Resources

About Us

Smart Highway Market Size, Share & Trends Analysis by Solution Type (Intelligent Traffic Management, Smart Tolling), Component (Hardware, Software, Services), Communication Technology, Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

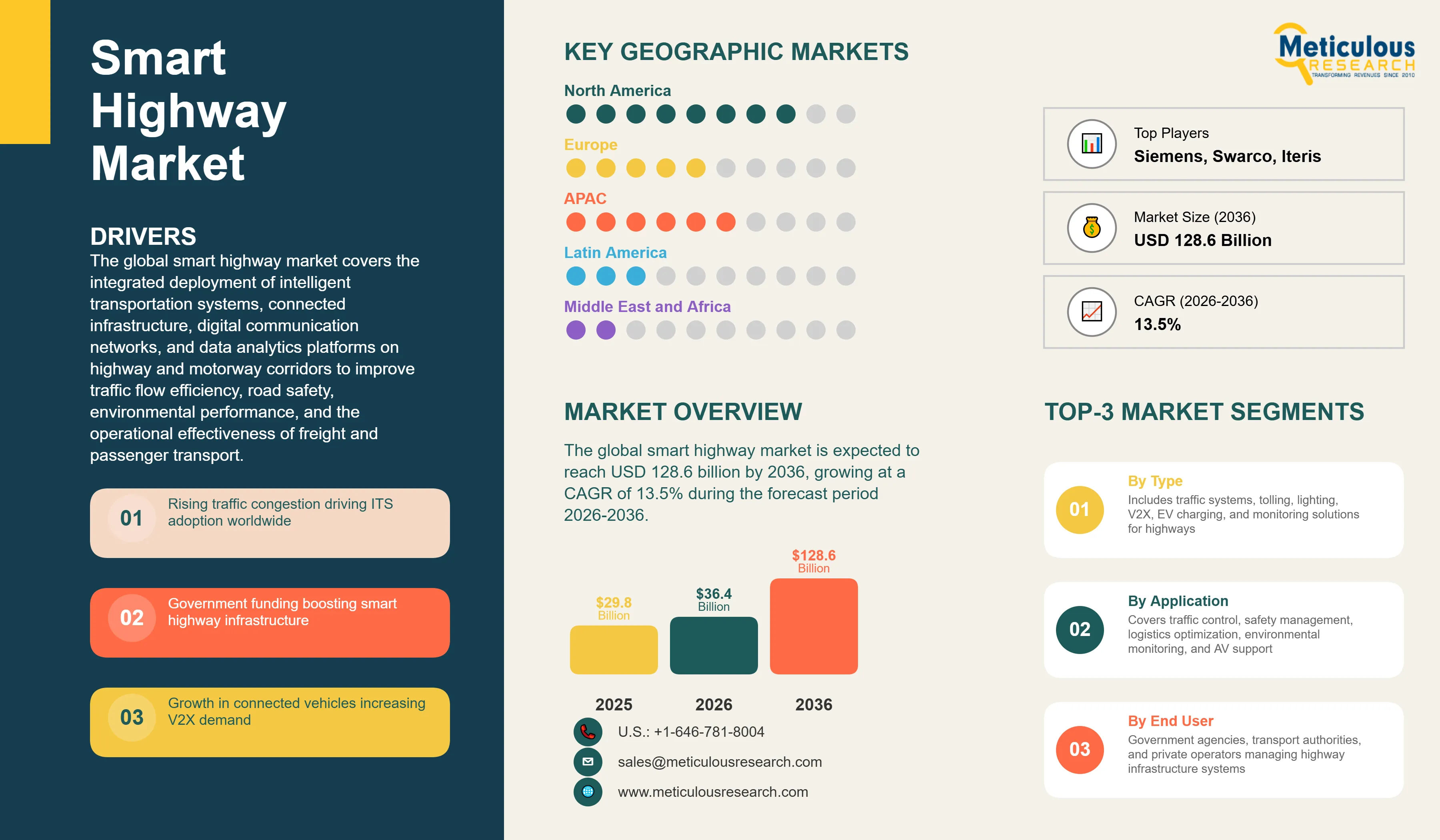

Report ID: MRAUTO - 1041894 Pages: 377 Apr-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global smart highway market was valued at USD 29.8 billion in 2025. This market is expected to reach USD 128.6 billion by 2036 from an estimated USD 36.4 billion in 2026, growing at a CAGR of 13.5% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global smart highway market covers the integrated deployment of intelligent transportation systems, connected infrastructure, digital communication networks, and data analytics platforms on highway and motorway corridors to improve traffic flow efficiency, road safety, environmental performance, and the operational effectiveness of freight and passenger transport. This encompasses intelligent traffic management and adaptive signal control systems, electronic toll collection and dynamic pricing platforms, smart lighting and energy management systems, V2X communication infrastructure supporting vehicle-to-infrastructure and vehicle-to-vehicle connectivity, AI-powered surveillance and incident detection, and the highway EV charging networks increasingly integrated with intelligent energy management systems.

The growth of the global smart highway market is primarily driven by the escalating global urban mobility crisis created by traffic congestion, which costs developed economies an estimated 1 to 3% of GDP annually in productivity losses, fuel waste, and environmental costs, creating compelling economic and social justification for intelligent traffic management investment. The unprecedented wave of government infrastructure investment programs being mobilized across North America, Europe, China, India, and the Gulf states is providing the public funding required to finance the large-scale smart highway deployments that individual transportation authorities previously lacked the capital to execute. These programs include the U.S. IIJA's transportation technology allocations, the EU's Trans-European Transport Network digital infrastructure requirements, and China's national expressway digital transformation initiative that are collectively mobilizing hundreds of billions of dollars in smart highway investment over the forecast period.

Two significant opportunities are shaping the market's long-term trajectory. The commercial deployment of 5G communication networks along highway corridors, combined with the Cellular V2X standard enabling direct vehicle-to-infrastructure communication at the latency levels required for safety-critical applications, represents the transformative connectivity upgrade that unlocks the full performance potential of smart highway infrastructure for connected and autonomous vehicle applications. The integration of EV fast and ultra-fast charging networks into highway infrastructure, enabled by smart energy management systems that optimize charging load relative to grid capacity and renewable energy availability, creates a new and rapidly scaling smart highway solution category whose growth is directly driven by the accelerating global EV adoption wave.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 128.6 Billion |

|

Market Size in 2026 |

USD 36.4 Billion |

|

Market Size in 2025 |

USD 29.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.5% |

|

Dominating Solution Type |

Intelligent Traffic Management Systems |

|

Fastest Growing Solution Type |

EV Charging Infrastructure on Highways |

|

Dominating Component |

Hardware |

|

Fastest Growing Component |

Software |

|

Dominating Communication Technology |

4G/LTE |

|

Fastest Growing Communication Technology |

5G |

|

Dominating Application |

Traffic Management and Control |

|

Fastest Growing Application |

Autonomous Vehicle Support |

|

Dominating Deployment Type |

Urban Highways |

|

Fastest Growing Deployment Type |

Intercity Highways |

|

Dominating End User |

Government and Transport Authorities |

|

Fastest Growing End User |

Private Infrastructure Operators |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Expansion of 5G-Enabled V2X Communication on Highway Corridors

The progressive deployment of 5G network coverage along major highway and motorway corridors is the most transformative technology trend in the smart highway market, enabling the transition from current 4G-based telematics and traffic management applications toward the real-time, ultra-low latency vehicle-to-infrastructure communication architecture that advanced connected and autonomous vehicle operation requires. 5G's sub-10 millisecond latency, high bandwidth capacity, and network slicing capability for safety-critical communication channels create the connectivity performance prerequisites for vehicle-to-infrastructure safety applications including curve speed warning, road hazard notification, intersection movement assist, and connected work zone alerts that reduce traffic accident rates and enable more efficient highway operations. The parallel advancement of the Cellular V2X standard as the preferred V2X communication protocol, supported by 3GPP Release 16 and 17 specifications, is creating a clear technology pathway for V2X deployment on 5G highway infrastructure that is accelerating equipment procurement and deployment planning at highway authorities globally.

The European Union's mandate for 5G connectivity on major Trans-European Transport Network corridors and the U.S. Federal Highway Administration's Connected Vehicle deployment programs are creating regulatory and funding frameworks that are translating the technology opportunity into funded deployment programs. Highway authorities in Germany, the Netherlands, the U.K., Japan, South Korea, and China have all announced or initiated 5G V2X corridor deployment programs that represent near-term procurement opportunities for communication infrastructure providers including Huawei, Ericsson, Nokia, Cisco, and Qualcomm, and for smart highway system integrators that must incorporate 5G V2X capabilities into upgraded ITS architectures.

Integration of EV Charging Infrastructure into Smart Highway Networks

The rapid integration of electric vehicle fast charging and ultra-fast charging infrastructure into the smart highway technology ecosystem represents a new and high-growth solution category that is transforming the scope of smart highway investment well beyond traditional traffic management and safety applications. National EV charging corridor mandates in the United States under the National Electric Vehicle Infrastructure program, the EU's Alternative Fuels Infrastructure Regulation requiring charging stations at maximum 60-kilometer intervals on the Trans-European Transport Network core network by 2025, and China's national highway EV charging network expansion program are collectively driving the deployment of hundreds of thousands of highway charging points across major markets over the forecast period, with each installation increasingly incorporating smart energy management, dynamic load balancing, and integration with highway traffic management systems.

The smart highway dimension of EV charging infrastructure goes beyond simple power delivery to encompass dynamic energy management systems that coordinate charging load across multiple highway charging stations relative to local grid capacity constraints and renewable energy availability, predictive charging demand modeling that anticipates traffic-driven charging load spikes on holiday travel routes, reservation and navigation integration that provides real-time charging availability data to EV drivers through connected vehicle and navigation platforms, and revenue management systems that optimize charging pricing to balance supply and demand across the charging network. These smart energy and digital management capabilities position highway EV charging as a core smart highway technology application rather than a standalone infrastructure category, integrating naturally with the data platforms, communication networks, and control center systems that define modern smart highway architectures.

AI-Powered Traffic Analytics and Predictive Highway Management

The adoption of artificial intelligence and machine learning for highway traffic analytics, predictive incident detection, and adaptive traffic management is progressively transforming smart highway operations from reactive monitoring and response systems toward proactive predictive management platforms that anticipate and prevent congestion events, accidents, and operational disruptions before they occur. AI traffic management systems trained on large historical datasets of traffic flow, incident occurrence, weather conditions, and special event patterns can generate highly accurate short-term traffic state predictions that enable adaptive ramp metering, variable speed limit adjustment, and dynamic lane management interventions timed to prevent congestion formation rather than responding to it after formation.

Computer vision AI applied to existing highway CCTV camera networks is enabling the automated detection of wrong-way drivers, debris on carriageways, stalled vehicles, and accident scenes with detection speed and reliability exceeding human traffic control center operator performance, enabling faster emergency response dispatch and variable message sign activations that reduce secondary accident risk. Highway authorities in Singapore, the Netherlands, Germany, and the United States have deployed AI traffic management pilot programs demonstrating 15 to 30% reductions in incident clearance times and measurable improvements in highway throughput relative to conventional traffic management approaches. The improving performance and falling cost of AI traffic analytics platforms from providers including Iteris, Swarco, Siemens Mobility, and a growing ecosystem of AI infrastructure software startups is making the technology increasingly accessible to transportation authorities beyond the most technically advanced early-adopter markets.

Increasing Traffic Congestion and Need for Intelligent Traffic Management

The worsening global urban and inter-urban traffic congestion crisis is the primary structural demand driver of the smart highway market, as the economic costs of congestion, the safety consequences of unmanaged highway incidents, and the environmental impact of stop-and-go traffic are compelling transportation authorities and governments to invest in intelligent highway management systems as a cost-effective alternative to the prohibitively expensive option of physical highway capacity expansion. The Texas Transportation Institute estimates that U.S. urban congestion costs road users approximately USD 87 billion annually in wasted time and fuel, with the figure rising substantially when freight logistics productivity impacts are included. European Commission studies consistently find that EU road congestion costs EUR 100 billion or more annually, representing approximately 1% of EU GDP. These documented economic costs provide strong quantified justification for government investment in intelligent traffic management systems whose demonstrated ability to increase effective highway throughput by 15 to 35% through adaptive management translates directly into measurable economic benefit that exceeds intelligent infrastructure deployment costs over the system lifecycle.

Government Investments in Smart Infrastructure

The unprecedented scale of government infrastructure investment programs being implemented across major economies is providing the public financing that is translating smart highway technology opportunity into large-scale funded deployment programs. The U.S. Infrastructure Investment and Jobs Act allocates USD 110 billion for roads and bridges with significant provisions for transportation technology including ITS deployment, the NEVI Formula Program providing USD 5 billion for national EV charging corridor infrastructure, and the SMART Grants program providing USD 500 million for innovative surface transportation technology pilots. The EU's Connecting Europe Facility and the EUR 43 billion EU Chips Act are supporting digital transport infrastructure investment across the Trans-European Transport Network. China's 14th Five-Year Plan allocates several trillion renminbi to expressway infrastructure including digital transformation programs for the national highway network. India's Bharatmala highway program is deploying ITS including electronic toll collection, incident management systems, and CCTV surveillance across tens of thousands of kilometers of national highway. These government spending programs are creating very large and funded procurement pipelines that represent the primary near-term market opportunity for smart highway solution providers.

Deployment of 5G and V2X Communication

The commercial rollout of 5G network coverage along major highway corridors and the parallel standardization and deployment of Cellular V2X communication technology represent the most transformative infrastructure upgrade opportunity in the smart highway market over the forecast period. 5G-enabled V2X communication unlocks safety-critical vehicle-to-infrastructure applications including cooperative perception data sharing between vehicles and roadside sensor networks, precision cooperative positioning enabling centimeter-level vehicle location accuracy for autonomous driving support, and real-time road condition broadcasting at the speed and reliability that active safety systems require. Highway authorities that invest in 5G V2X infrastructure upgrades are positioning their road networks for the connected and automated mobility future while generating near-term operational benefits from improved traffic information quality, faster incident detection, and enhanced weather-responsive traffic management capabilities. The large national 5G V2X deployment programs underway in China, Germany, the Netherlands, Japan, and South Korea represent hundreds of millions of dollars in near-term procurement opportunity for communication technology and smart highway system providers qualified to deliver certified C-V2X roadside infrastructure.

Integration with Electric Vehicle Charging Infrastructure

The integration of highway EV fast and ultra-fast charging infrastructure with smart highway digital platforms creates a commercially compelling opportunity that simultaneously addresses the EV range anxiety barrier to electric vehicle mass adoption and expands the smart highway technology addressable market into the rapidly growing EV infrastructure investment category. National highway EV charging networks that incorporate smart energy management, dynamic pricing, predictive load balancing, and real-time availability data integration with navigation and traffic management platforms represent a more valuable and differentiated infrastructure asset than simple charging stations, enabling highway authorities and private infrastructure operators to monetize highway charging through dynamic pricing models, reservation services, and premium charging products that generate revenue streams beyond conventional toll-based highway finance models. The NEVI program in the U.S., the AFIR regulation in Europe, and equivalent national programs in China and Japan are providing the funding frameworks and mandated deployment timelines that create defined procurement schedules for smart charging infrastructure along major highway networks.

By Solution Type: In 2026, Intelligent Traffic Management Systems to Dominate

Based on solution type, the global smart highway market is segmented into intelligent traffic management systems, smart tolling systems, smart lighting systems, highway communication systems, surveillance and monitoring systems, EV charging infrastructure on highways, and other smart highway solutions. In 2026, the intelligent traffic management systems segment is expected to account for the largest share of the global smart highway market. The large share of this segment is attributed to traffic monitoring, adaptive control, and incident detection systems representing the foundational and most universally deployed smart highway solution, with established procurement programs across transportation departments in North America, Europe, and Asia-Pacific generating the highest aggregate annual investment of any smart highway solution category. The segment encompasses traffic monitoring sensors and cameras, adaptive signal control and ramp metering systems, incident detection and automated response platforms, and the variable message signage networks that communicate real-time traffic information to highway users across the world's major highway networks.

However, the EV charging infrastructure on highways segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the massive national highway EV charging network deployment programs being financed through the U.S. NEVI program, the EU's AFIR regulation, and China's national EV charging expansion initiative, the accelerating growth of the global electric vehicle fleet creating rapidly expanding EV charging demand on intercity highway corridors, and the increasing integration of smart energy management and digital service capabilities into highway charging installations that positions EV charging as a core smart highway technology application.

By Component: In 2026, Hardware to Hold the Largest Share

Based on component, the global smart highway market is segmented into hardware, software, and services. In 2026, the hardware segment is expected to account for the largest share of the global smart highway market. This dominance reflects the capital-intensive nature of smart highway physical infrastructure deployment, where sensors, cameras, roadside controllers, communication gateways, variable message signs, and EV charging equipment constitute the majority of smart highway project capital expenditure and generate the highest aggregate revenue within the component landscape. The ongoing expansion of national highway sensor and camera networks, 5G V2X roadside unit deployments, and highway charging infrastructure represents sustained and growing hardware procurement demand from transportation authorities and private highway operators globally.

However, the software segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapid adoption of AI-powered traffic management software platforms, cloud-based data analytics systems, integrated highway operating software suites, and smart highway digital twin platforms that unlock the operational intelligence value of deployed physical infrastructure. The software segment benefits from high recurring revenue characteristics through annual software licensing, maintenance contracts, and cloud platform subscriptions that generate predictable revenue growth as the installed base of software-managed smart highway infrastructure expands.

By Communication Technology: In 2026, 4G/LTE to Hold the Largest Share

Based on communication technology, the global smart highway market is segmented into dedicated short-range communication, Cellular V2X, 4G/LTE, and 5G. In 2026, the 4G/LTE segment is expected to account for the largest share of the global smart highway market, reflecting the broad current deployment of 4G cellular networks for ITS applications including traffic monitoring data backhaul, vehicle telematics, fleet management communication, and existing connected vehicle services that are built on the 4G network infrastructure already comprehensively deployed along major highway corridors in developed markets.

However, the 5G segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating deployment of 5G network coverage along major highway corridors in conjunction with national broadband infrastructure expansion programs, the transition of V2X communication from DSRC to the 5G-based Cellular V2X standard in most major markets, and the requirement for 5G network availability to enable the latency-critical safety applications and autonomous vehicle support capabilities that represent the high-value frontier of smart highway technology development.

By Application: In 2026, Traffic Management and Control to Hold the Largest Share

Based on application, the global smart highway market is segmented into traffic management and control, road safety and incident management, freight and logistics optimization, environmental monitoring, and autonomous vehicle support. In 2026, the traffic management and control segment is expected to account for the largest share of the global smart highway market. This dominance reflects traffic management's position as the primary operational mandate of highway authorities globally, the universality of traffic management system deployment across all levels of highway network development, and the well-established procurement frameworks, technology standards, and performance measurement methodologies that have made intelligent traffic management the most commercially mature and broadly adopted smart highway application category worldwide.

However, the autonomous vehicle support segment is projected to register the highest CAGR during the forecast period. This growth is driven by the progressive commercialization of autonomous truck and passenger vehicle technology creating growing demand for the highway infrastructure upgrades required to support AV operations, including high-definition digital map maintenance, roadside sensor fusion infrastructure, V2X communication networks, and dedicated AV testing and operational corridors that are being developed on major highway routes in the United States, Europe, China, and Japan.

By Deployment Type: In 2026, Urban Highways to Hold the Largest Share

Based on deployment type, the global smart highway market is segmented into urban highways, intercity highways, and expressways. In 2026, the urban highways segment is expected to account for the largest share of the global smart highway market. Urban highways represent the highest-priority smart highway deployment environment, as the combination of the highest traffic volumes, the greatest congestion severity, the most complex operational environment requiring continuous intelligent management, and the proximity to population centers generating the strongest public demand for safety and mobility improvement creates the most compelling case for smart highway investment. Urban highway ITS deployments in major metropolitan areas including Los Angeles, New York, London, Tokyo, Beijing, Shanghai, and Singapore represent the largest individual procurement programs in the smart highway market and generate the highest solution complexity and system integration requirements that command premium contract values.

However, the intercity highways segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapid expansion of ITS deployment from urban highway networks onto national intercity and expressway corridors as governments extend smart highway investment beyond initial urban focus areas, the critical role of intercity highway corridors in national EV charging network deployment programs, and the strategic importance of intercity highway V2X communication infrastructure for enabling the long-distance autonomous truck operations that represent the most commercially valuable near-term autonomous vehicle application.

By End User: In 2026, Government and Transport Authorities to Hold the Largest Share

Based on end user, the global smart highway market is segmented into government and transport authorities, private infrastructure operators, and logistics and fleet operators. In 2026, the government and transport authorities segment is expected to account for the largest share of the global smart highway market. National highway agencies, state and provincial transportation departments, and municipal transport authorities represent the primary procurers of smart highway infrastructure globally, as the majority of the world's highway network remains under public ownership and the primary capital expenditure for ITS deployment is financed through government transportation budgets and infrastructure bonds. Federal Highway Administration programs in the United States, Highways England's ITS investment program, Germany's Digitales Testfeld Autobahn initiatives, and the National Highways Authority of India's ITS deployment under Bharatmala collectively represent the dominant procurement channel for smart highway solutions globally.

However, the private infrastructure operators segment is projected to register the highest CAGR during the forecast period. The expansion of public-private partnership models for highway concessions and the growing wave of infrastructure privatization and long-term lease arrangements transferring highway management to private operators are creating a rapidly growing private sector smart highway customer base. Private concessionaires including Ferrovial, Transurban, Atlantia, Abertis, and VINCI have strong financial incentives to invest in smart highway technology upgrades that reduce operating costs, increase toll revenue through dynamic pricing, and create new revenue streams from data services and EV charging that improve the financial returns on long-term highway concession investments.

Smart Highway Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global smart highway market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global smart highway market. The largest share of this region is mainly due to the substantial and immediate funding provided by the U.S. Infrastructure Investment and Jobs Act for transportation technology, ITS deployment, EV charging corridor infrastructure, and connected vehicle pilot programs that is translating into the world's largest single-country smart highway procurement wave, the established and technologically advanced ITS infrastructure base across the U.S. interstate highway system and Canadian national highway network that provides the foundation for technology upgrade investments, and the strong presence of leading smart highway technology vendors including Siemens, Cisco, IBM, Intel, Iteris, and Cubic Corporation that provide deep technical solutions and established customer relationships with state and federal transportation agencies. The NEVI program's USD 5 billion investment in national EV charging infrastructure along designated alternative fuel corridors represents the largest single smart highway infrastructure program globally and is positioning North America as the most active EV charging smart highway deployment market in the near term.

However, the Asia-Pacific smart highway market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by China's national expressway digital transformation program that is deploying ITS, smart lighting, V2X communication, and automated toll collection across the world's largest national expressway network of over 177,000 kilometers, India's Bharatmala highway program deploying ITS and electronic toll collection across 34,800 kilometers of national highway corridors with substantial additional network expansion planned through the decade, and the advanced smart highway programs of Japan, South Korea, and Singapore that are serving as technology demonstration environments for 5G V2X, cooperative intelligent transport systems, and autonomous vehicle corridor deployment. Huawei's Intelligent Road solution, Siemens Mobility's ITS portfolio, and domestic Chinese ITS vendors including China Communications Services Corporation and CITIC Construction are competing actively across the region's large procurement programs.

Europe represents the second-largest and most technically advanced smart highway market globally, anchored by the EU's TEN-T digital corridor requirements, Germany's A9 Digital Motorway Test Bed serving as a continental showcase for cooperative ITS and V2X deployment, the Netherlands' Advanced Motorway Traffic Management system recognized as among the world's most sophisticated operational highway management systems, and the progressive deployment of 5G network coverage along major European motorway corridors under national broadband programs. The Middle East and Africa region is experiencing accelerating smart highway investment, led by Saudi Arabia's NEOM smart mobility programs and the UAE's Abu Dhabi and Dubai smart highway initiatives, where ambitious national transformation programs are creating procurement opportunities for comprehensive smart highway deployments that leapfrog incremental upgrade approaches to implement state-of-the-art integrated smart highway systems.

The global smart highway market is moderately fragmented across a diverse ecosystem of large integrated technology and infrastructure companies, specialist ITS vendors, and communications and data analytics providers, with competition focused on system integration capability, breadth of ITS solution portfolio, established transportation authority customer relationships, compliance with national and international ITS standards, and the ability to deliver comprehensive multi-technology smart highway programs at large scale.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, geographic presence, and key strategic developments. Some of the key players operating in the global smart highway market include Siemens AG (Germany), Cisco Systems Inc. (U.S.), Huawei Technologies Co. Ltd. (China), Kapsch TrafficCom AG (Austria), Thales Group (France), Schneider Electric SE (France), IBM Corporation (U.S.), Intel Corporation (U.S.), Cubic Corporation (U.S.), Swarco AG (Austria), Iteris Inc. (U.S.), Indra Sistemas S.A. (Spain), Hitachi Ltd. (Japan), NEC Corporation (Japan), and Q-Free ASA (Norway), among others.

The global smart highway market is expected to reach USD 128.6 billion by 2036 from an estimated USD 36.4 billion in 2026, at a CAGR of 13.5% during the forecast period 2026-2036.

In 2026, the intelligent traffic management systems segment is expected to hold the largest share of the global smart highway market, driven by traffic monitoring, adaptive control, and incident detection systems representing the most universally deployed smart highway solution with established procurement programs across transportation authorities globally.

The EV charging infrastructure on highways segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by national highway EV charging network deployment mandates in the U.S., EU, and China and the accelerating growth of the global electric vehicle fleet creating rapidly expanding EV charging demand on intercity highway corridors.

In 2026, the 4G/LTE segment is expected to hold the largest share of the global smart highway market, reflecting the broad current deployment of 4G cellular networks for ITS applications across existing smart highway installations globally.

In 2026, the traffic management and control segment is expected to hold the largest share of the global smart highway market, reflecting traffic management's position as the primary operational mandate of highway authorities and the most commercially mature smart highway application category worldwide.

The growth of this market is primarily driven by the escalating economic and social costs of traffic congestion compelling transportation authorities to invest in intelligent highway management systems, the unprecedented scale of government infrastructure investment programs across North America, Europe, and Asia-Pacific providing the public funding for large-scale smart highway deployments, and the rapid commercialization of connected and autonomous vehicle technology creating strong demand for the V2X communication and smart infrastructure upgrades required to support next-generation mobility on highway networks.

Key players are Siemens AG (Germany), Cisco Systems Inc. (U.S.), Huawei Technologies Co. Ltd. (China), Kapsch TrafficCom AG (Austria), Thales Group (France), Schneider Electric SE (France), IBM Corporation (U.S.), Intel Corporation (U.S.), Cubic Corporation (U.S.), Swarco AG (Austria), Iteris Inc. (U.S.), Indra Sistemas S.A. (Spain), Hitachi Ltd. (Japan), NEC Corporation (Japan), and Q-Free ASA (Norway), among others.

Asia-Pacific is expected to register the highest growth rate in the global smart highway market during the forecast period 2026-2036, driven by China's national expressway digital transformation program, India's Bharatmala ITS deployment, and the advanced 5G V2X and autonomous vehicle corridor programs of Japan, South Korea, and Singapore.

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates