Resources

About Us

Electromagnetic Brakes Market Size, Share & Trends Analysis, by Product Type, Coil Type, End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

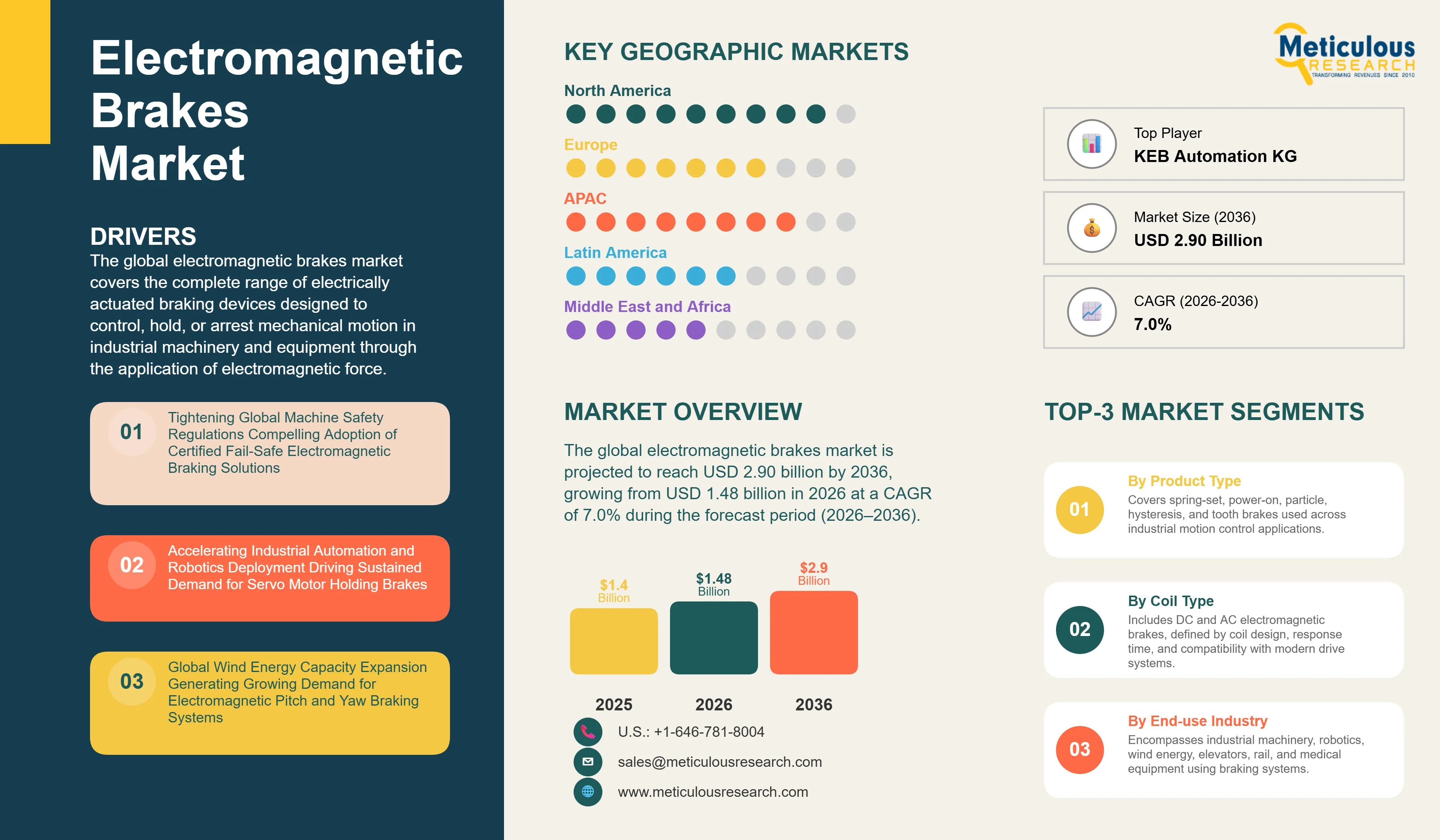

Report ID: MRAUTO - 1041958 Pages: 283 May-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global electromagnetic brakes market was valued at USD 1.40 billion in 2025. The market is projected to reach USD 2.90 billion by 2036, growing from USD 1.48 billion in 2026 at a CAGR of 7.0% during the forecast period (2026–2036).

• The global electromagnetic brakes market is projected to reach USD 2.90 billion by 2036.

• The market is expected to grow at a CAGR of 7.0% during the forecast period 2026–2036.

• The total electromagnetic brakes industry was valued at USD 1.40 billion in 2025 and is estimated to reach USD 1.48 billion in 2026.

• North America is expected to dominate this market with the largest revenue share in 2026, driven by the broad installed base of servo-driven industrial machinery, elevator and escalator systems, and crane and hoist equipment requiring certified fail-safe electromagnetic braking solutions, the active enforcement of OSHA machine safety standards and ASME elevator codes, and the strong presence of leading electromagnetic brake manufacturers and their established OEM supply relationships with major industrial machinery, robot, and motor manufacturers operating across the region.

• Asia Pacific is projected to witness the fastest revenue growth during the forecast period, driven by the rapid expansion of manufacturing automation across China, Japan, South Korea, India, and Southeast Asia, the accelerating adoption of servo-driven machinery and industrial robots across the electronics, automotive, and consumer goods manufacturing sectors, and the large-scale buildout of wind energy infrastructure requiring electromagnetic pitch and yaw braking systems as standard turbine components.

• By product type, the spring-set (power-off) electromagnetic brakes segment is expected to hold the largest share of the market in 2026, driven by its fundamental role as the fail-safe braking standard across elevator, crane, servo motor, and automated manufacturing applications where a loss of electrical power must trigger automatic, positive brake engagement without any active control intervention.

• By product type, the electromagnetic hysteresis brakes segment is projected to register the highest growth during the forecast period, driven by its growing adoption in precision tension control systems, collaborative robot joint braking, and servo axis holding applications that require smooth, frictionless, and electrically controllable torque delivery without the wear or replacement cycles associated with friction-based electromagnetic brake designs.

• By coil type, the DC electromagnetic brakes segment is expected to account for the largest share of the market in 2026, reflecting the near-universal adoption of DC coil designs across modern servo motor platforms, inverter-driven industrial machinery, and battery-powered mobile robotic systems where precise coil response timing and compatibility with digital safety controller architectures are required.

• By coil type, the DC electromagnetic brakes segment is also projected to register the highest growth during the forecast period, driven by the ongoing global modernization of industrial machinery away from legacy AC-driven platforms toward inverter-controlled and servo-driven equipment architectures, which expand the addressable market for DC electromagnetic brakes across new installations and equipment upgrade projects simultaneously.

• By end-use industry, the industrial machinery and automation segment is expected to account for the largest share in 2026, while the robotics and collaborative robots segment is projected to register the highest CAGR during the forecast period.

• By geography, North America is expected to dominate the market in 2026, while Asia Pacific is expected to witness the fastest growth during the forecast period.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global electromagnetic brakes market covers the complete range of electrically actuated braking devices designed to control, hold, or arrest mechanical motion in industrial machinery and equipment through the application of electromagnetic force. The market includes spring-set (power-off) brakes, power-on electromagnetic brakes, electromagnetic particle brakes, hysteresis brakes, and tooth (jaw) brakes, deployed across a wide spectrum of end-use industries including industrial machinery and automation, elevator and escalator systems, crane and hoist equipment, wind energy, packaging and printing machinery, railway and mass transit, robotics and collaborative robots, and medical equipment. These braking devices are manufactured and sold as either motor-integrated assemblies built directly onto the non-drive end of electric motors during the manufacturing process, or as standalone shaft-mounted and flange-mounted units integrated into machine drive trains at the machine builder or end-user level.

These components are fundamental to safe machine operation in applications where a controlled, reliable braking response is required under both normal operating conditions and emergency power-interruption scenarios. Spring-set electromagnetic brakes, which represent the dominant product category by revenue, engage automatically when electrical power is removed, making them the industry-standard fail-safe braking solution for elevators, hoists, servo-driven robot axes, CNC machine tool spindle and feed drives, and automated guided vehicles. The performance requirements governing electromagnetic brake behavior in safety-critical applications are defined by standards including EN 13135 for crane and lifting equipment, EN 81-20 and EN 81-50 for elevator safety, and IEC 61800-5-2 governing the functional safety of power drive systems, all of which specify brake engagement time, holding torque retention, and thermal performance parameters that directly influence product design and procurement decisions for original equipment manufacturer (OEM) machine builders globally.

The growth of the global electromagnetic brakes market is primarily driven by the accelerating adoption of industrial automation and servo motor-driven machinery across manufacturing, logistics, and energy sectors. According to the International Federation of Robotics (IFR) World Robotics 2023 report, global industrial robot installations reached a record 553,052 units in 2022, and the global installed operational base of industrial robots exceeded 3.9 million units by the end of the same year. Each servo-driven robot axis typically incorporates a spring-set electromagnetic brake for holding position during power-off and emergency stop conditions, directly linking the expanding robotics installed base to sustained demand growth for electromagnetic braking components. The increasing adoption of collaborative robots and autonomous mobile robots in factory and warehouse environments is further reinforcing this demand, as these systems require compact, low-inertia electromagnetic brakes capable of rapid, precisely controlled engagement within confined operating spaces and in proximity to human operators.

In addition to industrial automation, the global expansion of wind energy infrastructure is creating a growing and structurally significant demand segment for electromagnetic brakes. Wind turbines incorporate electromagnetic braking systems in pitch control mechanisms, where individual rotor blades are positioned to manage aerodynamic loading, and in yaw drive systems, where the nacelle is oriented toward prevailing wind direction. According to the Global Wind Energy Council's Global Wind Report 2024, global wind power capacity additions reached 117 gigawatts in 2023, the highest annual installation figure ever recorded at the time, bringing cumulative global installed capacity to 1,017 gigawatts. Each utility-scale wind turbine typically incorporates three independent pitch brake systems and one or more yaw brake assemblies, creating a durable per-unit demand for electromagnetic braking components that scales directly with annual turbine installation volumes.

Despite strong structural demand drivers, the electromagnetic brakes market faces challenges related to the increasing integration complexity of safety-certified electromagnetic brakes in modern servo and robotic systems, where space constraints, thermal management requirements, and the need for compatibility with functional safety control architectures require application-specific engineering iterations that extend product development cycles for OEM customers. The growing performance expectations associated with collaborative robot and cobot braking, including consistent engagement timing, low backlash, and stable holding torque retention across high-cycle operational profiles, are also pushing the performance boundaries of conventional electromagnetic brake technology and creating engineering challenges for manufacturers developing next-generation brake solutions for these applications.

The convergence of stricter machine safety regulation, expanding industrial automation investment, and accelerating wind energy development is creating significant growth opportunities for electromagnetic brake manufacturers capable of delivering application-engineered solutions that combine high torque density, compact form factors, functional safety certification to IEC 62061 and ISO 13849 standards, and digital monitoring integration for predictive maintenance platforms. The growing adoption of electromagnetic brakes in medical equipment, including surgical robotics, diagnostic imaging gantries, and patient lifting systems, represents an emerging high-value segment that rewards manufacturers with validated safety certification credentials and a track record in high-reliability motion control component supply.

|

Parameters

|

Details

|

|

Market Size by 2036

|

USD 2.90 Billion

|

|

Market Size in 2026

|

USD1.48 Billion

|

|

Market Size in 2025

|

USD 1.40 Billion

|

|

Revenue Growth Rate (2026–2036)

|

CAGR of 7.0%

|

|

Dominating Product Type

|

Spring-set (Power-off) Electromagnetic Brakes

|

|

Fastest Growing Product Type

|

Electromagnetic Hysteresis Brakes

|

|

Dominating Coil Type

|

DC Electromagnetic Brakes

|

|

Fastest Growing Coil Type

|

DC Electromagnetic Brakes

|

|

Dominating End-use Industry

|

Industrial Machinery & Automation

|

|

Fastest Growing End-use Industry

|

Robotics & Collaborative Robots

|

|

Dominating Geography

|

North America

|

|

Fastest Growing Geography

|

Asia Pacific

|

|

Base Year

|

2025

|

|

Forecast Period

|

2026 to 2036

|

EU Machinery Regulation and Evolving Global Machine Safety Standards Mandating Fail-Safe Electromagnetic Braking Solutions Across Industrial Machinery Applications

The adoption of EU Machinery Regulation (EU) 2023/1230 set to apply in 2027 and replacing the long-standing Machinery Directive 2006/42/EC symbolise the most significant regulatory shift in the European industrial machinery sector’s global electromagnetic brakes market in over a decade. Unlike its predecessor, the new regulation establishes explicit safety requirements for collaborative robots, autonomous machinery, and self-propelled equipment areas where spring-set electromagnetic fail-safe brakes are widely used to meet safety standards. It requires machinery operating alongside human workers to include control systems and mechanical safety components, such as braking mechanisms, that achieve functional safety levels defined by ISO 13849 and IEC 62061. These standards outline Performance Level (PL) and Safety Integrity Level (SIL) criteria for safety-related control functions, including motor braking. As a result, there is a clear shift in procurement toward electromagnetic brake systems with third-party functional safety certifications, strengthening the market position of manufacturers offering certified products while placing suppliers of non-certified, commodity components at a competitive disadvantage.

In the United States, OSHA’s machine guarding requirements under 29 CFR 1910 Subpart O together with standards such as ANSI/RIA R15.06 for industrial robots and ANSI/ITSDF B56.5 for automated guided vehicles, likewise mandate that powered industrial equipment include braking systems capable of securely holding loads and stopping motion in the event of a fault. Growing liability risks for machine builders and facility operators stemming from inadequate safety design are further driving the specification of certified electromagnetic brakes in new equipment across North America. This trend is especially evident as robot and automation system integrators face increased scrutiny of component-level safety compliance during customer acceptance processes. At the same time, the global adoption of IEC 61800-5-2 as a benchmark for power drive system design is encouraging the integration of SIL-rated electromagnetic brakes into servo drives and motor assemblies across industrial markets worldwide.

Manufacturers including Kendrion N.V., Mayr GmbH & Co. KG, and KEB Automation KG have responded to this regulatory and commercial demand by developing and certifying spring-set electromagnetic brake product lines rated to IEC 62061 SIL 2 and ISO 13849 PLe, the highest categories typically required in industrial machinery safety applications. These manufacturers are increasingly positioned as preferred suppliers for major machine builders, robot manufacturers, and motor OEMs who require documented brake safety performance as part of their machinery safety dossiers. The certification of electromagnetic brakes as safety components is effectively raising the barrier to entry for new competitors in the premium industrial brake segment and reinforcing the competitive advantages of established manufacturers with the engineering resources and testing infrastructure to support the certification process.

Global Wind Energy Capacity Expansion Creating Sustained Demand for High-Performance Electromagnetic Pitch and Yaw Braking Systems

The sustained global expansion of wind energy infrastructure represents one of the most clearly defined structural growth drivers for the electromagnetic brakes market over the forecast period. Wind turbines rely on electromagnetic braking systems in two critical mechanical functions: pitch braking, where spring-set electromagnetic brakes hold individual rotor blades in position during grid connection events, wind turbulence, and emergency shutdown sequences; and yaw braking, where electromagnetic brakes hold the nacelle in a fixed azimuth orientation during power generation and apply controlled resistance during nacelle rotation to prevent drivetrain fatigue from rapid yaw oscillation. Each utility-scale wind turbine typically incorporates three independent pitch brake systems, one per blade, and one or more yaw brake assemblies, creating a meaningful and predictable per-unit electromagnetic brake demand that scales directly with annual turbine installation volumes globally.

According to the Global Wind Energy Council's Global Wind Report 2024, cumulative global installed wind capacity reached 1,017 gigawatts by the end of 2023, with annual capacity additions of 117 gigawatts in 2023 representing the highest single-year installation volume ever recorded at the time. The International Energy Agency’s Renewables 2024 report further highlights that wind power is on course to become the world’s largest source of electricity generation by 2030. This trajectory points to a strong and sustained pipeline of turbine installations, which in turn will drive demand for electromagnetic pitch and yaw braking systems as integral components of wind turbines. At the same time, the rapid expansion of offshore wind projects in regions such as the North Sea, coastal China and South Korea, and the U.S. East Coast is increasing the need for more advanced electromagnetic braking solutions. These systems must be designed to withstand harsh marine conditions, support larger turbines with capacities exceeding 12 megawatts, and operate with extended maintenance intervals of up to five years key requirements for offshore wind operations.

The ongoing transition toward direct-drive and medium-speed wind turbine drivetrains is also reshaping electromagnetic brake design requirements, as larger-diameter, lower-speed generator shafts in direct-drive architectures require higher-torque electromagnetic brake assemblies than those used in conventional high-speed geared turbine designs. This is prompting major turbine OEMs to work closely with electromagnetic brake manufacturers on application-specific designs that accommodate the mechanical constraints of direct-drive configurations while satisfying the reliability and certification requirements of offshore turbine qualification programs. Electromagnetic brake suppliers with established wind energy application expertise, including Kendrion N.V. and Regal Rexnord Corporation, are increasingly engaged as strategic component development partners by major turbine manufacturers rather than as interchangeable commodity suppliers, reflecting the growing technical and commercial significance of reliable electromagnetic braking performance in the global wind turbine supply chain.

Industrial Robotics and Collaborative Robot Proliferation Expanding the Addressable Market for Compact, Safety-Certified Electromagnetic Holding Brakes

The rapid expansion of industrial robots, collaborative robots, and autonomous mobile robots across manufacturing and logistics is creating a significant, high-volume demand for compact electromagnetic holding brakes. These applications require brakes with low inertia, fast engagement, and stable torque retention to support the performance of multi-axis servo systems. The International Federation of Robotics World Robotics 2023 report notes that the global operational stock of industrial robots surpassed 3.9 million units by the end of 2022, with annual installations reaching a record 553,052 units that year. Typically, each multi-axis robot arm is equipped with electromagnetic brakes on most or all servo-driven joints as standard components for safety and position holding, meaning a six-axis robot may use up to six separate brake units. As robot adoption continues to accelerate and the installed base expands, the cumulative demand for electromagnetic brakes as essential joint components is set to grow accordingly. This positions brake manufacturers integrated into industrial robot OEM supply chains to benefit from a stable and expanding revenue stream.

The growth of collaborative robots is particularly significant for the electromagnetic brakes market. Cobots are designed to operate without traditional safety enclosures in direct proximity to human workers, which requires their joint braking systems to deliver high reliability and very short engagement times to ensure operator safety in response to emergency stop commands. This functional safety requirement creates a strong procurement preference for spring-set electromagnetic brakes certified to ISO 13849 PLe and IEC 62061 SIL 2, specifications that carry a meaningful technical differentiation and price premium relative to uncertified alternatives and that effectively exclude commodity brake suppliers from the cobot OEM supply chain. The global cobot market has grown from an emerging product category into a commercially established segment, with the IFR estimating that cobots represented approximately 10% of total new robot installations globally in recent years, a share that is expected to grow further as unit costs decline and deployment simplicity improves across an expanding range of manufacturing and assembly applications.

The rise of autonomous mobile robots and automated guided vehicles as standard components of modern warehouse and fulfillment center operations is creating an additional and rapidly expanding demand segment for small-format, low-voltage electromagnetic brakes used as wheel drive holding brakes in mobile robotic platforms. These applications require electromagnetic brakes with fast engagement times, compatibility with 24V DC power architectures common in mobile robotic systems, and compact envelope dimensions that allow integration within the constrained wheel drive assemblies of AMR platforms. Leading electromagnetic brake manufacturers including Kendrion N.V., Ogura Industrial Corp., and KEB Automation KG have responded to this market development by introducing dedicated AMR and cobot brake product lines, reflecting the commercial importance of robotics-driven demand in the overall electromagnetic brakes market growth trajectory.

By Product Type: In 2026, the Spring-set (Power-off) Electromagnetic Brakes Segment to Dominate the Global Electromagnetic Brakes Market

Based on product type, the electromagnetic brakes industry is segmented into spring-set (power-off) electromagnetic brakes, power-on electromagnetic brakes, electromagnetic particle brakes, electromagnetic hysteresis brakes, and electromagnetic tooth (jaw) brakes. In 2026, the spring-set (power-off) electromagnetic brakes segment is expected to account for the largest share of this market. The growth of this segment is attributable to the fundamental and non-substitutable role that spring-set electromagnetic brakes serve across the broadest range of industrial safety braking applications, including elevator and escalator drive systems, crane and hoist lifting equipment, servo motor drives integrated into industrial robots and CNC machine tools, and conveying and material handling systems operating under the machine safety requirements of major global industrial markets. The defining characteristic of spring-set electromagnetic brakes is that they engage positively in the absence of electrical power, providing an inherent fail-safe function required by safety standards governing powered machinery across all major industrial markets globally. Manufacturers including Mayr GmbH & Co. KG through its ROBA-stop product series, Kendrion N.V., and KEB Automation KG have developed extensive spring-set brake portfolios covering torque ranges from below 1 Nm in miniature servo motor applications to several thousand Nm in heavy-duty crane and industrial hoist installations, sustaining the segment's commercial dominance across a wide range of end-use applications.

However, the electromagnetic hysteresis brakes segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the expanding deployment of precision tension control systems in packaging, film converting, wire drawing, and textile manufacturing applications, where the smooth, frictionless, and electrically controllable torque characteristics of hysteresis brakes deliver a level of tension regulation accuracy that is unattainable with friction-based electromagnetic brake alternatives. The growing adoption of hysteresis brakes in collaborative robot joint holding and precision servo axis applications, where the absence of mechanical contact wear components extends service life and eliminates the periodic friction disc inspection and replacement cycles inherent to conventional electromagnetic brake designs, is reinforcing segment growth. Manufacturers including Kendrion N.V., Miki Pulley Co., Ltd., and Ogura Industrial Corp. are expanding their hysteresis brake product portfolios with miniaturized designs targeting the precision servo and robotic joint braking markets.

By Coil Type: In 2026, the DC Electromagnetic Brakes Segment to Hold the Largest Share

Based on coil type, the electromagnetic brakes industry is segmented into DC electromagnetic brakes and AC electromagnetic brakes. In 2026, the DC electromagnetic brakes segment is expected to account for the largest share of this market by a substantial margin, reflecting the near-universal specification of DC coil designs across modern servo motor platforms, inverter-driven industrial machinery, and battery-powered mobile robotic systems. DC electromagnetic brakes offer faster coil response times, more precise engagement and release timing, and better compatibility with modern digital safety controller and drive architectures compared to AC designs, making them the standard specification for newly designed motion control systems across virtually all industrial sectors. The prevalent availability of compact AC-to-DC rectifier accessories as standard offerings from leading electromagnetic brake manufacturers has further reduced the installation complexity of DC brakes in facilities with AC power distribution infrastructure, effectively eliminating the last practical barrier to DC brake adoption even in environments where three-phase AC power is the primary supply format.

The DC electromagnetic brakes segment is also projected to register the highest growth rate during the forecast period. This growth is driven by the ongoing global modernization of industrial machinery away from legacy AC-driven platforms toward inverter-controlled and servo-driven equipment architectures, which require DC-compatible electromagnetic brake assemblies as standard components. As industrial operators in Asia Pacific, Latin America, and the Middle East expand and upgrade their manufacturing infrastructure with modern servo and variable frequency drive equipped machinery, the adoption of DC electromagnetic brakes across these markets is growing in parallel with the broader modernization of the regional industrial equipment base. The AC electromagnetic brakes segment retains a residual presence in legacy crane, hoist, and industrial conveying installations, but new equipment procurement is almost exclusively directed toward DC brake designs, and the aftermarket replacement of AC brake assemblies in equipment undergoing drive system upgrades represents an additional source of DC electromagnetic brake demand growth throughout the forecast period.

By End-use Industry: In 2026, the Industrial Machinery & Automation Segment to Hold the Largest Share

Based on end-use industry, the electromagnetic brakes industry is segmented into industrial machinery and automation, elevator and escalator, wind energy, crane and hoist equipment, packaging and printing machinery, robotics and collaborative robots, railway and mass transit, medical equipment, and other end-use industries. In 2026, the industrial machinery and automation segment is expected to account for the largest share of this market. The growth is driven by the pervasive requirement for electromagnetic braking across the full spectrum of servo-driven and motor-equipped machinery deployed in manufacturing environments, including CNC machining centers, conveying and sorting systems, palletizing and depalletizing equipment, textile machinery, and automated assembly systems, all of which incorporate electromagnetic holding brakes as standard safety and positioning components. The continuous expansion of global manufacturing capacity driven by reshoring activity in North America and Europe, the buildout of semiconductor and electronics manufacturing infrastructure across Asia Pacific, and the broad automation of previously manual production processes in food processing, consumer goods, and logistics sectors sustains broad-based demand for electromagnetic brakes as essential motor and drive system components across this end-use segment.

However, the robotics and collaborative robots segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the compounding effect of accelerating robot installation rates globally, the growing per-robot electromagnetic brake content as multi-axis cobot and autonomous mobile robot platforms become the dominant growth categories within the broader robotics market, and the technical differentiation of electromagnetic brake requirements for collaborative robot applications that creates a premium-priced procurement category distinct from conventional industrial automation brake supply. The increasing deployment of robotic automation in electronics assembly, life sciences and pharmaceutical manufacturing, food processing, and logistics fulfillment is continuously expanding the total installed base of robotic systems and, by extension, the addressable market for electromagnetic brakes as both OEM components in new robot builds and as aftermarket replacement parts in the growing global robot installed base.

Based on geography, the overall electromagnetic brakes market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This position is supported by the region's extensive installed base of servo-driven industrial machinery and elevator and escalator systems requiring fail-safe electromagnetic braking compliant with ASME A17.1 (Safety Code for Elevators and Escalators) and ASME A17.3 standards, the active enforcement of OSHA machine guarding requirements and ANSI/RIA robotics safety standards that drive certified electromagnetic brake procurement across the region's broad manufacturing and logistics sectors, and the strong design-in relationships between leading North American and European electromagnetic brake manufacturers and the major industrial robot OEMs, motor manufacturers, and machine builders operating in the United States and Canada. The United States represents a large and recurring aftermarket demand base for electromagnetic brake replacement components, driven by the aging installed base of industrial machinery, commercial elevator systems, and material handling equipment across the manufacturing, commercial real estate, and logistics sectors where periodic brake component replacement is a standard maintenance requirement.

However, the Asia Pacific electromagnetic brakes market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive scale of new manufacturing infrastructure investment across China, South Korea, Japan, India, and the emerging industrial economies of Southeast Asia, where industrial robot adoption is accelerating across the automotive, electronics, and consumer goods manufacturing sectors. China's sustained investment in manufacturing modernization and domestic robotics capacity development continues to generate large-scale deployment of servo-driven automated production systems, creating growing domestic demand for electromagnetic brakes as both OEM components in locally manufactured machinery and as imported assemblies for advanced automation equipment procured from international suppliers. India's Production Linked Incentive schemes across electronics manufacturing, pharmaceutical production, automotive components, and specialty chemicals are driving manufacturing capacity investments that include substantial automation equipment procurement, creating a growing addressable market for electromagnetic braking components from both domestic and international suppliers. Japan and South Korea maintain strong demand for high-specification electromagnetic brakes driven by their advanced robotics, semiconductor manufacturing equipment, and precision machinery sectors, where manufacturers including Miki Pulley Co., Ltd. and Ogura Industrial Corp. maintain established competitive positions in their home markets while serving global customers through their international distribution networks.

Europe is a large and technically mature market for electromagnetic brakes, supported by the continent's deep industrial machinery manufacturing base in Germany, Italy, Sweden, and the Netherlands, and by a stringent regulatory environment that drives consistent compliance-led investment in certified, safety-rated electromagnetic brake solutions. German machine tool and automation equipment manufacturers, who produce a significant share of global capital equipment output, are among the most technically demanding purchasers of high-specification electromagnetic brakes, driving continued product development investment by leading European brake manufacturers including Mayr GmbH & Co. KG, KEB Automation KG, Kendrion N.V., and Precima Magnettechnik GmbH. The entry into full application of EU Machinery Regulation (EU) 2023/1230 in 2027 is expected to reinforce compliance-driven procurement of safety-certified electromagnetic braking solutions across European markets, providing a durable regulatory tailwind for electromagnetic brake demand throughout the forecast period.

Latin America and the Middle East and Africa represent smaller but developing markets for electromagnetic brakes, with demand concentrated in mining, oil and gas processing, and expanding manufacturing and logistics infrastructure. Growing capital investment in manufacturing automation across Brazil and Mexico, and the expansion of industrial and energy infrastructure projects across the Gulf Cooperation Council countries, are creating incremental demand for electromagnetic braking components in these regions, supported by the growing local presence of international brake manufacturers and motion control distributors.

The global electromagnetic brakes market is categorised by moderate consolidation at the premium technology segment, where a small number of established European, American, and Japanese manufacturers compete primarily on the basis of functional safety certification credentials, application engineering depth, coil response timing precision, torque density, and the ability to supply safety-certified brake assemblies to technically demanding robot, elevator, wind energy, and medical equipment OEM customers. Key competitive differentiators include the availability of spring-set electromagnetic brake product lines certified to ISO 13849 PLe and IEC 62061 SIL 2 for functional safety applications, the breadth of product portfolios covering the full torque range from miniature servo brakes to heavy-duty industrial and wind turbine applications, the strength of direct OEM design-in relationships with major robot and motor manufacturers, and the depth of application engineering expertise deployed across end-use industries.

Kendrion N.V. competes as a global leader in the industrial electromagnetic brake and clutch market through its broad product portfolio covering industrial, medical, and commercial vehicle applications, having significantly expanded its industrial brake capabilities through the acquisition of INTORQ GmbH & Co. KG, which added a comprehensive range of spring-set and tooth brake product lines to its industrial brakes portfolio. Regal Rexnord Corporation competes through its Warner Electric and Stromag brand portfolios, offering an extensive range of spring-set, power-on, particle, and hysteresis brake products supported by one of the broadest electromagnetic brake distribution networks across North America and Europe. Mayr GmbH & Co. KG and KEB Automation KG compete as leading German engineering specialists with strong design-in positions among European machine tool, elevator, and robotics OEMs through their ROBA-stop and safety brake product lines respectively. Japanese manufacturers Ogura Industrial Corp. and Miki Pulley Co., Ltd. maintain strong positions across Asia and in global markets through their comprehensive electromagnetic brake and clutch portfolios serving industrial automation, precision machinery, and office equipment sectors.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global electromagnetic brakes market include Kendrion N.V. (Netherlands), Regal Rexnord Corporation (U.S.), Ogura Industrial Corp. (Japan), Mayr GmbH & Co. KG (Germany), KEB Automation KG (Germany), Moog Inc. (U.S.), Nexen Group, Inc. (U.S.), Columbus McKinnon Corporation (U.S.), Miki Pulley Co., Ltd. (Japan), Carlyle Johnson Machine Company, LLC (U.S.), Precima Magnettechnik GmbH (Germany), Ortlinghaus-Werke GmbH (Germany), Placid Industries Inc. (U.S.), Sepac Inc. (U.S.), and Magnetic Technologies Corporation (U.S.), among others.

The global electromagnetic brakes market is expected to reach USD 2.90 billion by 2036 from an estimated USD 1.48 billion in 2026, at a CAGR of 7.0% during the forecast period 2026–2036.

In 2026, the spring-set (power-off) electromagnetic brakes segment is expected to hold the largest share of this market, driven by its established and non-substitutable role as the standard fail-safe braking solution for elevator, crane, servo motor, and industrial robot applications across all major industrial markets globally.

The electromagnetic hysteresis brakes segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by accelerating adoption in precision tension control applications, collaborative robot joint braking, and servo axis holding systems that require smooth, frictionless, and electrically controllable torque delivery with extended maintenance-free service life.

In 2026, the DC electromagnetic brakes segment is expected to hold the largest share of this market, reflecting the dominant adoption of DC coil designs across modern servo motor platforms, inverter-driven industrial machinery, and mobile robotic equipment globally.

In 2026, the industrial machinery and automation segment is expected to hold the largest share of this market, reflecting the pervasive integration of electromagnetic holding brakes across servo-driven manufacturing machinery, conveying systems, and automated assembly equipment across all major industrial economies.

The growth of this market is primarily driven by the accelerating adoption of industrial automation and servo-driven robotics globally, the sustained expansion of wind energy capacity requiring electromagnetic pitch and yaw braking systems, the tightening of machine safety regulations including EU Machinery Regulation (EU) 2023/1230 and global functional safety standards, the growing deployment of collaborative robots and autonomous mobile robots requiring compact safety-certified electromagnetic holding brakes, and the modernization of industrial machinery across Asia Pacific markets transitioning from legacy AC-driven platforms to modern inverter-driven and servo-controlled equipment.

Key players in the global electromagnetic brakes market include Kendrion N.V. (Netherlands), Regal Rexnord Corporation (U.S.), Ogura Industrial Corp. (Japan), Mayr GmbH & Co. KG (Germany), KEB Automation KG (Germany), Moog Inc. (U.S.), Nexen Group, Inc. (U.S.), Columbus McKinnon Corporation (U.S.), Miki Pulley Co., Ltd. (Japan), Carlyle Johnson Machine Company, LLC (U.S.), Precima Magnettechnik GmbH (Germany), Ortlinghaus-Werke GmbH (Germany), Placid Industries Inc. (U.S.), Sepac Inc. (U.S.), and Magnetic Technologies Corporation (U.S.).

Asia Pacific is expected to register the highest growth rate in the global electromagnetic brakes market during the forecast period 2026–2036, driven by accelerating manufacturing automation, rapid expansion of industrial robotics adoption in electronics and automotive production, large-scale wind energy capacity additions, and broad-based industrial infrastructure modernization across China, India, South Korea, Japan, and Southeast Asia.

Published Date: Jan-2025

Published Date: Sep-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates