Resources

About Us

Immersion Cooling Fluids Market Size, Share & Trends Analysis, by Fluid Type, Cooling Technology (Single-phase, Two-phase), Application (Data Centers, High-performance Computing, Cryptocurrency Mining, Electric Vehicle Batteries), End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

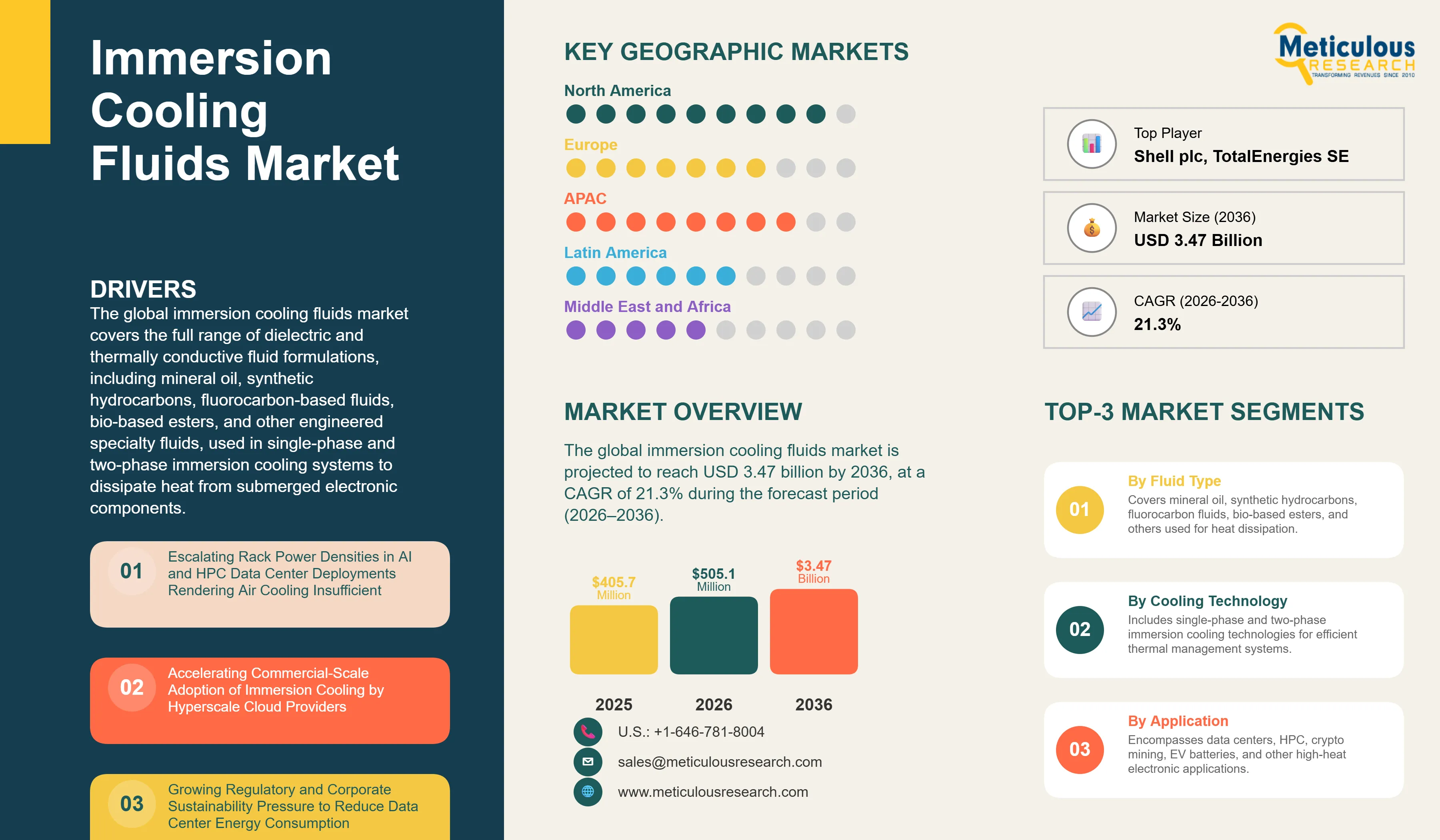

Report ID: MRCHM - 1041870 Pages: 293 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global immersion cooling fluids market was valued at USD 405.7 million in 2025. The market is projected to reach USD 3.47 billion by 2036, growing from USD 505.1 million in 2026 at a CAGR of 21.3% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global immersion cooling fluids market covers the full range of dielectric and thermally conductive fluid formulations, including mineral oil, synthetic hydrocarbons, fluorocarbon-based fluids, bio-based esters, and other engineered specialty fluids, used in single-phase and two-phase immersion cooling systems to dissipate heat from submerged electronic components. These fluids are deployed across data center, high-performance computing, cryptocurrency mining, electric vehicle battery thermal management, and industrial power electronics applications where conventional air cooling is insufficient to manage thermal loads generated by high-density computing hardware.

The growth of the immersion cooling fluids market is primarily driven by the rapid increase in rack power densities associated with artificial intelligence (AI) and high-performance computing (HPC) workloads, which are exceeding the thermal limits of conventional air cooling systems. This is driving the adoption of immersion cooling technologies among hyperscale cloud providers and colocation operators aiming to achieve ultra-low power usage effectiveness (PUE) levels in next-generation data centers.

In addition, increasing regulatory and corporate sustainability mandates are pushing data center operators to reduce energy consumption and carbon emissions, further driving the adoption of advanced liquid cooling solutions.

Despite strong growth prospects, the market faces challenges related to the high upfront capital investment required for transitioning from air-cooled to immersion cooling infrastructure. Concerns regarding fluid compatibility with standard IT hardware, including potential impacts on server warranties, as well as the operational complexity associated with fluid handling, maintenance, and system integration, continue to limit large-scale adoption.

The transition away from PFAS-based chemistries is creating significant opportunities for next-generation immersion cooling fluids, mainly synthetic hydrocarbons and bio-based esters that meet evolving environmental and regulatory requirements.

Additionally, the emergence of immersion cooling in electric vehicle battery thermal management is opening a new application segment beyond data centers. The increasing number of large-scale deployments by hyperscale operators is also driving bulk procurement of immersion fluids, creating economies of scale and expanding the addressable market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 3.47 Billion |

|

Market Size in 2026 |

USD 505.1 Million |

|

Market Size in 2025 |

USD 405.7 Million |

|

Revenue Growth Rate (2026–2036) |

CAGR of 21.3% |

|

Dominating Fluid Type |

Synthetic Hydrocarbons |

|

Fastest Growing Fluid Type |

Bio-Based Esters |

|

Dominating Cooling Technology |

Single-Phase Immersion Cooling |

|

Fastest Growing Cooling Technology |

Two-Phase Immersion Cooling |

|

Dominating Application |

Data Centers |

|

Fastest Growing Application |

Electric Vehicle Batteries |

|

Dominating End Use |

IT & Telecom |

|

Fastest Growing End Use |

Automotive |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

PFAS Regulatory Transition Driving Formulation Innovation and Market Restructuring

The increasing regulatory phase-down of per- and polyfluoroalkyl substances (PFAS), driven by initiatives such as the United States Environmental Protection Agency PFAS Strategic Roadmap and the European Chemicals Agency proposed universal PFAS restrictions, is emerging as the most significant regulatory force driving the immersion cooling fluids market. These frameworks are expected to impose substantial limitations on the production and use of fluorinated cooling fluids, particularly in medium- to long-term deployment scenarios.

Fluorinated fluids, including legacy product families such as Fluorinert and Novec, have historically dominated two-phase immersion cooling applications due to their low boiling points, dielectric properties, and non-flammability. However, increasing regulatory scrutiny and uncertainty around long-term availability are creating procurement risks for data center operators that require stable, multi-year supply assurance.

As a result, the market is witnessing increasing development and adoption of PFAS-free alternatives, mainly hydrofluoroolefin (HFO)-based fluids such as Opteon 2P50 and advanced synthetic hydrocarbon formulations. Fluid manufacturers are intensifying R&D efforts to develop next-generation PFAS-free two-phase fluids that can match the performance characteristics of legacy fluorinated solutions while meeting evolving regulatory requirements. This transition is not only driving formulation innovation but also reshaping competitive dynamics, as companies with compliant, scalable, and certified alternatives gain a strategic advantage.

Hardware Certification Programs Accelerating Mainstream Immersion Cooling Adoption

The emergence of formal hardware compatibility and certification programs for immersion cooling fluids is significantly reducing one of the most critical barriers to adoption, concerns related to server warranties and hardware reliability. Initiatives such as fluid validation programs conducted by Intel in collaboration with fluid providers such as Shell, along with broader industry efforts such as submerged server testing and certification frameworks developed jointly by system OEMs and fluid manufacturers, are establishing standardized benchmarks for performance, safety, and compatibility.

These certification programs are enabling fluid formulations to be validated for use with enterprise-grade server hardware from leading OEMs, including Dell Technologies, Hewlett Packard Enterprise, and Supermicro. As a result, the perceived risk associated with immersion cooling deployment is declining, particularly among enterprise and colocation data center operators that require assurance of long-term hardware support and serviceability.

This shift is expanding the addressable market for immersion cooling beyond early adopters such as high-performance computing (HPC) and cryptocurrency mining, enabling broader penetration into mainstream enterprise and colocation data center environments. The increasing standardization of hardware–fluid compatibility is expected to play a pivotal role in accelerating the commercialization and large-scale deployment of immersion cooling technologies.

Bio-Based Esters Emerging as the Sustainability-Preferred Alternative Fluid Category

Bio-based ester immersion cooling fluids, derived from renewable feedstocks such as rapeseed, sunflower, and palm-based oils, are emerging as a preferred alternative to conventional synthetic fluids, mainly among hyperscale data center operators with stringent sustainability targets. These fluids are engineered to deliver thermal performance comparable to synthetic hydrocarbons while offering superior environmental characteristics, including biodegradability, low aquatic toxicity, and safer end-of-life disposal profiles.

Leading players such as Cargill and TotalEnergies are actively commercializing bio-based ester formulations, including products such as NatureCool and BioLife, which align with environmental management frameworks such as ISO 14001 and evolving corporate ESG reporting requirements. These attributes are increasingly influencing procurement decisions among hyperscale operators seeking to decarbonize their data center infrastructure and supply chains.

In addition, major cloud providers, such as Microsoft and Google, have evaluated bio-based ester fluids within immersion cooling pilot programs, indicating growing industry confidence in their performance and compatibility. As sustainability considerations become a core driver of technology adoption, bio-based esters are expected to capture an increasing share of new immersion cooling fluid deployments over the forecast period.

By Fluid Type: In 2026, the Synthetic Hydrocarbons Segment to Dominate the Global Immersion Cooling Fluids Market

Based on fluid type, the global immersion cooling fluids market is segmented into mineral oil, synthetic hydrocarbons, fluorocarbon-based fluids, bio-based esters, and other fluids. In 2026, the synthetic hydrocarbons segment is expected to account for the largest share of the global immersion cooling fluids market. The large market share of this segment is attributed to synthetic hydrocarbons' unique combination of high thermal conductivity, low viscosity for efficient pump circulation, broad material compatibility with server hardware components, established dielectric performance credentials, and PFAS-free chemistry that aligns with both current and anticipated regulatory requirements.

Unlike fluorinated fluids, synthetic hydrocarbon formulations do not face regulatory phase-out risk, providing data center operators with long-term fluid supply security. Shell's DLC Fluid S3, demonstrating a 25% thermal conductivity improvement over mineral oil baselines, and Lubrizol's CompuZol family at 0.15 W/m·K thermal conductivity exemplify the continuous formulation advancement driving this segment's dominance.

However, the bio-based esters segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the increasing alignment between fluid procurement decisions and corporate sustainability commitments at major hyperscale operators, with bio-based esters offering full biodegradability and favorable end-of-life disposal profiles alongside thermal performance equivalent to synthetic hydrocarbon competitors.

By Cooling Technology: In 2026, the Single-Phase Immersion Cooling Segment to Hold the Largest Share

Based on cooling technology, the global immersion cooling fluids market is segmented into single-phase immersion cooling and two-phase immersion cooling. In 2026, the single-phase immersion cooling segment is expected to account for the largest share of the global immersion cooling fluids market. This dominance is attributed to the lower system complexity and capital cost of single-phase deployments compared to two-phase alternatives, the established operational workflows compatible with conventional data center maintenance practices, and the broad hardware compatibility of single-phase dielectric fluids with the full range of server and storage hardware currently deployed in hyperscale and enterprise data center environments.

However, the two-phase immersion cooling segment is projected to grow at the highest CAGR from 2026 to 2036. The high growth of this segment is driven by its superior thermal efficiency at extreme rack power densities above 100 kW where phase-change heat transfer provides significantly higher heat removal capacity than single-phase convection, and the growing adoption of two-phase systems in purpose-built AI data center campuses where operating temperatures within the single-phase regime cannot be maintained at next-generation GPU thermal design power levels.

By Application: In 2026, the Data Centers Segment to Account for the Largest Share

Based on application, the global immersion cooling fluids market is segmented into data centers (hyperscale, colocation, enterprise, edge), high-performance computing, cryptocurrency mining, electric vehicle batteries, and other applications. In 2026, the data centers segment is expected to account for the largest share of the global immersion cooling fluids market, indicating the dominant role of data center operators as both the primary volume procurers and the innovation-leading adopters of immersion cooling fluid technology. Hyperscale cloud providers, such as Microsoft, Google, and Meta, are deploying immersion cooling at commercial scale in AI data center campuses, with each gigawatt-scale campus requiring tens of millions of liters of high-performance dielectric fluid.

However, the electric vehicle batteries segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the rapid global expansion of electric vehicle production and the growing adoption of immersion cooling by leading EV manufacturers and battery suppliers seeking to enable faster charging rates, more stable performance in demanding conditions, and extended battery cycle life through superior thermal uniformity that direct battery cell immersion cooling provides.

By End Use: In 2026, the IT & Telecom Segment to Hold the Largest Share

Based on end use, the global immersion cooling fluids market is segmented into IT and telecom, BFSI, automotive, energy and utilities, healthcare, and other end uses. In 2026, the IT and telecom segment is expected to account for the largest share of the global immersion cooling fluids market, reflecting the dominant position of cloud service providers, telecommunications carriers, and IT infrastructure companies as the largest procurers of immersion cooling systems and associated fluid volumes globally. This segment covers both the hyperscale cloud providers deploying commercial-scale immersion cooling in AI data centers and the colocation operators retrofitting existing facilities with immersion cooling to attract premium AI workload tenants.

However, the automotive segment is projected to register the highest CAGR during the forecast period, driven by the growing adoption of immersion cooling for electric vehicle battery thermal management and the growing incorporation of immersion-cooled power electronics in EV drivetrains and fast-charging infrastructure.

Based on geography, the global immersion cooling fluids market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global immersion cooling fluids market. This dominant position is driven by the highest concentration of hyperscale AI data center deployments adopting immersion cooling at commercial scale, the presence of leading fluid manufacturers including Dow, ExxonMobil, Engineered Fluids, Calumet, and Lubrizol, the most advanced regulatory and operational infrastructure for immersion cooling deployment, and the deepest ecosystem of immersion cooling system vendors, such as Submer, GRC, LiquidStack, and Iceotope, with established hyperscale customer relationships. The U.S. market benefits from the Inflation Reduction Act's energy efficiency incentives that improve the ROI of advanced cooling investments.

However, the Asia Pacific immersion cooling fluids market is expected to grow at the fastest CAGR from 2026 to 2036. The rapid growth of this market is driven by the massive data center capacity expansion across China, India, Japan, Singapore, and Southeast Asia; the growing adoption of AI workloads creating significant rack density requirements that make immersion cooling a practical necessity; and strong government-led digital infrastructure investment programs that are compressing the AI data center buildout timeline and driving large-volume fluid procurement. China's domestic AI data center investment is creating substantial demand for immersion cooling fluids, with domestic fluid manufacturers and international suppliers competing for a rapidly growing market that benefits from Chinese hyperscalers' early adoption of immersion cooling to manage AI GPU thermal densities without PFAS-restricted fluorinated alternatives.

The global immersion cooling fluids market is moderately fragmented at the specialty fluid level, with competition primarily focused on thermal performance, fluid stability, and compatibility with immersion cooling hardware systems. Key competitive factors include fluid-hardware certification, regulatory compliance (particularly the transition toward PFAS-free chemistries), scalability of supply for hyperscale data center deployments, and technical capabilities related to fluid management and lifecycle services.

Large chemical and energy companies such as The Dow Chemical Company, Exxon Mobil Corporation, Shell plc, and Solvay compete through established product portfolios supported by strong R&D capabilities and global manufacturing and distribution networks. These players are increasingly focusing on developing advanced dielectric fluids tailored for data center and high-performance computing applications.

Specialty fluid providers such as Engineered Fluids and M&I Materials offer purpose-built immersion cooling fluids optimized for performance, safety, and long-term stability in data center environments. In parallel, bio-based and sustainable fluid developers, including Cargill and TotalEnergies, are gaining traction as sustainability becomes a key procurement criterion among hyperscale operators.

The market is also influenced by regulatory shifts, particularly the phase-out of PFAS-based chemistries, which is driving innovation in alternative fluid formulations across both synthetic and bio-based segments.

The report provides a comprehensive competitive analysis based on an assessment of key players’ product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global immersion cooling fluids market include The Dow Chemical Company (U.S.), Exxon Mobil Corporation (U.S.), Shell plc (U.K.), The Chemours Company (U.S.), 3M Company (U.S.), Engineered Fluids, Inc. (U.S.), Solvay SA (Belgium), M&I Materials Limited (U.K.), Calumet Specialty Products Partners, L.P. (U.S.), Cargill, Incorporated (U.S.), FUCHS SE (Germany), Chevron Phillips Chemical Company LLC (U.S.), TotalEnergies SE (France), The Lubrizol Corporation (U.S.), and BASF SE (Germany) among others.

The global immersion cooling fluids market is expected to reach USD 3.47 billion by 2036 from an estimated USD 505.1 million in 2026, at a CAGR of 21.3% during the forecast period 2026–2036.

In 2026, the synthetic hydrocarbons segment is expected to hold the largest share of the global immersion cooling fluids market.

The bio-based esters segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by accelerating adoption of biodegradable, environmentally compliant fluid formulations.

In 2026, the single-phase immersion cooling segment is expected to hold the largest share of the global immersion cooling fluids market.

In 2026, the data centers segment is expected to hold the largest share of the global immersion cooling fluids market.

The growth of this market is primarily driven by escalating rack power densities in AI and HPC data center deployments rendering air cooling insufficient, the accelerating adoption of immersion cooling by hyperscale cloud providers, and growing regulatory and sustainability pressure.

Key players in the global immersion cooling fluids market include The Dow Chemical Company (U.S.), Exxon Mobil Corporation (U.S.), Shell plc (U.K.), The Chemours Company (U.S.), 3M Company (U.S.), Engineered Fluids, Inc. (U.S.), Solvay SA (Belgium), M&I Materials Limited (U.K.), Calumet Specialty Products Partners, L.P. (U.S.), Cargill, Incorporated (U.S.), FUCHS SE (Germany), Chevron Phillips Chemical Company LLC (U.S.), TotalEnergies SE (France), The Lubrizol Corporation (U.S.), and BASF SE (Germany).

Asia Pacific is expected to register the highest growth rate in the global immersion cooling fluids market during the forecast period 2026–2036.

Published Date: Jan-2025

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates