Resources

About Us

Dental Materials Market by Type (Indirect Restorative Materials, Direct Restorative Materials, Dental Biomaterials, Impression Materials, Bonding Agents), End User (Dental Clinics & Hospitals, Dental Products Manufacturers, Dental Laboratories, Academic & Research Institutes), and Geography – Global Forecast to 2036

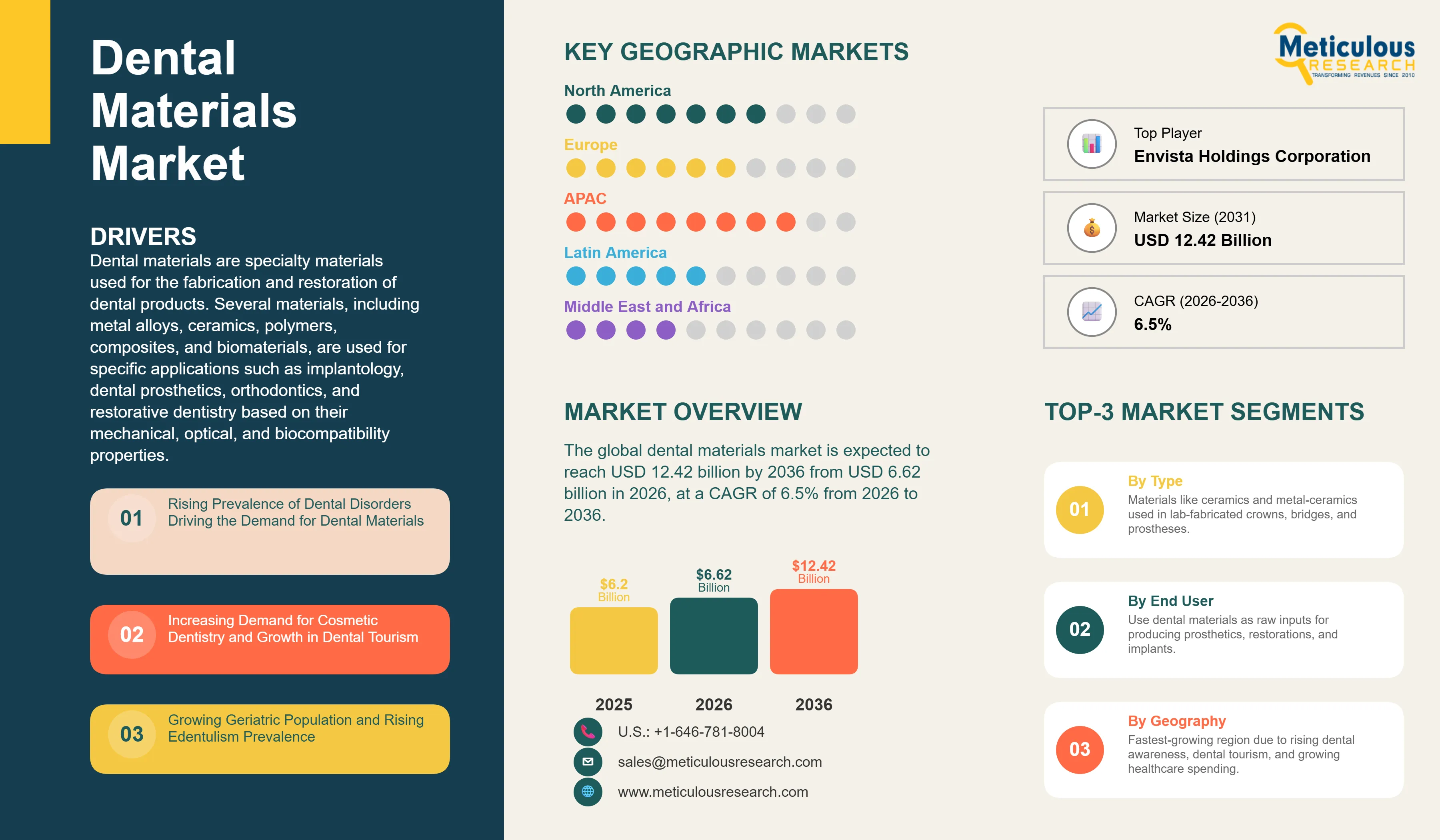

Report ID: MRHC - 10482 Pages: 250 Mar-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 48 Hours Download Free Sample ReportThe global dental materials market was valued at USD 6.2 billion in 2025. This market is expected to reach USD 12.42 billion by 2036 from USD 6.62 billion in 2026, at a CAGR of 6.5% from 2026 to 2036.

Dental materials are specialty materials used for the fabrication and restoration of dental products. Several materials, including metal alloys, ceramics, polymers, composites, and biomaterials, are used for specific applications such as implantology, dental prosthetics, orthodontics, and restorative dentistry based on their mechanical, optical, and biocompatibility properties.

The growth of the dental materials market is attributed to the rising prevalence of dental disorders, the increasing demand for cosmetic dentistry, and the rise in dental tourism. Furthermore, the increasing adoption of CAD/CAM technology in dentistry and the growing integration of digital workflows in dental laboratories and clinics are expected to offer significant opportunities for market growth. However, the high cost of dental treatments and the biocompatibility challenges associated with certain dental material categories remain key restraints for the growth of this market.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Dental materials are specialty materials used in the diagnosis, prevention, and treatment of dental conditions and in the fabrication of dental prostheses, restorations, and implant-supported devices. The dental materials market includes a broad range of material categories including indirect restorative materials such as ceramics and metal-ceramics used in crowns, bridges, and fixed prostheses; direct restorative materials including resin-based composites, amalgam, and glass ionomer cements used in chairside restorations; dental biomaterials including bone graft substitutes, barrier membranes, and collagen-based products used in periodontal and implant surgery; impression materials used to capture accurate dental anatomy; and bonding agents used to facilitate adhesion between restorative materials and tooth structure.

The rising global burden of dental diseases is a key driver of the demand for dental materials. According to the World Health Organization (WHO) Global Oral Health Status Report 2022, oral diseases affect nearly half of the world's population, with around 3.5 billion people affected globally. According to updated data from the WHO Global Burden of Disease Study 2021, as published in The Lancet in 2024–2025, the combined global age-standardized prevalence of the main oral conditions, including untreated caries, severe periodontitis, edentulism, and other oral disorders, was approximately 45,900 per 100,000 population in 2021, with nearly 3.7 billion people affected globally. Untreated dental caries in permanent teeth remains the most prevalent condition, with a global age-standardized prevalence of approximately 27,500 per 100,000 population, while severe periodontitis affected over 1 billion people globally. According to the WHO, the estimated global average prevalence of complete tooth loss is approximately 7% among people aged 20 years or older, rising to a prevalence of 23% among people aged 60 years or older. This high and growing burden of dental diseases drives demand for restorative, prosthetic, and preventive dental treatments, and consequently for dental materials.

The market is further driven by the growing demand for cosmetic dentistry and the rapid adoption of digital dentistry workflows. Patients’ choices and requirements, ranging from basic oral hygiene to aesthetic enhancement, are changing dental industry dynamics. Baby boomers with high disposable incomes, the younger generation of working individuals seeking improved dental aesthetics, and significant technological advances in the dental materials industry have contributed to the rise of cosmetic dentistry. Increasing acceptance of tooth-colored resin-based composites and all-ceramic restorations as aesthetic alternatives to metal-based restorations is driving a long-term shift in indirect and direct restorative material preferences.

Growing Adoption of CAD/CAM Technology and Digital Workflows in Dental Material Processing

One of the significant trends driving the dental materials market is the growing adoption of computer-aided design and computer-aided manufacturing (CAD/CAM) technology in dental material processing and restorative dentistry. CAD/CAM systems enable dental laboratories and clinics to design and mill high-precision dental restorations from a range of advanced dental materials including zirconia ceramics, lithium disilicate glass ceramics, and resin-based composites with significantly reduced chairside time and improved dimensional accuracy. The integration of intraoral digital scanning, CAD/CAM design software, and chairside or laboratory milling units is enabling the end-to-end digital production of crowns, bridges, inlays, onlays, and full-arch restorations within a single appointment or with reduced turnaround times compared to conventional laboratory fabrication methods.

Major dental materials manufacturers are expanding their CAD/CAM-compatible material portfolios to address the growing demand from digitally equipped dental laboratories and clinics. Dentsply Sirona Inc. offers a broad portfolio of CAD/CAM materials including zirconia blocks, ceramics, and resin materials under the CEREC brand, with validated compatibility across more than 60 material options from Dentsply Sirona and partner manufacturers. Institut Straumann AG has strengthened its digital prosthetics capabilities through strategic investments in digital workflow integration, including the launch of the CoDiagnostix AI assistant for implant planning and expansion of its AXS digital platform to support interoperable intraoral scanning and design solutions.

The growing integration of artificial intelligence in digital dental workflows, including AI-assisted design of dental restorations and AI-powered shade matching, is further expanding the functionality of CAD/CAM-based dental material processing systems. This aligns with the World Dental Federation (FDI) 2025 Policy Statement on Digital Dentistry, which recognizes artificial intelligence as an integral component of evidence-based digital workflows aimed at enhancing the quality, safety, and efficiency of oral healthcare.

Rising Demand for Zirconia-Based Ceramics and Tooth-Colored Restorative Materials

The growing preference for tooth-colored, metal-free restorations among patients and dental practitioners is driving demand for zirconia-based ceramics and advanced resin composites. Zirconia ceramic has emerged as a leading material for full-arch prosthetics, implant-supported restorations, and posterior crowns due to its high mechanical strength, biocompatibility, and improved translucency in newer multi-layered formulations; clinical surveys indicate zirconia-based restorations now represent approximately 60–70% of all-ceramic fixed dental prostheses globally.

Advances in the formulation of translucent and ultra-translucent zirconia materials are enabling their use in anterior restorations where optical properties have historically limited zirconia adoption. Kuraray Noritake Dental has introduced KATANA™ Zirconia UTML and HTML PLUS formulations, which deliver high translucency levels (49% to 45%) alongside flexural strength up to 1,150 MPa to support aesthetic anterior crowns and veneers. Similarly, Ivoclar Vivadent AG launched the IPS e.max® ZirCAD Prime block at IDS 2025, combining gradient translucency with strength up to 1,200 MPa to meet aesthetic demands for monolithic anterior restorations.

The long-term trend toward the phase-out of dental amalgam as a restorative material is also driving demand for alternative direct restorative materials. The Minamata Convention on Mercury, an international treaty to protect human health and the environment from the effects of mercury, calls for the phasing down of dental amalgam use. At the 5th Conference of the Parties (COP-5) in October 2023, parties adopted a decision reinforcing the phase-down approach with enhanced reporting requirements. Subsequently, at COP-6 in November 2025, parties agreed to amend Annex A to establish a global phase-out of the manufacture, import, and export of dental amalgam by 2034, subject to limited exemptions. This policy is expected to increase demand for resin-based composites and glass ionomer cements as amalgam replacements during the forecast period of 2026 to 2036, consistent with the World Dental Federation (FDI) policy guidance supporting evidence-based adoption of mercury-free restorative alternatives.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 12.42 Billion |

|

Revenue CAGR from 2026 to 2036 |

6.5% |

|

Largest Type Segment (2025) |

Indirect Restorative Materials |

|

Fastest Growing Type Segment |

Dental Biomaterials |

|

Largest End User (2025) |

Dental Clinics & Hospitals |

|

Fastest Growing End User |

Dental Laboratories |

|

Largest Geography (2025) |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, End User, and Geography |

|

Geographies Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Rising Prevalence of Dental Disorders Driving the Demand for Dental Materials

Dental disorders and conditions such as edentulism, dental caries, periodontal diseases, and malocclusion, pose a significant health burden globally. The increasing prevalence of these disorders drives demand for dental treatments and procedures. According to the WHO Global Oral Health Status Report 2022 and updated 2025 fact sheets, untreated dental caries in permanent teeth remains the most common health condition worldwide, with oral diseases collectively affecting approximately 3.7 billion people globally. Periodontal diseases are prevalent both in developed and developing countries, with severe periodontitis estimated to affect over 1 billion people worldwide, corresponding to a global age-standardized prevalence of approximately 12.5%. According to the Global Burden of Disease Study 2021, published in The Lancet in 2024–2025, approximately 3.69 billion people were affected by the main oral conditions globally in 2021, with the global economic burden of preventable oral diseases reaching an estimated $710 billion in 2024.

Malocclusion is one of the most prevalent clinical dental conditions, with systematic reviews estimating a global prevalence of approximately 56% to 74% depending on dentition stage and regional variation. In developing countries, the prevalence is expected to be higher due to limited access to oral healthcare and poor oral hygiene practices. Furthermore, the risk of dental diseases increases with age due to the progressive deterioration in the structure and function of oral tissues. Older adults are at increased risk of root caries due to increased gingival recession and higher use of medications that produce xerostomia; global prevalence of dental caries in adults aged 60 years and older is estimated at approximately 60.7%. The growth in the global geriatric population is expected to increase edentulism prevalence globally, resulting in the increased adoption of dental treatments and subsequently driving demand for dental materials; WHO estimates the global prevalence of complete tooth loss at approximately 7% among adults aged 20 years or older, rising to 23% among those aged 60 years or older.

Increasing Demand for Cosmetic Dentistry and Growth in Dental Tourism

The choices and requirements of Patients, ranging from mere hygiene to aesthetic image enhancement, are changing the dynamics of the dental industry. People today are more willing to invest in dental aesthetics than ever before. Baby boomers with high disposable incomes, the younger generation of working individuals who want the perfect appearance for better career prospects, and significant advances in tooth-colored restorative and prosthetic materials have contributed to the rise of cosmetic dentistry. The American Academy of Cosmetic Dentistry reports that a substantial majority of adults consider their smile an important social and professional asset, with cosmetic procedures such as teeth whitening, veneers, and clear aligners representing the fastest-growing segments of elective dental care.

Dental tourism is growing rapidly due to the increasing demand for cosmetic and restorative dentistry and the significantly lower costs of dental procedures in developing countries. The growth in dental tourism is largely observed in low-to-middle-income countries, mainly due to the lower cost of dental procedures. WHO and UNWTO joint reports indicate that Asia-Pacific accounted for approximately one-third of global health and wellness tourism flows in 2024, with Thailand and Malaysia reporting significant growth in inbound patients seeking dental care supported by national medical tourism frameworks. Countries in Asia-Pacific are preferred for medical and dental procedures that are significantly costlier in developed countries such as the U.S., Canada, and the U.K. The growth in dental tourism in developing countries is expected to increase demand for dental products and treatments, driving the demand for dental materials in these markets.

Why Does the Indirect Restorative Materials Segment Dominate the Dental Materials Market?

Based on type, in 2026, the indirect restorative materials segment is expected to account for the largest share of the global dental materials market. The adoption of indirect restorative materials is high due to the rising prevalence of periodontal diseases and dental caries. The World Health Organization's Oral Health Fact Sheet (March 2025) confirms that severe periodontal disease remains among the most prevalent noncommunicable conditions globally, with over 1 billion cases reported and prevalence concentrated in adults aged 35 years and older. The FDI World Dental Federation notes that severe periodontal diseases affect approximately 19% of the global adult population specifically, representing more than 1 billion cases worldwide. Additionally, the high awareness of dental health in developed countries, the increasing focus on dental aesthetics, and the growing adoption of all-ceramic and zirconia-based restorations as alternatives to metal-ceramic restorations contribute to the large market share of this segment. Indirect restorative materials include metal-ceramics, ceramics including zirconia and lithium disilicate, and other indirect restorative materials used in the laboratory fabrication of crowns, bridges, inlays, onlays, and removable prostheses.

However, the dental biomaterials segment is expected to witness the fastest CAGR during the forecast period of 2026 to 2036. The faster growth of this segment is driven by the growing number of dental implant procedures globally, the increasing adoption of guided bone regeneration and guided tissue regeneration techniques in implant and periodontal surgery, and the growing availability of advanced synthetic and biologic bone graft substitute materials. The expanding clinical acceptance of bone grafting procedures among general dental practitioners, in addition to specialist oral surgeons and periodontists, is broadening the commercial base for dental biomaterials products.

Why Does the Dental Clinics & Hospitals Segment Dominate the Dental Materials Market?

Based on end user, in 2026, the dental clinics and hospitals segment is expected to account for the largest share of the global dental materials market. The high preference of dental clinics and hospitals by patients for the diagnosis and treatment of dental conditions, rising technological developments in dentistry, the consolidation of dental clinics into large group practices, and the increasing prevalence of dental diseases contribute to the large market share of this segment. Dental clinics and hospitals are the preferred choice of patients for the treatment of dental conditions, and they represent the primary point of consumption for direct restorative materials, bonding agents, impression materials, and dental biomaterials used in surgical procedures. Globally, dental caries remains a significant public health issue, ranking as the fourth most costly chronic disease in terms of treatment expenses.

The dental products manufacturers segment is expected to witness significant CAGR during the forecast period. This growth is driven by the increasing demand from dental product manufacturers for specialty dental materials as raw inputs for the production of dental restorations, prosthetics, and devices. The growing adoption of digital manufacturing and industrial-scale CAD/CAM milling of dental restorations by large dental laboratory networks and dental service organizations is increasing demand for consistently formulated dental material feedstocks from manufacturers.

U.S. Dental Materials Market Size and Growth 2026 to 2036

The U.S. dental materials market is projected to grow at a significant CAGR from 2026 to 2036, driven by a well-established dental products industry, the presence of leading dental materials manufacturers and distributors, a high prevalence of dental diseases, high consumer awareness of dental health and cosmetic dentistry, and a robust dental insurance infrastructure that supports patient access to dental treatments.

How is North America Maintaining Dominance in the Dental Materials Market?

Based on geography, in 2026, North America is expected to account for the largest share of the global dental materials market. The major market share of North America is attributed to the high awareness of dental health, the large and well-established dental industry infrastructure, the high prevalence of dental caries and periodontal diseases in the region, the availability of dental insurance coverage supporting patient access to treatments, and the strong presence of leading dental materials manufacturers in the U.S. The U.S. dental materials market benefits from the presence of global market leaders including Dentsply Sirona Inc., Envista Holdings Corporation (Kerr, Nobel Biocare), and 3M Company, which have their headquarters or primary commercial operations in the U.S.

Which Factors Support the Growth of the Asia-Pacific Dental Materials Market?

Based on geography, Asia-Pacific is expected to grow at the fastest CAGR during the forecast period of 2026 to 2036. The growth of this market is attributed to the increasing prevalence of dental diseases in Asia-Pacific, the growing awareness of dental treatments and oral health, the rising healthcare spending across the region, and the growth in dental tourism. Countries including India, Thailand, Mexico, and Turkey are popular dental tourism destinations due to the significantly lower cost of dental procedures compared to developed countries. The large and growing population in China and India, combined with improving access to dental healthcare services and rising disposable incomes, provides significant market potential.

China, Japan, South Korea, and India are the major markets in Asia-Pacific for dental materials. Japan has a well-developed dental market supported by a universal healthcare system that includes dental coverage. China’s dental materials market is growing rapidly, driven by the large population, increasing dental disease awareness, expanding dental clinic networks, and government investment in oral health infrastructure; whereas, the Indian dental materials market is driven by a large and growing dental practitioner base, increasing urbanization, rising dental health awareness, and significant dental tourism activity.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by major players in the dental materials market between 2023 and 2026. The key players profiled in the dental materials market report are Dentsply Sirona Inc. (U.S.), Institut Straumann AG (Switzerland), Envista Holdings Corporation (U.S.), Kuraray Co., Ltd. (Japan), Ivoclar Vivadent AG (Liechtenstein), GC Corporation (Japan), Kulzer GmbH (Germany), Ultradent Products Inc. (U.S.), 3M Company (U.S.), ZimVie Inc. (U.S.), VOCO GmbH (Germany), Tokuyama Dental Corporation (Japan), Shofu Inc. (Japan), Mitsui Chemicals, Inc. (Japan), and Gc America Inc. (U.S.) among others.

Dental Materials Market, by Type

Dental Materials Market, by End User

Dental Materials Market, by Geography

This study provides a comprehensive assessment of the global dental materials market, including market size and forecast by material type and end user, along with value analysis across major regions and countries.

The global dental materials market is projected to reach USD 12.42 billion by 2036 from USD 6.62 billion in 2026, at a CAGR of 6.5% during the forecast period from 2026 to 2036.

Based on type, the indirect restorative materials segment is expected to account for the largest share of the dental materials market in 2026 due to the increasing demand for aesthetic, tooth-colored restorations and the rising burden of dental disorders globally.

Based on end user, the dental clinics & hospitals segment is expected to account for the largest share of the dental materials market in 2026 due to the growing preference for clinical dental procedures and the increasing prevalence of dental conditions.

The growth of this market is attributed to the rising prevalence of dental disorders, increasing demand for cosmetic dentistry, and the growth in dental tourism. Furthermore, the adoption of CAD/CAM technology and digital dentistry workflows, along with the growing demand for biocompatible and bioactive dental biomaterials, is expected to create significant growth opportunities for market participants.

Key companies operating in the global dental materials market include Dentsply Sirona Inc. (U.S.), Institut Straumann AG (Switzerland), Envista Holdings Corporation (U.S.), Kuraray Noritake Dental Inc. (Japan), Ivoclar Vivadent AG (Liechtenstein), GC Corporation (Japan), Kulzer GmbH (Germany), Ultradent Products Inc. (U.S.), 3M Company (U.S.), VOCO GmbH (Germany), Tokuyama Dental Corporation (Japan), Shofu Dental Corporation (Japan), DMG Chemisch-Pharmazeutische Fabrik GmbH (Germany), Septodont Holding (France), Coltene Holding AG (Switzerland), and VITA Zahnfabrik H. Rauter GmbH & Co. KG (Germany), among others.

Countries in the Asia-Pacific region are expected to offer significant growth opportunities for market players due to the rising prevalence of dental disorders, increasing awareness regarding oral health, growing healthcare expenditure, and the expansion of dental tourism.

Published Date: Nov-2024

Published Date: May-2024

Published Date: May-2024

Published Date: Apr-2023

Published Date: Aug-2018

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates