Resources

About Us

Smart Grid Market Size, Share & Trends Analysis by Component, Grid Layer, Application, End User, Communication Technology, Voltage Level, and Geography - Global Opportunity Analysis & Industry Forecast (2026-2036)

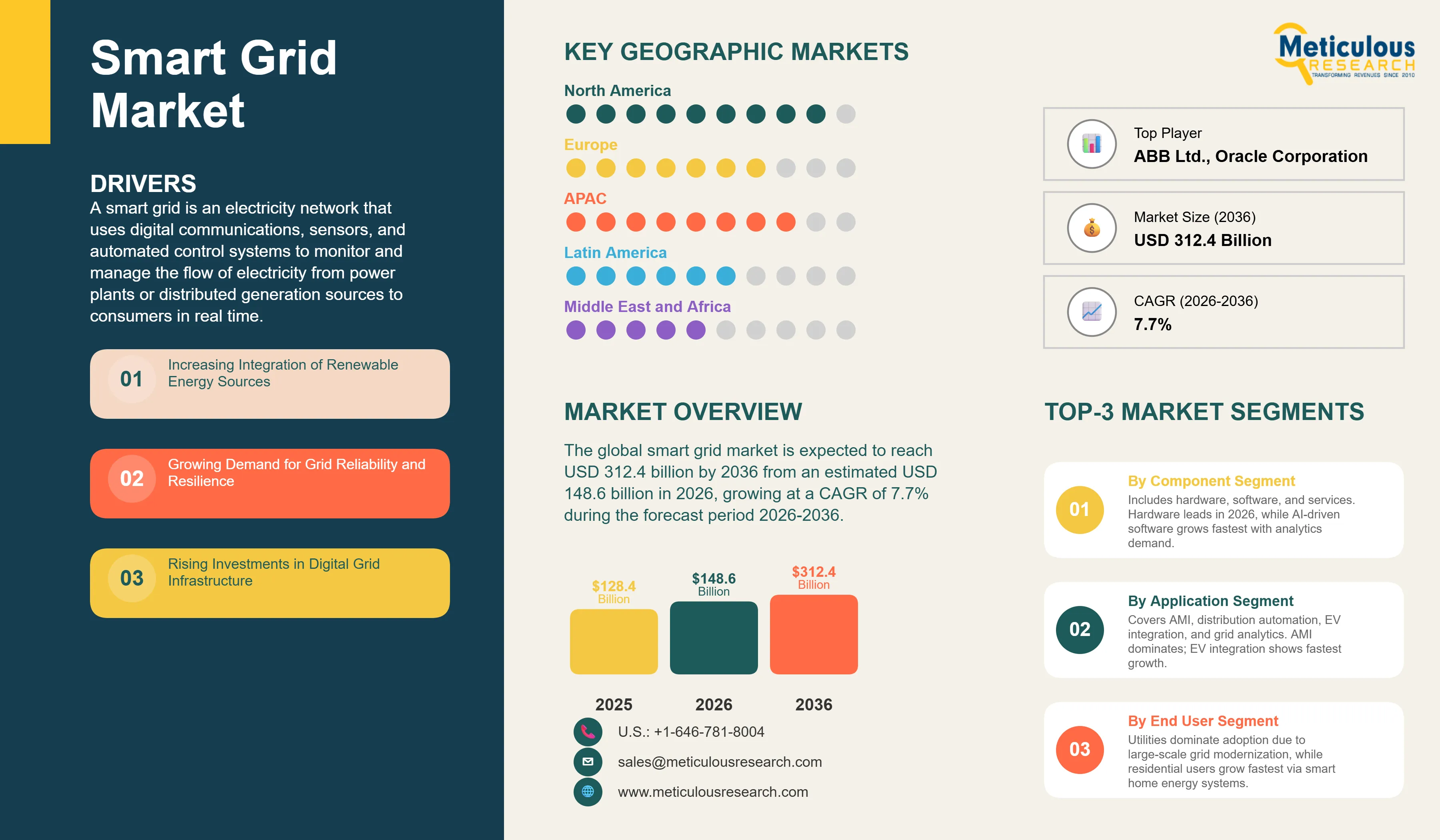

Report ID: MRSE - 1041937 Pages: 280 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global smart grid market was valued at USD 128.4 billion in 2025. This market is expected to reach USD 312.4 billion by 2036 from an estimated USD 148.6 billion in 2026, growing at a CAGR of 7.7% during the forecast period 2026-2036. According to the International Energy Agency’s World Energy Investment 2025 report, global investment in electricity grids reached approximately USD 400–420 billion in 2024, up from around USD 370–380 billion in 2023, reflecting continued record-level spending. Grid investment has now become one of the fastest-growing segments of the energy sector, underscoring its critical role in enabling renewable energy integration, electrification, and energy security.

Click here to: Get Free Sample Pages of this Report

A smart grid is an electricity network that uses digital communications, sensors, and automated control systems to monitor and manage the flow of electricity from power plants or distributed generation sources to consumers in real time. Unlike a conventional grid, where electricity flows one-way from large centralized generators through transmission and distribution networks to passive consumers, a smart grid creates a two-way system where utilities can monitor consumption, detect faults, redirect power flows, and respond to demand changes automatically and instantly. Smart meters in homes and businesses communicate usage data back to utilities, distribution automation systems identify and isolate faults before they cascade into widespread outages, and demand response programs reduce load during peak periods by signaling connected devices and industrial systems to temporarily reduce consumption.

The market is growing at an accelerating pace because grid modernization is no longer optional: it has become operationally necessary. According to the IEA's World Energy Investment 2024, the world added a record 295 gigawatts of solar and wind capacity in 2023, and grids designed for centralized coal and gas generation are struggling to integrate this intermittent distributed capacity without smart monitoring and automated balancing systems. The U.S. Department of Energy's Grid Deployment Office has noted that the average age of large power transformers in the U.S. is over 40 years, and a significant portion of the transmission system was built in the 1950s and 1960s. Across Europe, the IEA estimates that EUR 600 billion in additional grid investment will be required by 2030 to meet the EU's clean energy targets. These infrastructure realities are generating substantial and urgent government-backed investment commitments globally.

Two specific opportunities stand out. The growth of distributed energy resources including rooftop solar, behind-the-meter battery storage, and small-scale wind is transforming millions of electricity consumers into prosumers who both consume and produce electricity. Managing this two-way flow requires distribution management systems, advanced inverter controls, and real-time monitoring that conventional grids cannot provide. Equally important is EV integration: according to the IEA's Global EV Outlook 2024, global EV sales reached 14 million in 2023, and managing the charging loads of tens of millions of EVs without causing local grid overloads requires smart charging management systems and ultimately vehicle-to-grid capabilities that are driving a major new smart grid investment cycle.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 312.4 Billion |

|

Market Size in 2026 |

USD 148.6 Billion |

|

Market Size in 2025 |

USD 128.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 7.7% |

|

Dominating Component |

Hardware |

|

Fastest Growing Component |

Software (Analytics & AI Platforms) |

|

Dominating Grid Layer |

Distribution |

|

Fastest Growing Grid Layer |

Consumption |

|

Dominating Application |

Advanced Metering Infrastructure (AMI) |

|

Fastest Growing Application |

EV Integration |

|

Dominating End User |

Utilities |

|

Fastest Growing End User |

Residential |

|

Dominating Communication Technology |

Wired (PLC, Fiber Optics) |

|

Fastest Growing Communication Technology |

Cellular (4G/5G) |

|

Dominating Voltage Level |

Medium Voltage |

|

Fastest Growing Voltage Level |

Low Voltage |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Record Global Grid Investment Driven by Energy Transition Urgency

Grid investment has reached historic levels globally and is continuing to grow. According to the IEA's World Energy Investment 2025 report, global electricity grid investment reached USD 400-420 billion in 2024, and the first time grid investment has exceeded clean energy generation investment globally. The IEA projects that grid investment will need to reach over USD 600 billion annually by 2030 to stay on track with net-zero scenarios, meaning the market is currently operating significantly below the required investment rate. This gap between current and needed investment represents a large and growing commercial opportunity for smart grid technology and service providers.

The U.S. Bipartisan Infrastructure Law allocated USD 65 billion specifically for electricity grid upgrades, representing the largest federal grid investment in American history. The EU's REPowerEU plan has established grid investment as a top priority, with member states required to fast-track permitting for grid projects and the European Commission estimating that EUR 584 billion in grid investment is needed by 2030. In India, the Smart Grid Mission and the Revamped Distribution Sector Scheme have committed over INR 3 lakh crore (approximately USD 36 billion) to distribution network modernization. These are not distant plans but actively funded and executing programs, generating near-term procurement demand for smart grid hardware, software, and services.

AI and Digital Twin Technology Transforming Grid Operations

Artificial intelligence and digital twin technology are rapidly moving from pilot programs into operational deployment across major utilities globally, representing a fundamental shift in how grids are planned, operated, and maintained. A digital twin of an electricity distribution network is a real-time virtual replica of the physical network, continuously updated with sensor data from smart meters, substation monitors, and grid sensors, that allows operators to run simulations of different operating scenarios, test the impact of connecting new load or generation, and predict equipment failures before they occur. Siemens Energy and ABB have both developed digital twin platforms for power grids, and several large utilities including National Grid in the UK and E.ON in Germany have deployed digital twins covering portions of their distribution networks.

AI applications in grid management are delivering measurable operational benefits. Google DeepMind's AI model, applied to grid management in a 2023 research collaboration with utilities, demonstrated the ability to predict grid constraints with significantly greater accuracy than conventional methods. Itron's artificial intelligence forecasting tools, used by utilities in the U.S. and Europe, improve load forecasting accuracy and reduce the need for costly spinning reserve capacity. According to a 2024 report by the Rocky Mountain Institute, utilities deploying AI-based grid management systems are reporting reductions in outage duration of 20 to 40% and improvements in asset utilization that reduce capital expenditure requirements. These documented operational returns are building the business case for AI investment across the global utility sector.

EV Integration Becoming the Defining Grid Challenge of the Late 2020s

The rapid growth of electric vehicle adoption is creating the most immediate and technically challenging grid integration problem that distribution utilities have faced in decades. According to the International Energy Agency’s Global EV Outlook 2025, global electric vehicle (EV) sales exceeded 17 million units in 2024, up from 14 million in 2023, while the total global EV stock surpassed 45 million vehicles, reflecting continued rapid growth in electric mobility adoption. When an EV charging at 11 kW represents approximately the same electrical load as adding five average European homes to the local distribution network, the simultaneous evening charging of multiple EVs on a residential street can rapidly exceed the capacity of distribution transformers and cables that were never designed for this load profile. Unmanaged EV charging is already causing local grid stress in dense EV adoption markets including Norway, where EV market share exceeded 90% of new car sales in 2023, and in California, where utilities have documented transformer stress from EV charging loads.

The smart grid solution to the EV challenge is managed charging, where smart charging systems communicate with EVs, home energy management systems, and grid operators to schedule and shape charging load in ways that avoid coincident peak demand and can be shifted to periods of high renewable generation and low grid stress. Vehicle-to-grid technology, which allows EVs to discharge electricity back to the grid during peak demand events, is being piloted by utilities in the UK, Japan, and the U.S. and represents a potentially transformative grid resource: the IEA estimates that the global EV fleet could theoretically provide over 2,400 GWh of battery storage by 2030, dwarfing the current global installed grid-scale battery storage capacity. These applications are driving significant smart grid software and infrastructure investment across the distribution layer.

Increasing Integration of Renewable Energy Sources

According to the IEA's Renewables 2024 report, the world added a record 295 GW of renewable energy capacity in 2023, and the IEA projects that renewable energy will account for over 40% of global electricity generation by 2030. Integrating this volume of variable generation into power systems designed for controllable thermal plants requires a fundamentally different approach to grid management. Solar and wind generate electricity based on weather conditions rather than demand, and their output can vary significantly within minutes. Managing this variability without causing frequency instability or voltage fluctuations requires smart grid systems including advanced SCADA, automated demand response, distributed energy resource management systems, and energy storage coordination that can balance supply and demand in real time. Every gigawatt of new renewable capacity added to the grid increases the need for smart grid investment to maintain system stability, creating a direct and growing linkage between the global renewable energy boom and smart grid market growth.

Electrification of Transportation (EV Integration)

The global EV fleet exceeded 40 million in 2023 and grew to 45+ million in 2024, according to the International Energy Agency, and BloombergNEF's Electric Vehicle Outlook 2024 projects that EVs will account for 75% of global passenger vehicle sales by 2040. Managing the charging loads of this growing EV fleet without causing grid congestion and local outages requires smart charging management systems, time-of-use tariff infrastructure, and ultimately vehicle-to-grid capabilities. The U.S. DOE's National Electric Vehicle Infrastructure program is installing charging infrastructure across the country, with federal requirements that new NEVI-funded chargers must include smart charging capabilities including demand response and grid communication. European utilities including E.ON and Enel have both launched large-scale smart EV charging infrastructure programs that integrate charging management with their smart grid platforms, creating direct demand for grid software and communication infrastructure upgrades.

Growth of Distributed Energy Resources (DERs)

The rapid proliferation of rooftop solar, behind-the-meter battery storage, and small-scale wind generation is creating a new operational challenge for distribution utilities: managing a grid that increasingly generates as well as consumes electricity at the distribution level. According to Wood Mackenzie's 2024 Distributed Energy Resources Outlook, global distributed solar capacity additions exceeded 300 GW in 2023, and the global behind-the-meter battery storage market is growing at over 30% annually. Managing these distributed resources requires distributed energy resource management systems that can aggregate, monitor, and control thousands or millions of small generating assets to provide grid services that were previously only available from large centralized generators. Utilities that deploy effective DERMS platforms can monetize the flexibility of their customers' distributed assets, reducing the need for costly grid reinforcement and new peaking generation while providing customers with optimized returns on their solar and storage investments.

AI and Advanced Analytics in Grid Management

AI-based grid analytics platforms are transitioning from early adoption to mainstream deployment across the global utility sector, creating a substantial and growing software market segment. Predictive maintenance applications use machine learning models trained on sensor data from transformers, cables, and substation equipment to identify developing equipment failures days or weeks before they cause outages, allowing utilities to schedule proactive maintenance at significantly lower cost than emergency repair. Load forecasting AI models improve accuracy for both short-term operational planning and long-term capacity planning, reducing the reserve margin utilities must maintain and lowering electricity system costs. Advanced distribution state estimation, which uses smart meter data and network sensors to create real-time models of power flows across distribution networks, enables utilities to optimize network operation and delay expensive infrastructure investment. The EPRI's 2024 Technology Innovation Outlook identifies AI-enhanced grid analytics as one of the highest-priority technology investments for the global utility sector, with expected returns through reduced outage costs, deferred capital expenditure, and improved renewable energy integration capability.

By Component: In 2026, Hardware to Hold the Largest Share

Based on component, the global smart grid market is segmented into hardware (smart meters, sensors, transformers and switchgear, communication equipment), software (grid management software, analytics and AI platforms, energy management systems, distribution management systems), and services (consulting, integration and deployment, maintenance and support). In 2026, the hardware segment is expected to account for the largest share of the global smart grid market. Smart meters, substation automation equipment, grid sensors, and communication infrastructure represent the largest procurement category by value in grid modernization programs globally. The scale of smart meter rollouts alone is very large: according to the IEA, over 1 billion smart meters were installed globally by end 2023, with hundreds of millions more planned across China, India, and emerging markets over the next five years.

However, the software segment, particularly analytics and AI platforms, is projected to register the highest CAGR during the forecast period. As the hardware infrastructure of smart grids matures, utilities are increasingly investing in the software layers that extract operational value from the data generated by smart meters and grid sensors. AI-based grid analytics, digital twin platforms, and distribution management systems are growing faster than the hardware market and command improving margins, with subscription-based software pricing models generating recurring revenue streams for providers including Oracle, Schneider Electric, and Siemens.

By Application: In 2026, Advanced Metering Infrastructure to Hold the Largest Share

Based on application, the global smart grid market is segmented into advanced metering infrastructure, distribution automation, demand response management, renewable energy integration, EV integration, grid analytics and monitoring, and other applications. In 2026, the AMI segment is expected to account for the largest share of the global smart grid market. Smart metering programs represent the largest and most mature smart grid investment category globally, with mandatory smart meter rollouts mandated or in progress in the EU, the UK, the U.S., China, India, and many other markets. The EU's revised Energy Efficiency Directive requires member states to ensure that 80% of consumers have smart meters by 2024 where technically feasible and cost-justified. China's State Grid Corporation has deployed over 600 million smart meters making it the world's largest single smart metering program. These programs generate very large hardware procurement volumes and associated meter data management and analytics software investment.

However, the EV integration segment is projected to register the highest CAGR during the forecast period. With global EV sales growing, the smart grid software and infrastructure required to manage EV charging loads at scale, including managed charging systems, demand response for EV chargers, and vehicle-to-grid platforms, is growing from an early-stage deployment base to commercial mainstream adoption across all major EV markets.

By End User: In 2026, Utilities to Hold the Largest Share

Based on end user, the global smart grid market is segmented into utilities, industrial, commercial, and residential. In 2026, the utilities segment is expected to account for the largest share of the global smart grid market. Electric utilities are the primary investors in smart grid infrastructure globally, deploying smart meters, distribution automation, SCADA upgrades, and grid analytics platforms as part of their asset management and network modernization programs. The scale of utility investment is very large: a single major national utility modernization program can represent billions of dollars of smart grid technology procurement over a multi-year deployment cycle.

However, the residential segment is projected to register the highest CAGR during the forecast period. Smart home energy management systems, residential batteries, rooftop solar inverters with grid communication, smart EV chargers, and demand response-enabled appliances are creating a growing residential smart grid participation market. As time-of-use electricity tariffs become more widely available and as home energy management apps allow consumers to optimize their electricity costs by shifting flexible loads to low-price periods, residential engagement with smart grid programs is growing rapidly and creating a fast-growing market for consumer-facing smart grid technology.

Smart Grid Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global smart grid market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global smart grid market. The United States has been investing in grid modernization longer than any other major market, and the Bipartisan Infrastructure Law's USD 65 billion grid allocation represents the largest single federal grid investment in U.S. history, supporting smart meter deployments, transmission upgrades, and distribution automation across the country's over 3,000 electric utilities. According to the Edison Electric Institute, U.S. electric utilities invested approximately USD 140 billion in infrastructure in 2023, with a growing share directed toward smart grid technology. The U.S. also has the world's largest advanced metering infrastructure deployment, with over 130 million smart meters installed according to the U.S. Energy Information Administration's 2024 data. Grid reliability challenges, including the increasing frequency of severe weather-related outages highlighted by events such as Winter Storm Uri in 2021, are driving continued utility investment in grid resilience technology including automated self-healing distribution systems and advanced monitoring. Canada's grid modernization programs, particularly in Ontario, British Columbia, and Alberta, add to the regional demand base.

However, the Asia-Pacific smart grid market is expected to grow at the fastest CAGR during the forecast period. China is undertaking the world's most ambitious grid modernization program: State Grid Corporation of China, which operates the world's largest utility network, has committed to investing over CNY 6 trillion (approximately USD 840 billion) in grid infrastructure over the 2021 to 2025 period, with a major portion directed toward smart grid technology, ultra-high voltage transmission, and distribution automation. According to China's National Energy Administration, China had deployed over 600 million smart meters by 2024, making it the world's largest single smart metering deployment. India's Smart Grid Mission and the Revamped Distribution Sector Scheme are directing over USD 36 billion toward distribution network modernization across India's state distribution companies, addressing the country's very high distribution losses which the Ministry of Power reported at approximately 17% in 2024. Japan's grid is undergoing significant modernization driven by the integration of distributed rooftop solar, which has grown rapidly following post-Fukushima energy policy changes, and South Korea's Smart Grid Roadmap targets nationwide smart grid deployment supported by government investment programs.

Europe is a technically advanced smart grid market driven by the EU's ambitious clean energy targets and the world's most comprehensive smart metering mandates. Germany, the Netherlands, France, and the Nordic countries are among the most active European smart grid investment markets. The EU's revised Energy Efficiency Directive requires 80% smart meter penetration where cost-justified, and the Clean Energy for All Europeans package creates the regulatory framework for demand response, prosumer participation, and energy community models that require smart grid infrastructure to operate. Norway's very high EV penetration above 90% of new car sales in 2023 per the Norwegian Road Federation is creating immediate smart grid integration requirements that are making Norway an active early-adopter market for EV-integrated smart grid solutions.

The smart grid market is served by large diversified energy technology companies that provide both the physical hardware of grid modernization and the software platforms that operate it, IT and software companies applying enterprise technology to grid management, and specialized smart metering and grid automation companies. Competition is based on the comprehensiveness and integration of the smart grid technology portfolio, software platform capabilities particularly in AI and analytics, cybersecurity credentials, the strength of utility relationships and reference deployments, and geographic reach.

Siemens AG and Siemens Energy AG together provide one of the broadest smart grid portfolios in the market, covering transmission and distribution automation, SCADA systems, smart metering, and grid analytics through their respective Energy Management and Grid Technologies divisions. ABB provides grid automation, HVDC transmission, and substation automation technology, with its Ability digital platform covering grid management software. Schneider Electric's EcoStruxure Grid platform integrates advanced distribution management, outage management, and grid analytics for utilities globally. GE Grid Solutions, now operating as part of GE Vernova, provides grid automation, protection, and control systems for transmission and distribution networks. Hitachi Energy, the former ABB Power Grids business acquired by Hitachi, has a strong position in HVDC, transformers, and grid automation. Itron and Landis+Gyr are the world's two leading smart metering companies, each supplying hundreds of millions of smart meters globally with integrated meter data management and analytics platforms.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology portfolios, utility customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global smart grid market include Siemens AG (Germany), ABB Ltd. (Switzerland), Schneider Electric SE (France), General Electric Company/GE Vernova (U.S.), Hitachi Energy Ltd. (Switzerland), Eaton Corporation plc (Ireland), Itron Inc. (U.S.), Landis+Gyr Group AG (Switzerland), Honeywell International Inc. (U.S.), Cisco Systems Inc. (U.S.), Oracle Corporation (U.S.), IBM Corporation (U.S.), Wipro Limited (India), Infosys Limited (India), and Siemens Energy AG (Germany), among others.

The global smart grid market is expected to reach USD 312.4 billion by 2036 from an estimated USD 148.6 billion in 2026, at a CAGR of 7.7% during the forecast period 2026-2036. According to the IEA's World Energy Investment 2024, global grid investment reached a record USD 400 billion in 2023, and the IEA projects annual grid investment must exceed USD 600 billion by 2030 to meet net-zero scenarios, indicating the market is well below the required investment level and has significant growth ahead.

In 2026, the advanced metering infrastructure segment is expected to hold the largest share of the global smart grid market, driven by mandatory smart meter rollout programs across the EU, the U.S., China, and India. China's State Grid Corporation alone has deployed over 600 million smart meters, and the U.S. has over 130 million installed according to the U.S. EIA's 2024 data.

The EV integration segment is projected to register the highest CAGR during the forecast period 2026-2036. With global EV sales reaching 14 million in 2023 per the IEA and the global EV stock exceeding 40 million vehicles, managing EV charging loads requires smart charging management systems, demand response infrastructure, and ultimately vehicle-to-grid platforms, creating rapidly growing smart grid software and hardware demand.

The U.S. Bipartisan Infrastructure Law allocated USD 65 billion specifically for electricity grid upgrades, the largest federal grid investment in U.S. history. This is in addition to ongoing utility capital expenditure of approximately USD 140 billion annually according to the Edison Electric Institute 2023 data, a growing portion of which is directed toward smart grid technology.

The market is primarily driven by the urgent need to integrate record volumes of renewable energy into power systems designed for centralized generation, with the IEA reporting 295 GW of new renewable capacity added in 2023, combined with the grid modernization funding commitments from governments globally, including USD 65 billion in the U.S. and EUR 584 billion projected for Europe by 2030, and the rapidly growing EV fleet creating new smart charging management requirements.

Key players are Siemens AG (Germany), ABB Ltd. (Switzerland), Schneider Electric SE (France), General Electric Company/GE Vernova (U.S.), Hitachi Energy Ltd. (Switzerland), Eaton Corporation plc (Ireland), Itron Inc. (U.S.), Landis+Gyr Group AG (Switzerland), Honeywell International Inc. (U.S.), Cisco Systems Inc. (U.S.), Oracle Corporation (U.S.), IBM Corporation (U.S.), Wipro Limited (India), Infosys Limited (India), and Siemens Energy AG (Germany), among others.

Asia-Pacific is expected to register the highest growth rate in the global smart grid market during the forecast period 2026-2036. China's State Grid commitment of approximately USD 840 billion in grid infrastructure over 2021 to 2025, India's USD 36 billion distribution modernization program under the RDSS scheme, and the rapidly growing renewable energy and EV fleets across the region collectively make Asia-Pacific the highest-growth smart grid investment region globally.

Published Date: May-2025

Published Date: Sep-2025

Published Date: Mar-2026

Published Date: Aug-2024

Published Date: Dec-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates