Resources

About Us

Europe Food Waste Recycling Market Size, Share & Trends Analysis by Byproduct (Organic Fertilizers, Biofuels, Animal Feed, Bioplastics, Biochemicals), Feedstock Source, Recycling Method, End Use Application, and Geography — Opportunity Analysis and Industry Forecast (2026–2036)

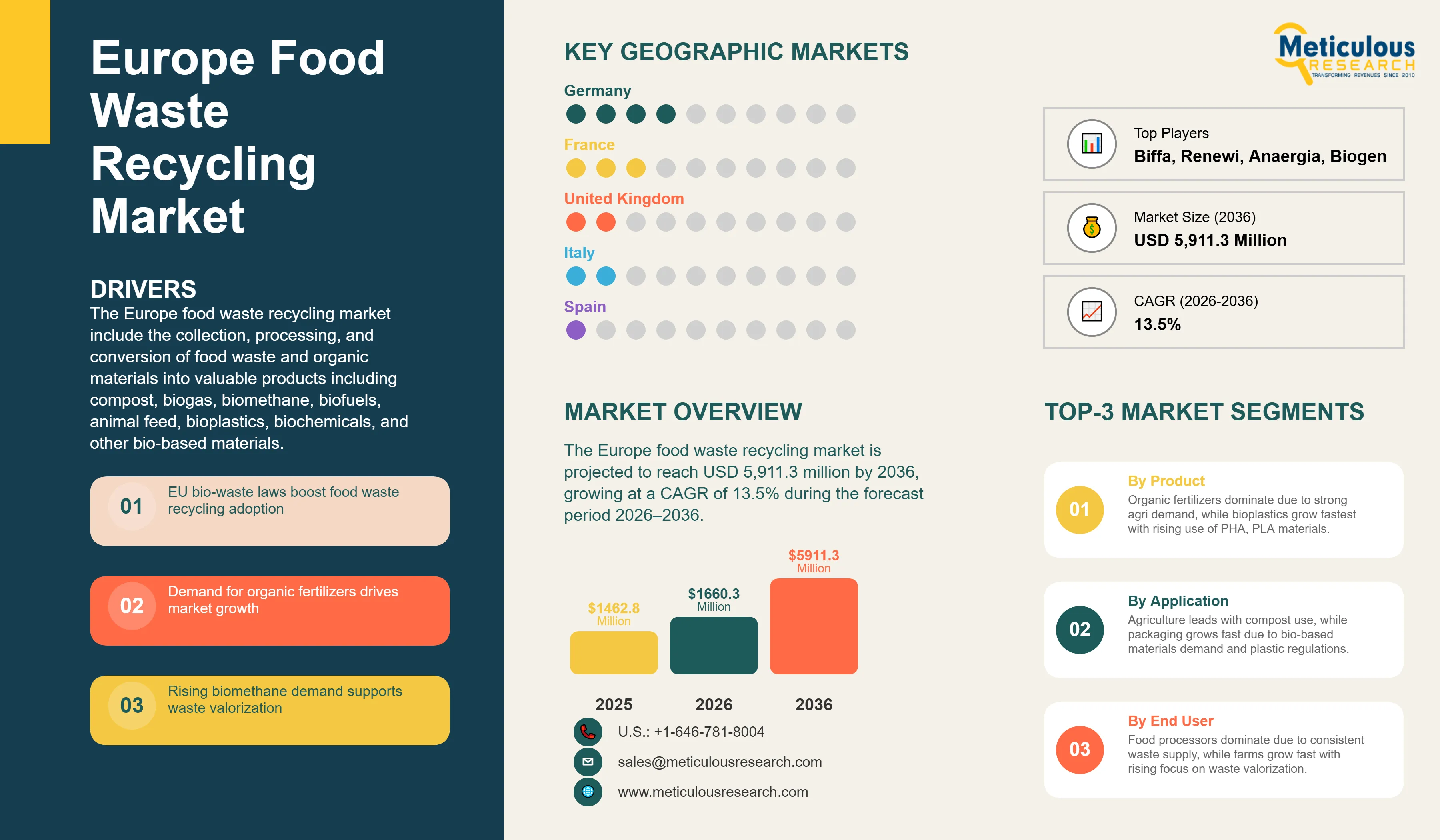

Report ID: MRAGR - 1041566 Pages: 470 Apr-2026 Formats*: PDF Category: Agriculture Delivery: 2 to 4 Hours Download Free Sample ReportThe Europe food waste recycling market was valued at USD 1,660.3 million in 2026 and is projected to reach USD 5,911.3 million by 2036, growing at a CAGR of 13.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The Europe food waste recycling market include the collection, processing, and conversion of food waste and organic materials into valuable products including compost, biogas, biomethane, biofuels, animal feed, bioplastics, biochemicals, and other bio-based materials. These products are generated through a range of treatment methods including anaerobic digestion, composting, fermentation, hydrothermal processing, and integrated biorefinery approaches. With Europe generating an estimated 58 to 60 million tonnes of food waste annually across all sectors of the food supply chain, the recycling infrastructure plays a vital role in diverting organic materials from landfills, reducing methane emissions, recovering valuable nutrients, and contributing to renewable energy production in alignment with the European Green Deal and Waste Framework Directive requirements.

Food waste recycling has been a key component in Europe circular economy strategy, solving environmental concerns related to greenhouse gas emissions from landfills, resource depletion, and sustainable waste management. The sector processes organic waste generated at every stage of the food supply chain, from agricultural production and food processing to retail, hospitality, and household consumption. Advanced processing technologies transform this organic waste into renewable energy in the form of biogas and biomethane, nutrient-rich fertilizers and soil amendments, and a growing range of value-added chemical and material products, supporting the region's ambitious sustainability targets.

The growth of the food waste recycling market in Europe is primarily driven by the mandatory bio-waste separate collection obligations introduced under the revised EU Waste Framework Directive, the European Green Deal's climate neutrality and circular economy commitments that elevate food waste valorization as a strategic policy priority, and the accelerating demand for domestically produced organic fertilizers, biomethane, and bio-based materials that can be derived from recycled food waste streams across European member states. Furthermore, the rising deployment of Extended Producer Responsibility schemes and the growing commercial appetite for carbon credit monetization linked to methane avoidance and biogenic carbon sequestration are reinforcing market expansion.

However, the growth of this market is restrained by the high capital investment requirements for advanced food waste processing infrastructure, challenges of feedstock contamination and quality inconsistency that affect output of product quality, and the complexity of achieving regulatory compliance across 27 divergent national waste management legislative frameworks.

The development of integrated biorefinery models capable of generating high-value chemical outputs from food waste feedstocks, the growing monetization potential of carbon credits, and the significant export potential for European food waste processing technology to emerging markets represent substantial growth opportunities for market participants. Seasonal variability in feedstock composition and availability, persistent public acceptance and NIMBY concerns around processing facility siting, and a growing shortage of skilled workforce capable of operating advanced food waste valorization technologies remain the key challenges facing the industry.

EU Regulatory Framework and Circular Economy Policies Drive Market Transformation

The European food waste recycling market is largely defined by EU legislation that outlines mandatory requirements and provides economic incentives to divert waste from landfills. In particular, the Waste Framework Directive has targets which require member states to recycle 65% municipal waste by 2030 and reduce landfilling to a maximum of 10% by 2035. With fines of EUR 1 million per day for non-compliance, member states are under pressure to develop their organic waste processing infrastructure immediately. The requirement for the mandatory separation of bio-waste by December 2023, impacts 150 million households in the EU, which will increase source-separated food waste collection by 60%. This will also provide recycling facilities with a consistent contamination-free feedstock.

The Renewable Energy Directive (RED III) mandates a minimum target of 42.5% renewable energy in the EU by 2030 and specifies food waste-derived biogas and biomethane as important sources. Biogas and biomethane derived from food waste achieves between 80-90% greenhouse gas savings over natural gas and provides a highly sustainable source of energy. Various regulatory frameworks, converging on biogas and biomethane derived from food waste are emerging around Europe. France’s anti-waste law prohibits food waste from being destroyed, while Italy provides biowaste collection for around 7.1 million tonnes of organic waste each year, and Germany’s cascade utilisation preference encourages full material recovery and utilisation. Under the EU Taxonomy Regulations, recycling food waste is considered a sustainable economic activity, allowing for green financing and capital raising with extralow interest rates, in many cases 1-2% lower. There is anticipation that these combined voting and regulatory frameworks could attract around EUR 20 billion in private sector investment on food waste recycling and food waste related activities by 2030.

Rising Demand for Sustainable Products Creates Market Pull for Food Waste Derivatives

The growing consumer awareness and commitment to corporate sustainability has begun to drive vast demand for food waste products, including fertilizers, biobased surfactants, Biolubricants and biobased plastics and so on, taking food processing waste processors and turning them into sustainable materials & chemicals suppliers. The public would pay 20-30% more for food waste-derived organic fertilizers than conventional fertilizers. Various retailers, including Carrefour, Tesco and REWE have committed to NO food waste sent to landfill (in total they invested EUR 2 billion in recycling infrastructure), providing guaranteed feedstocks through long-term contracts.

The European bioplastics market is expected to reach between 1.5 and 2 million tonnes by 2030, fueling demand for food waste-based bioplastics such as PHA and PLA. Leading global brands like Nestlé and Unilever are actively reducing waste, committing to 100% recyclable or bio-based packaging, and securing offtake agreements worth hundreds of millions of euros annually, including around EUR 500 million per year.

Integrated Biorefinery Models Unlocking High-Value Output from Food Waste Streams

The shift toward integrated biorefinery methods is one of the most significant changes currently affecting the food waste recycling industry in Europe. Unlike traditional recycling methods that produce limited outputs like compost or biogas, biorefineries can convert food waste into a wide variety of products. These include bio based chemicals, bioplastics, enzymes, specialty ingredients, and platform chemicals. This process greatly increases the value gained from each tonne of organic material processed.

Increasing investments in processing technologies and a rising demand for sustainable materials in the chemical, packaging, and pharmaceutical sectors are speeding up the adoption of integrated biorefinery models in Europe. Although these systems are still in the early stages of commercialization, they offer much higher profit margins and greater product variety compared to traditional biological treatment methods. This makes them appealing for future investment, especially as technology improves and production scales up.

This trend fits well with European policy goals in the Circular Economy Action Plan and the EU Bioeconomy Strategy. Both emphasize the high-value use of bio-based waste over lower-end disposal or energy recovery. As a result, biorefinery processing is likely to become a more significant part of the European food waste recycling landscape in the coming years.

Digitalization and AI-Powered Optimization Enhancing Operational Efficiency

The increasing adoption of digital technologies and artificial intelligence across food waste processing operations is emerging as a meaningful trend within the recycling industry in Europe. The facility operators are progressively deploying sensor based monitoring, predictive analytics, and machine learning tools to optimize feedstock intake scheduling, improve process control in anaerobic digestion and composting operations, and enhance output quality consistency. These technologies are helping operators to manage the inherent variability of food waste feedstocks more effectively, reduce operational downtime, and improve overall resource recovery rates.

Furthermore, blockchain based traceability platforms are also gaining traction for certifying the origin, processing pathway, and end use compliance of recycled products such as digestate and compost, providing food manufacturers and agricultural buyers with greater assurance of product safety and regulatory conformity. As European regulations become more stringent and buyers increasingly demand greater transparency across supply chains, digital traceability infrastructure is expected to play a significantly larger role in supporting market access for recycled products.

Biomethane Gaining Commercial Momentum as a Strategically Important Renewable Gas

The commercial development of biomethane as a domestically produced renewable gas is gaining considerable momentum across Europe, driven by the ambitious targets under the revised Renewable Energy Directive in Europe and the broader push to reduce dependence on imported fossil gas. Food waste is one of the most productive feedstocks for biomethane production through anaerobic digestion and gas upgrading, and the combination of guaranteed feed in premiums, renewable gas certification revenues, and carbon savings is significantly improving the investment economy of biomethane projects across the region.

Countries such as Germany, France, Denmark, and the Netherlands have well established biomethane industries, while emerging markets across Southern and Eastern Europe are investing heavily in capacity expansion supported by national renewable energy incentives and EU funding programs. Using biomethane made from food waste in gas grids and as a low emission transport fuel is expanding its commercial use and strengthening its long term importance in the food waste recycling sector.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 5,911.3 Million |

|

Market Size in 2026 |

USD 1,660.3 Million |

|

Revenue Growth Rate (2026–2036) |

CAGR of 13.5% |

|

Dominating Byproduct |

Organic Fertilizers |

|

Fastest Growing Byproduct |

Bioplastics |

|

Dominating Feedstock Source |

Food Processing Industry |

|

Fastest Growing Feedstock Source |

Agricultural Waste & Post-Harvest Losses |

|

Dominating Recycling Method |

Biological Methods |

|

Fastest Growing Recycling Method |

Integrated Biorefinery |

|

Dominating End Use Application |

Agriculture & Horticulture |

|

Fastest Growing End Use Application |

Packaging Industry |

|

Dominating Geography |

Western Europe |

|

Fastest Growing Geography |

Eastern Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on byproduct, the Europe food waste recycling market is segmented into organic fertilizers, biofuels, animal feed, biochemicals and high-value products, and bioplastics. The large share of this segment is mainly attributable to its direct alignment with circular economy principles and widespread applicability in agriculture. A significant portion of food waste is processed through composting and anaerobic digestion, producing compost and digestate that are readily used as soil amendments. The strong policy push under the European Green Deal, Farm to Fork Strategy, and restrictions on synthetic fertilizers have accelerated the adoption of organic fertilizers across the region. Additionally, the well-established infrastructure for composting and biogas plants ensures large-scale conversion of food waste into fertilizers, making this segment both commercially viable and operationally mature.

However, the bioplastics segment is projected to register the highest growth rate during the forecast period. The strong growth of this segment is mainly driven by increasing demand for sustainable alternatives to conventional plastics, rising regulatory pressure to reduce plastic waste, and the growing traction of bio based polymers such as PHA and PLA in packaging applications where single-use plastic regulations are becoming progressively stricter. Rapid advancements in biorefinery technologies, increasing investments in bio-based materials, and growing adoption by packaging and consumer goods industries are further supporting expansion of this segment over the forecast period.

By Feedstock Source: In 2026, the Food Processing Industry Segment to Hold the Largest Share

Based on feedstock source, the Europe food waste recycling market is segmented into the food processing industry, household food waste, food service and hospitality, agricultural waste and post-harvest losses, and retail and supermarkets. The large share of this segment is attributed to the high volume, consistency, and quality of waste generated at centralized facilities. Unlike household or retail waste, food processing waste is typically homogeneous, less contaminated, and produced in large quantities at a single location, making it highly suitable for efficient collection and large-scale recycling processes such as anaerobic digestion, fermentation, and biorefinery applications. The predictable supply and lower handling costs associated with processing waste make this segment the most commercially attractive and operationally efficient feedstock source in the market.

However, the agricultural waste and post-harvest losses segment is projected to register the highest growth rate during the forecast period. The strong growth of this segment is driven by increasing efforts to valorize upstream food losses, improve resource efficiency in agriculture, and capitalize on the significant volume of crop residues, unsold produce, and post-harvest spoilage generated at the primary production stage. Advances in decentralized processing technologies, improved logistics for biomass collection, and growing investments in rural biorefineries are further enabling the conversion of agricultural waste into value-added products.

By Recycling Method: In 2026, the Biological Methods Segment to Account for the Largest Share

Based on recycling method, the Europe food waste recycling market is segmented into biological methods, integrated biorefinery methods, and thermochemical methods. The leading position of this segment attributed to the technological maturity, cost effectiveness, and strong policy alignment of anaerobic digestion and composting processes, which are widely deployed across Europe, supported by well established infrastructure and regulatory backing under the Waste Framework Directive. These methods are highly suitable for handling wet and biodegradable food waste and are relatively simple to operate, scalable, and economically viable, making them the preferred treatment choice for municipalities, food processors, and waste management companies.

However, the integrated biorefinery segment is projected to register the highest growth rate during the forecast period, driven by its ability to generate a wider range of high value products and maximize resource efficiency from food waste feedstocks. Although still at a relatively early stage of commercialization, integrated biorefinery systems offer higher margins and diversification opportunities, and increasing investments in advanced processing technologies and the broader shift toward a circular bioeconomy are expected to increase their adoption during the forecast period.

By End Use Application: In 2026, the Agriculture & Horticulture Segment to Hold the Largest Share

Based on end use application, the Europe food waste recycling market is segmented into agriculture and horticulture, energy generation, animal nutrition, chemical industry, packaging industry, pharma and cosmetics, and other applications. The large share of this segment attributed to the direct and large scale utilization of recycled outputs such as compost and digestate as organic fertilizers and soil conditioners in European farming operations. The strong policy push under the European Green Deal and Farm to Fork Strategy, which promotes sustainable farming and reduced reliance on synthetic fertilizers, has further accelerated demand for organic soil inputs. Furthermore, the agriculture sector offers a stable and high volume outlet for recycled products, making it the most established and commercially viable end-use segment in the market.

However, the packaging industry segment is projected to register the highest growth rate during the forecast period, driven by increasing demand for sustainable and bio based materials as alternatives to conventional plastics, stringent European regulations on single-use plastics, and growing investments by packaging and consumer goods companies in circular materials derived from food waste feedstocks.

Based on geography, the Europe food waste recycling market is assessed across Western Europe, Southern Europe, Northern Europe, and Eastern Europe. The leading position of Western Europe is attributed to the advanced and long established bio waste separate collection infrastructure across Germany, France, the United Kingdom, the Netherlands, Belgium, and Austria; the high density of anaerobic digestion and composting processing facilities serving these markets; and the commercially advanced state of domestic markets for organic fertilizer, biomethane, and food waste derived byproducts. The regulatory maturity of national waste management frameworks in these countries, which have progressively enforced mandatory bio-waste separation and valorization requirements over multiple decades, further underpins Western Europe's market leadership.

However, Eastern Europe is expected to register the highest growth rate during the forecast period. The rapid growth of this region is primarily driven by EU compliance pressure for mandatory bio waste separate collection across Romania, Poland, Hungary, and other member states where collection and processing infrastructure development remains considerably behind the Waste Framework Directive's requirements, creating mandatory investment stimulus for processing capacity development supported by EU cohesion fund co-financing.

The competitive landscape of the Europe food waste recycling market is shaped by the scale of processing capacity, technological capability, geographic coverage, and the ability to generate certified, commercially marketable output products across diverse end use sectors. Companies with vertically integrated operations spanning feedstock collection, processing, and product offtake agreements hold a structural competitive advantage in this market.

Veolia Environment S.A. and SUEZ S.A. maintain leading positions as large scale integrated waste management operators with extensive food waste collection, processing, and valorization capabilities across multiple European geographies. Renewi plc and Biffa plc hold strong regional positions in the Netherlands, Belgium, and the United Kingdom through their well-developed organic waste treatment and resource recovery operations. FCC Environment and PreZero International represent significant players in Southern and Central European markets respectively, with growing investments in biological treatment and energy recovery infrastructure.

In the biogas and biomethane segment, specialized technology companies including BTS Biogas, WELTEC BIOPOWER, EnviTec Biogas, and Xergi A/S are driving innovation in high-performance anaerobic digestion plant design and operation. Nature Energy, now part of Shell, represents a strategically important player in the commercialization of food waste derived biomethane as a grid-injectable renewable gas in Northern Europe. Emerging companies such as Better Origin, Enterra Feed Corporation, and Paques Biomaterials are advancing novel valorization routes including insect protein production and high-value bio-based material extraction.

Some of the key players operating in the Europe food waste recycling market include Veolia Environment S.A. (France), SUEZ S.A. (France), Biffa plc (UK), Renewi plc (Netherlands/UK), FCC Environment (Spain), PreZero International (Germany), Anaergia Inc. (Canada/Italy), BTS Biogas Srl/GmbH (Italy/Germany), WELTEC BIOPOWER GmbH (Germany), EnviTec Biogas AG (Germany), Biogen (UK) Ltd., Agrivert Ltd. (UK), HZI International (Switzerland), Xergi A/S (Denmark), Nature Energy (Shell) (Denmark), Paques Biomaterials B.V. (Netherlands), Better Origin Ltd. (UK), Enterra Feed Corporation (Canada/Europe), and ReFood UK Ltd. (UK/Germany), among others.

The Europe food waste recycling market is expected to reach USD 5,911.3 million by 2036 from an estimated USD 1,660.3 million in 2026, at a CAGR of 13.5% during the forecast period 2026–2036.

In 2026, the organic fertilizers segment is expected to hold the largest share of the Europe food waste recycling market, driven by the widespread use of compost and digestate in European agriculture and strong policy alignment with the European Green Deal and Farm to Fork Strategy.

The bioplastics segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by increasing demand for sustainable packaging materials, stricter single-use plastic regulations across Europe, and the growing adoption of food waste as a feedstock for bio-based polymers such as PHA and PLA.

In 2026, the food processing industry segment is expected to hold the largest share of the Europe food waste recycling market, owing to the high volume, consistency, and commercial suitability of centrally generated processing waste.

In 2026, the biological methods segment is expected to hold the largest share of the Europe food waste recycling market, reflecting the technological maturity and wide deployment of anaerobic digestion and composting processes across the region.

In 2026, the agriculture and horticulture segment is expected to hold the largest share of the Europe food waste recycling market, driven by the large-scale application of compost and digestate as organic soil inputs across European farming.

The growth of this market is primarily driven by mandatory bio-waste separate collection obligations under the revised EU Waste Framework Directive, the European Green Deal's circular economy and climate neutrality commitments, accelerating demand for domestically produced organic fertilizers and biomethane, and the expanding commercial viability of biorefinery-based high-value product recovery from food waste streams.

Key players operating in the Europe food waste recycling market include Veolia Environment S.A. (France), SUEZ S.A. (France), Biffa plc (UK), Renewi plc (Netherlands/UK), FCC Environment (Spain), PreZero International (Germany), Anaergia Inc. (Canada/Italy), BTS Biogas Srl/GmbH (Italy/Germany), WELTEC BIOPOWER GmbH (Germany), EnviTec Biogas AG (Germany), Biogen (UK) Ltd., Agrivert Ltd. (UK), HZI International (Switzerland), Xergi A/S (Denmark), Nature Energy (Shell) (Denmark), Paques Biomaterials B.V. (Netherlands), Better Origin Ltd. (UK), Enterra Feed Corporation (Canada/Europe), and ReFood UK Ltd. (UK/Germany).

Eastern Europe is expected to register the highest growth rate in the Europe food waste recycling market during the forecast period 2026–2036, driven by mandatory EU compliance investment in bio-waste collection and processing infrastructure across Romania, Poland, Hungary, and other member states supported by EU cohesion fund co-financing.

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates