Resources

About Us

Automotive Aramid Fiber Market Size, Share & Trends Analysis by Type (Para-Aramid, Meta-Aramid), Application (Brake Pads & Clutch Facings, Reinforced Tires, Hoses, Belts & Gaskets), Vehicle Type (Passenger Vehicles, Commercial Vehicles, EVs), and Geography — Global Opportunity Analysis & Industry Forecast (2026–2036)

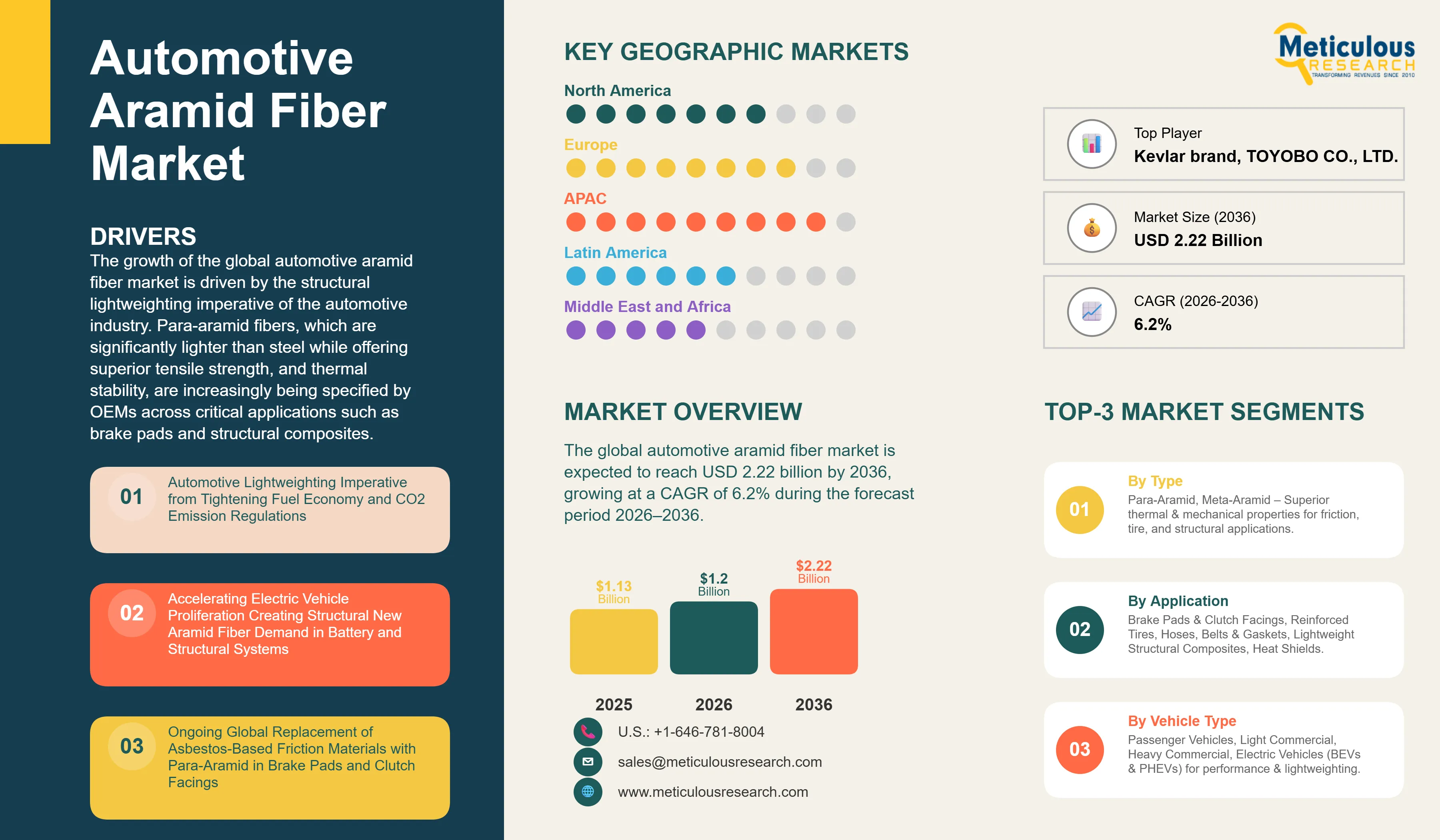

Report ID: MRAUTO - 1041857 Pages: 285 Apr-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global automotive aramid fiber market was valued at USD 1.13 billion in 2025. This market is expected to reach USD 2.22 billion by 2036 from an estimated USD 1.20 billion in 2026, growing at a CAGR of 6.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The growth of the global automotive aramid fiber market is primarily driven by the structural lightweighting imperative of the automotive industry. Para-aramid fibers, which are significantly lighter than steel while offering superior tensile strength, impact resistance, and thermal stability, are increasingly being specified by OEMs across critical applications such as brake pads, clutch facings, tire reinforcement, hoses, gaskets, and structural composites. This shift is evident across both internal combustion engine (ICE) and electric vehicle (EV) platforms, where weight reduction directly contributes to improved fuel efficiency, vehicle performance, and emissions compliance.

The growing electrification of the global vehicle fleet further strengthens demand for aramid fibers. In EV platforms, aramid materials are being utilized in battery thermal management systems, high-voltage cable insulation, and lightweight structural components that enhance vehicle range, durability, and safety. At the same time, increasingly stringent fuel economy and CO₂ emission regulations across major automotive markets, including North America, Europe, China, and India, are compelling OEMs to adopt fiber-reinforced composites as part of a broader, system-level mass reduction strategy.

However, the growth of this market is constrained by the relatively high cost of aramid fibers compared to conventional reinforcement materials such as glass fiber and steel. This cost differential limits adoption, mainly in price-sensitive vehicle segments and emerging markets. In addition, the processing of aramid fiber-reinforced composites remains complex, requiring specialized manufacturing equipment, controlled processing conditions, and advanced technical expertise, which can increase production costs and limit scalability for high-volume automotive applications.

Despite these challenges, several structural growth opportunities are emerging. The rapid expansion of electric vehicle production, mainly in China, which dominates global EV manufacturing, is creating incremental demand for aramid fibers in battery enclosures, thermal runaway mitigation systems, and lightweight body structures. Additionally, the increasing integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies is driving the need for durable, lightweight, and heat-resistant materials for sensor housings and electronic protection systems.

Electric Vehicle Proliferation Creating Structural New Aramid Fiber Demand Categories

The growing global adoption of battery electric vehicles (BEVs) is creating significant demand for automotive aramid fibers. This trend is led by China, the world’s largest EV market, alongside rapidly increasing EV penetration across Europe, North America, and Southeast Asia. While global EV adoption surpassed 2024 milestones, continued double-digit growth in EV production through 2025–2026 is driving demand for advanced materials tailored to electrified powertrains, mainly in thermal management, electrical insulation, and lightweight structural applications.

Battery-pack thermal management is a key new application area. Para-aramid fiber-reinforced composite sheets and meta-aramid non-woven materials are increasingly specified as intumescent thermal barriers within battery modules and between individual cells to mitigate thermal runaway propagation. These materials are critical for compliance with evolving battery safety standards, including China’s GB/T framework and international standards such as IEC 62660, which continue to tighten as EV deployment scales globally.

Lightweight body-in-white structures are emerging as one of the fastest-growing application segments. Para-aramid-reinforced composites enable significant weight reduction compared to conventional steel while maintaining comparable crash energy absorption performance. This directly improves vehicle efficiency by reducing mass, thereby enhancing BEV driving range and optimizing energy consumption across vehicle platforms.

In addition, high-voltage cable insulation is becoming an increasingly important demand driver. Meta-aramid and para-aramid braided sleeving materials are being widely adopted in 400–800 V battery management systems to provide thermal resistance, electrical insulation, and mechanical protection. As EV platforms transition toward higher-voltage architectures to support ultra-fast charging and improved system efficiency, demand for advanced aramid-based insulation solutions is expected to expand further over the forecast period.

Lightweighting Imperative and Regulatory Stringency Driving Structural Composite Adoption

The combination of tightening global fuel‑economy and CO₂‑emission regulations, including the U.S. CAFE standards targeting 49+ mpg by 2026, the EU’s 95 g CO₂/km fleet‑average target, and China’s Phase 4 fuel‑consumption framework, with the EV‑platform design imperative to maximize energy efficiency through mass reduction is driving automotive OEMs to systematically adopt para‑aramid fiber‑reinforced composites in structural applications that were previously served by steel, aluminum, or glass‑fiber‑reinforced polymers.

Para‑aramid composites deliver tensile strengths in the 2,700–3,600 MPa range, approaching the performance of carbon fiber at roughly one‑third the material cost, and combine this with superior impact resistance and toughness, which makes them preferred over carbon fiber for automotive crash‑critical structures and underbody‑protection components where energy absorption rather than stiffness is the primary design requirement.

Advances in processing technologies, such as resin transfer molding (RTM), vacuum‑assisted resin infusion (VARI), and thermoplastic compression molding using pre‑impregnated aramid fabrics, are now enabling cycle times compatible with automotive‑production rates, making structural para‑aramid composites commercially scalable for mid‑volume and increasingly high‑volume vehicle programs.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 2.22 Billion |

|

Market Size in 2026 |

USD 1.20 Billion |

|

Market Size in 2025 |

USD 1.13 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.2% |

|

Dominating Type |

Para-Aramid |

|

Fastest Growing Type |

Para-Aramid (Lightweight Structural Composites) |

|

Dominating Application |

Brake Pads & Clutch Facings |

|

Fastest Growing Application |

Lightweight Structural Composites |

|

Dominating Vehicle Type |

Passenger Vehicles |

|

Fastest Growing Vehicle Type |

Electric Vehicles (EVs) |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on type, the global automotive aramid fiber market is segmented into para-aramid and meta-aramid. In 2026, the para-aramid segment is expected to account for the largest share of the global automotive aramid fiber market. This dominance is primarily attributed to its superior mechanical and thermal performance characteristics, including tensile strength significantly higher than steel at a fraction of the weight, high modulus, and excellent heat resistance. These properties make para-aramid particularly suitable for demanding automotive applications such as brake pads, clutch facings, tire reinforcement, power transmission belts, hydraulic hoses, gaskets, and structural composite components, where strength-to-weight ratio and durability under dynamic loading are critical.

In addition, para-aramid fibers exhibit high thermal stability, withstanding elevated temperatures typically encountered in friction materials without significant degradation. This enables reliable performance in braking systems and other high-heat environments. The segment is also expected to register the highest growth rate during the forecast period, driven by increasing adoption in lightweight structural composites for electric vehicle (EV) platforms and growing demand for high-performance tire reinforcement in premium and performance vehicles.

The meta-aramid segment, while smaller in market share, plays a critical role in applications requiring enhanced thermal and flame resistance. Meta-aramid fibers are widely used in automotive heat shields, underbody insulation, engine compartment fire barriers, and high-voltage cable insulation in EVs. Their inherent flame resistance, flexibility, and conformability make them well-suited for protective and insulation applications where exposure to high temperatures and fire risk is a concern.

This segment is expected to witness steady growth over the forecast period, driven by increasing EV adoption and the associated demand for high-voltage cable insulation and battery compartment thermal protection solutions. As vehicle architectures continue to evolve toward electrification, the complementary roles of para-aramid and meta-aramid fibers are expected to strengthen across both structural and thermal management applications.

Based on application, the global automotive aramid fiber market is segmented into brake pads and clutch facings, reinforced tires, hoses, belts & gaskets, racing vehicle components, heat shields & thermal insulation, and lightweight structural composites. In 2026, the brake pads & clutch facings segment is expected to account for the largest share of the market. This dominance is primarily attributed to the widespread use of para-aramid pulp and short fibers as a high-performance, non-hazardous alternative to asbestos in automotive friction materials. Para-aramid enables stable friction performance, high thermal resistance, and effective structural reinforcement of friction matrices, making it a preferred material in both OEM and aftermarket brake system applications.

However, the lightweight structural composites segment is expected to register the highest CAGR during the forecast period. This growth is driven by the transition toward electric and fuel-efficient vehicles, where para-aramid-reinforced composites are increasingly used in body panels, underbody protection systems, reinforcement beams, and interior structural components. These materials enable substantial weight reduction while maintaining or enhancing crash performance, thereby supporting automakers in achieving both efficiency and safety targets.

Based on vehicle type, the global automotive aramid fiber market is segmented into passenger vehicles, light commercial vehicles, heavy commercial vehicles, and electric vehicles. In 2026, passenger vehicles are expected to account for the largest share of the global automotive aramid fiber market. This is primarily attributed to their dominant share in global vehicle production, estimated at approximately 70–75 million units annually, and relatively higher per-unit consumption of aramid fibers, particularly in premium and performance segments.

Applications such as para-aramid-based brake pad compounds, tire reinforcement, and structural composites are more extensively utilized in passenger vehicles, especially where performance, durability, and lightweighting are prioritized.

Premium and luxury passenger vehicle manufacturers such as BMW AG, Mercedes-Benz Group AG, Porsche AG, Audi AG, and Toyota Motor Corporation (Lexus division) are among the most intensive adopters of aramid fiber-reinforced materials. These OEMs increasingly incorporate aramid-based components in structural and friction applications where high performance, safety, and weight reduction justify higher material costs.

However, the electric vehicle segment is expected to register the highest CAGR during the forecast period. This growth is driven by the emergence of new application areas specific to EV architectures, including battery thermal management systems, high-voltage cable insulation, and lightweight structural composites. These applications are critical for enhancing safety, improving energy efficiency, and extending vehicle range.

The rapid expansion of the global EV fleet, led by China as the largest EV production hub, is further driving demand for aramid fibers. Leading EV manufacturers such as BYD Company Limited, SAIC Motor Corporation Limited, Geely Automobile Holdings Limited, and NIO Inc. are driving large-scale adoption, positioning Asia Pacific as the primary growth engine for EV-related aramid fiber demand over the forecast period.

Based on geography, the global automotive aramid fiber market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, Asia Pacific is expected to hold the largest market share of the global automotive aramid fiber market.

The growth of Asia Pacific automotive aramid fiber is driven by the its established leadership as the world's largest automotive production hub, with China alone producing over 30 million vehicles annually, combined with the world's most rapidly growing EV market that is creating new aramid fiber demand in battery thermal management, high-voltage cable management, and lightweight structural applications.

Local governments in China, India, Japan, and South Korea are enforcing increasingly stringent emissions and safety standards that promote the adoption of aramid-reinforced components by friction material manufacturers and composite suppliers serving regional OEMs. China's domestic para-aramid producers including Yantai Tayho and SRO Aramid Jiangsu are simultaneously expanding supply availability and reducing the cost premium over glass fiber alternatives for standard-grade applications, further driving the growth of this market.

Europe is the second-largest regional market, driven by its stringent Euro 7 emission regulations, high concentration of premium OEMs intensive in aramid composite adoption, and the established leadership of European friction material manufacturers, including TMD Friction and SGL Carbon in para-aramid brake compound technology.

North America is also a significant market for automotive aramid fiber, driven by the U.S. defense procurement of para-aramid composites for military vehicle programs that benefit civilian automotive-grade fiber producers through shared R&D and process technology infrastructure.

The global automotive aramid fiber market is characterized by a highly concentrated supply structure at the fiber production level, with DuPont de Nemours, Inc. and Teijin Limited (through Teijin Aramid B.V.) collectively accounting for a substantial share of premium automotive-grade para-aramid supply. These companies benefit from long-established technological capabilities, proprietary production processes, and strong OEM relationships. They are supported by other key manufacturers, including Kolon Industries, Inc. and Hyosung Advanced Materials Corporation in South Korea; Toray Industries, Inc. in Japan; and emerging Chinese producers such as Yantai Tayho Advanced Materials Co., Ltd. and SRO Aramid (Jiangsu) Co., Ltd.

The competitive landscape is primarily shaped by the technology leadership and brand equity of DuPont de Nemours, Inc. and Teijin Limited in high-performance para-aramid grades, which are widely specified in demanding automotive applications such as structural composites and high-performance tire reinforcement. These incumbents maintain a strong competitive advantage due to their ability to meet stringent OEM qualification standards, ensure consistent product quality, and support advanced application engineering requirements. In contrast, several Chinese manufacturers are still in the process of scaling production capabilities and achieving comparable levels of OEM qualification, particularly in high-value automotive applications.

The report provides a comprehensive competitive analysis based on an extensive assessment of key players’ product portfolios, geographic presence, and strategic developments over the past few years. Key companies operating in the global automotive aramid fiber market include DuPont de Nemours, Inc., Teijin Limited, Kolon Industries, Inc., Hyosung Advanced Materials Corporation, Toray Industries, Inc., Yantai Tayho Advanced Materials Co., Ltd., X FIPER New Material Co., Ltd., Huvis Corporation, SRF Limited, Kermel S.A., SRO Aramid (Jiangsu) Co., Ltd., Teijin Frontier Co., Ltd., China National Bluestar (Group) Co., Ltd., TOYOBO CO., LTD., and Solvay S.A. among others.

The global automotive aramid fiber market is expected to reach USD 2.22 billion by 2036 from an estimated USD 1.20 billion in 2026, at a CAGR of 6.2% during the forecast period 2026–2036.

In 2026, para-aramid is expected to hold the largest market share of the global automotive aramid fiber market, driven by its superior mechanical and thermal properties making it ideal for brake pads, tire reinforcement, and structural composite applications.

In 2026, brake pads and clutch facings is expected to hold the largest market share, driven by para-aramid's established role as the premium asbestos substitute in automotive friction materials globally.

Lightweight structural composites is expected to register the highest CAGR during the forecast period, driven by the global automotive shift toward electric and fuel-efficient vehicles where para-aramid composites deliver significant mass reduction at equivalent crash performance.

The electric vehicle segment is expected to register the highest CAGR during the forecast period, driven by structural new aramid fiber applications in battery thermal management, high-voltage cable insulation, and lightweight structural components.

The growth of this market is primarily driven by the automotive lightweighting imperative from fuel economy and CO2 regulations, accelerating EV proliferation creating structural new demand for aramid in battery systems and lightweight structures, and ongoing asbestos replacement in friction materials globally. Key opportunities include thermoplastic aramid composite processing enabling mass production scalability, EV-specific battery thermal barrier applications, and the expanding Chinese EV market driving regional fiber demand.

Key players are DuPont de Nemours, Inc. (U.S.) — Kevlar brand, Teijin Limited / Teijin Aramid B.V. (Japan/Netherlands) — Twaron and Technora brands, Kolon Industries, Inc. (South Korea) — HERACRON brand, Hyosung Advanced Materials Corporation (South Korea), Toray Industries, Inc. (Japan) — Mictron and ARAWIN brands, Yantai Tayho Advanced Materials Co., Ltd. (China) — TAMETAR and Newstar brands, X-FIPER New Material Co., Ltd. (China), Huvis Corporation (South Korea), SRF Limited (India), Kermel S.A. (France), SRO Aramid (Jiangsu) Co., Ltd. (China), Teijin Frontier Co., Ltd. (Japan), China National Bluestar (Group) Co., Ltd. (China), TOYOBO CO., LTD. (Japan), and Solvay S.A. (Belgium).

Asia Pacific is expected to register the highest growth rate in the global automotive aramid fiber market during the forecast period 2026–2036, driven by China's EV production dominance, India's expanding automotive manufacturing base, and the region's large-scale transition from asbestos-based to para-aramid friction materials.

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Sep-2024

Published Date: Jun-2024

Published Date: Aug-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates