Resources

About Us

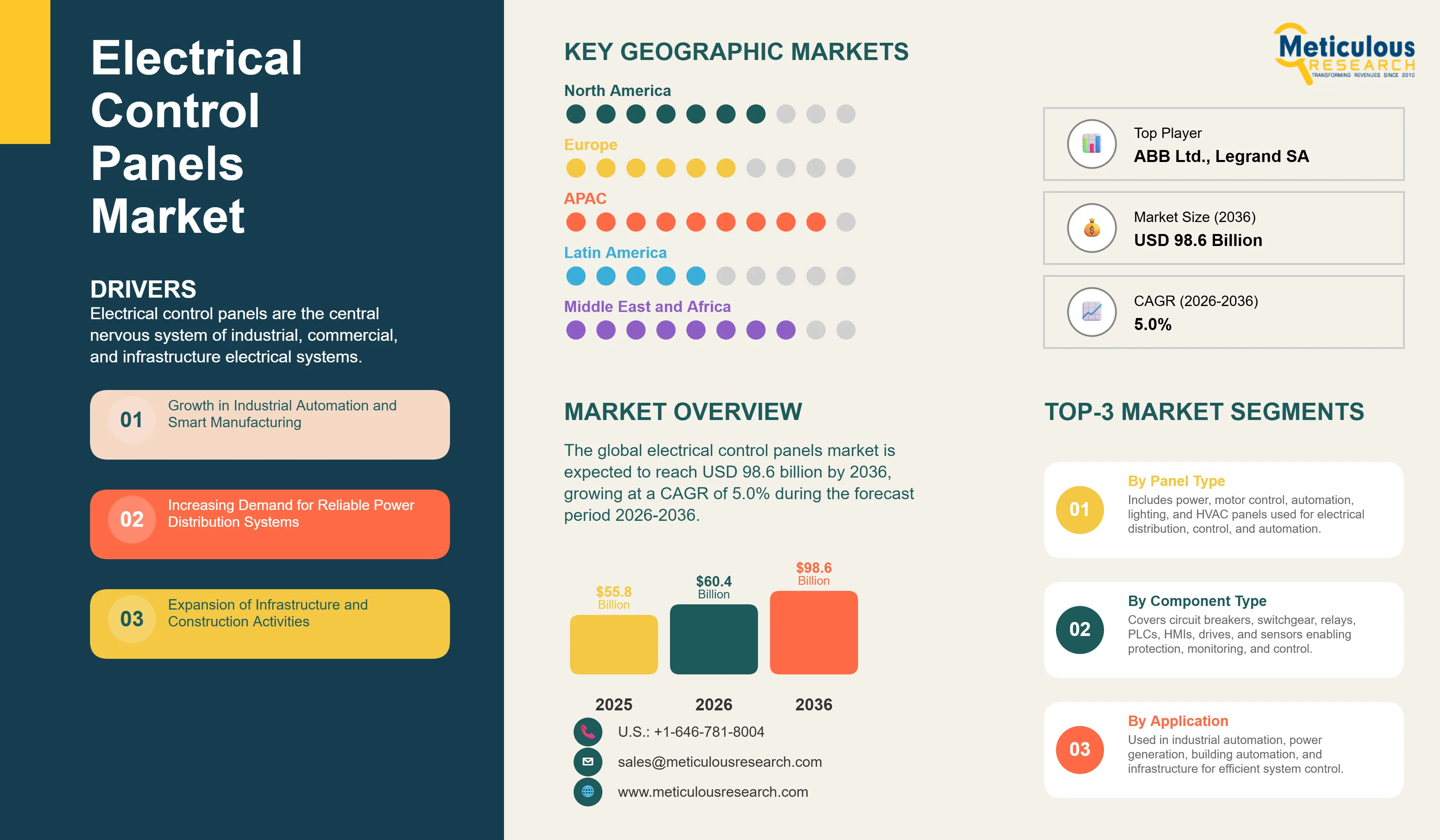

Electrical Control Panels Market Size, Share & Trends Analysis by Panel Type, Component Type, Application, and End-Use Industry- Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MREP - 1041941 Pages: 285 Apr-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global electrical control panels market was valued at USD 55.8 billion in 2025. This market is expected to reach USD 98.6 billion by 2036 from an estimated USD 60.4 billion in 2026, growing at a CAGR of 5.0% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Electrical control panels are the central nervous system of industrial, commercial, and infrastructure electrical systems. They house the circuit breakers, contactors, PLCs, drives, and monitoring devices that control and protect electrical equipment ranging from simple lighting circuits to complex automated production lines. Every modern factory, commercial building, power plant, water treatment facility, and data center relies on electrical control panels to manage the flow of electricity to its equipment safely and efficiently.

The market is growing because industrial automation is expanding rapidly across manufacturing sectors globally, and every new automated production line or robotic cell requires dedicated motor control and automation control panels. The global construction boom in infrastructure, commercial real estate, and data centers is generating very large quantities of power distribution and building automation panel demand. The accelerating deployment of solar and wind energy requires specialized control panels for inverter management, grid connection, and protection, adding a significant new demand segment that barely existed a decade ago.

Two key opportunities stand out. The integration of IoT connectivity and smart monitoring into control panels, allowing remote access, real-time diagnostics, and predictive maintenance through cloud platforms, is transforming panels from passive enclosures into intelligent nodes in the industrial internet of things. Simultaneously, the very large installed base of aging control panels in factories and utilities globally that need upgrading to comply with updated safety standards and to interface with new digital control systems is creating a substantial and growing retrofitting market alongside new installation demand.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 98.6 Billion |

|

Market Size in 2026 |

USD 60.4 Billion |

|

Market Size in 2025 |

USD 55.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 5.0% |

|

Dominating Panel Type |

Power Control Panels |

|

Fastest Growing Panel Type |

Automation Control Panels |

|

Dominating Component Type |

Circuit Breakers and Switchgear |

|

Fastest Growing Component Type |

Programmable Logic Controllers (PLC) |

|

Dominating Application |

Industrial Automation |

|

Fastest Growing Application |

Power Generation and Distribution |

|

Dominating End-Use Industry |

Manufacturing |

|

Fastest Growing End-Use Industry |

Energy & Utilities |

|

Dominating Voltage Level |

Low Voltage |

|

Fastest Growing Voltage Level |

Medium Voltage |

|

Dominating Mounting Type |

Floor-Mounted Panels |

|

Fastest Growing Mounting Type |

Wall-Mounted Panels |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Industry 4.0 Driving Intelligence into Control Panel Design

The adoption of Industry 4.0 principles across manufacturing is fundamentally changing what customers expect from electrical control panels. Traditional panels housed electromechanical components and performed protection and switching functions without any digital communication capability. Modern smart control panels integrate PLCs with Ethernet connectivity, SCADA interfaces, condition monitoring sensors, and cloud data logging as standard features, enabling remote monitoring, automated diagnostics, and integration with plant-wide manufacturing execution systems.

Rockwell Automation, Siemens, and Schneider Electric are driving this smart panel evolution through integrated automation architectures where the control panel is a connected node in a broader digital factory infrastructure. For panel builders and system integrators, smart panel capability has become a competitive requirement. Customers commissioning new production lines increasingly specify IoT connectivity, remote access, and energy monitoring as standard requirements, and panels without these features are no longer competitive for modern industrial automation projects.

Renewable Energy Boom Creating a New Specialist Panel Segment

The global expansion of solar, wind, and battery storage installations is creating a fast-growing specialist segment within the electrical control panels market. Solar farms and wind parks require combiner boxes, inverter control panels, grid interconnection switchboards, and energy management panels that are quite different from conventional industrial panels in their design requirements, environmental ratings, and certification needs. The scale of renewable energy deployment globally means that this segment is growing significantly faster than the traditional industrial and commercial panel markets.

Battery energy storage system panels, which manage the charge and discharge of large battery banks for grid stabilization, demand response, and renewable energy firming, are a newer and rapidly growing subset of this segment. As battery storage deployment accelerates alongside renewable energy, the demand for specialized battery management and protection panels is growing rapidly. Specialist panel manufacturers and the major automation companies are developing certified panel designs specifically for renewable energy applications to capture this fast-growing market.

Emerging Markets Infrastructure Drive Creating Large Panel Demand

The very large infrastructure investment programs underway across the Middle East, Southeast Asia, and Africa are creating substantial electrical control panel demand across multiple application areas simultaneously. New industrial cities, manufacturing zones, commercial developments, water treatment facilities, and power grid expansions all require large quantities of control panels at every stage of construction and fit-out. Saudi Arabia's Vision 2030 industrial program, India's manufacturing expansion under its Production Linked Incentive schemes, and the rapid industrial development of Vietnam and Indonesia are among the largest contributing drivers.

In these emerging markets, both the new installation market and the growing maintenance and upgrade market for earlier-installed panels are expanding. As industrial facilities installed ten to fifteen years ago require panel upgrades to interface with new automation systems or comply with updated safety standards, the retrofitting market is adding to the demand generated by new construction. Panel manufacturers with strong distribution networks and local system integrator partnerships in these markets are well-positioned to capture growing market share.

Growth in Industrial Automation and Smart Manufacturing

The global expansion of factory automation is the most consistent and reliable demand driver for electrical control panels. Every automated production line, robotic cell, conveyor system, and packaging machine requires motor control panels and automation panels to manage its electrical power and control logic. Global manufacturing investment is growing across automotive, electronics, food processing, pharmaceuticals, and consumer goods industries as companies build new capacity and upgrade existing plants with more automated equipment. The shift from labor-intensive to capital-intensive production models in Asia, combined with reshoring and nearshoring of manufacturing in North America and Europe, is generating sustained investment in new automated facilities that each require significant control panel procurement. Industrial automation investment is not cyclical in the way that some construction markets are: even in slower economic periods, manufacturers continue upgrading to automation to reduce costs and improve quality, providing a stable and growing baseline demand for control panels.

Rising Adoption of Renewable Energy Systems

The global deployment of solar, wind, and battery storage systems is creating structural new demand for specialized electrical control panels that did not exist at significant scale before 2010. A utility-scale solar farm requires dozens of string combiner boxes, inverter control panels, and MV switchboards. A wind farm requires nacelle control panels, HV transformer protection panels, and grid connection switchgear. A grid-scale battery storage system requires battery management system panels, power conversion system controls, and protection switchboards. As global renewable energy capacity continues growing rapidly, driven by falling technology costs and government decarbonization commitments, the demand for renewable energy-specific control panels is growing proportionally, adding a significant new and fast-growing demand category to the electrical control panels market.

Growth in Smart Control Panels with IoT Integration

The integration of IoT connectivity, remote monitoring, and intelligent diagnostics into control panels represents the most commercially significant product evolution opportunity in the electrical control panels market over the forecast period. Smart panels that can transmit operational data to cloud platforms, alert maintenance teams to developing faults, and allow remote configuration changes add substantial value over conventional panels and command premium pricing. For industrial customers facing production uptime pressure and skilled maintenance workforce shortages, the ability to remotely monitor panel health and diagnose issues before they cause unplanned shutdowns provides a quantifiable return that justifies the investment in smart panel technology. Panel manufacturers and system integrators that develop validated smart panel architectures with strong cybersecurity credentials and integration with widely used industrial IoT platforms such as Siemens MindSphere, Rockwell FactoryTalk, and Schneider EcoStruxure are positioned to capture the growing premium segment of this market.

Retrofitting and Upgradation of Legacy Systems

The enormous global installed base of electrical control panels that were installed ten to twenty-five years ago presents a large and growing market opportunity for retrofitting, upgrading, and modernizing existing installations. Many of these older panels use obsolete components for which spare parts are becoming unavailable, and they lack the digital communication capabilities needed to integrate with modern automation and energy management systems. Regulatory updates to electrical safety standards in key markets including the revision of IEC 61439 low voltage switchgear standards are creating compliance-driven retrofit requirements. For panel manufacturers and system integrators, retrofit projects offer attractive margins because they require detailed engineering assessment, custom component selection, and specialized installation work that is less price-competitive than new-build panel supply. The retrofit segment is expected to grow steadily through the forecast period as more of the post-2000 installation wave reaches the end of its economic service life.

By Panel Type: In 2026, Power Control Panels to Dominate

Based on panel type, the global market for electrical control panels is segmented into power control panels, motor control panels, automation control panels, lighting control panels, HVAC control panels, and other control panels. In 2026, the power control panels segment is expected to account for the largest share of the global electrical control panels market. Main and sub-distribution boards are required in every commercial, industrial, and infrastructure electrical installation to distribute power from the incoming supply to individual circuits and equipment. The universal requirement for power distribution panels across every building and facility type makes this the highest-volume panel category by a significant margin, with every new construction project requiring multiple distribution boards at various levels of the electrical distribution hierarchy.

However, the automation control panels segment is projected to register the highest CAGR during the forecast period. PLC and SCADA panels are growing faster than the overall market as industrial automation investment accelerates and as more previously manual or semi-automated processes are upgraded to fully automated control. The ongoing global expansion of manufacturing automation, combined with the growing demand for digital connectivity and remote monitoring in all types of industrial facilities, is driving strong growth in automation panel procurement across most industry sectors.

By Component Type: In 2026, Circuit Breakers and Switchgear to Hold the Largest Share

Based on component type, the global market is segmented into circuit breakers and switchgear, relays and contactors, PLCs, human machine interfaces, drives (VFDs and soft starters), sensors and monitoring devices, and other components. In 2026, the circuit breakers and switchgear segment is expected to account for the largest share of the global electrical control panels market. Circuit breakers and switchgear are the foundational protection and switching components in every type of electrical control panel and represent the highest total procurement value across the broadest range of panel types from simple distribution boards to complex industrial switchboards. Every panel contains circuit breakers at minimum, and many contain multiple layers of switchgear for different protection functions.

However, the PLCs segment is projected to register the highest CAGR during the forecast period. Programmable logic controllers are the intelligence at the heart of automation, motor control, and process control panels, and their adoption is growing rapidly as more industrial and infrastructure systems shift from relay-based to programmable control architectures. The expansion of industrial automation and the growing demand for smart, connected panels that can communicate with supervisory systems are both driving strong growth in PLC procurement for new and retrofit panel applications.

By Application: In 2026, Industrial Automation to Hold the Largest Share

Based on application, the global market is segmented into industrial automation, power generation and distribution, building automation, infrastructure projects, and other applications. In 2026, the industrial automation segment is expected to account for the largest share of the global electrical control panels market. Manufacturing plants, process industries, and automated production facilities represent the largest and most technically demanding application for electrical control panels, requiring motor control centers, PLC automation panels, and sophisticated protection schemes for complex multi-motor drive systems. The global scale of manufacturing investment makes industrial automation the dominant application by revenue.

However, the power generation and distribution segment is projected to register the highest CAGR during the forecast period. The renewable energy deployment boom is generating very large and fast-growing procurement of specialized control panels for solar, wind, and battery storage systems. Simultaneously, grid modernization programs in both developed and emerging markets are investing in upgraded substation and distribution switchgear that requires new control panel installations. The combination of these two demand sources is making power generation and distribution the fastest-growing application segment.

By End-Use Industry: In 2026, Manufacturing to Hold the Largest Share

Based on end-use industry, the global electrical control panels market is segmented into manufacturing, energy and utilities, oil and gas, commercial buildings, infrastructure, water and wastewater, and others. In 2026, the manufacturing segment is expected to account for the largest share of the global electrical control panels market. Manufacturing encompasses the broadest and most diverse range of electrical control panel applications, from simple motor control for conveyor systems to complex multi-axis robot controllers for automotive production. The very large global investment in manufacturing capacity, particularly in Asia, combined with ongoing automation upgrades in developed market factories, generates the highest total panel procurement of any end-use category.

However, the energy and utilities segment is projected to register the highest CAGR during the forecast period. The combination of renewable energy system deployment, grid modernization investment, and new power generation and transmission infrastructure is creating rapidly growing demand for control panels across the energy and utility sector. As energy transition investment accelerates globally, this segment is expected to grow significantly faster than manufacturing and other established end-use categories.

Electrical Control Panels Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global electrical control panels market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global market. The region's dominance reflects the extraordinary scale of its manufacturing and infrastructure sectors. China is by far the world's largest manufacturing economy and also the largest investor in renewable energy, data center infrastructure, and grid modernization, making it the single largest national market for electrical control panels globally. India's rapid industrial expansion, supported by the government's Production Linked Incentive schemes and manufacturing zone development, is generating large control panel demand across automotive, electronics, pharmaceuticals, and food processing sectors. Japan, South Korea, and Taiwan all have very large and sophisticated electronics and semiconductor manufacturing industries that require the highest-specification automation and process control panels. Southeast Asian industrial economies including Vietnam, Thailand, and Indonesia are growing rapidly as manufacturing investment flows into the region from China and from developed market manufacturers seeking to diversify their supply chains. The combination of the world's largest manufacturing investment volumes, very rapid renewable energy deployment, and extensive ongoing infrastructure construction makes Asia-Pacific the dominant region by a large margin.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. Saudi Arabia's Vision 2030 transformation program is investing at unprecedented scale in new industrial cities, manufacturing zones, petrochemical complexes, tourism infrastructure, and utility-scale renewable energy, all of which generate large electrical control panel procurement. The UAE's continued expansion as a commercial, logistics, and data center hub is driving commercial building and data center panel demand. Egypt's industrial development programs, Turkey's large manufacturing sector expansion, and the growing economic development investment across Sub-Saharan Africa collectively contribute to the region's above-average growth trajectory. The combination of large new construction programs starting from a lower installed base than mature markets generates the highest percentage growth rate of any region through the forecast period.

North America is a large and technologically sophisticated electrical control panels market, driven by continued manufacturing investment including reshoring programs, major data center construction, infrastructure modernization spending under the U.S. Infrastructure Investment and Jobs Act, and the rapid expansion of renewable energy across solar and wind installations. Rockwell Automation's strong position in the U.S. industrial automation panel market, combined with the broad presence of Schneider Electric, Eaton, and Siemens, gives the market a competitive and innovative supplier ecosystem. Europe is characterized by high technical standards, strong demand for energy-efficient and smart panel solutions, and significant industrial automation investment particularly in Germany, which has Europe's most active manufacturing automation market. European renewable energy deployment, particularly in Germany, Spain, and the UK, is also driving growing demand for specialized energy control panels.

The electrical control panels market is served by a combination of large diversified electrical and automation companies that supply the key components and complete panel solutions, specialist panel builders and integrators that design and build custom panels for specific applications, and local panel fabricators serving regional markets. The market is more fragmented than the power quality equipment market because panel building is often a local or regional activity where proximity to the installation site and understanding of local electrical codes and standards are important competitive advantages.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, geographic presence, and recent strategic developments. Some of the key players operating in the global electrical control panels market include Schneider Electric SE (France), Siemens AG (Germany), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), Rockwell Automation Inc. (U.S.), Mitsubishi Electric Corporation (Japan), General Electric Company (U.S.), Larsen & Toubro Limited (India), Fuji Electric Co. Ltd. (Japan), Delta Electronics Inc. (Taiwan), Legrand SA (France), Rittal GmbH & Co. KG (Germany), Emerson Electric Co. (U.S.), Hitachi Ltd. (Japan), and Honeywell International Inc. (U.S.), among others.

The global electrical control panels market is expected to reach USD 98.6 billion by 2036 from an estimated USD 60.4 billion in 2026, at a CAGR of 5.0% during the forecast period 2026-2036.

In 2026, the power control panels segment is expected to hold the largest share of the global electrical control panels market, driven by main and sub-distribution boards being a universal requirement in every commercial, industrial, and infrastructure electrical installation and representing the highest-volume panel category by a significant margin.

The automation control panels segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the accelerating global adoption of industrial automation and the growing demand for PLC and SCADA-based digital control systems across manufacturing, process industries, and infrastructure.

In 2026, the industrial automation segment is expected to hold the largest share of the global electrical control panels market, reflecting manufacturing and process industries being the largest and most technically demanding application for motor control, automation, and protection panels.

Asia-Pacific is expected to dominate the global electrical control panels market in 2026, driven by China's position as the world's largest manufacturing economy and renewable energy investor, India's rapid industrial expansion, and the large-scale manufacturing and infrastructure investment across Japan, South Korea, and Southeast Asia.

The market is primarily driven by the global expansion of industrial automation generating consistent high demand for motor control and automation panels across manufacturing sectors, and by the accelerating deployment of renewable energy systems creating fast-growing demand for specialized solar, wind, and battery storage control panels as a new and significant application category.

Key players are Schneider Electric SE (France), Siemens AG (Germany), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), Rockwell Automation Inc. (U.S.), Mitsubishi Electric Corporation (Japan), General Electric Company (U.S.), Larsen & Toubro Limited (India), Fuji Electric Co. Ltd. (Japan), Delta Electronics Inc. (Taiwan), Legrand SA (France), Rittal GmbH & Co. KG (Germany), Emerson Electric Co. (U.S.), Hitachi Ltd. (Japan), and Honeywell International Inc. (U.S.), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global electrical control panels market during the forecast period 2026-2036, driven by Saudi Arabia's Vision 2030 industrial transformation programs creating very large new control panel demand across manufacturing, energy, and infrastructure projects, alongside the UAE's continued large-scale commercial and data center construction activity.

Published Date: Jul-2025

Published Date: Jun-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates