Resources

About Us

High Barrier Films Market for Food Packaging by Material Type (PE, BOPP & BOPET, CPP, EVOH, Nylon), Technology, Application (Meat and Fish, Dairy, Snacks, Confectionery, Bakery Products, Pet Food), End User, and Geography – Global Forecast to 2036

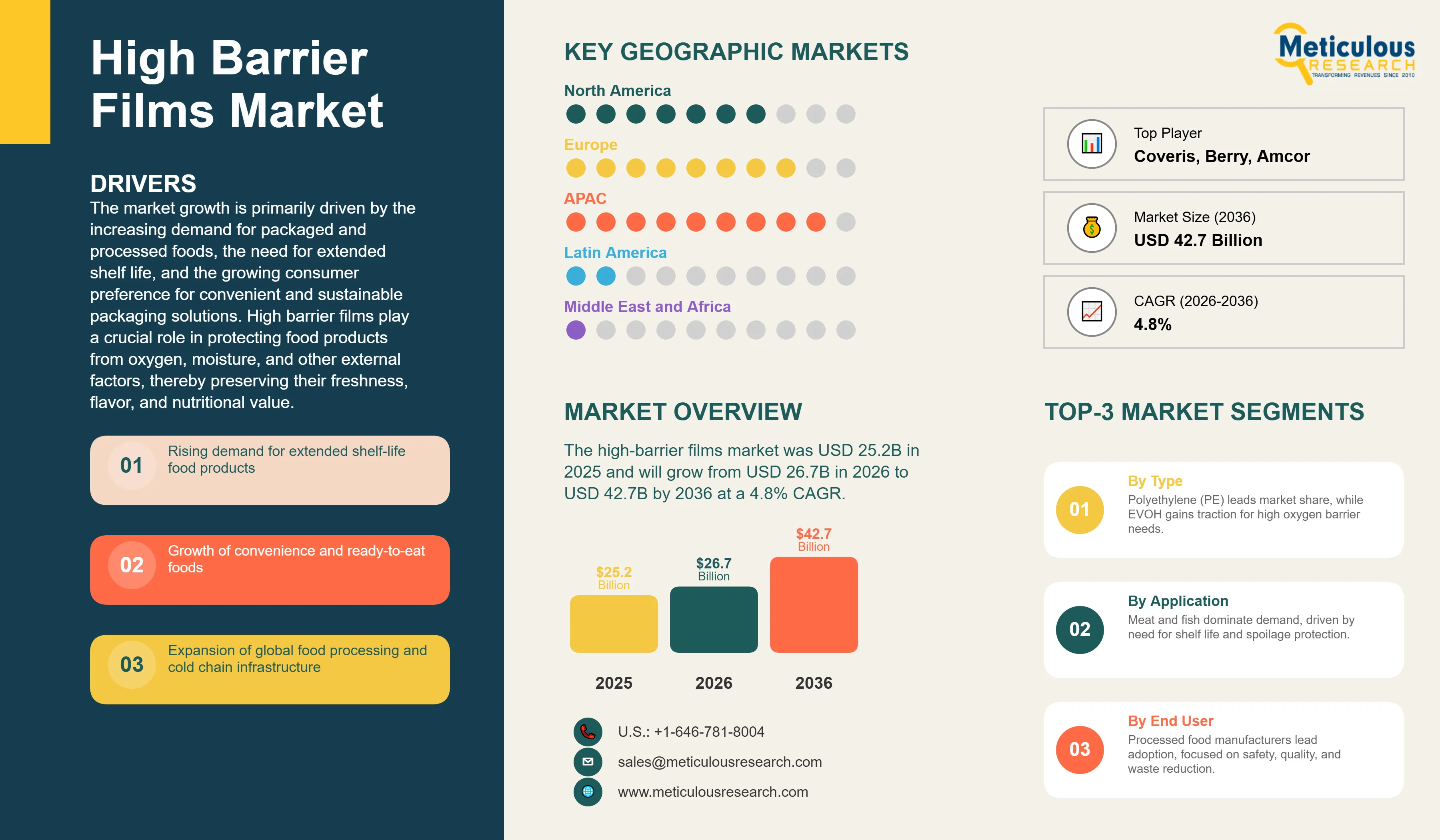

Report ID: MRCHM - 104402 Pages: 172 Feb-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 48 Hours Download Free Sample ReportThe global high-barrier films market for food packaging was valued at USD 25.2 billion in 2025. This market is expected to reach USD 42.7 billion by 2036 from USD 26.7 billion in 2026, growing at a CAGR of 4.8% from 2026 to 2036. The market growth is primarily driven by the increasing demand for packaged and processed foods, the need for extended shelf life, and the growing consumer preference for convenient and sustainable packaging solutions. High barrier films play a crucial role in protecting food products from oxygen, moisture, and other external factors, thereby preserving their freshness, flavor, and nutritional value.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global high barrier films market for food packaging comprises a wide range of flexible packaging materials designed to provide a high level of protection against oxygen, moisture, light, and other environmental factors. These films are essential for extending the shelf life of food products, reducing food waste, and ensuring food safety. The market is characterized by a diverse range of materials, including polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), ethylene vinyl alcohol (EVOH), and nylon.

The demand for high barrier films is closely linked to the growth of the flexible packaging industry. According to the Flexible Packaging Association (FPA), the flexible packaging industry is a significant and growing segment of the packaging industry. The increasing consumer preference for convenient and on-the-go food products is driving the demand for flexible packaging solutions, which in turn is fueling the growth of the high barrier films market.

Leading players in the market, such as Amcor plc and Sealed Air Corporation, are focusing on developing innovative and sustainable packaging solutions. For example, Amcor has developed a range of high barrier films made from post-consumer recycled (PCR) content, while Sealed Air offers a variety of recyclable and compostable packaging solutions. The industry is also witnessing a growing trend towards the use of biodegradable and bio-based materials for high barrier film production.

What are the Key Trends in the High Barrier Films Market for Food Packaging?

Growing Demand for Sustainable and Recyclable Films

There is a growing demand for sustainable and recyclable high barrier films in the food packaging industry. Consumers are increasingly aware of the environmental impact of packaging waste, and they are demanding more eco-friendly packaging solutions. This has led to the development of a wide range of sustainable high barrier films, including those made from recycled materials, biodegradable polymers, and bio-based plastics. For example, TIPA Corp offers a range of compostable high barrier films that are designed to break down in a commercial composting facility.

Development of Advanced Coating Technologies

The development of advanced coating technologies is another key trend in the high barrier films market. These coatings are used to enhance the barrier properties of films, making them more effective at protecting food products from oxygen and moisture. For example, plasma-enhanced chemical vapor deposition (PECVD) is a technology that is used to apply a thin layer of silicon oxide (SiOx) to films, which significantly improves their barrier properties. This technology is being used to develop a new generation of high barrier films that are both high-performing and recyclable.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 42.7 Billion |

|

Market Size in 2026 |

USD 26.7 Billion |

|

Market Size in 2025 |

USD 25.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.8% |

|

Dominating Material |

Polyethylene (PE) |

|

Fastest Growing Material |

EVOH |

|

Largest Application Segment |

Meat and Fish |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Driver: Increasing Demand for Extended Shelf Life

The growing demand for packaged food products with longer shelf life is a key driver of the global high-barrier films market for food packaging. Rising urbanization, busy lifestyles, and increasing reliance on convenience foods have led consumers to favor products that remain fresh over extended periods while maintaining nutritional quality and safety. High-barrier films, engineered with materials such as EVOH, polyamide, and multilayer PET/PE structures, provide critical resistance to oxygen, moisture, light, and aroma transmission, significantly slowing microbial growth and oxidative degradation.

These properties are particularly important for perishable food categories such as fresh and processed meats, dairy products, ready-to-eat meals, and bakery goods. For example, modified atmosphere packaging (MAP) systems using high-barrier films can extend the shelf life of fresh meat products from a few days to several weeks under refrigerated conditions. Beyond consumer convenience, shelf-life extension also supports supply chain efficiency by enabling longer distribution cycles and reducing product returns.

Additionally, reducing food waste has become a major priority across the food industry. By preserving product integrity and preventing premature spoilage, high-barrier films contribute directly to waste reduction initiatives, aligning with sustainability goals and regulatory focus on minimizing food loss across global markets.

Opportunity: Growth of E-commerce and Online Food Retail

The rapid expansion of e-commerce and online food retail channels presents a strong growth opportunity for the high-barrier films market. Unlike traditional retail, online food distribution involves longer transit times, multiple handling stages, and exposure to varying environmental conditions, increasing the risk of spoilage, leakage, and quality deterioration. High-barrier flexible packaging solutions help mitigate these risks by maintaining internal atmospheres and protecting against oxygen and moisture ingress during transportation.

The rise of meal kit delivery services, online grocery platforms, and direct-to-consumer food brands has accelerated demand for durable, lightweight, and protective packaging formats. Products such as vacuum-sealed meats, portion-controlled cheese packs, and ready-to-heat meal trays increasingly rely on multilayer high-barrier films to ensure freshness and safety until final consumption.

Moreover, the growth of cross-border and long-distance food distribution further strengthens the role of high-performance barrier materials. As e-commerce food sales continue to expand, particularly in urban markets and among younger consumer groups, the need for packaging that combines protection, convenience, and extended shelf stability is expected to drive sustained demand for high-barrier films.

Why Does Polyethylene Dominate the Market?

Based on material type, the polyethylene (PE) segment is expected to account for the largest share of the market, in 2026. PE is a versatile and cost-effective material that offers good barrier properties against moisture. It is widely used in a variety of food packaging applications, including films for meat and cheese, as well as liners for cereal boxes. The high availability and low cost of PE also contribute to its market dominance.

How Does the Meat and Fish Segment Lead the Market?

The meat and fish segment is expected to account for the largest share of the market by application, in 2026. High barrier films are essential for packaging meat and fish products, as they help to prevent spoilage and extend shelf life. The growing demand for packaged and processed meat and fish products is driving the growth of this segment.

How is Asia-Pacific Maintaining Its Leadership in the Global High Barrier Films Market?

Asia-Pacific is projected to account for the largest share of the global high-barrier films market for food packaging throughout the forecast period. This is primarily driven by its large and expanding population base, rapid urbanization, and shifting dietary patterns toward packaged and processed food products. Rising disposable incomes and changing lifestyles are increasing demand for convenience foods, ready-to-eat meals, dairy products, and packaged meats, key application areas for high-barrier flexible packaging.

Major economies such as China and India represent significant consumption hubs due to their large food processing industries and expanding modern retail networks. The growth of organized retail, cold chain infrastructure, and foodservice sectors in these countries is further strengthening demand for packaging solutions that ensure product protection, extended shelf life, and regulatory compliance.

In addition to strong consumption, Asia-Pacific is also a major production base for packaging materials. The presence of large polymer manufacturing capacities, cost-competitive converting industries, and growing investments in multilayer film technologies support regional supply capabilities. This combination of demand-side expansion and manufacturing strength underpins Asia-Pacific’s sustained leadership in the high-barrier films market.

Which Regions Are Experiencing Steady Growth?

Europe is expected to witness steady growth in the global high-barrier films market for food packaging during the forecast period. The food and beverage industry in Europe is mature, but demand for advanced packaging remains robust due to increasing focus on food safety, product quality, and sustainability. European consumers show strong preference for high-quality, minimally processed, and premium packaged food products, which often require high-performance barrier materials.

Stringent food safety regulations and traceability requirements across European markets further drive adoption of packaging that can effectively prevent contamination, moisture ingress, and oxygen exposure. Additionally, the region’s emphasis on reducing food waste supports the use of high-barrier packaging that extends shelf life. At the same time, sustainability initiatives are encouraging innovation in recyclable and mono-material high-barrier film solutions, supporting gradual but stable market expansion.

The global high-barrier films market for food packaging is characterized by the presence of large multinational packaging converters and material technology providers. Key companies profiled in this report include Amcor plc, Sealed Air Corporation, Berry Global Inc., and Coveris Holdings S.A., among others. These players compete through multilayer film innovations, sustainable material development, and expansion of global manufacturing and distribution networks to meet evolving food packaging requirements.

The global high barrier films market for food packaging is expected to grow from USD 26.7 billion in 2026 to USD 42.7 billion by 2036.

The global high barrier films market for food packaging is expected to grow at a CAGR of 4.8% from 2026 to 2036.

The key players operating in the global high barrier films market for food packaging include Amcor plc, Sealed Air Corporation, Berry Global Inc., and Coveris Holdings S.A.

The main factors include the increasing demand for packaged and processed foods, the need for extended shelf life, and the growing consumer preference for convenient and sustainable packaging solutions.

Asia-Pacific will lead the global high barrier films market for food packaging during the forecast period 2026 to 2036.

Published Date: Feb-2026

Published Date: Sep-2024

Published Date: May-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates