Resources

About Us

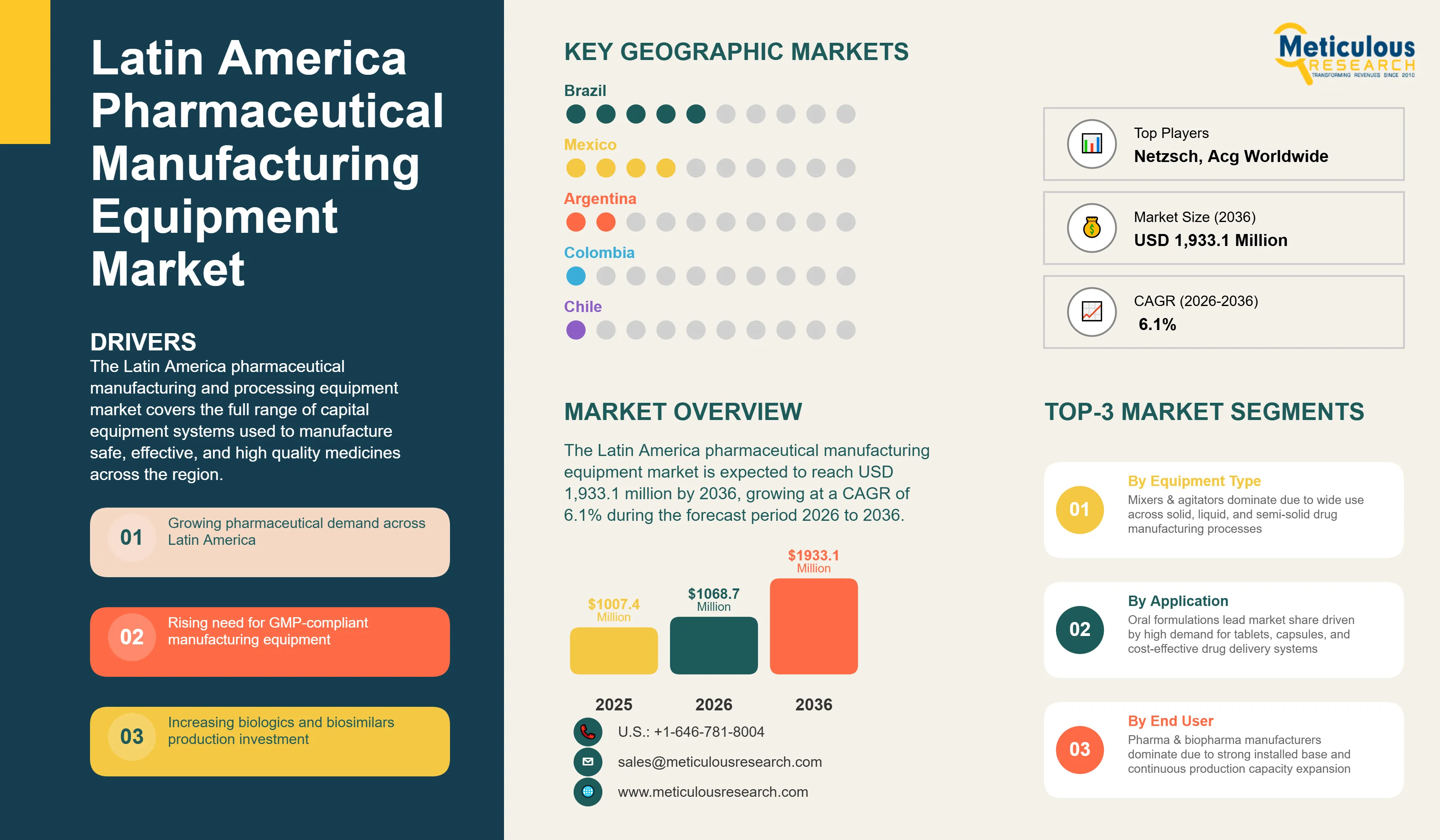

The Latin America pharmaceutical manufacturing equipment market was valued at USD 1,007.4 million in 2025. This market is expected to reach USD 1,933.1 million by 2036 from an estimated USD 1,068.7 million in 2026, growing at a CAGR of 6.1% during the forecast period 2026 to 2036.

Click here to: Get Free Sample Pages of this Report

The Latin America pharmaceutical manufacturing and processing equipment market covers the full range of capital equipment systems used to manufacture safe, effective, and high quality medicines across the region. These include milling equipment, dispersing equipment, homogenizers, mixers and agitators, blending equipment, fluidized bed machines, compression and press equipment, capsule filling equipment, coating equipment, preparation vessels, filtration units, sterilization tunnels, CIP and SIP systems, and aseptic inspection systems deployed across pharmaceutical manufacturers, contract manufacturing organizations, and research institutions throughout Brazil, Mexico, Argentina, Colombia, Chile, Peru, and the broader Latin American region.

The Latin American pharmaceutical manufacturing landscape is characterized by a strong foundation in generic drug production, increasing demand for affordable healthcare, and a gradual but accelerating advancement toward complex formulations including biologics and injectable therapies. As pharmaceutical companies expand their production capabilities to meet growing regional healthcare needs, the demand for advanced, efficient, and GMP compliant manufacturing equipment continues to increase.

The growth of this market is primarily driven by the growing pharmaceuticals market across Latin America, the rising demand for GMP compliant processing equipment to meet ANVISA, COFEPRIS, ANMAT, INVIMA, and DIGEMID regulatory requirements, the growing trend of contract manufacturing in the pharmaceutical sector, and growing investment in biologics and biosimilar manufacturing. Additionally, the USMCA nearshoring trend is driving new pharmaceutical manufacturing investment in Mexico, further propelling market growth.

However, the growth of this market is restrained by the preference for refurbished equipment among smaller regional manufacturers and currency volatility compressing local currency capital equipment budgets, both of which continue to limit the pace of new equipment procurement across certain market segments.

On the other hand, the aseptic injectable and biopharmaceutical manufacturing expansion across Brazil, Mexico, and Argentina, the emergence of pharmaceutical manufacturing hotspots in Colombia, Chile, and Peru, and GMP compliance upgrade cycles driving replacement of aging equipment fleets are expected to generate significant growth opportunities for stakeholders in this market. The limited GMP trained technical workforce outside primary manufacturing hubs and the multi country regulatory complexity across the region remain the major challenges impacting market growth.

Increasing Adoption of Continuous Manufacturing and Process Intensification

Regular adoption of continuous manufacturing technologies alongside process intensification approaches is the major structural shift transforming pharmaceutical manufacturing in Latin America. Traditionally, the region has relied on batch based production models which, despite being well understood and aligned with regulatory frameworks, face inherent challenges related to efficiency, scalability, and real time quality monitoring. Continuous manufacturing helps to overcome these constraints by allowing uninterrupted processing of drug substances and finished products, allowing companies to shorten production cycles, reduce material usage, and deliver more consistent quality through integrated process analytical technologies.

For Latin American manufacturers, this transition carries particular significance in the context of increasing competitive pressure from Asian generic manufacturers and the need to optimize cost structures while simultaneously meeting more stringent international GMP expectations. Leading multinational pharmaceutical companies with regional production facilities in Brazil and Mexico are among the early adopters of this technology, and their investment decisions are beginning to influence broader manufacturing norms across the region. Equipment suppliers are responding by developing modular continuous processing platforms better suited to the mid scale production volumes characteristic of Latin American operations, further supporting adoption.

Rising Focus on Single Use Technologies in Biopharmaceutical Manufacturing

The increasing disposition of single use technologies across biopharmaceutical manufacturing operations represents another important trend shaping equipment procurement patterns in Latin America. As regional manufacturers and contract manufacturing organizations expand their capabilities in biologics, biosimilars, and advanced injectable formulations, the operational and economic advantages of single use bioprocessing systems, including bioreactors, mixing bags, filtration assemblies, and fluid transfer systems, are becoming more widely recognized and adopted. Single use systems eliminate the need for cleaning validation, reduce cross contamination risk, and offer significant flexibility for multi product manufacturing facilities, making them particularly well suited to the contract manufacturing model that is gaining ground across Brazil, Mexico, and Argentina.

The progressive alignment of regional regulatory frameworks with EU GMP Annex 1 sterility requirements and the growing sophistication of ANVISA and COFEPRIS inspection standards are also encouraging manufacturers to invest in more advanced aseptic processing infrastructure, with single use technologies increasingly embedded within these investments. As the regional biologics and biosimilar pipeline deepens over the forecast period, the adoption of single use manufacturing technologies is expected to become more widespread, sustaining a positive demand outlook for the associated equipment categories.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 1,933.1 Million |

|

Market Size in 2026 |

USD 1,068.7 Million |

|

Revenue Growth Rate (2026 to 2036) |

CAGR of 6.1% |

|

Dominating Equipment Type |

Mixers & Agitators |

|

Fastest Growing Equipment Type |

Homogenizers |

|

Dominating Mode of Delivery |

Oral Formulations |

|

Fastest Growing Mode of Delivery |

Parenteral Formulations |

|

Dominating End User |

Pharmaceutical & Biopharmaceutical Manufacturers |

|

Fastest Growing End User |

Contract Manufacturing Organizations (CMOs) |

|

Dominating Country |

Brazil |

|

Fastest Growing Country |

Mexico |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on equipment type, the Latin America pharmaceutical manufacturing equipment industry is segmented into milling equipment, dispersing equipment, homogenizers, mixers and agitators, and other manufacturing equipment. The other manufacturing equipment segment is further sub segmented into blending equipment, fluidized bed machines, compression and press equipment, capsule making equipment, capsule filling equipment, coating equipment, preparation vessels, melting vessels and storage tanks, filtration units, sterilization tunnels, CIP and SIP systems, aseptic inspection systems, and other equipment.

In 2026, the mixers and agitators segment is expected to account for the largest share of the pharmaceutical manufacturing equipment market in Latin America. The large share of this segment is mainly due to their widespread application across multiple stages of drug production, including solid, liquid, and semi solid formulations. These systems are essential for ensuring uniform blending, consistency, and stability of pharmaceutical products, making them indispensable across both generics and specialty drug manufacturing. Their relatively lower cost compared to high end sterile processing equipment and their applicability in large scale batch production further contribute to their dominant adoption across pharmaceutical manufacturers in the region.

However, the homogenizers segment is expected to witness the fastest growth during the forecast period. The high growth of this segment is primarily driven by the increasing shift toward biologics, biosimilars, and injectable drug production across the region. Homogenization plays a critical role in particle size reduction, emulsion stability, and formulation of complex drug products, especially in parenteral and advanced therapies. Rising investments in sterile manufacturing infrastructure, growing adoption of high pressure homogenization technologies, and increasing focus on high value formulations are accelerating demand for homogenizers. Markets such as Mexico and Brazil, which are witnessing growth in export oriented manufacturing and biologics capabilities, are particularly contributing to this trend.

Based on Mode of Delivery, the Latin America pharmaceutical manufacturing equipment industry is segmented into oral formulations, parenteral formulations, topical formulations, and other formulations.

In 2026, the oral formulations segment is expected to account for the largest share of the pharmaceutical manufacturing equipment market in Latin America. The large share of this segment is primarily attributed to the dominance of solid oral dosage forms tablets, capsules, and granules as the most widely prescribed, dispensed, and consumed pharmaceutical product category across all Latin American healthcare systems. Public health programs across Brazil, Mexico, Argentina, Colombia, Chile, and Peru disburse most of their essential medicines budgets through oral solid dosage forms, creating sustained high volume manufacturing requirements that in turn represent the largest installed base of pharmaceutical manufacturing equipment in the region.

However, the parenteral formulations segment is projected to record the highest growth during the forecast period. The growth of this segment is primarily driven by the rapidly expanding production of injectable pharmaceuticals across Latin America, including the increasing manufacture of biosimilars, monoclonal antibodies, vaccines, and sterile injectable generics that require highly specialized and capital intensive aseptic manufacturing equipment. The growing investment in biologics manufacturing infrastructure, the progressive adoption of EU GMP Annex 1 aligned sterility standards by ANVISA, COFEPRIS, and other regional regulators, and the regional expansion of contract manufacturing organizations with sterile manufacturing capabilities are collectively generating the fastest growth in equipment demand within the parenteral formulations segment.

Based on end user, the Latin America pharmaceutical manufacturing equipment industry is segmented into pharmaceutical and biopharmaceutical manufacturers, contract manufacturing organizations, and research and academic institutions.

In 2026, the pharmaceutical and biopharmaceutical manufacturers segment is expected to account for the largest share of the market. The large share of this segment is primarily attributed to the region's extensive installed base of captive pharmaceutical manufacturing capacity across Brazil, Mexico, Argentina, Colombia, Chile, and Peru, where both multinational and domestic manufacturers operate dedicated production facilities spanning solid oral dosage forms, liquid formulations, semi solids, and increasingly sterile and biopharmaceutical products.

However, the contract manufacturing organizations segment is projected to record the highest growth during the forecast period. The growth of this segment is primarily driven by the growing trend of pharmaceutical outsourcing across Latin America, the rapid scale up of CMO capacity to serve both regional domestic demand and North American and European pharmaceutical companies seeking cost competitive manufacturing partners in the USMCA zone and the broader Latin American region. The growing shift of Latin American CMOs toward higher complexity biopharmaceutical and sterile manufacturing is creating demand for particularly capital intensive equipment categories, including aseptic filling lines, lyophilizers, isolators, and bioreactor based upstream processing systems.

Based on geography, the Latin America pharmaceutical manufacturing equipment industry is segmented into Brazil, Mexico, Argentina, Colombia, Chile, Peru, and the Rest of Latin America.

In 2026, Brazil is expected to account for the largest share of the pharmaceutical manufacturing equipment market in Latin America. The large share of Brazil is mainly due to its well established pharmaceutical industry, large domestic demand, and strong government support for local drug production. As the largest pharmaceutical market in the region, Brazil benefits from a robust network of domestic manufacturers, significant public healthcare spending, and regulatory frameworks that encourage local manufacturing. Stringent regulatory standards enforced by ANVISA are driving pharmaceutical companies to upgrade their equipment and comply with international GMP requirements, further supporting sustained demand for advanced manufacturing and processing equipment.

However, Mexico is witnessing the rapid growth in the Latin America pharmaceutical manufacturing equipment space. This growth is primarily driven by its strong position as an export oriented manufacturing hub and increasing contract manufacturing activities. The country's proximity to the United States, favorable trade agreements, and cost advantages have made it an attractive destination for global pharmaceutical companies seeking to outsource production. Regulatory improvements, rising foreign direct investment, and the expansion of pharmaceutical exports are accelerating the adoption of advanced and automated manufacturing equipment in Mexico.

The competition for pharmaceutical manufacturing equipment market in the Latin America is primarily driven by product performance, GMP compliance capabilities, after sales service infrastructure, and the ability to support regional regulatory validation requirements across multiple jurisdictions.

GEA Group Aktiengesellschaft maintains one of the strongest competitive positions in the region, supported by its broad portfolio of processing and filling technologies spanning granulation, drying, tableting, and aseptic filling across multiple pharmaceutical dosage forms. IKA-Werke GmbH & Co. KG and Silverson Machines Ltd. hold strong positions in the dispersing and high shear mixing categories, while NETZSCH Group and Hosokawa Micron Group maintain competitive differentiation through their milling and particle engineering technology portfolios.

Syntegon Technology GmbH and Romaco Group are active across packaging and processing segments, while Fette Compacting GmbH and KORSCH AG serve as key suppliers of tablet compression equipment to the region's oral solid dosage form manufacturers. Indian manufacturers including ACG Worldwide, Cadmach Machinery Company, and Kevin Process Technologies are expanding their footprint in Latin America by offering cost competitive solutions aligned with GMP standards, making them increasingly relevant to mid tier regional manufacturers. Marchesini Group S.p.A. and IDEX Corporation through Quadro Engineering also maintain meaningful market positions through their specialized equipment offerings across packaging and size reduction applications.

The report provides a comprehensive competitive analysis based on an extensive assessment of the leading players' product portfolios, geographic presence, financial strength, and key growth strategies adopted over the last few years.

Some of the key players operating in the Latin America pharmaceutical manufacturing equipment industry include GEA Group Aktiengesellschaft (Germany), IKA-Werke GmbH & Co. KG (Germany), NETZSCH Group (Germany), Silverson Machines Ltd. (U.K.), Hosokawa Micron Group (Japan and Netherlands), IDEX Corporation and Quadro Engineering (U.S. and Canada), Syntegon Technology GmbH (Germany), Romaco Group (Germany), ACG Worldwide (India), Cadmach Machinery Company Private Limited (India), Kevin Process Technologies Private Limited (India), SPX Flow Inc. and APV (U.S.), Fette Compacting GmbH (Germany), KORSCH AG (Germany), Marchesini Group S.p.A. (Italy), Willy A. Bachofen AG (Switzerland), BECOMIX (Germany), and UNIMIX (Germany), among others.

The Latin America pharmaceutical manufacturing equipment market is expected to reach USD 1,933.1 million by 2036 from an estimated USD 1,068.7 million in 2026, at a CAGR of 6.1% during the forecast period 2026 to 2036.

In 2026, the mixers and agitators segment is expected to hold the largest share of the market, driven by the widespread application of these systems across multiple stages of solid, liquid, and semi solid drug production and their critical role in ensuring formulation uniformity and consistency.

The homogenizers segment is expected to register the highest growth during the forecast period 2026 to 2036, driven by the increasing shift toward biologics, biosimilars, and injectable drug production across the region and the growing adoption of high pressure homogenization technologies in sterile manufacturing.

In 2026, the oral formulations segment is expected to hold the largest share of the market, reflecting the structural dominance of solid oral dosage forms across all Latin American healthcare systems and public procurement programs.

In 2026, the pharmaceutical and biopharmaceutical manufacturers segment is expected to hold the largest share of the market, supported by the region's extensive installed base of captive manufacturing capacity spanning generics, specialty, and increasingly biopharmaceutical production.

The growth of this market is primarily driven by the growing pharmaceuticals market across Latin America, the rising demand for GMP-compliant processing equipment to meet ANVISA, COFEPRIS, ANMAT, INVIMA, and DIGEMID regulatory requirements, the growing trend of contract manufacturing in the pharmaceutical sector, accelerating investment in biologics and biosimilar manufacturing, and the USMCA nearshoring trend driving new pharmaceutical manufacturing investment in Mexico.

Key players operating in this market include GEA Group Aktiengesellschaft (Germany), IKA-Werke GmbH & Co. KG (Germany), NETZSCH Group (Germany), Silverson Machines Ltd. (U.K.), Hosokawa Micron Group (Japan and Netherlands), IDEX Corporation and Quadro Engineering (U.S. and Canada), Syntegon Technology GmbH (Germany), Romaco Group (Germany), ACG Worldwide (India), Cadmach Machinery Company Private Limited (India), Kevin Process Technologies Private Limited (India), SPX Flow Inc. and APV (U.S.), Fette Compacting GmbH (Germany), KORSCH AG (Germany), Marchesini Group S.p.A. (Italy), Willy A. Bachofen AG (Switzerland), BECOMIX (Germany), and UNIMIX (Germany).

Mexico is expected to register the highest growth rate in this market during the forecast period 2026 to 2036, driven by its position as an export oriented manufacturing hub, nearshoring driven investment inflows, and the rapid expansion of contract manufacturing operations serving both regional and North American demand.

1. Introduction

1.1. Market Definition & Scope

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions For The Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Surge In Private Capital Investment and Commercial Constellation Revenue Validation

4.2.1.2. Rising Demand For Gmp-Compliant Processing Equipment to Meet Anvisa, Cofepris, Anmat, Invima, and Digemid Requirements Boosting Market Growth

4.2.1.3. Growing Trend Of Contract Manufacturing in The Pharmaceutical Sector Fueling Market Growth

4.2.1.4. Accelerating Investment in Biologics And Biosimilar Manufacturing Propelling Market Growth

4.2.1.5. Usmca Nearshoring Driving New Pharmaceutical Manufacturing Investment In Mexico

4.2.2. Restraints

4.2.2.1. Preference For Refurbished Equipment Among Smaller Regional Manufacturers Limiting Market Growth

4.2.2.2. Currency Volatility Compressing Local-Currency Capital Equipment Budgets Restraining Market Growth

4.2.3. Opportunities

4.2.3.1. Aseptic Injectable and Biopharmaceutical Manufacturing Expansion Across Brazil, Mexico, and Argentina Expected to Generate Growth Opportunities

4.2.3.2. Emerging Pharmaceutical Manufacturing Hotspots In Colombia, Chile, and Peru Expected to Accelerate Market Expansion

4.2.3.3. Gmp Compliance Upgrade Cycles Driving Replacement of Aging Equipment Fleets Expected To Generate Growth Opportunities for Market Players

4.2.4. Challenges

4.2.4.1. Limited Gmp-Trained Technical Workforce Outside Primary Manufacturing Hubs Expected To Remain A Major Challenge for Market Stakeholders

4.2.4.2. Multi-Country Regulatory Complexity Across the Region Impacting Market Growth

4.2.5. Key Trends

4.2.5.1. Increasing Adoption of Continuous Manufacturing And Process Intensification

4.2.5.2. Rising Focus on Single-Use Technologies in Biopharmaceutical Manufacturing

4.3. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.4. Use Cases

4.5. Porter’s Five Forces Analysis

4.5.1. Bargaining Power Of Buyers: Moderate To High

4.5.2. Bargaining Power Of Suppliers: Moderate

4.5.3. Threat Of Substitutes: Low

4.5.4. Threat Of New Entrants: Low To Moderate

4.5.5. Degree Of Competition: High

4.6. Value Chain Analysis

4.7. Regulatory Analysis

4.7.1. Brazil — Anvisa

4.7.2. Mexico — Cofepris

4.7.3. Argentina — Anmat

4.7.4. Colombia — Invima

4.7.5. Chile — Instituto De Salud Pública (Isp)

4.7.6. Peru — Digemid

4.7.7. Rest of Latin America

5. Latin America Pharmaceutical Manufacturing Equipment Market, By Equipment Type

5.1. Overview

5.2. Mixers & Agitators

5.2.1. Planetary Mixers

5.2.2. High-Shear Mixers

5.2.3. Colloid Mills

5.2.4. Agitator-Stirrers

5.3. Homogenizers

5.3.1. High-Pressure Homogenizers

5.3.2. Rotor-Stator Homogenizers

5.3.3. Ultrasonic Homogenizers

5.4. Granulation Equipment

5.4.1. Wet Granulation Equipment

5.4.2. Dry Granulation Equipment

5.5. Milling Equipment

5.5.1. Conical Mills

5.5.2. Hammer Mills

5.5.3. Jet Mills / Micronizers

5.5.4. Bead Mills (Wet Grinding / Nanonization)

5.6. Dispersing Equipment

5.6.1. Rotor-Stator Dispersers

5.6.2. High-Speed Dissolvers / Dispersers

5.6.3. Toothed-Disc Dispersers

5.7. Other Manufacturing Equipment

5.7.1. Blending Equipment

5.7.2. Fluidized Bed Machines

5.7.3. Compression / Press Equipment

5.7.4. Capsule Filling Equipment

5.7.5. Coating Equipment

5.7.6. Preparation Vessels, Melting Vessels, And Storage Tanks

5.7.7. Filtration Units

5.7.8. Sterilization Tunnels

5.7.9. Cip And Sip Systems

5.7.10. Aseptic Inspection Systems

5.7.11. Other Equipment

6. Latin America Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery

6.1. Overview

6.2. Oral Formulations

6.3. Parenteral Formulations

6.4. Topical Formulations

6.5. Other Formulations

7. Latin America Pharmaceutical Manufacturing Equipment Market, By End-User

7.1. Overview

7.2. Pharmaceutical & Biopharmaceutical Manufacturers

7.3. Contract Manufacturing Organizations (Cmos)

7.4. Research & Academic Institutions

8. Latin America Pharmaceutical Manufacturing Equipment Market, By Country

8.1. Overview

8.2. Brazil

8.3. Mexico

8.4. Argentina

8.5. Colombia

8.6. Chile

8.7. Peru

8.8. Rest of Latin America

9. Competitive Landscape

9.1. Introduction

9.2. Competitive Benchmarking

9.3. Competitive Dashboard

9.4. Industry Leaders

9.5. Market Differentiators

9.6. Vanguards

9.7. Emerging Companies

9.8. Market Share/Position Analysis

10. Company Profiles

10.1. Gea Group Aktiengesellschaft

10.1.1. Company Overview

10.1.2. Financial Overview

10.1.3. Product Portfolio

10.1.4. Swot Analysis

10.2. Ika-Werke Gmbh & Co. Kg

10.2.1. Company Overview

10.2.2. Product Portfolio

10.2.3. Swot Analysis

10.3. Netzsch Group

10.3.1. Company Overview

10.3.2. Product Portfolio

10.3.3. Strategic Developments

10.3.4. Swot Analysis

10.4. Silverson Machines Ltd

10.4.1. Company Overview

10.4.2. Product Portfolio

10.4.3. Strategic Developments

10.4.4. Swot Analysis

10.5. Hosokawa Micron Group

10.5.1. Company Overview

10.5.2. Financial Overview

10.5.3. Product Portfolio

10.5.4. Swot Analysis

10.6. Idex Corporation / Quadro Engineering

10.6.1. Company Overview

10.6.2. Financial Overview

10.6.3. Product Portfolio

10.6.4. Swot Analysis

10.7. Syntegon Technology Gmbh

10.7.1. Company Overview

10.7.2. Product Portfolio

10.7.3. Swot Analysis

10.8. Romaco Group

10.8.1. Company Overview

10.8.2. Product Portfolio

10.8.3. Swot Analysis

10.9. Acg Worldwide

10.9.1. Company Overview

10.9.2. Product Portfolio

10.9.3. Swot Analysis

10.10. Cadmach Machinery Company Private Limited

10.10.1. Company Overview

10.10.2. Product Portfolio

10.10.3. Swot Analysis

10.11. Kevin Process Technologies Private Limited

10.11.1. Company Overview

10.11.2. Product Portfolio

10.11.3. Swot Analysis

10.12. Spx Flow, Inc. / Apv

10.12.1. Company Overview

10.12.2. Product Portfolio

10.12.3. Swot Analysis

10.13. Fette Compacting Gmbh

10.13.1. Company Overview

10.13.2. Product Portfolio

10.13.3. Swot Analysis

10.14. Korsch Ag

10.14.1. Company Overview

10.14.2. Product Portfolio

10.14.3. Swot Analysis

10.15. Marchesini Group S.P.A.

10.15.1. Company Overview

10.15.2. Product Portfolio

10.15.3. Swot Analysis

10.16. Wab Group (Willy A. Bachofen Ag)

10.16.1. Company Overview

10.16.2. Product Portfolio

10.16.3. Swot Analysis

10.17. Becomix (A. Berents Gmbh & Co. Kg)

10.17.1. Company Overview

10.17.2. Product Portfolio

10.17.3. Swot Analysis

10.18. Unimix (Ekato Systems Gmbh)

10.18.1. Company Overview

10.18.2. Product Portfolio

10.18.3. Swot Analysis

11. Appendix

11.1. Available Customization

11.2. Related Reports

List Of Tables

Table 1. Latin America Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2026–2036 (USD Million)

Table 2. Latin America Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2026–2036 (USD Million)

Table 3. Latin America Pharmaceutical Manufacturing Mixers & Agitators Market, By Country/Region, 2024–2036 ($ Million)

Table 4. Latin America Pharmaceutical Manufacturing Planetary Mixers Market, By Country/Region, 2024–2036 ($ Million)

Table 5. Latin America Pharmaceutical Manufacturing High-Shear Mixers Market, By Country/Region, 2024–2036 ($ Million)

Table 6. Latin America Pharmaceutical Manufacturing Colloid Mills Market, By Country/Region, 2024–2036 ($ Million)

Table 7. Latin America Pharmaceutical Manufacturing Agitator-Stirrers Market, By Country/Region, 2024–2036 ($ Million)

Table 8. Latin America Pharmaceutical Manufacturing Homogenizers Market, By Type, 2026–2036 (USD Million)

Table 9. Latin America Pharmaceutical Manufacturing Homogenizers Market, By Country/Region, 2024–2036 ($ Million)

Table 10. Latin America Pharmaceutical Manufacturing High-Pressure Homogenizers Market, By Country/Region, 2024–2036 ($ Million)

Table 11. Latin America Pharmaceutical Manufacturing Rotor-Stator Homogenizers Market, By Country/Region, 2024–2036 ($ Million)

Table 12. Latin America Pharmaceutical Manufacturing Ultrasonic Homogenizers Market, By Country/Region, 2024–2036 ($ Million)

Table 13. Latin America Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2026–2036 (USD Million)

Table 14. Latin America Pharmaceutical Manufacturing Granulation Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 15. Latin America Pharmaceutical Manufacturing Wet Granulation Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 16. Latin America Pharmaceutical Manufacturing Dry Granulation Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 17. Latin America Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2026–2036 (USD Million)

Table 18. Latin America Pharmaceutical Manufacturing Milling Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 19. Latin America Pharmaceutical Manufacturing Conical Mills Market, By Country/Region, 2024–2036 ($ Million)

Table 20. Latin America Pharmaceutical Manufacturing Hammer Mills Market, By Country/Region, 2024–2036 ($ Million)

Table 21. Latin America Pharmaceutical Manufacturing Jet Mills / Micronizers Market, By Country/Region, 2024–2036 ($ Million)

Table 22. Latin America Pharmaceutical Manufacturing Bead Mills Market, By Country/Region, 2024–2036 ($ Million)

Table 23. Latin America Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2026–2036 (USD Million)

Table 24. Latin America Pharmaceutical Manufacturing Dispersing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 25. Latin America Pharmaceutical Manufacturing Rotor-Stator Dispersers Market, By Country/Region, 2024–2036 ($ Million)

Table 26. Latin America Pharmaceutical Manufacturing High-Speed Dissolvers Market, By Country/Region, 2024–2036 ($ Million)

Table 27. Latin America Pharmaceutical Manufacturing Toothed-Disc Dispersers Market, By Country/Region, 2024–2036 ($ Million)

Table 28. Latin America Pharmaceutical Manufacturing Other Manufacturing Equipment Market, By Type, 2026–2036 (USD Million)

Table 29. Latin America Pharmaceutical Manufacturing Other Manufacturing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 30. Latin America Pharmaceutical Manufacturing Blending Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 31. Latin America Pharmaceutical Manufacturing Fluidized Bed Machines Market, By Country/Region, 2024–2036 ($ Million)

Table 32. Latin America Pharmaceutical Manufacturing Compression / Press Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 33. Latin America Pharmaceutical Manufacturing Capsule Filling Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 34. Latin America Pharmaceutical Manufacturing Coating Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 35. Latin America Pharmaceutical Manufacturing Vessels & Storage Tanks Market, By Country/Region, 2024–2036 ($ Million)

Table 36. Latin America Pharmaceutical Manufacturing Filtration Units Market, By Country/Region, 2024–2036 ($ Million)

Table 37. Latin America Pharmaceutical Manufacturing Sterilization Tunnels Market, By Country/Region, 2024–2036 ($ Million)

Table 38. Latin America Pharmaceutical Manufacturing Cip/Sip Systems Market, By Country/Region, 2024–2036 ($ Million)

Table 39. Latin America Pharmaceutical Manufacturing Aseptic Inspection Systems Market, By Country/Region, 2024–2036 ($ Million)

Table 40. Latin America Pharmaceutical Manufacturing Other Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 41. Latin America Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2026–2036 (USD Million)

Table 42. Latin America Oral Formulations Pharmaceutical Manufacturing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 43. Latin America Parenteral Formulations Pharmaceutical Manufacturing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 44. Latin America Topical Formulations Pharmaceutical Manufacturing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 45. Latin America Other Formulations Pharmaceutical Manufacturing Equipment Market, By Country/Region, 2024–2036 ($ Million)

Table 46. Latin America Pharmaceutical Manufacturing Equipment Market, By End User, 2026–2036 (USD Million)

Table 47. Latin America Pharmaceutical Manufacturing Equipment Market For Pharmaceutical & Biopharmaceutical Manufacturers, By Country/Region, 2024–2036 ($ Million)

Table 48. Latin America Pharmaceutical Manufacturing Equipment Market For Contract Manufacturing Organizations (Cmos), By Country/Region, 2024–2036 ($ Million)

Table 49. Latin America Pharmaceutical Manufacturing Equipment Market For Research & Academic Institutions, By Country/Region, 2024–2036 ($ Million)

Table 50. Latin America Pharmaceutical Manufacturing Equipment Market, By Country, 2024–2036 (USD Million)

Table 51. Brazil: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 52. Brazil: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 53. Brazil: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 54. Brazil: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 55. Brazil: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 56. Brazil: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 57. Brazil: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 58. Brazil: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 59. Brazil: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 60. Mexico: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 61. Mexico: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 62. Mexico: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 63. Mexico: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 64. Mexico: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 65. Mexico: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 66. Mexico: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 67. Mexico: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 68. Mexico: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 69. Argentina: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 70. Argentina: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 71. Argentina: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 72. Argentina: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 73. Argentina: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 74. Argentina: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 75. Argentina: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 76. Argentina: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 77. Argentina: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 78. Colombia: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 79. Colombia: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 80. Colombia: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 81. Colombia: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 82. Colombia: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 83. Colombia: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 84. Colombia: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 85. Colombia: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 86. Colombia: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 87. Chile: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 88. Chile: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 89. Chile: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 90. Chile: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 91. Chile: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 92. Chile: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 93. Chile: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 94. Chile: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 95. Chile: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 96. Peru: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 97. Peru: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 98. Peru: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 99. Peru: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 100. Peru: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 101. Peru: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 102. Peru: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 103. Peru: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 104. Peru: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

Table 105. Rest of Latin America: Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2024–2036 (USD Million)

Table 106. Rest of Latin America: Pharmaceutical Manufacturing Mixers & Agitators Market, By Type, 2024–2036 (USD Million)

Table 107. Rest of Latin America: Pharmaceutical Manufacturing Homogenizers Market, By Type, 2024–2036 (USD Million)

Table 108. Rest of Latin America: Pharmaceutical Manufacturing Granulation Equipment Market, By Type, 2024–2036 (USD Million)

Table 109. Rest of Latin America: Pharmaceutical Manufacturing Milling Equipment Market, By Type, 2024–2036 (USD Million)

Table 110. Rest of Latin America: Pharmaceutical Manufacturing Dispersing Equipment Market, By Type, 2024–2036 (USD Million)

Table 111. Rest of Latin America: Pharmaceutical Other Manufacturing Equipment Market, By Type, 2024–2036 (USD Million)

Table 112. Rest of Latin America: Pharmaceutical Manufacturing Equipment Market, By Mode of Delivery, 2024–2036 (USD Million)

Table 113. Rest of Latin America: Pharmaceutical Manufacturing Equipment Market, By End User, 2024–2036 (USD Million)

List of Figures

Figure 1. Research Process

Figure 2. Key Secondary Sources

Figure 3. Primary Research Techniques

Figure 4. Key Executives Interviewed

Figure 5. Breakdown of Primary Interviews (Supply-Side & Demand-Side)

Figure 6. Market Sizing And Growth Forecast Approach

Figure 7. Latin America Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2026 Vs. 2036 (Usd Million)

Figure 8. Latin America Pharmaceutical Manufacturing Equipment Market, By Mode Of Delivery, 2026 Vs. 2036 (Usd Million)

Figure 9. Latin America Pharmaceutical Manufacturing Equipment Market, By End User, 2025 Vs. 2035 (Usd Million)

Figure 10. Latin America Pharmaceutical Manufacturing Equipment Market, By Geography, 2026 Vs. 2036 (Usd Million)

Figure 11. Market Dynamics: Drivers, Restraints, Opportunities, And Challenges

Figure 12. Latin America Pharmaceutical Manufacturing Equipment Market, By Equipment Type, 2026 Vs. 2036 (Usd Million)

Figure 13. Latin America Pharmaceutical Manufacturing Equipment Market, By Mode Of Delivery, 2026 Vs. 2036 (Usd Million)

Figure 14. Latin America Pharmaceutical Manufacturing Equipment Market, By End-User, 2026 Vs. 2036 (Usd Million)

Figure 15. Latin America Pharmaceutical Manufacturing Equipment Market, By Region, 2026 Vs. 2036 (Usd Million)

Figure 16. Latin America Pharmaceutical Manufacturing Equipment: Competitive Benchmarking, By Region

Figure 17. Competitive Dashboard: Latin America Pharmaceutical Manufacturing Equipment Market

Figure 18. Latin America Pharmaceutical Manufacturing Equipment Market Position Analysis, 2025

Figure 19. Gea Group Aktiengesellschaft: Financial Overview (2025)

Figure 20. Hosokawa Micron Group: Financial Overview (2025)

Figure 21. Idex Corporation: Financial Overview (2025)

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jul-2023

Subscribe to get the latest industry updates