Resources

About Us

Theranostics Market Size, Share & Trends Analysis by Product & Service (Therapeutics, Diagnostics, Instruments), Technology (Radioligand Therapy, Targeted Alpha Therapy, Nanotheranostics), Application, End User, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

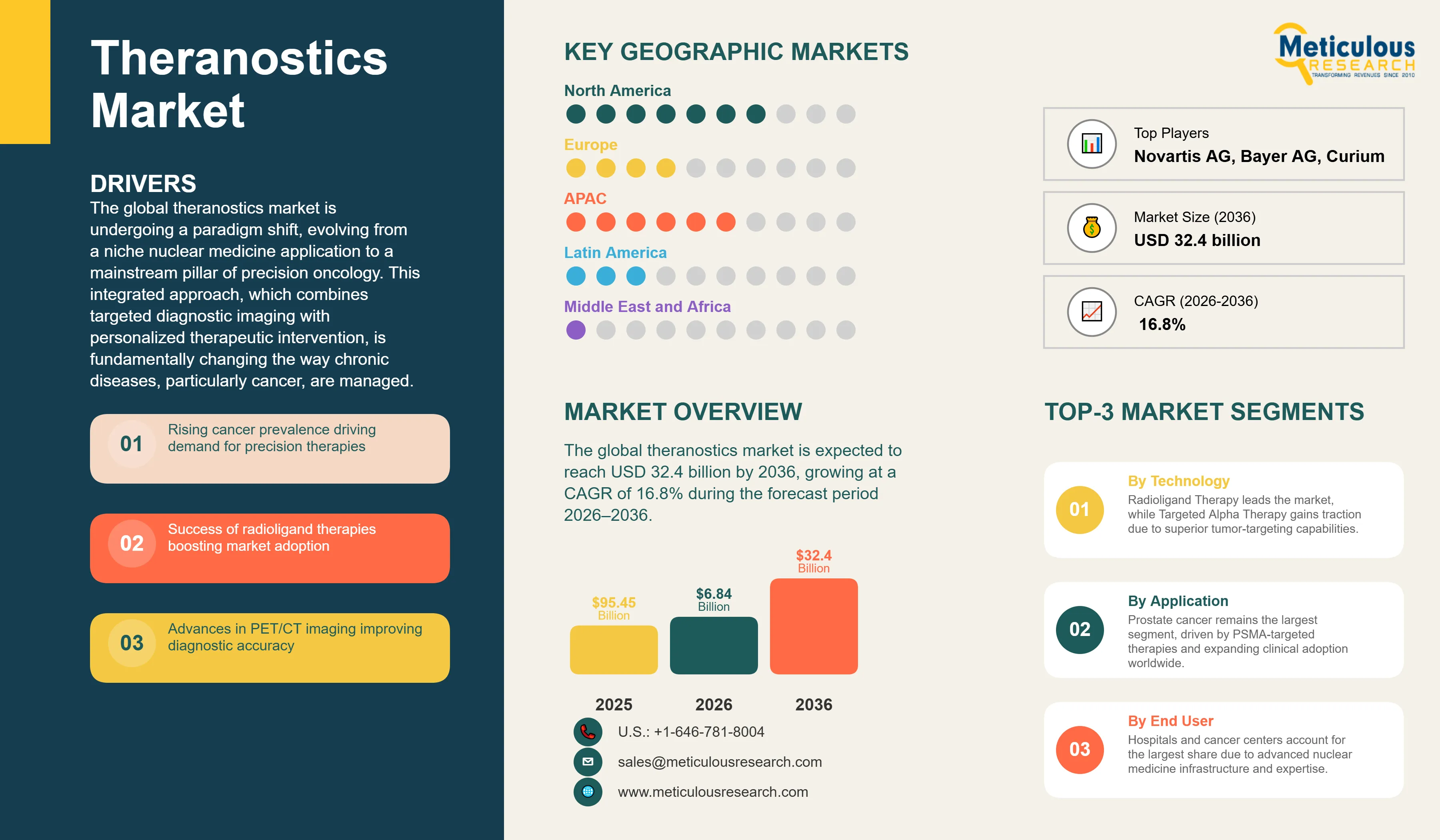

Report ID: MRHC - 1042029 Pages: 285 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global theranostics market was valued at USD 6.84 billion in 2026. This market is expected to reach USD 32.4 billion by 2036, growing at a CAGR of 16.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global theranostics market is undergoing a paradigm shift, evolving from a niche nuclear medicine application to a mainstream pillar of precision oncology. This integrated approach, which combines targeted diagnostic imaging with personalized therapeutic intervention, is fundamentally changing the way chronic diseases, particularly cancer, are managed. By using the same targeting molecule for both detecting and treating a disease, theranostics allows for unprecedented precision, ensuring that the right treatment is delivered to the right patient at the right time. The market's robust growth is primarily fueled by the commercial success of radioligand therapies (RLTs), which have demonstrated superior clinical outcomes in late-stage cancers that were previously considered untreatable.

The commercial success of Novartis' Pluvicto for metastatic prostate cancer and Lutathera for neuroendocrine tumors has validated the theranostic model on a global scale. Oncology remains the dominant application area, accounting for approximately 85% of market revenue, driven by the growing global cancer burden and the increasing demand for highly targeted treatment approaches with improved efficacy and safety profiles. Global cancer incidence is projected to rise substantially over the coming decades, supporting continued adoption of theranostic solutions. Beyond oncology, theranostic approaches are being explored in cardiovascular and neurological disorders, creating opportunities for future growth through advanced molecular imaging and targeted therapeutic strategies. The integration of high-resolution PET/CT and SPECT/CT systems continues to strengthen the diagnostic component of theranostics by providing detailed molecular information that supports patient selection, treatment planning, and response monitoring.

Technological advancements remain a key driver of theranostics market growth, with increasing emphasis on Targeted Alpha Therapy (TAT). Alpha-emitting isotopes such as Actinium-225 (Ac-225) deliver highly localized, high-energy radiation and have demonstrated significant potential for targeting tumor cells while limiting radiation exposure to adjacent healthy tissues due to their short path length. As a result, TAT has attracted substantial investment from leading pharmaceutical companies, contributing to a wave of strategic acquisitions and partnerships across the radiopharmaceutical sector. In parallel, the development of nanotheranostics, which integrates targeted drug delivery with diagnostic imaging capabilities, is creating new opportunities for precision medicine and the development of personalized treatment strategies.

Geographically, North America is expected to remain the largest regional market, accounting for approximately 42% of global revenue in 2026. The region's leadership is supported by a strong research ecosystem, favorable regulatory pathways, established radiopharmacy networks, and advanced nuclear medicine infrastructure. Asia-Pacific is projected to register the fastest growth during the forecast period, driven by rising cancer incidence, expanding healthcare investments, and increasing deployment of cyclotron facilities and radiopharmaceutical manufacturing capabilities in countries such as China and India. As investments in isotope production infrastructure improve supply availability and clinical evidence continues to support the use of theranostic agents in earlier treatment settings, the market is expected to maintain strong double-digit growth through 2036.

The primary driver for the theranostics market is the proven clinical and commercial success of targeted radioligand therapies. These treatments have provided significant survival benefits in patients with metastatic cancers, leading to rapid adoption by oncologists worldwide. Furthermore, the rising global prevalence of cancer and the increasing demand for precision medicine—which reduces healthcare costs by avoiding ineffective treatments are significant catalysts. Advancements in molecular imaging technology, particularly the development of high-sensitivity PET/CT systems, are also enhancing the diagnostic accuracy and patient monitoring capabilities of theranostic platforms.

A major restraint is the complex and highly regulated supply chain for medical isotopes, many of which have short half-lives requiring just-in-time manufacturing and sophisticated logistics. The high initial cost of establishing nuclear medicine infrastructure, including cyclotrons and specialized PET/CT suites, also poses challenges, particularly in resource-limited settings. Furthermore, the shortage of trained nuclear medicine specialists and radiopharmacists can limit the capacity of healthcare systems to scale theranostic services.

Significant opportunities exist in the development of next-generation alpha-emitting theranostics, which offer superior efficacy in treating micro-metastatic disease. The expansion of theranostic agents into earlier lines of therapy—moving from salvage treatment to first-line settings—presents a massive growth path. Furthermore, the application of theranostics in non-oncology areas, such as identifying vulnerable atherosclerotic plaques or neurodegenerative biomarkers, offers long-term diversification. The move toward decentralized radiopharmaceutical production through automated 'pharmacy-on-a-chip' technology also presents a high potential for market scaling.

A key challenge is navigating the complex regulatory hurdles for integrated platforms, as the co-approval of a diagnostic agent and its corresponding therapeutic counterpart requires extensive clinical validation. Ensuring a stable and redundant supply of critical isotopes like Lutetium-177 and Actinium-225 remains a persistent challenge for manufacturers. Furthermore, the standardization of dosimetry—the calculation of the exact radiation dose delivered to the tumor—is critical for optimizing patient outcomes and minimizing toxicity, requiring sophisticated software and specialized expertise.

Targeted Alpha Therapy (TAT) is emerging as one of the most significant technological trends in the theranostics market. Alpha-emitting isotopes such as Actinium-225 (Ac-225) deliver high linear energy transfer (LET) radiation over a short path length, enabling highly localized tumor cell destruction while limiting exposure to surrounding tissues. Growing interest in TAT is supported by the rising global cancer burden, with the International Agency for Research on Cancer (IARC) projecting 28.4 million new cancer cases annually by 2040, up from 19.3 million in 2020. The need for more effective therapies for metastatic and treatment-resistant cancers is accelerating investment in Ac-225-based radiopharmaceutical development across the industry.

The theranostics industry is witnessing substantial consolidation as major pharmaceutical companies seek to strengthen their radiopharmaceutical capabilities. In 2024, AstraZeneca acquired Fusion Pharmaceuticals for approximately USD 2.0 billion to expand its radioconjugate oncology portfolio, while Bristol Myers Squibb completed the acquisition of RayzeBio to gain access to its Actinium-225-based radiopharmaceutical platform and manufacturing capabilities. Similar strategic investments by Eli Lilly through the acquisition of POINT Biopharma highlight growing confidence in theranostics as a key pillar of future precision oncology strategies.

Based on technology, the market is segmented into Radioligand Therapy (RLT), Targeted Alpha Therapy (TAT), Nanotheranostics, and Others. In 2026, the Radioligand Therapy segment is expected to hold the largest share of the market. This dominance is driven by the commercial success of FDA-approved agents like Pluvicto and Lutathera, which have established RLT as a standard of care in metastatic settings.

The Targeted Alpha Therapy (TAT) segment is projected to witness the fastest growth during the forecast period. The potential for TAT to treat micro-metastatic disease with higher precision and lower toxicity is driving intense clinical research and investment.

Based on application, the market is segmented into Prostate Cancer, Neuroendocrine Tumors (NETs), Bone Metastasis, and Others. In 2026, the Prostate Cancer segment is expected to hold the largest share of the market. The high prevalence of prostate cancer and the rapid adoption of PSMA-targeted theranostics are the primary growth drivers.

The Prostate Cancer segment is also projected to witness the fastest growth as indications expand to include earlier-stage patients and as the availability of PSMA-PET imaging increases globally.

North America is expected to hold the largest share of the global theranostics market in 2026, accounting for around 42% of the total revenue. This is due to a robust R&D ecosystem, rapid regulatory approvals from the FDA, and a well-established nuclear medicine infrastructure. Key companies operating in the North American market include GE HealthCare, Lantheus, and Cardinal Health.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region is investing heavily in radiopharmaceutical manufacturing and cyclotron networks, particularly in China and India. The rising incidence of cancer and the increasing adoption of precision medicine are the primary growth drivers. Key companies operating in the Asia-Pacific market include Telix Pharmaceuticals and major global vendors.

The global theranostics market is characterized by intense competition and rapid consolidation. Novartis currently leads the therapeutic segment following its strategic acquisitions, while GE HealthCare and Siemens Healthineers dominate the imaging and instrumentation space. Competition is centered on the development of novel targeting molecules, securing isotope supply chains, and clinical validation in earlier lines of therapy.

Strategic partnerships between pharmaceutical companies and isotope producers are critical for ensuring a stable supply of Lu-177 and Ac-225. Companies are also investing in digital dosimetry platforms to optimize treatment planning and improve patient safety. Key players in the global theranostics market include Novartis AG, Bayer AG, GE HealthCare, Siemens Healthineers, Lantheus Holdings, Cardinal Health, Curium, Telix Pharmaceuticals, ITM Isotope Technologies Munich SE, and Eli Lilly (Point Biopharma).

The market is projected to reach USD 32.4 billion by 2036, growing at a CAGR of 16.8% from 2026 to 2036.

Prostate cancer is the fastest-growing application due to the success of PSMA-targeted radioligand therapies.

TAT uses alpha-emitting isotopes like Ac-225 for high-potency, short-range destruction of tumor cells with minimal damage to healthy tissue.

The Asia-Pacific region is projected to witness the fastest growth due to heavy investment in radiopharmaceutical infrastructure.

It uses a diagnostic imaging agent to confirm the presence of a specific target before delivering the corresponding therapeutic agent.

The market is expected to grow at a CAGR of 16.8% during the forecast period 2026–2036.

Novartis AG currently leads the segment with its blockbuster agents Pluvicto and Lutathera.

The high cost of PET/CT infrastructure and the complex logistics of short-lived isotopes are the main restraints.

Molecular imaging provides the 'diagnostic' component, allowing for real-time visualization of disease targets and treatment response.

The market is led by Novartis, Bayer, GE HealthCare, Siemens Healthineers, and Lantheus.

Published Date: Jan-2025

Published Date: Jul-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates