arguments for immunotherapy adoption despite high per-treatment costs. The emergence of next-generation immunotherapy platforms including personalized neoantigen cancer vaccines, tumor-infiltrating lymphocyte therapies, natural killer cell therapies, and gamma-delta T cell platforms is expanding the technology landscape beyond the checkpoint inhibitor and CAR-T paradigms that defined the first generation of immunotherapy commercialization, creating additional waves of innovation that will sustain market growth through the forecast period and beyond.

Immunotherapy platforms encompass the full range of therapeutic approaches that work by engaging, amplifying, redirecting, or modulating the immune system to treat disease - distinguishing themselves from conventional pharmacological approaches that directly target disease biology independent of immune involvement. The modern immunotherapy platform landscape is architecturally organized around several distinct mechanisms of action and technology classes that have achieved regulatory approval, clinical validation, or advanced development status: immune checkpoint blockade, adoptive cell therapies, therapeutic cancer vaccines, cytokine-based therapies, bispecific antibodies, antibody-drug conjugates with immunostimulatory payloads, oncolytic virotherapy, and innate immune agonists. The conceptual breakthrough underpinning checkpoint inhibitor development -- the demonstration by James Allison and Tasuku Honjo (2018 Nobel Laureates) that T cells could be released from tumor-imposed immunosuppression by blocking CTLA-4 and PD-1 co-inhibitory receptors, respectively - transformed oncology treatment paradigms and established the scientific foundation for an entire generation of immune checkpoint-targeting drug development that has expanded to include PD-L1, LAG-3, TIM-3, TIGIT, VISTA, and numerous additional checkpoint targets currently in clinical evaluation.

Checkpoint inhibitors -- anti-CTLA-4, anti-PD-1, anti-PD-L1, and the recently approved anti-LAG-3 antibody relatlimab - represent the most commercially established immunotherapy platform, with pembrolizumab (Keytruda, Merck) alone generating approximately USD 25 billion in annual revenue across more than 40 FDA-approved indications and representing the highest-revenue oncology drug globally. The CAR-T cell therapy platform -- engineering patient or donor T cells to express chimeric antigen receptors targeting tumor-associated antigens including CD19, BCMA, CD22, and CD20 -- has achieved transformative clinical outcomes in heavily pre-treated hematologic malignancies with response rates of 70-90% in populations where conventional therapy has failed, establishing cellular engineering as a bona fide curative modality for subsets of B-cell leukemia, lymphoma, and multiple myeloma patients. Cancer vaccine platforms -including peptide vaccines, dendritic cell vaccines, mRNA neoantigen vaccines, and viral vector-delivered tumor antigen platforms - are experiencing a renaissance driven by mRNA vaccine manufacturing expertise developed through COVID-19 vaccination programs, AI-powered neoantigen identification algorithms enabling personalized vaccine design from tumor genomic sequencing, and combination strategies pairing vaccines with checkpoint inhibitors that show compelling efficacy signals in clinical trials.

The commercial immunotherapy ecosystem extends across multiple layers: innovator pharmaceutical companies including Merck, Bristol-Myers Squibb, Roche/Genentech, AstraZeneca, Pfizer, Johnson & Johnson, Novartis, and Gilead Sciences generating the majority of approved immunotherapy revenue; cell therapy contract manufacturers including Lonza, Wuxi AppTec, and Hitachi Healthcare providing specialized manufacturing services for autologous and allogeneic cellular therapies; specialized biotech companies including Moderna, BioNTech, Allogene, Fate Therapeutics, Autolus, Agenus, Inhibrx, and Relay Therapeutics advancing next-generation immunotherapy platforms; and enabling technology providers including 10x Genomics, Pacific Biosciences, and Adaptive Biotechnologies providing the genomic and immune profiling tools that enable immunotherapy biomarker development and personalized therapy design.

Personalized mRNA Neoantigen Cancer Vaccines Entering Pivotal Clinical Stage

The convergence of mRNA vaccine manufacturing technology - industrialized at unprecedented scale through Moderna and BioNTech's COVID-19 vaccine programs - with AI-powered tumor genomic sequencing pipelines enabling rapid identification of patient-specific neoantigens and computational epitope selection algorithms has positioned personalized mRNA neoantigen cancer vaccines as one of the most transformative emerging immunotherapy platform technologies, with pivotal clinical trial results expected from 2025-2028 that could establish personalized vaccines as standard adjuvant therapy across multiple solid tumor types. The scientific rationale is compelling: tumor neoantigens - novel peptide sequences arising from somatic mutations unique to each patient's cancer -- are not subject to central tolerance and represent ideal targets for generating tumor-specific T cell responses without the autoimmune toxicity risks of targeting self-antigens. Moderna's mRNA-4157 (V940) neoantigen vaccine in combination with pembrolizumab demonstrated statistically significant 44% reduction in recurrence or death versus pembrolizumab alone in the KEYNOTE-942 Phase 2b trial in high-risk resected melanoma patients, with the combination also showing significant recurrence-free survival improvement in the adjuvant NSCLC setting across the KEYNOTE-942 Phase 3 expansion - generating substantial clinical excitement and accelerating the Phase 3 mRNA-4157 development program in multiple indications. BioNTech's individualized neoantigen specific therapy (iNeST) platform BNT111 and BNT112 similarly advanced through early phase trials demonstrating immune activation and clinical activity in melanoma and prostate cancer, establishing the German mRNA company's presence in the neoantigen vaccine space alongside its dominant mRNA manufacturing infrastructure. The manufacturing challenge - designing, synthesizing, and quality-releasing a personalized mRNA vaccine within 4-6 weeks of tumor biopsy using automated bioinformatics pipelines for neoantigen prediction and mRNA synthesis - has been substantially addressed through the industrial automation developed during COVID-19 vaccine production, with costs declining dramatically as the manufacturing process is further optimized for commercial scale.

Allogeneic Off-the-Shelf CAR-T Platforms Breaking Through Manufacturing Constraints

The development of allogeneic CAR-T cell therapies derived from healthy donor T cells - engineered to express chimeric antigen receptors while removing endogenous TCR expression through gene editing to prevent graft-versus-host disease - addresses the fundamental manufacturing limitations of autologous CAR-T therapies where each patient's own T cells must be collected, shipped to centralized manufacturing facilities, engineered over 3-4 weeks, and returned to the treating center before infusion: a process costing USD 400,000-500,000 per treatment and accessible only to patients fit enough to wait 4-6 weeks for their custom product. Allogeneic platforms promise to transform CAR-T from a bespoke personalized medicine requiring complex individualized manufacturing into an off-the-shelf pharmaceutical product manufactured at scale from donor cells and stored frozen in hospital pharmacies for immediate administration - dramatically reducing cost, improving access, and enabling combination strategies and repeat dosing that autologous manufacturing economics preclude. Allogene Therapeutics, Fate Therapeutics (iPSC-derived), Precision BioSciences (ARCUS gene editing), Caribou Biosciences, and Nkarta are advancing allogeneic CAR-T platforms through clinical trials with Phase 1 and emerging Phase 2 data demonstrating proof-of-concept clinical activity in hematologic malignancies, though persistence and durability concerns compared to autologous products remain active areas of platform optimization. CRISPR Therapeutics and Intellia Therapeutics are applying their gene-editing platforms to allogeneic cell therapy manufacturing - using CRISPR-Cas9 to remove TCR alpha chain, beta-2 microglobulin (HLA), and additional immunosuppressive checkpoints from donor cells while inserting optimized CAR constructs - with clinical results beginning to provide comparative efficacy data that will define the competitive position of allogeneic versus autologous CAR-T in commercial markets. Natural killer cell therapies - including Fate Therapeutics' iPSC-derived FT596 and FT576 NK cell products and Nkarta's NKX101 - provide an additional allogeneic cell therapy modality that does not require TCR knockout since NK cells do not cause graft-versus-host disease, enabling simpler manufacturing and potentially superior safety profiles for early line treatment settings.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 584.37 Billion |

|

Market Size in 2026 |

USD 214.68 Billion |

|

Market Size in 2025 |

USD 184.20 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Platform Type, Indication, Molecule Type, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Expanding Checkpoint Inhibitor Indications and Combination Therapy Strategies

The primary growth driver of the immunotherapy platforms market is the continued expansion of checkpoint inhibitor approved indications across earlier treatment lines, additional cancer types, and combination regimens with chemotherapy, targeted therapy, radiation, and other immunotherapy modalities that are collectively broadening the addressable patient population for the established checkpoint inhibitor drugs while generating sustained revenue growth from what are already the world's largest-selling oncology products. Pembrolizumab's FDA approval portfolio has expanded to over 40 indications spanning NSCLC, melanoma, head and neck squamous cell carcinoma, gastric and gastroesophageal junction cancer, colorectal cancer, cervical cancer, endometrial cancer, biliary tract cancer, esophageal cancer, urothelial carcinoma, triple-negative breast cancer, hepatocellular carcinoma, and TMB-high tumor-agnostic indications -- with each new indication approval driving incremental revenue from new patient populations and extending the patent-protected revenue runway of an already extraordinary commercial franchise. First-line combination regimens pairing PD-1/PD-L1 inhibitors with chemotherapy -- exemplified by pembrolizumab plus pemetrexed/carboplatin in non-squamous NSCLC (KEYNOTE-189), nivolumab plus ipilimumab as a chemotherapy-free doublet (CheckMate 227), and atezolizumab combinations in SCLC -- have established checkpoint inhibitor combinations as the new standard of care across multiple major tumor types, displacing platinum-based chemotherapy as the backbone of first-line treatment and dramatically increasing the eligible patient population receiving checkpoint inhibitors. The second-generation checkpoint targets -- LAG-3, TIM-3, TIGIT, and VISTA -- are generating Phase 2 and Phase 3 data that will determine whether combination checkpoint blockade (combining PD-1 inhibition with a second checkpoint target) provides meaningful clinical benefit over single-agent checkpoint inhibition in tumors that have developed resistance to PD-1 monotherapy, with relatlimab (anti-LAG-3) plus nivolumab's approval in melanoma establishing the commercial precedent for dual checkpoint blockade as a standard treatment option.

Opportunity: Autoimmune and Inflammatory Disease Expansion Beyond Oncology

The extension of immunotherapy platforms -- particularly engineered regulatory T cell therapies, tolerogenic dendritic cell approaches, antigen-specific immunosuppression, and the emerging CAR-Treg platform -- into autoimmune and inflammatory disease indications represents the largest market expansion opportunity beyond the established oncology immunotherapy infrastructure, addressing disease areas including rheumatoid arthritis, multiple sclerosis, type 1 diabetes, inflammatory bowel disease, and transplant rejection where durable immune tolerance induction could transform patient outcomes beyond the symptomatic management provided by existing biologics. CAR-Treg therapies engineering regulatory T cells to express chimeric antigen receptors targeting disease-relevant antigens -- allowing Tregs to preferentially accumulate at sites of autoimmune inflammation and exert local immunosuppression -- are entering clinical trials for indications including HLA-A2+ kidney transplant rejection (Quell Therapeutics), pemphigus vulgaris (Cabaletta Bio), and Crohn's disease, with the potential to achieve lasting immune tolerance rather than the continuous immunosuppression required by existing biologic therapies including TNF inhibitors and IL-6 receptor antagonists. The non-oncology immunotherapy opportunity also encompasses therapeutic vaccines for autoimmune conditions -- inducing antigen-specific tolerance to myelin antigens in multiple sclerosis, insulin antigens in type 1 diabetes, and synovial joint antigens in rheumatoid arthritis -- where the precision of antigen-specific immunotherapy offers the prospect of restoring immune homeostasis without the global immunosuppression and infection risk of conventional immunosuppressant drugs. Allergy immunotherapy -- including subcutaneous and sublingual allergen-specific immunotherapy platforms and the emerging epicutaneous patch delivery approaches -- represents an established but evolving market where next-generation platforms including adjuvanted peptide vaccines and mRNA allergen immunotherapy are seeking to improve efficacy and tolerability over traditional extract-based desensitization regimens.

Why Do Checkpoint Inhibitors Lead the Market?

Checkpoint inhibitors command approximately 52-56% of total immunotherapy platforms market revenue in 2026, representing the dominant therapeutic class in immuno-oncology by both approved indications and commercial revenue, with the four principal checkpoint inhibitor drugs -- pembrolizumab (Merck, Keytruda), nivolumab (Bristol-Myers Squibb, Opdivo), atezolizumab (Roche/Genentech, Tecentriq), and durvalumab (AstraZeneca, Imfinzi) -- collectively generating approximately USD 40-50 billion in annual global sales. The extraordinary commercial dominance of pembrolizumab specifically -- with over 40 FDA-approved indications, an estimated 250,000+ patients treated in the US alone annually, and global sales exceeding USD 25 billion in 2024 -- establishes it as the highest-revenue pharmaceutical product of any class globally, reflecting the breadth of the PD-1 blockade mechanism across tumor types with any degree of immune infiltration or PD-L1 expression. The bispecific antibodies platform -- combining antigen-binding domains targeting two distinct epitopes within a single antibody molecule to redirect T cells to tumor targets or simultaneously block two immunosuppressive pathways -- is the fastest-growing segment of the checkpoint and antibody immunotherapy space, with tebentafusp (ImmTAC bispecific for uveal melanoma), teclistamab (BCMAxCD3 for myeloma), and mosunetuzumab (CD20xCD3 for follicular lymphoma) establishing the commercial bispecific antibody immunotherapy market. Antibody-drug conjugates representing precision-targeted immunostimulatory payload delivery -- particularly trastuzumab deruxtecan (HER2-targeted), sacituzumab govitecan (TROP-2 targeted), and enfortumab vedotin (Nectin-4 targeted) -- are generating exceptional clinical efficacy data across multiple solid tumor types, with the ADC platform increasingly considered a distinct immunotherapy modality as immunogenic cell death mechanisms of payload action are recognized as contributing to clinical benefit beyond direct cytotoxicity.

How Does Oncology Maintain Dominant Market Share?

Oncology commands approximately 78-82% of total immunotherapy platforms market revenue in 2026, reflecting cancer's position as the therapeutic area where immune modulation has achieved the most transformative and commercially valuable clinical outcomes and where the mechanistic rationale for immunotherapy -- targeting the tumor's evasion of immune surveillance -- is most directly supported by decades of scientific evidence. Within oncology, non-small cell lung cancer represents the single largest immunotherapy revenue indication, with the combination of the large global patient population -- approximately 1.8 million new NSCLC diagnoses annually worldwide -- the broad applicability of checkpoint inhibitors across PD-L1 expressing and TMB-high patient populations, and the use of checkpoint inhibitors in first-line, second-line, maintenance, and neo-adjuvant/adjuvant settings collectively generating the highest immunotherapy drug utilization of any cancer type. Hematologic malignancies -- including diffuse large B-cell lymphoma, follicular lymphoma, multiple myeloma, B-cell acute lymphoblastic leukemia, and chronic lymphocytic leukemia -- represent the second-largest oncology immunotherapy revenue category, dominated by CAR-T cell therapies that have demonstrated transformative response rates in relapsed/refractory patients and are progressively moving into earlier treatment lines where the curative potential of CAR-T can be maximized. Melanoma retains historical significance as the first indication where checkpoint inhibitors (ipilimumab, 2011) and subsequently PD-1 inhibitors demonstrated durable long-term survival benefits -- with 10-year overall survival rates of 20-25% in patients receiving anti-PD-1 monotherapy -- establishing the proof-of-concept for modern immunotherapy and remaining an active development arena for next-generation combination strategies and personalized neoantigen vaccines.

Why Do Monoclonal Antibodies Lead the Market?

Monoclonal antibodies command approximately 60-64% of total immunotherapy platforms market revenue in 2026, encompassing checkpoint inhibitor antibodies, bispecific T cell engagers, immunostimulatory antibodies targeting co-stimulatory receptors including OX40, CD137, and GITR, and the antibody components of antibody-drug conjugates that collectively represent the highest-revenue molecule class across biopharmaceuticals. The technical maturity of monoclonal antibody manufacturing -- with established CHO cell culture production platforms, Protein A chromatography purification, and regulatory precedent for diverse antibody formats including IgG1, IgG4, humanized, fully human, and Fc-engineered variants -- provides a highly developed commercial infrastructure supporting the continued dominance of antibody-based immunotherapy across the forecast period. Cell-based therapies -- encompassing autologous CAR-T, allogeneic CAR-T, TIL therapy, NK cell therapy, and dendritic cell vaccines -- represent the second-largest molecule type by revenue and the fastest-growing segment at approximately 15-18% CAGR, driven by the expansion of autologous CAR-T into additional hematologic and solid tumor indications, the first commercial approvals of TIL therapy (lifileucel/Amtagvi for melanoma), and the clinical advancement of next-generation allogeneic and iPSC-derived cell therapy products. Nucleic acid platforms -- encompassing mRNA cancer vaccines, mRNA-encoded cytokines and immunostimulatory proteins, plasmid DNA vaccines, and siRNA-based immunomodulation -- represent the highest-growth emerging molecule class at approximately 20-22% CAGR, driven by the mRNA platform's validated clinical proof-of-concept in neoantigen cancer vaccines and the expanding pipeline of mRNA-encoded immunotherapy constructs leveraging the manufacturing infrastructure built for COVID-19 vaccines.

Why Do Hospitals and Cancer Centers Lead?

Hospitals and cancer centers command approximately 68-72% of immunotherapy platforms market revenue in 2026, reflecting their role as the exclusive sites for administration of the most complex and high-value immunotherapy products -- including intravenous checkpoint inhibitor infusions, CAR-T cell infusions requiring Risk Evaluation and Mitigation Strategy (REMS) programs and specialized monitoring for cytokine release syndrome, and TIL therapy requiring lymphodepletion conditioning and intensive post-infusion monitoring. Comprehensive cancer centers and academic medical centers with specialized immunotherapy programs including Memorial Sloan Kettering Cancer Center, MD Anderson Cancer Center, Dana-Farber/Harvard Cancer Center, and their international equivalents represent the highest-volume and highest-complexity immunotherapy administration sites, deploying multi-disciplinary tumor boards and specialized infusion suites with intensive care unit backup capability required for safe CAR-T administration. Community oncology practices and hospital outpatient infusion centers administer the majority of checkpoint inhibitor volume by patient numbers, as the relative operational simplicity of IV antibody infusions allows community oncology deployment beyond the specialized academic center infrastructure required for cellular therapies. Contract manufacturing organizations -- including Lonza Group, WuXi Biologics, Catalent Pharma Solutions, Thermo Fisher Scientific (Patheon), and specialized cell therapy CDMOs including Oxford Biomedica, Cobra Biologics, and PCT (Hitachi Healthcare) -- represent a critical end-user segment enabling immunotherapy platform development by providing the specialized manufacturing infrastructure required for complex biologic and cellular therapy production that most biotech developers lack in-house capacity to perform at commercial scale.

How is North America Maintaining Market Leadership?

North America holds approximately 44-48% of the global immunotherapy platforms market in 2026, anchored by the United States as the world's largest single-country immunotherapy market where the combination of FDA's accelerated approval pathways enabling rapid market entry, highest per-capita oncology drug spending globally, comprehensive commercial insurance and Medicare coverage for approved immunotherapy indications, and the concentration of leading academic medical centers administering the most complex and highest-cost immunotherapy products creates unparalleled commercial scale. The US immunotherapy market benefits from the FDA's Breakthrough Therapy and Priority Review designations that have consistently accelerated checkpoint inhibitor and CAR-T approvals -- with pembrolizumab carrying multiple breakthrough designations across different indications and all six approved CAR-T products receiving accelerated or priority review -- maintaining the US as the market where new immunotherapy innovations first achieve commercial revenue. Canada's publicly funded provincial cancer programs -- including Ontario Health, BC Cancer, and the Canadian Agency for Drugs and Technologies in Health -- provide immunotherapy coverage for approved indications after health technology assessment review, with reimbursement timelines of 12-24 months post-FDA/Health Canada approval creating a secondary but significant North American market.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 13-15% CAGR, driven by China's rapidly expanding domestic checkpoint inhibitor market generating substantial revenue from domestically developed and priced PD-1/PD-L1 antibodies, Japan's accelerating immunotherapy adoption, and South Korea's emerging position as a significant immunotherapy manufacturing and clinical development hub. China's domestic checkpoint inhibitor market has been transformed by the approval and National Reimbursement Drug List inclusion of multiple domestically developed PD-1 and PD-L1 antibodies -- sintilimab (Innovent), tislelizumab (BeiGene), camrelizumab (Hengrui), and sugemalimab (CStone Pharmaceuticals) -- at price points 50-80% below imported pembrolizumab and nivolumab, dramatically expanding immunotherapy access across China's large oncology patient population. BeiGene's global expansion strategy -- seeking FDA approval for tislelizumab in Western markets and partnering with Novartis for ex-China commercialization -- exemplifies the emerging competitive dynamic where Chinese immunotherapy developers are transitioning from domestic market focus toward global competitive positioning. Japan's Pharmaceuticals and Medical Devices Agency has approved multiple checkpoint inhibitors and CAR-T products, with the Japanese oncology market's sophisticated treatment guidelines and relatively high healthcare expenditure creating a premium immunotherapy market where both imported and domestically developed products command significant revenue. India's immunotherapy market is growing rapidly from a low base, with cost-competitive biosimilar pembrolizumab and nivolumab products approved domestically enabling immunotherapy access for the large Indian cancer patient population at price points compatible with the healthcare system's reimbursement capacity.

The global immunotherapy platforms market is dominated by large pharmaceutical companies with established checkpoint inhibitor and cellular therapy franchises alongside an expansive ecosystem of specialized biotechnology companies advancing next-generation platforms. Merck & Co. leads the market through Keytruda (pembrolizumab), the world's highest-revenue oncology drug, deployed across 40+ indications globally. Bristol-Myers Squibb operates the second-largest checkpoint inhibitor franchise with Opdivo (nivolumab) and Yervoy (ipilimumab), alongside the Opdualag (nivolumab + relatlimab) dual checkpoint regimen for melanoma. Roche/Genentech provides Tecentriq (atezolizumab), Kadcyla and Polivy antibody-drug conjugates, and the Lunsumio bispecific antibody. AstraZeneca commercializes Imfinzi (durvalumab) and Imjudo (tremelimumab) alongside extensive checkpoint combination clinical programs. Johnson & Johnson markets Darzalex (daratumumab) and Rybrevant (amivantamab bispecific) while developing next-generation immunotherapy combinations. In CAR-T and cellular therapy, Novartis (Kymriah), Gilead/Kite (Yescarta, Tecartus), Bristol-Myers Squibb (Breyanzi, Abecma), Janssen/Legend Biotech (Carvykti), and Iovance Biotherapeutics (Amtagvi TIL therapy) represent the commercial cellular immunotherapy landscape. In mRNA and neoantigen cancer vaccines, Moderna (mRNA-4157) and BioNTech (BNT111 series) lead the clinical development pipeline. Emerging platform companies including Allogene Therapeutics, Fate Therapeutics, Relay Therapeutics, Agenus, iTeos Therapeutics, Arcus Biosciences, and Immunomedics (Gilead) represent the next wave of immunotherapy innovation advancing through clinical pipelines toward potential approval in the forecast period.

The global immunotherapy platforms market is expected to grow from USD 214.68 billion in 2026 to USD 584.37 billion by 2036.

The global immunotherapy platforms market is projected to grow at a CAGR of 10.5% from 2026 to 2036.

Checkpoint inhibitors dominate representing approximately 52-56% of revenue through the pembrolizumab, nivolumab, atezolizumab, and durvalumab franchises across 40+ combined indications. CAR-T and cellular therapies demonstrate the fastest growth driven by allogeneic off-the-shelf platform advances, TIL therapy commercialization, and expansion into solid tumor indications and earlier treatment lines that will dramatically increase the eligible patient population.

Moderna's mRNA-4157 neoantigen vaccine demonstrated 44% reduction in recurrence or death versus pembrolizumab alone in the KEYNOTE-942 Phase 2b melanoma trial, leveraging AI-powered neoantigen prediction algorithms, automated mRNA synthesis pipelines producing patient-specific vaccines within 4-6 weeks of tumor biopsy, and COVID-19 vaccine-derived manufacturing infrastructure to translate personalized cancer vaccine science into clinically and commercially viable products approaching Phase 3 pivotal programs.

North America leads with approximately 44-48% of global market driven by the US as the world's largest immunotherapy drug market with the broadest FDA-approved product portfolio and highest oncology spending. Asia-Pacific demonstrates the fastest growth at 13-15% CAGR driven by China's large domestic PD-1/PD-L1 antibody market at accessible price points, Japan's accelerating cellular therapy adoption, and South Korea's emerging manufacturing hub.

The leading companies include Merck & Co. (Keytruda), Bristol-Myers Squibb (Opdivo/Yervoy/Opdualag), Roche/Genentech, AstraZeneca (Imfinzi), Novartis (Kymriah), Gilead/Kite (Yescarta/Tecartus), BMS (Breyanzi/Abecma), Janssen/Legend Biotech (Carvykti), Iovance Biotherapeutics (Amtagvi), Moderna (mRNA-4157), BioNTech, Allogene Therapeutics, and Fate Therapeutics across checkpoint inhibitors, cellular therapies, and emerging mRNA vaccine platforms.

Published Date: Jul-2020

Published Date: May-2026

Published Date: Aug-2026

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates