Resources

About Us

Speech and Voice Recognition Market by Function (Speech Recognition, Voice Recognition), Technology (AI and Non-AI), Deployment Mode (Cloud, On-premise), End User (IT & Telecommunications, BFSI, Healthcare, Consumer Electronics, Automotive, and Other End Users), and Geography – Global Forecast to 2036

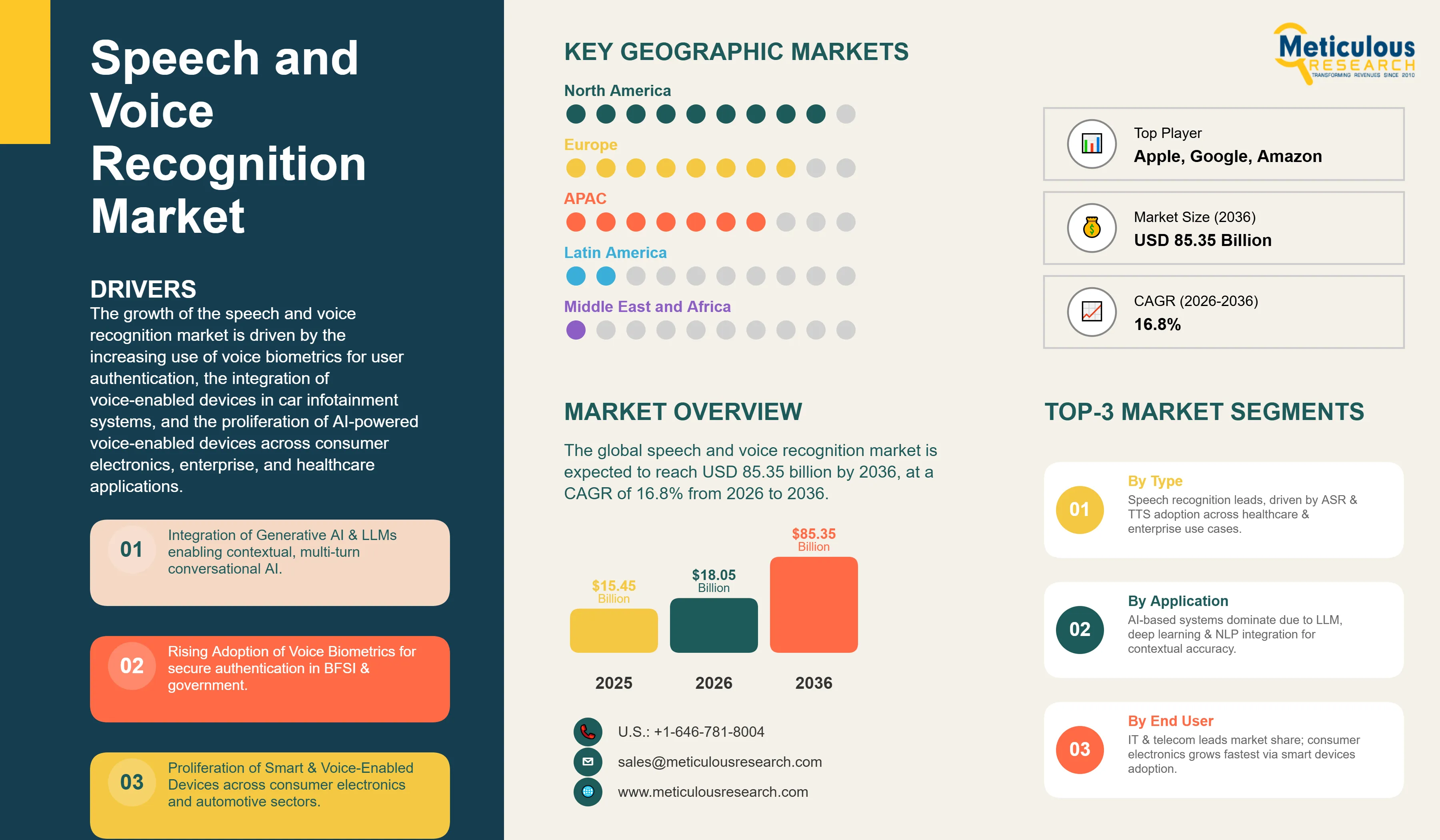

Report ID: MRICT - 104339 Pages: 240 Mar-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 48 Hours Download Free Sample ReportThe global speech and voice recognition market was valued at USD 15.45 billion in 2025. This market is expected to reach USD 85.35 billion by 2036 from USD 18.05 billion in 2026, at a CAGR of 16.8% from 2026 to 2036.

The growth of the speech and voice recognition market is driven by the increasing use of voice biometrics for user authentication, the integration of voice-enabled devices in car infotainment systems, and the proliferation of AI-powered voice-enabled devices across consumer electronics, enterprise, and healthcare applications. The growing integration of generative AI and large language models (LLMs) into speech and voice recognition platforms represents a defining development transforming the market, enabling context-aware, multi-turn conversational interactions that far surpass the command-and-control capabilities of earlier voice recognition systems.

By early 2026, major technology platforms had transitioned from pilot initiatives to scaled commercial deployment of LLM-integrated voice interfaces. Amazon expanded the rollout of Alexa+ with generative responses and persistent multi-turn context; Apple broadened integration of its conversational Siri under the Apple Intelligence framework with goal-oriented task execution; Microsoft embedded voice-enabled Copilot experiences across Windows, Teams, and Edge; and Google scaled Gemini Live for real-time, multimodal voice-native interactions across supported devices.

Venture capital investment in voice AI increased more than sixfold between 2022 and 2024, rising from approximately USD 315 million to over USD 2 billion, and remained strong through 2025 as investor conviction in voice as a primary interface layer intensified across enterprise and consumer applications. ElevenLabs raised a USD 180 million Series C round in January 2025 at a valuation exceeding USD 3 billion, underscoring robust demand for generative voice technologies. SoundHound AI raised its 2025 revenue outlook to USD 157–177 million, driven by a contracted bookings backlog exceeding USD 1 billion. The growing demand for voice authentication in mobile banking applications, increased integration of AI and machine learning into speech recognition platforms, and rising adoption of speech-based biometric systems are expected to generate substantial growth opportunities for the players in this market throughout the forecast period.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Integration of Generative AI and Large Language Models into Speech Recognition Platforms

The integration of generative AI and large language models (LLMs) into speech and voice recognition platforms represents the most transformative technological trend reshaping the market. Traditional speech recognition systems excelled at converting spoken words to text but lacked the contextual understanding and reasoning capabilities necessary for natural, multi-turn conversations. The incorporation of LLMs such as GPT-4, Gemini, and proprietary enterprise models into speech processing pipelines enables systems to infer user intent from previous queries, tone, and sentence structure, handle complex multi-turn dialogues, recall past interactions, and deliver highly tailored responses. By mid-2025, this LLM integration had moved from experimental to mainstream: Amazon’s Alexa+ incorporated generative responses; Apple previewed a conversational Siri with goal-oriented planning; Microsoft deployed ‘Hey Copilot’ voice interaction across its entire software ecosystem; and Google debuted Gemini Live for real-time voice-native multimodal conversations. Y Combinator reported a 70% rise in vertical voice AI startups between winter and fall 2024, underscoring the explosive commercial momentum around LLM-integrated voice applications across healthcare, finance, logistics, and customer service.

Rising Adoption of Voice Biometrics for Security and User Authentication

The rising adoption of voice biometrics for user authentication across the BFSI, government, and enterprise sectors is a prominent trend driving sustained growth in the speaker verification and identification segment of the speech and voice recognition market. Voice biometric authentication enables organizations to verify user identity through the unique acoustic characteristics of individual voices, offering a frictionless, hands-free authentication experience that is increasingly preferred over traditional PIN, password, and knowledge-based authentication methods. Consistently increasing instances of fraud and identity theft across the BFSI, retail and e-commerce, and legal sectors are intensifying demand for high-level security technologies including voice biometrics. The BFSI sector leads voice AI adoption with a 32.9% market share in 2024, with financial institutions deploying voice biometrics for mobile banking authentication, e-banking security, call center customer verification, and app-based transaction authorization. Growing concerns about personal data security and the increasing regulatory focus on strong customer authentication are reinforcing the voice biometrics adoption trend across digital financial services globally.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 85.35 Billion |

|

Market Size in 2025 |

USD 15.45 Billion |

|

Market Size in 2026 |

USD 18.05 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 16.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Function: Speech Recognition (Automatic Speech Recognition, Text-to-Speech), Voice Recognition (Speaker Identification, Speaker Verification) By Technology: Artificial Intelligence, Non-Artificial Intelligence By Deployment Mode: Cloud-based Deployments, On-premise Deployments By End User: IT & Telecommunications, Media & Entertainment, BFSI, Healthcare, Manufacturing/Enterprises, Education, Government and Public Services, Retail and E-commerce, Automotive, Consumer Electronics, Other End Users By Geography: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Why Does the Speech Recognition Segment Dominate the Speech and Voice Recognition Market?

Based on function, the speech recognition segment is expected to account for the largest share of the global speech and voice recognition market in 2026. The dominant share of this market is attributed to the consistent proliferation of AI, machine learning, and deep learning across the healthcare, education, enterprise, and consumer electronics sectors, and the rapid expansion of the smart devices market that embeds ASR capabilities. The automatic speech recognition (ASR) sub-segment captured the majority of market share in 2025 across industries including customer service, healthcare documentation, education, media captioning, and virtual assistant applications. The text-to-speech (TTS) sub-segment is also experiencing strong growth driven by the rapid expansion of voice AI agents, audiobook and podcast generation, accessibility applications, and the proliferation of LLM-powered conversational systems requiring natural-sounding synthetic speech output.

The voice recognition segment, encompassing speaker identification and speaker verification, is expected to register the highest CAGR during the forecast period, driven by the surging demand for voice biometric security solutions across the BFSI, government, and enterprise sectors and the growing adoption of voice-based authentication in mobile banking, e-commerce, and digital identity applications.

Why Does the Artificial Intelligence Segment Dominate the Speech and Voice Recognition Market?

Based on technology, the artificial intelligence segment is expected to account for the largest share of the global speech and voice recognition market in 2026 and is also expected to register the fastest growth through 2036. The dominant position of AI-based speech and voice recognition reflects the fundamental superiority of deep learning-based ASR models over traditional rule-based and statistical approaches in terms of recognition accuracy, language coverage, adaptability, and contextual understanding. AI-enabled voice assistants are now embedded in smart home systems, smart speakers, autonomous and connected vehicles, smartphones, and smart wearables, creating a massive and growing installed base of AI-powered voice recognition endpoints. The integration of LLMs into voice AI systems, driven by Microsoft’s expansion of Azure AI Speech with OpenAI-powered models and Amazon’s advanced multilingual streaming speech capabilities within AWS, is enabling superior accuracy, contextual adaptation, and natural language understanding at scale. Several organizations are partnering to provide AI-enabled speech and voice analysis solutions for specific verticals; in January 2025, ElevenLabs raised a USD 180 million Series C round to expand enterprise deployment of its generative AI-powered voice platform across media, customer engagement, and enterprise applications.

Why Does the Cloud-Based Deployments Segment Register the Higher CAGR?

Based on deployment mode, cloud-based deployments are expected to grow at the highest CAGR during the forecast period, driven by the scalability, cost-effectiveness, and ease of integration that cloud platforms provide for enterprises deploying speech and voice recognition solutions. Cloud deployment allows businesses to access advanced speech recognition capabilities without heavy investment in on-premises hardware and software infrastructure, making high-quality ASR accessible to organizations of all sizes, including startups and SMEs.

Cloud platforms, including Amazon Web Services (Amazon Lex, Transcribe), Microsoft Azure (AI Speech Service), and Google Cloud (Speech-to-Text API), provide continuously updated neural speech models, RESTful APIs, real-time and batch processing capabilities, and multilingual support that accelerate development, deployment, and customization. The expansion of remote work, virtual collaboration platforms, and cloud-based enterprise software ecosystems is further driving the adoption of cloud ASR for real-time meeting transcription, voice-enabled CRM systems, conversational AI assistants, and contact center analytics. Meanwhile, on-premise and private cloud deployments continue to hold strategic relevance for organizations with stringent data sovereignty, privacy, security, or ultra-low latency requirements, particularly across regulated healthcare, government, defense, and financial services sectors.

Why Does the IT & Telecommunications Segment Dominate the Speech and Voice Recognition Market?

Based on end user, the IT & telecommunications segment is expected to account for the largest share of the global speech and voice recognition market in 2026. The largest share of this segment is mainly attributed to the extensive adoption of voice recognition in contact centers for call transcription and analytics, IVR (interactive voice response) automation, virtual agent deployment, first-call resolution improvement, and agent assistance tools. The increasing focus of the regional telecommunications companies on improving first-call resolution rates, combined with enterprise adoption of cloud communication platforms requiring voice AI capabilities, drives the adoption of speech and voice recognition technologies for IT & telecommunications. The growing demand for speech analytics solutions in contact centers, enabling real-time transcription, sentiment analysis, compliance monitoring, and agent coaching, is a particularly strong sub-driver within this segment.

However, the consumer electronics segment is expected to grow at the highest CAGR during the forecast period, driven by the rapid proliferation of smart speakers, smartphones, AI-enabled home appliances, smart televisions, and wearable devices incorporating voice recognition capabilities. Over 35% of new smart consumer product development efforts are focused on improving voice assistants and AI interaction capabilities, reflecting the growing investment in voice-first user experience design. The BFSI and healthcare segments also represent significant growth opportunities, driven by voice biometric adoption and AI-powered clinical documentation respectively.

Based on geography, North America is expected to account for the largest share of the global speech and voice recognition market in 2026. This is driven by the concentration of leading speech and voice recognition technology providers including Microsoft Corporation, Amazon Web Services, Google, IBM, Apple, Verint Systems, Speechmatics, Sensory, and AssemblyAI; the advanced digital infrastructure and high penetration of smart devices; the strong demand for speech analytics solutions in contact centers; and the extensive adoption of AI-powered enterprise applications integrating voice recognition. The U.S. is the largest market for speech and voice recognition in North America, due to increased digitalization, rapid AI technology adoption across industries, and the presence of major technology companies continuously investing in voice AI capabilities.

The Asia-Pacific speech and voice recognition market is projected to grow at the highest CAGR during the forecast period. The rapid growth of this market is driven by China, India, and Japan’s increased government and enterprise investment in speech and voice recognition technology; the rapidly expanding smart device penetration in emerging Asian markets; the growing demand for speech and voice recognition solutions embedded with latest AI technologies; and the increasing government initiatives supporting digital transformation in healthcare, public services, and financial inclusion.

The global speech and voice recognition market is characterized by the strong presence of established cloud hyperscalers, AI-native speech technology providers, and vertical-focused solution developers actively expanding their capabilities through product innovation, strategic partnerships, and generative AI integration between 2023 and 2026. Leading market players include Microsoft Corporation, Amazon Web Services, and Google LLC, which dominate the enterprise cloud speech ecosystem through scalable AI speech platforms, multilingual automatic speech recognition (ASR), neural text-to-speech (TTS), and LLM-powered conversational AI integration. Apple Inc. and Baidu maintain strong positions in consumer and regional AI ecosystems, while iFLYTEK continues to lead in Mandarin speech recognition and AI-driven voice applications across education, healthcare, and government sectors.

In the enterprise speech analytics and customer engagement domain, IBM Corporation and Verint Systems remain active in delivering AI-powered speech analytics, contact center automation, and industry-specific conversational intelligence solutions. AI-native and specialized speech technology providers such as Speechmatics, AssemblyAI, Sensory Inc., LumenVox, SESTEK, and Dolbey Systems are actively expanding their offerings through enhanced neural ASR models, voice biometrics, edge deployment capabilities, and vertical-focused applications in healthcare, automotive, financial services, and government sectors. These companies continue to compete on model accuracy, multilingual coverage, latency optimization, compliance readiness, and integration flexibility, shaping a highly dynamic and innovation-driven competitive landscape.

Speech and Voice Recognition Market, by Function

Speech and Voice Recognition Market, by Technology

Speech and Voice Recognition Market, by Deployment Mode

Speech and Voice Recognition Market, by End User

Speech and Voice Recognition Market, by Geography

The global speech and voice recognition market was valued at USD 15.45 billion in 2025 and is projected to reach USD 85.35 billion by 2036, growing at a CAGR of 16.8% from 2026 to 2036.

Market growth is driven by increasing adoption of voice biometrics for authentication, expanding integration of voice-enabled systems in automotive and consumer electronics, and the rapid incorporation of generative AI and LLMs into speech platforms. Growing applications in healthcare documentation, contact center automation, and enterprise AI assistants are expected to create significant opportunities for both established players and new entrants.

Key players include Microsoft Corporation, Amazon Web Services, Google LLC, IBM Corporation, Verint Systems, Baidu, Apple Inc., Speechmatics, Sensory Inc., AssemblyAI, iFLYTEK, LumenVox, SESTEK, and Dolbey Systems.

The speech recognition segment is expected to account for the larger market share throughout the forecast period due to widespread ASR and TTS adoption across healthcare, enterprise, and consumer applications.

The artificial intelligence segment is projected to register the highest CAGR, driven by LLM integration, deep learning advancements, and improved natural language processing capabilities.

The cloud-based deployment segment is expected to grow at the highest CAGR, supported by scalability, continuous model upgrades, and API-driven integration.

The consumer electronics segment is projected to register the highest CAGR, driven by the rapid proliferation of smart devices and AI-powered voice assistants.

Published Date: Apr-2023

Published Date: Jan-2023

Published Date: Sep-2022

Published Date: Sep-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates